Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 3

Cost-Volume-Profit Relationships

Solutions to Questions

3-1 The contribution margin (CM) ratio is

estimate the effect on profits of a change in

sales revenue.

3-3 All other things equal, Company B, with

its higher fixed costs and lower variable costs,

profits when sales increase.

3-4 Operating leverage measures the impact

dividing the contribution margin at that level of

sales by the net operating income at that level

sales at which profits are zero.

3-6 (a) If the selling price decreased, then

increased, then both the fixed cost line and the

cost line would rise more steeply and the break-

even point would occur at a higher unit volume.

can drop before losses begin to be incurred.

3-8 The sales mix is the relative proportions

3-9 A higher break-even point and a lower

net operating income could result if the sales

contribution margin ratio in the company to

decline, resulting in less total contribution

would be higher because more sales would be

required to cover the same amount of fixed

costs.

Exercise 3-1 (continued)

3. The new income statement would be:

Total

Per Unit

Sales (7,000 units) .......

$182,000

$26.00

Variable expenses ........

126,000

18.00

Contribution margin ......

56,000

$ 8.00

Fixed expenses ............

56,000

Net operating income ...

$ 0

Note: This is the company's break-even point.

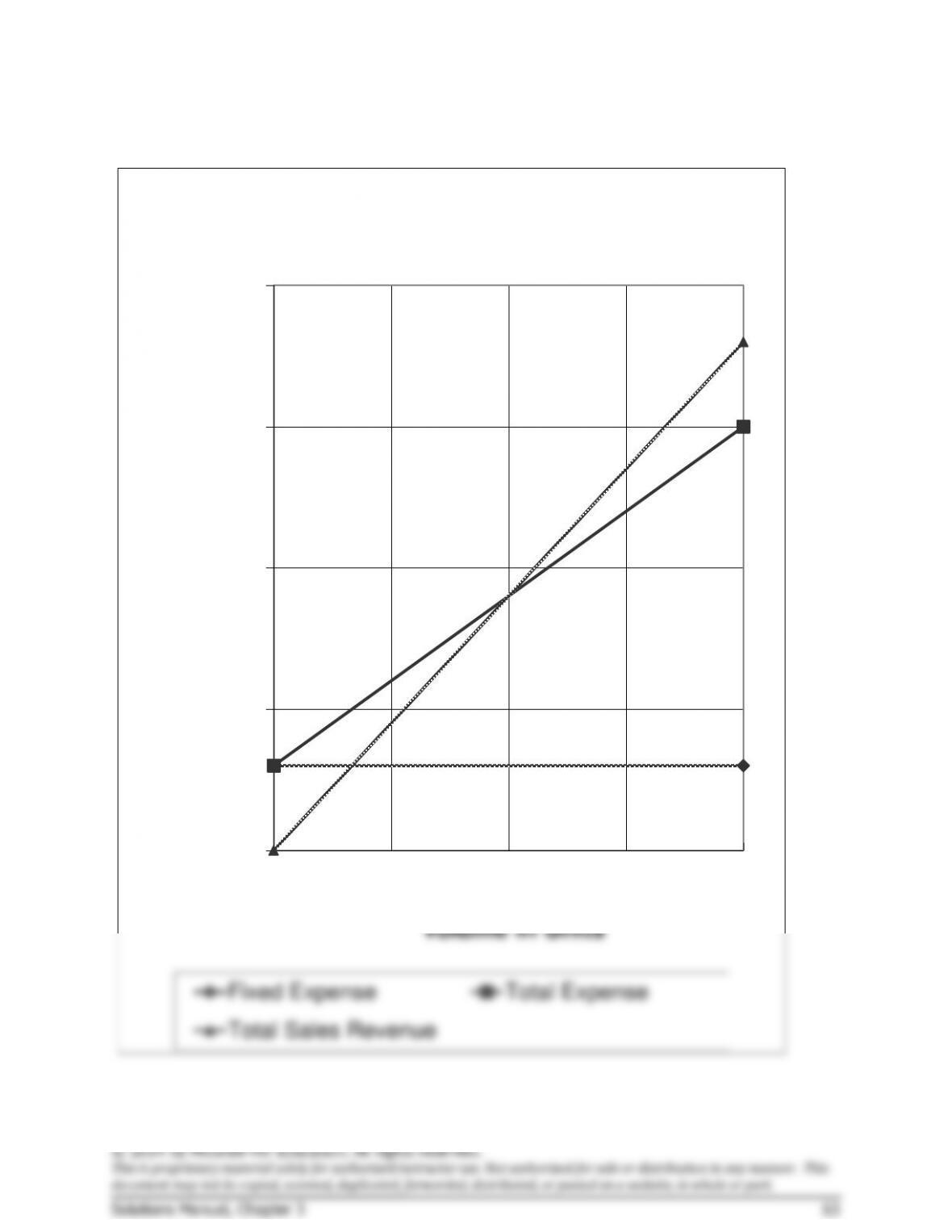

Exercise 3-2 (continued)

