Chapter 11

Standard Costs and Variances

Solutions to Questions

11-1 A quantity standard indicates how much

11-2 Ideal standards assume perfection and

do not allow for any inefficiency. Ideal standards

normal breaks and work interruptions.

11-3 Under management by exception,

investigation.

variances are usually the responsibilities of

different managers.

variances are usually the responsibility of

production managers and supervisors.

usually better to compute the variance when

materials are purchased because that is when

materials are purchased allows the company to

carry its raw materials in the inventory accounts

at standard cost, which greatly simplifies

11-7 This combination of variances may

11-8 If standards are used to find who to

blame for problems, they can breed resentment

11-9 Several factors other than the

contractual rate paid to workers can cause a

labor rate variance. For example, skilled workers

variance. Or unskilled or untrained workers can

be assigned to tasks that should be filled by

overtime work at premium rates.

11–10 If poor quality materials create

not ordinarily affect the labor rate variance.

11-11 If overhead is applied on the basis of

together. Both variances are computed by

comparing the number of direct labor-hours

Only the “SR” part of the formula, the standard

rate, differs between the two variances.

© 2014 by McGraw-Hill Education. All rights reserved.

This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This

document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

512 Managerial Accounting for Managers, 3rd Edition

those limits are considered to be normal. Any

variances falling outside of those limits are

considered abnormal and are investigated.

11–13 If labor is a fixed cost and standards are

tight, then the only way to generate favorable

unable to process all of the work in process. In

general, if every workstation is attempting to

produce at capacity, then work in process

inventory will build up in front of the

workstations with the least capacity.

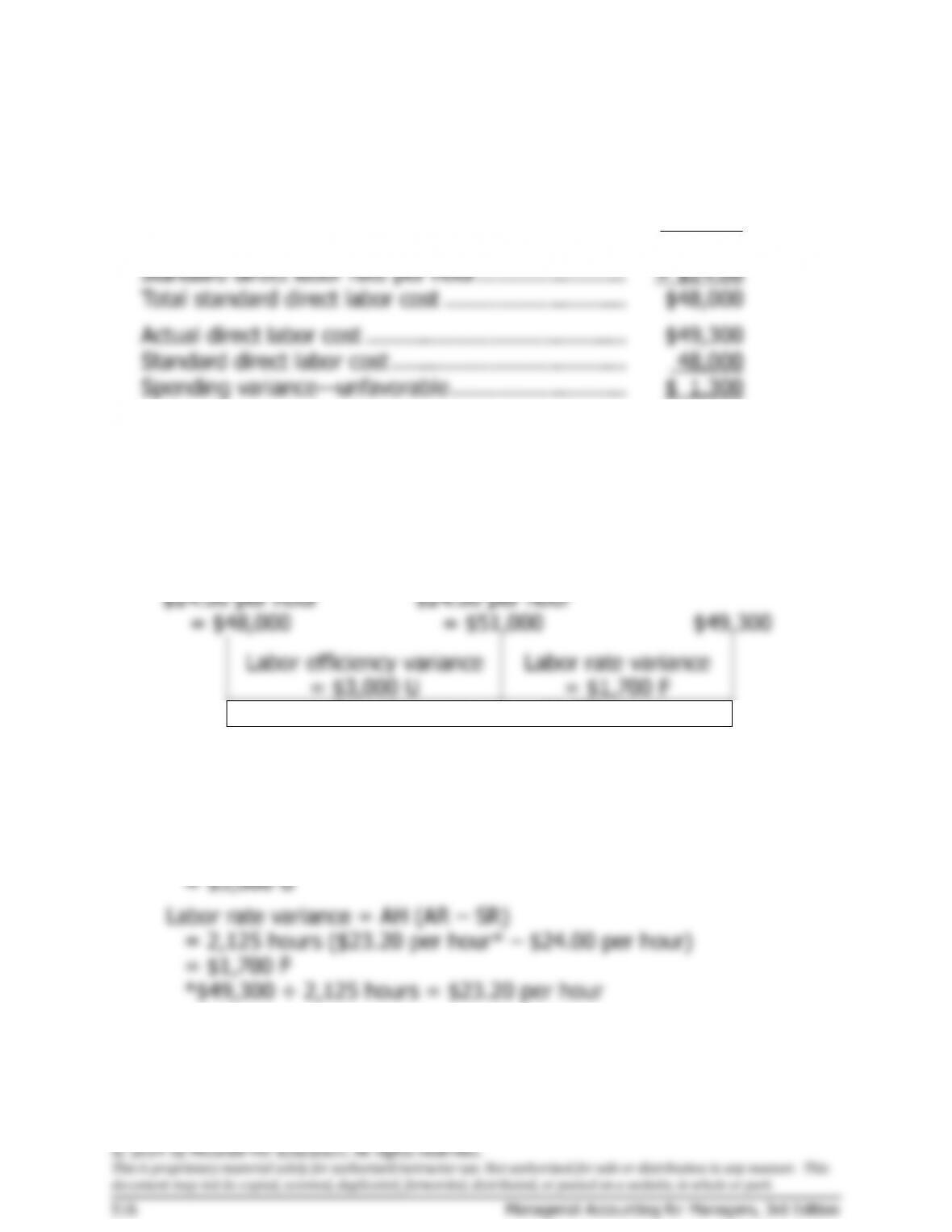

Exercise 11-4 (continued)

3.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

2,000 hours ×

$16.00 per hour

= $32,000

2,125 hours ×

$16.00 per hour

= $34,000

$39,100

Variable overhead

efficiency variance

= $2,000 U

Variable overhead

rate variance

= $5,100 U

Spending variance = $7,100 U

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

=$16.00 per hour (2,125 hours – 2,000 hours)

= $2,000 U

Variable overhead rate variance = AH (AR – SR)

= 2,125 hours ($18.40 per hour* – $16.00 per hour)

= $5,100 U

*$39,100 ÷ 2,125 hours = $18.40 per hour