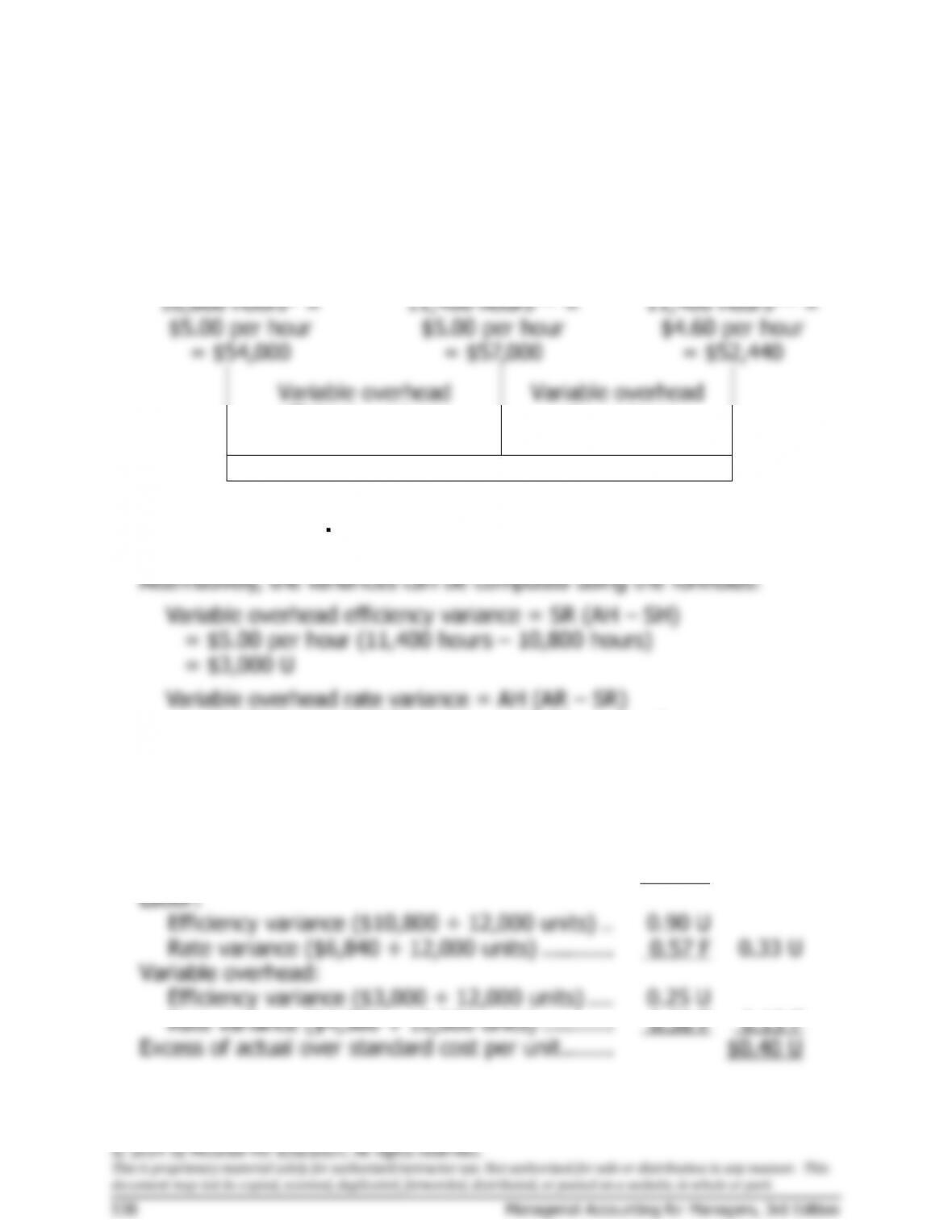

Problem 11–10 (continued)

Note that all of the price variance is due to the hospital’s 4% quantity

discount. Also note that the $8,000 quantity variance for the month is

equal to nearly 30% of the standard cost allowed for plates. This

variance may be the result of using too many assistants in the lab.