$0

$20,000

$40,000

$60,000

$80,000

0500 1,000 1,500 2,000

Dollars

Volume in Units

CVP Graph

Fixed Expense Total Expense

Total Sales Revenue

Exercise 3-3 (continued)

2. Looking at the graph, the break-even point appears to be 3,000 units.

Exercise 3-5 (20 minutes)

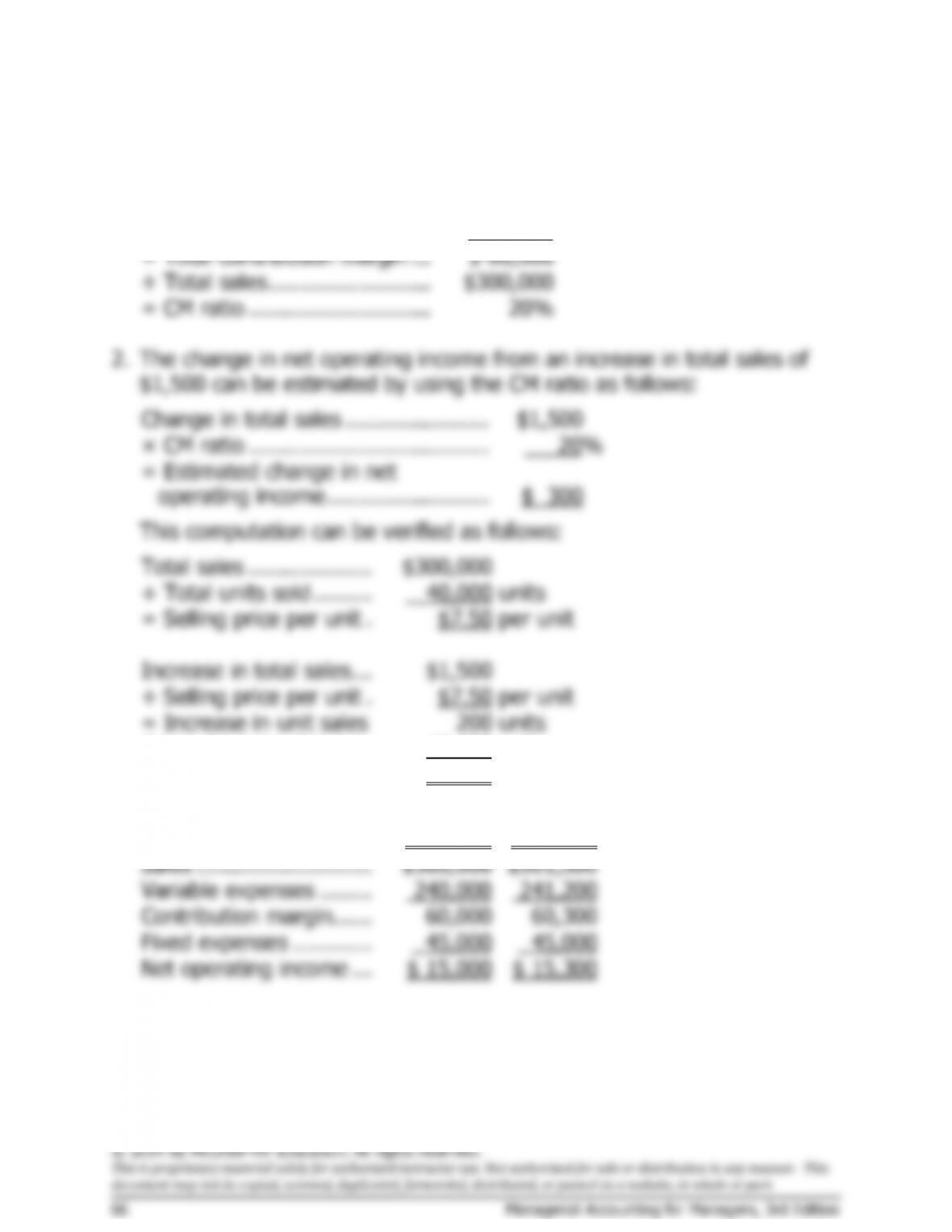

1. The following table shows the effect of the proposed change in monthly

advertising budget:

Sales With

Additional

Current

Advertising

Sales

Budget

Difference

Sales ...........................

$225,000

$240,000

$15,000

Variable expenses ........

135,000

144,000

9,000

Contribution margin ......

90,000

96,000

6,000

Fixed expenses ............

75,000

83,000

8,000

Net operating income ...

$ 15,000

$ 13,000

$(2,000)

Assuming that there are no other important factors to be considered,

the increase in the advertising budget should not be approved because

it would lead to a decrease in net operating income of $2,000.

Alternative Solution 1

Expected total contribution margin:

$240,000 × 40% CM ratio ..................

$96,000

Present total contribution margin:

$225,000 × 40% CM ratio ..................

90,000

Incremental contribution margin ...........

6,000

Change in fixed expenses:

Less incremental advertising expense .

8,000

Change in net operating income ............

$(2,000)