Exercise 5-8 (10 minutes)

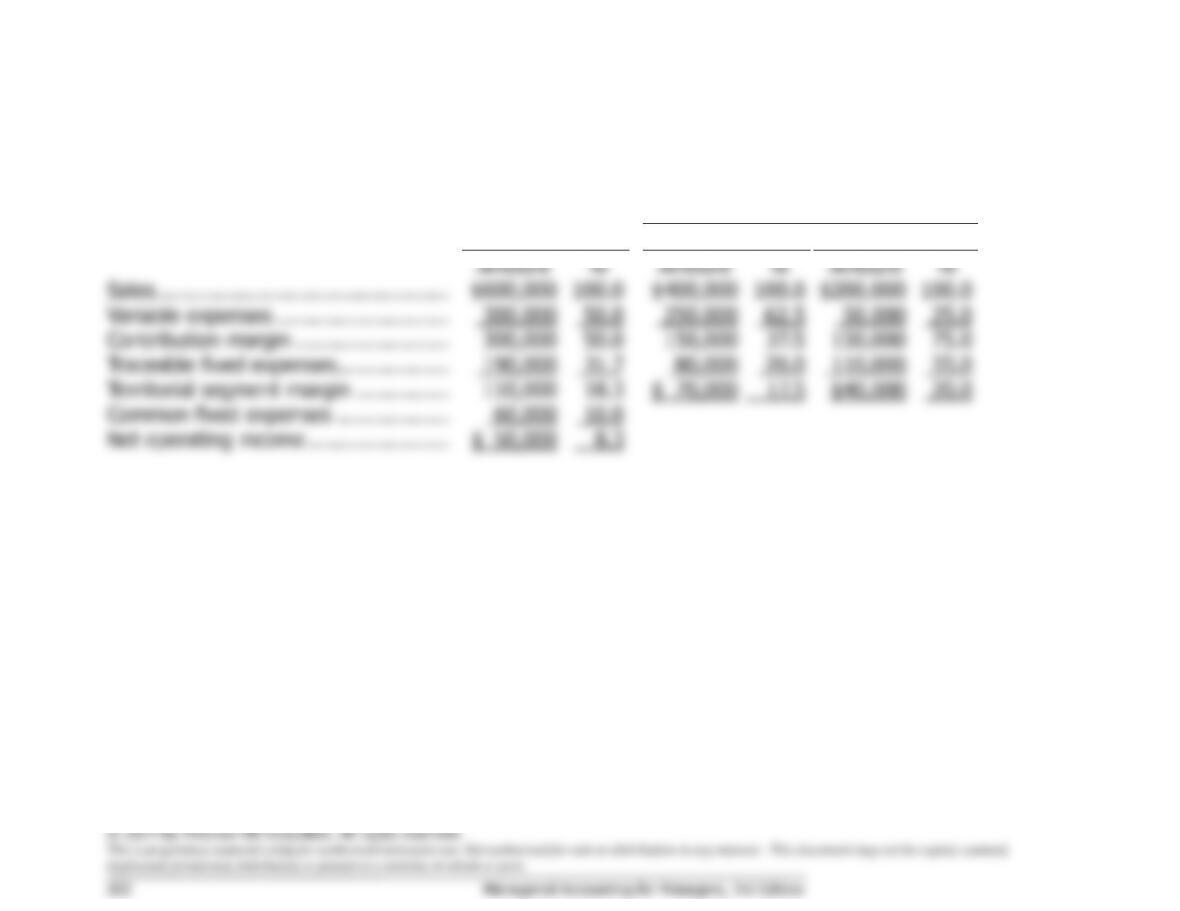

The completed segmented income statement should appear as follows:

Divisions

Total Company

East

West

Amount

%

Amount

%

Amount

%

Sales ………………………………………..

$600,000

100.0

$400,000

100.0

$200,000

100.0

Variable expenses ……………………….

300,000

50.0

250,000

62.5

50,000

25.0

Contribution margin …………………….

300,000

50.0

150,000

37.5

150,000

75.0

Traceable fixed expenses ………………

190,000

31.7

80,000

20.0

110,000

55.0

Territorial segment margin ……………

110,000

18.3

$ 70,000

17.5

$40,000

20.0

Common fixed expenses ………………

60,000

10.0

Net operating income …………………..

