Case 4-25 (continued)

However, use of a plantwide overhead rate in effect redistributes

overhead costs proportionately between the three departments (at

160% of direct labor cost) and results in a large amount of overhead

cost being charged to the Hastings job, as shown in Part 1. This may

labor in the Cutting or Machining Departments. The reason is that the

plantwide overhead rate (160%) is much lower than the rates if these

departments were considered separately.

4. The company’s bid price was:

Direct materials ……………………………………….

$ 18,500

Direct labor …………………………………………….

21,200

Manufacturing overhead applied (above) ………

33,920

Total manufacturing cost …………………………..

73,620

Bidding rate ……………………………………………

× 1.5

Total bid price …………………………………………

$110,430

If departmental overhead rates had been used, the bid price would have

been:

Direct materials ……………………………………….

$ 18,500

Direct labor …………………………………………….

21,200

Manufacturing overhead applied (above) ………

21,750

Total manufacturing cost …………………………..

61,450

Bidding rate ……………………………………………

× 1.5

Total bid price …………………………………………

$ 92,175

Note that if departmental overhead rates had been used, Lenko

Products would have been the low bidder on the Hastings job since the

competitor underbid Lenko by only $10,000.

Case 4-25 (continued)

5. a.

Actual overhead cost …………………………………

$1,482,000

Applied overhead cost ($870,000 × 160%) …….

1,392,000

Underapplied overhead cost ………………………..

$ 90,000

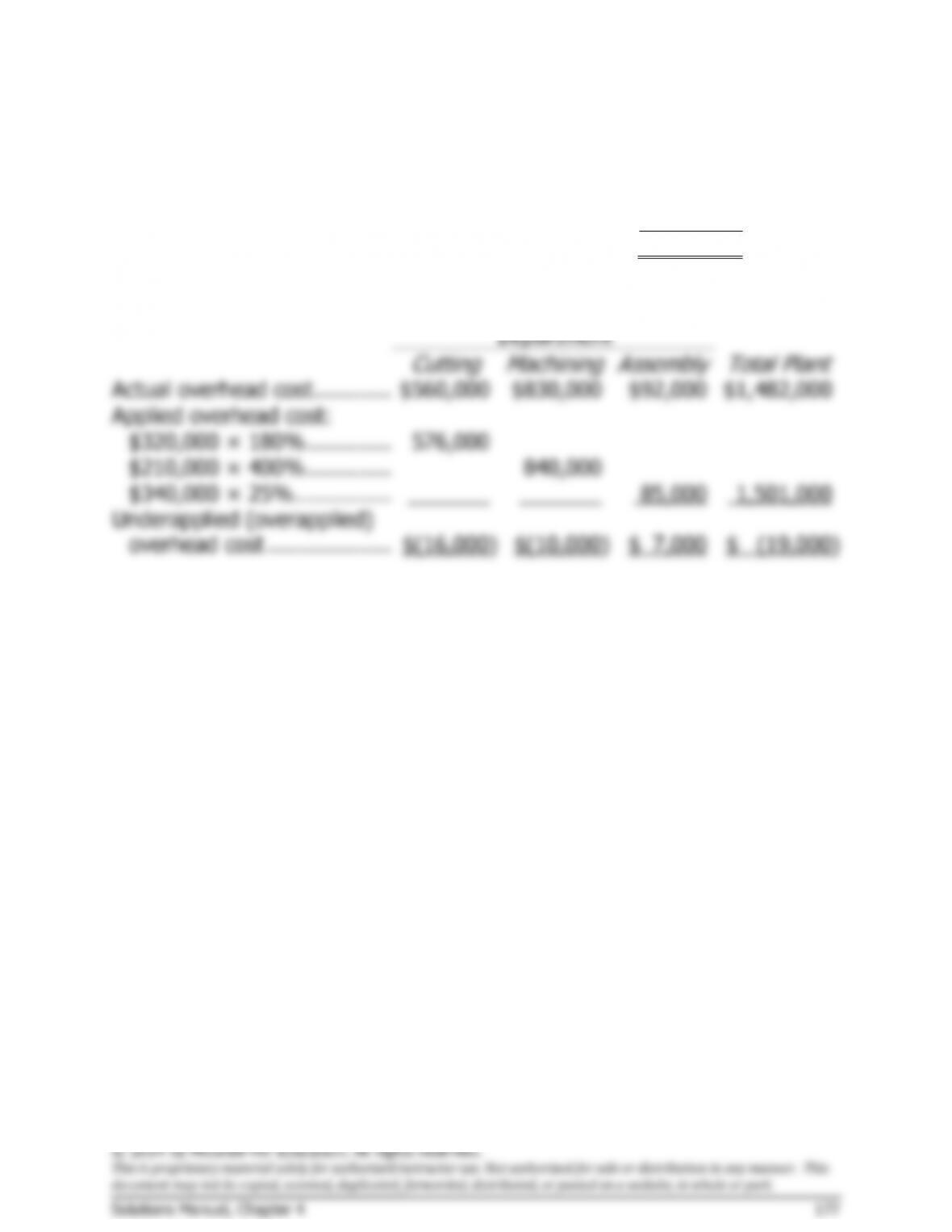

b.

Department

Cutting

Machining

Assembly

Total Plant

Actual overhead cost …………

$560,000

$830,000

$92,000

$1,482,000

Applied overhead cost:

$320,000 × 180% ………….

576,000

$210,000 × 400% ………….

840,000

$340,000 × 25% ……………

85,000

1,501,000

Underapplied (overapplied)

overhead cost ……………….