Problem 11–10 (continued)

2. b. The policy probably should not be continued. Although the hospital is

saving $1.75 per hour by employing more assistants relative to the

number of senior technicians than other hospitals, this savings is

more than offset by other factors. Too much time is being taken in

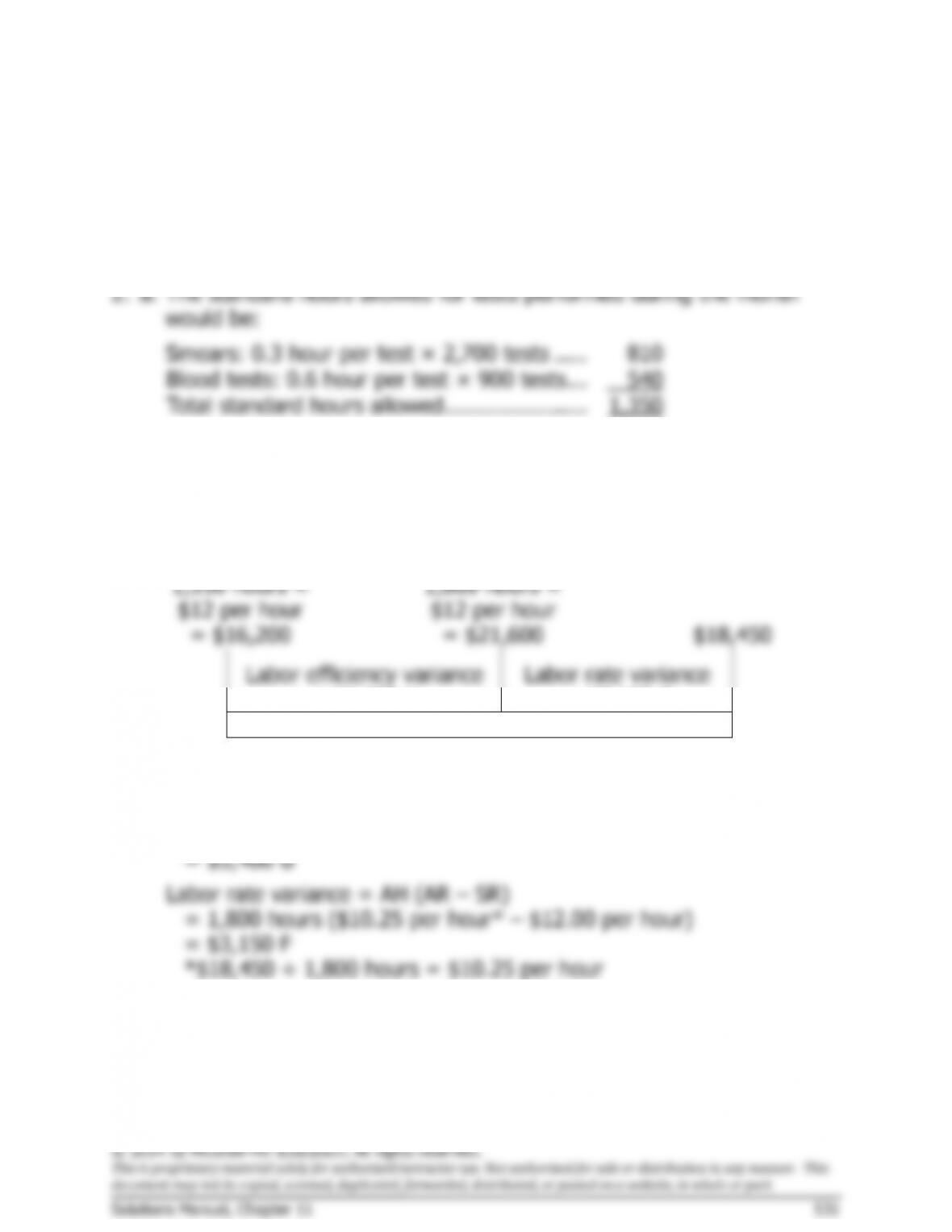

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

1,350 hours ×

$6.00 per hour

= $8,100

1,800 hours ×

$6.00 per hour

= $10,800

$11,700

Variable overhead

efficiency variance

= $2,700 U

Variable overhead

rate variance

= $900 U

Spending variance = $3,600 U

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

= $6 per hour (1,800 hours – 1,350 hours)

Yes, the two variances are related. Both are computed by comparing

Problem 11–13 (45 minutes)

1. a. Materials price variance = AQ (AP – SP)

6,000 pounds ($2.75 per pound* – SP) = $1,500 F**

$16,500 – 6,000 pounds × SP = $1,500***

6,000 pounds × SP = $18,000