Chapter 10 – Liabilities

CHAPTER 10 NAME #

10-MINUTE QUIZ B SECTION

Shown below is a summary of the annual payroll data of Rose Co.:

Wages and salaries expense (gross pay)

$2,250,000

Amounts withheld from employees’ pay:

Income taxes …………………………………………………..

$170,000

Social Security and Medicare …………………………...

$150,000

320,000

Payroll taxes expense:

Social Security and Medicare …………………………...

$150,000

Unemployment taxes ……………………………………….

58,000

208,000

Workers’ compensation premiums …………………………….

130,000

Group health insurance premiums (paid by employer)

252,000

Contributions to employees’ pension plan (paid by

employer and fully funded) ………………………………

140,000

Cost of other postretirement benefits:

Funded ……………………………………………………………

$90,000

Unfunded …………………………..…………………………...

120,000

210,000

1 Refer to the above data. Rose Company’s total payroll–related expense for the year is:

a $2,250,000. b $3,510,000. c $2,840,000. d $3,190,000.

2 Refer to the above data. Compute the company’s cash outlays during the year for

payroll-related costs. Assume short-term obligations such as insurance premiums and

payroll taxes have been paid.

a $2,750,000. b $3,070,000. c $1,930,000. d $3,510,000.

3 Refer to the above data. The annual ”take–home-pay” of Rose’ employees is:

a $2,520,000. b $2,250,000. c $1,930,000. d $2,750,000.

4 Refer to the above data Amounts paid during the year to retirees for pension and other

postretirement benefits total:

a $140,000. b $350,000. c $230,000. d None of above.

5 Refer to the above data. When a company has a fully-funded pension plan:

a The dollar amounts paid to retirees are greater than the amounts recognized as

pension expense by the employer.

b Pension expense is equal to the cash payments made to retirees during the current

period.

c No pension expense is recognized in the income statement.

d It does not use the services of a trustee to operate the pension plan.

Chapter 10 – Liabilities

Financial and Managerial Accounting, 17e 10-9

CHAPTER 10 NAME #

10-MINUTE QUIZ C SECTION

Seaview Industries received authorization on December 31, Year 1, to issue $7,000,000 face value of 6%,

10–year bonds. The interest payment dates are June 30 and December 31. All the bonds were issued at par,

plus accrued interest, April 1, Year 2. The bonds are callable by Seaview Industries at any time at 102.

1 Prepare the journal entry to record issuance of the bonds on April 1, Year 2.

2 Prepare the journal entry to record the first semiannual interest payment on the bonds at June 30,

Year 2.

3 What is the amount of bond interest expense that appears in Seaview’s Year 2 income statement

relating to these bonds?

$_________________________

4 What is the amount of accrued bond interest expense that appears in Seaview’s balance sheet at

December 31, Year 2, with respect to these bonds?

$_________________________

5 Seaview exercises the call provision and retires one-half of the bond issue on July, 1, Year 4.

Prepare the journal entry to record this transaction on July 1, Year 4.

Chapter 10 – Liabilities

CHAPTER 10 NAME #

10-MINUTE QUIZ D SECTION

On December 1, 2009, Fisher Corporation incurs a 30-year, $400,000 mortgage liability upon

purchase of a warehouse. This mortgage is payable in monthly installments of $4,116, which include

interest computed at the rate of 12% per year. The first monthly payment is made on December 31,

2009.

1 How much of the first payment made on December 31, 2009, is allocated to repayment of principal?

$________

2 What is the total liability related to this mortgage to be reported in Fisher’s balance sheet at December

31, 2009? (Do not separate into current and long-term portions.)

$________

3 The portion of the second monthly payment made on January 31, 2010, which represents interest

expense is: $________

4 What is the aggregate amount paid by Fisher over the 30-year life of the mortgage?

$________

5 Over the 30–year life of the mortgage, the total amount Fisher will pay for interest charges is

$________

Chapter 10 – Liabilities

Financial and Managerial Accounting, 17e 10–11

SOLUTIONS TO CHAPTER 10 10-MINUTE QUIZZES

QUIZ A QUIZ B

QUIZ C

1

Cash …………………………………………………………………………………….. 7,105,000

Bonds Payable ………………………………………………………………….. 7,000,000

Bond Interest Payable ……………………………………………………….. 105,000

Issued $7,000,000 face value bonds at par,

plus three months’ accrued interest.