$(16,000)

$(10,000)

$ 7,000

$ (19,000)

Case 4-27 (continued)

4. While it may have been a good idea to acquire the new equipment

because of its greater capabilities, the calculations of the cost savings

were in error. The original calculations implicitly assumed that overhead

would decrease because of the reduction in direct labor-hours. In

Cost consequences of leasing the automated equipment:

Increase in manufacturing overhead cost:

Lease cost of the new machine …………………………….

$300,000

Cost of new technician/programmer ………………………

45,000

345,000

Deduct: labor cost savings (2,000 hours × $30 per

hour) .……………………………………………………………..

60,000

Net increase in annual costs ……………………………..……

$285,000

Even if the entire 6,000-hour reduction in direct labor-hours occurred,

that would have added only $120,000 (4,000 hours × $30 per hour) in

cost savings. The net increase in annual costs would have been

$165,000 and the machine would still be an unattractive proposal. The

entire 6,000-hour reduction may ultimately be realized as workers retire

or quit. However, this is by no means automatic.

There are two morals to this tale. First, predetermined overhead rates

reduce the direct labor force and may be virtually impossible in some

© 2014 by McGraw-Hill Education. All rights reserved.

This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This

document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

182 Managerial Accounting for Managers, 3rd Edition

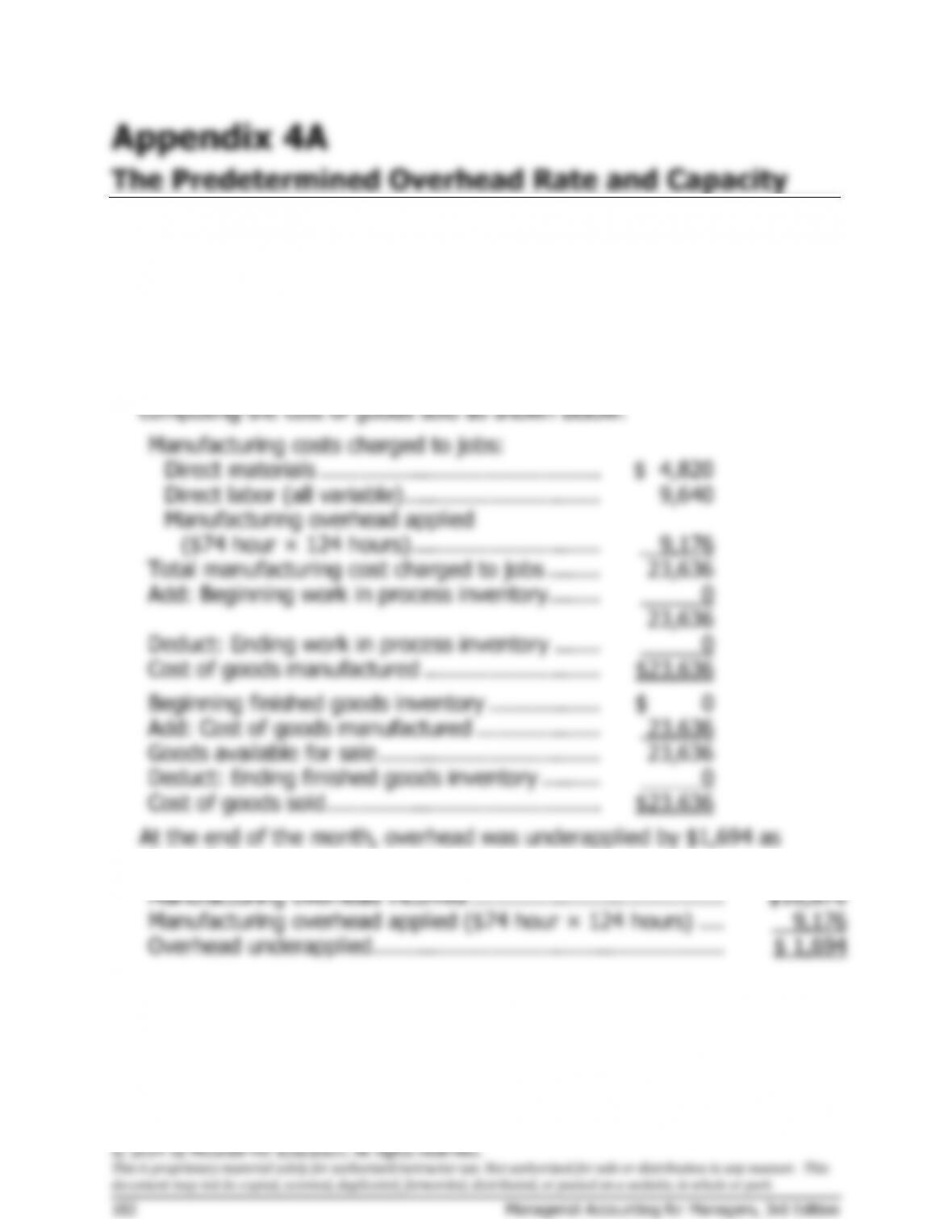

Exercise 4A-1 (30 minutes)

1. There were no beginning or ending inventories, so all of the jobs were

started, finished, and sold during the month. Therefore cost of goods

sold equals the total manufacturing cost. We can verify that by

Manufacturing costs charged to jobs:

Add: Beginning work in process inventory ……..

shown below:

Manufacturing overhead incurred …………………………………

$10,870

Manufacturing overhead applied ($74 hour × 124 hours) ….

9,176

Overhead underapplied………………………………………………

$ 1,694