$ 50,000

8.3

Exercise 5-10 (20 minutes)

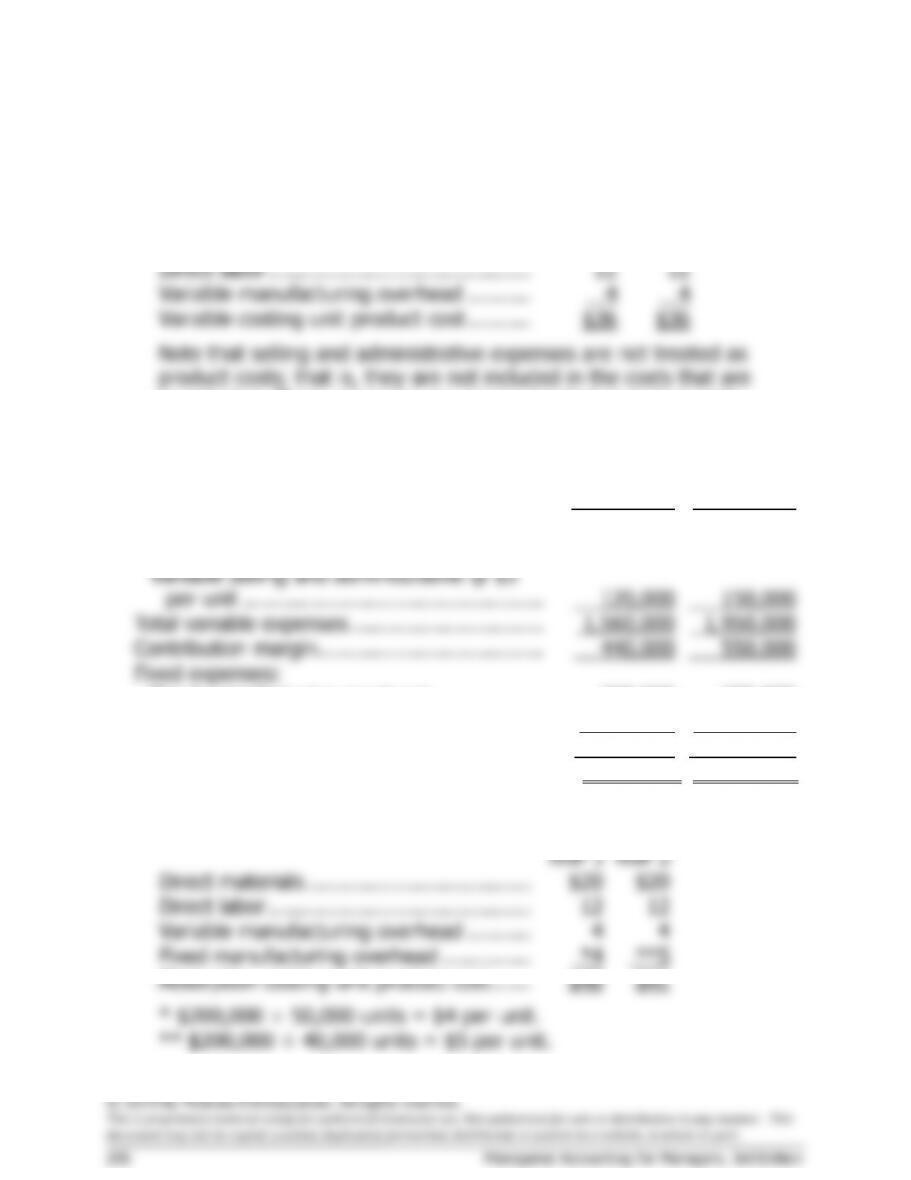

1. Under absorption costing, all manufacturing costs (variable and fixed)

are included in product costs.

Direct materials ………..…………………..

$ 60

Direct labor ………………………………….

30

Variable manufacturing overhead ……..

10

Fixed manufacturing overhead

($300,000 ÷ 10,000 units) ……………

30

Unit product cost …………………………..

$130

2. The absorption costing income statement appears below:

Sales (9,000 units × $200 per unit) ……..…………………..

$1,800,000

Cost of goods sold (9,000 units × $130 per unit) …….…..

1,170,000

Gross margin ……………………………………………………….

630,000

Selling and administrative expenses

(9,000 units × $20 per unit) + $450,000 ……….………..

630,000

Net operating income ……………………………………………

$ 0

Note: The company apparently has exactly zero net operating income

even though its sales are below the break-even point computed in

Exercise 5-9. This occurs because $30,000 of fixed manufacturing

overhead has been deferred in inventory and does not appear on the

income statement prepared using absorption costing.