($7,000,000 x 6% x 3/12 = $105,000)

3

Chapter 10 – Liabilities

QUIZ D

Chapter 10 – Liabilities

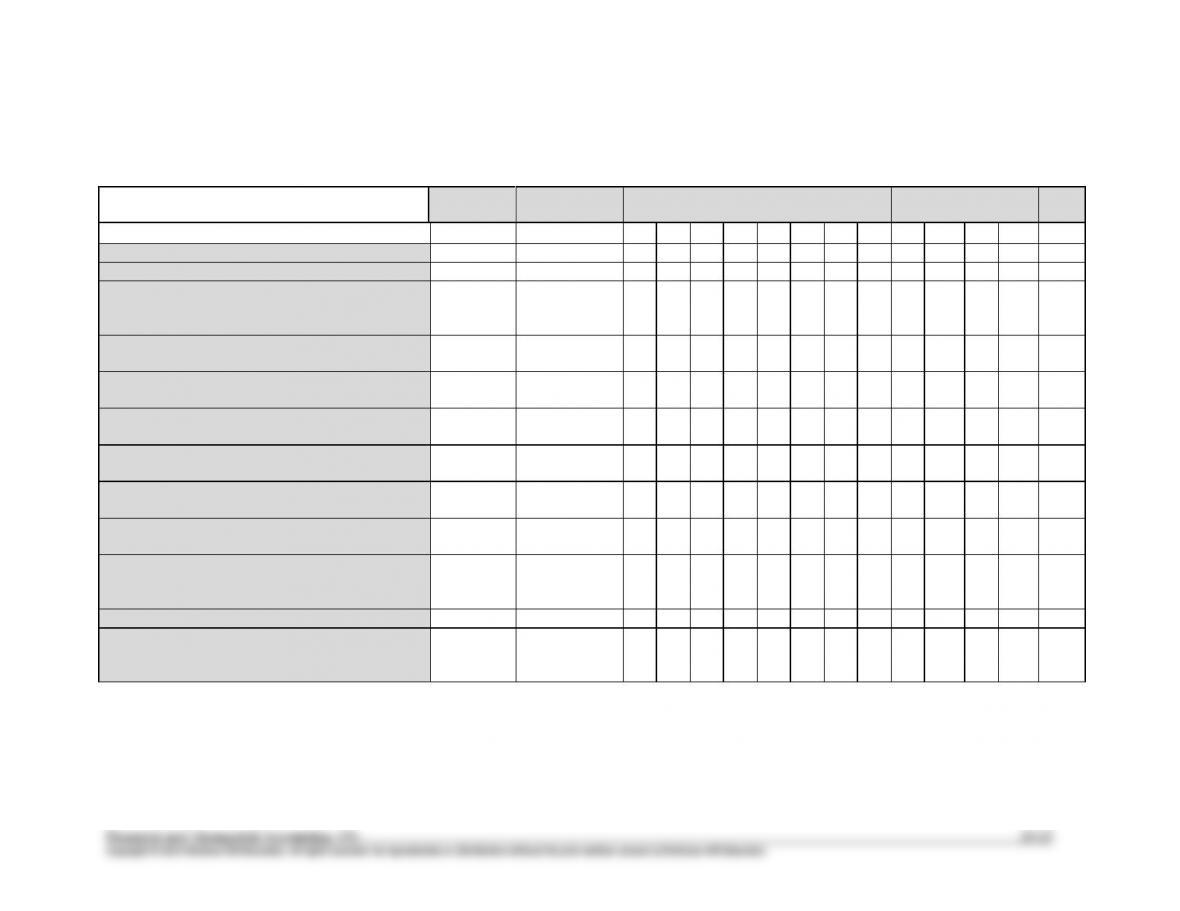

Assignment Guide to Chapter 10

Brief

Exercises

Exercises

Problems

Cases

Net

1-10

1-15

1

2

3

4

5

6

7

8

1

2

3

4

5

Time estimate (in minutes)

<15

<15

40

40

25

30

30

30

40

40

30

20

25

20

20

Difficulty rating

E

E

M

M

S

M

M

M

M

M

M

S

M

M

S

Learning Objectives:

2, 3

√

√

1. Define liabilities and distinguish between

current and long-term liabilities.

2. Account for notes payable and interest

expense.

1

2, 3

3. Describe the costs and the basic

accounting activities relating to payrolls.

2, 4, 5

4. Prepare an amortization table allocating

payments between interest and principal.

1, 2, 3, 6

5. Describe corporate bonds and explain

the tax advantage of debt financing.

2

2, 3, 7, 8, 9, 10

√

√

6. Account for bonds issued at a discount

or premium.

3, 4, 5, 6, 8

2, 3, 9, 10

√

√

7. Explain the concept of present value as it

relates to bond prices.

8. Explain how estimated liabilities, loss

contingencies, and commitments are

disclosed in financial statements.

3

9. Evaluate the safety of creditors’ claims.

7

11, 15

10.

Describe reporting issues related to

leases, postretirement benefits, and

deferred taxes.

9, 10

12, 13, 14