Exercise 3-13 (30 minutes)

1. The contribution margin per person would be:

Price per ticket …………………………………………..

$30

Variable expenses:

Dinner ……………………………………………………

$7

Favors and program ………………………………….

3

10

Contribution margin per person ……………………..

$20

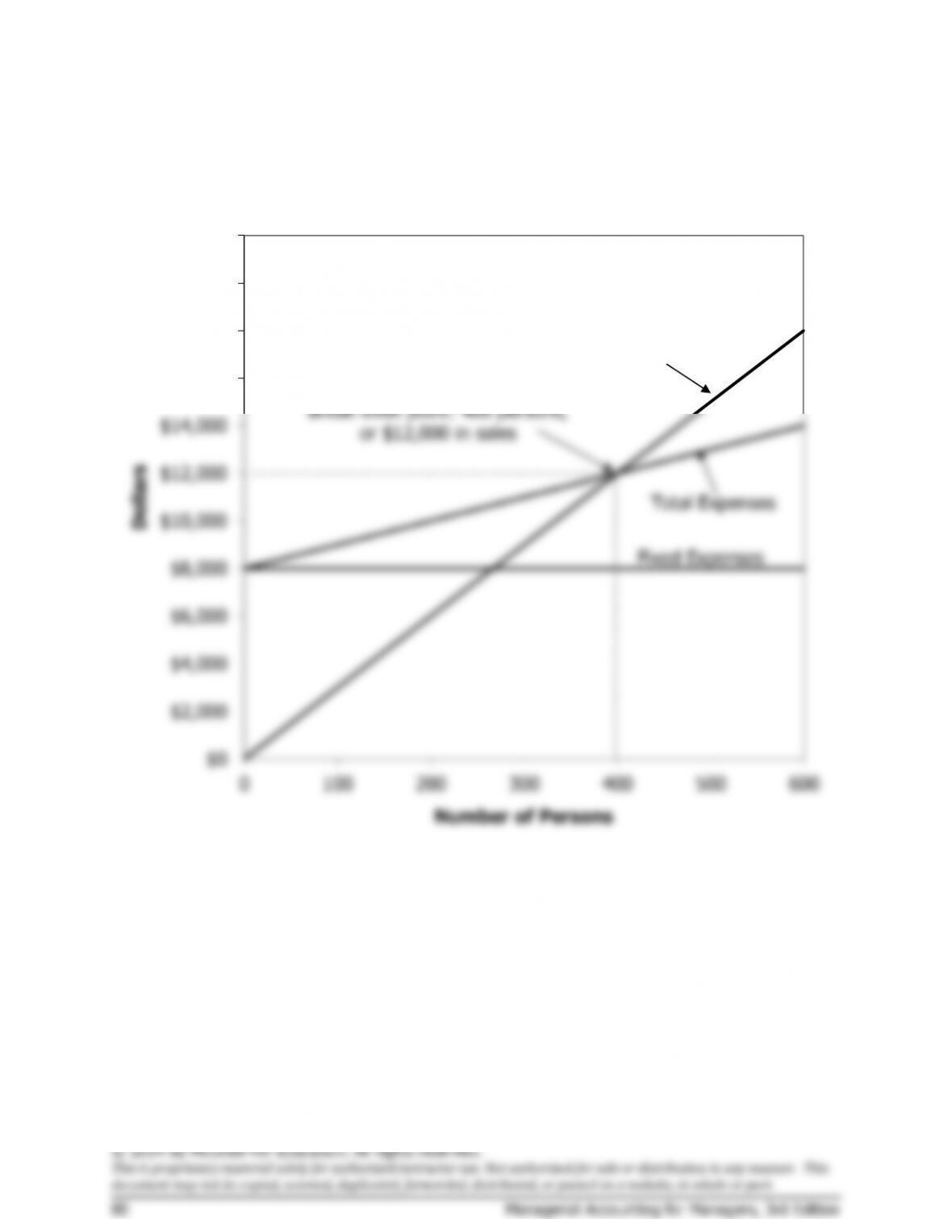

The fixed expenses of the Extravaganza total $8,000; therefore, the

break-even point would be computed as follows:

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30 − $10) × Q − $8,000

$0

= ($20) × Q − $8,000

$20Q

= $8,000

Q

= $8,000 ÷ $20

Q

= 400 persons; or, at $30 per person, $12,000

Alternative solution:

Fixed expenses

Unit sales =

to break even Unit contribution margin

$8,000

= = 400 persons

$20 per person

or, at $30 per person, $12,000.

2.

Variable cost per person ($7 + $3) …………………..

$10

Fixed cost per person ($8,000 ÷ 250 persons) ……

32

Ticket price per person to break even ……………….

$42

Exercise 3-14 (30 minutes)

1.

Model A100

Model B900

Total Company

Amount

%

Amount

%

Amount

%

Sales ……………

$700,000

100

$300,000

100

$1,000,000

100

Variable

expenses …….

280,000

40

90,000

30

370,000

37

Contribution

margin ……….

$420,000

60

$210,000

70

630,000

63

*

Fixed expenses

598,500

Net operating

income ……….

$ 31,500

*630,000 ÷ $1,000,000 = 63%.

2. The break-even point for the company as a whole is:

Fixed expenses

Break-even point in =

total dollar sales Overall CM ratio

$598,500

= = $950,000 in sales

0.63

3. The additional contribution margin from the additional sales is computed

as follows:

$50,000 × 63% CM ratio = $31,500

Assuming no change in fixed expenses, all of this additional contribution

Exercise 3-16 (30 minutes)

1. Variable expenses: $60 × (100% – 40%) = $36.

2.

a.

Selling price ……………………..

$60

100%

Variable expenses ……………..

36

60%

Contribution margin …………..

$24

40%

Let Q = Break-even point in units.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($60 − $36) × Q − $360,000

$0

=

($24) × Q − $360,000

$24Q

=

$360,000

Q

=

$360,000 ÷ $24 per unit

Q

=

15,000 units

CM ratio × Sales − Fixed expenses

0.40 × Sales − $360,000

0.40 × Sales

$360,000

$360,000 ÷ 0.40

$900,000

Unit CM × Q − Fixed expenses

$450,000

Exercise 3-16 (continued)

3.

a.

Fixed expenses

Unit sales =

to break even Unit contribution margin

= $360,000 ÷ $24 per unit = 15,000 units

Exercise 3-17 (20 minutes)

Total

Per Unit

1.

Sales (30,000 units × 1.15 = 34,500 units) ..

$172,500

$5.00

Variable expenses ………………………………..

103,500

3.00

Contribution margin ………………………………

69,000

$2.00

Fixed expenses ……………………………………

50,000

Net operating income …………………………...

$ 19,000

2.

Sales (30,000 units × 1.20 = 36,000 units) ..

$162,000

$4.50

Variable expenses ………………………………..

108,000

3.00

Contribution margin ………………………………

54,000

$1.50

Fixed expenses ……………………………………

50,000

Net operating income …………………………...

$ 4,000

3.

Sales (30,000 units × 0.95 = 28,500 units) ..

$156,750

$5.50

Variable expenses ………………………………..

85,500

3.00

Contribution margin ………………………………

71,250

$2.50

Fixed expenses ($50,000 + $10,000) ……….

60,000

Net operating income …………………………...

$ 11,250

4.

Sales (30,000 units × 0.90 = 27,000 units) ..

$151,200

$5.60

Variable expenses ………………………………..

86,400

3.20

Contribution margin ………………………………

64,800

$2.40

Fixed expenses ……………………………………

50,000

Net operating income …………………………...

$ 14,800