Exercise 4-15 (continued)

2 a. Molding Department:

The estimated total manufacturing overhead cost in the Molding

Department is computed as follows:

Estimated fixed manufacturing overhead ………………

$800,000

Estimated variable manufacturing overhead

$5.00 per MH × 20,000 MHs …………………………...

100,000

Estimated total manufacturing overhead cost …………

$900,000

MHs

per MH

Estimated fixed manufacturing overhead ………………

Estimated total manufacturing overhead cost …………

$450,000

MHs

per MH

Problem 4-16 (continued)

We can now complete the job cost sheet for the Krimmer Corporation

Problem 4-17 (continued)

Durham Company

Income Statement

For the Year Ended December 31

Sales …………………………….……………

$200,000

Cost of goods sold …………………………

124,000

Gross margin ………………………………..

76,000

Selling and administrative expenses …..

61,000

Net operating income …………………….

$ 15,000

Problem 4-19 (45 minutes)

1. The actual manufacturing overhead costs incurred were as follows:

Reference

(a)

Indirect materials ……………………………..

$ 38,000

(b)

Indirect labor …………………………………..

18,000

(c)

Factory heat, power, and water ……………

42,000

(d)

Factory insurance ……………………………..

9,000

(f)

Factory depreciation ………………………….

51,000

Total manufacturing overhead incurred …

$158,000

In contrast, $170,000 in manufacturing overhead cost was applied to

jobs:

$153,000 =$4.25 per MH; 40,000 MHs×$4.25 per MH=$170,000.

36,000 MHs

Therefore, the overhead was overapplied by $3,000.

Manufacturing overhead incurred ………..

$158,000

Manufacturing overhead applied

(40,000 MHs × $4.25 per MH) ………….

170,000

Overhead overapplied ……………………….

$ 12,000

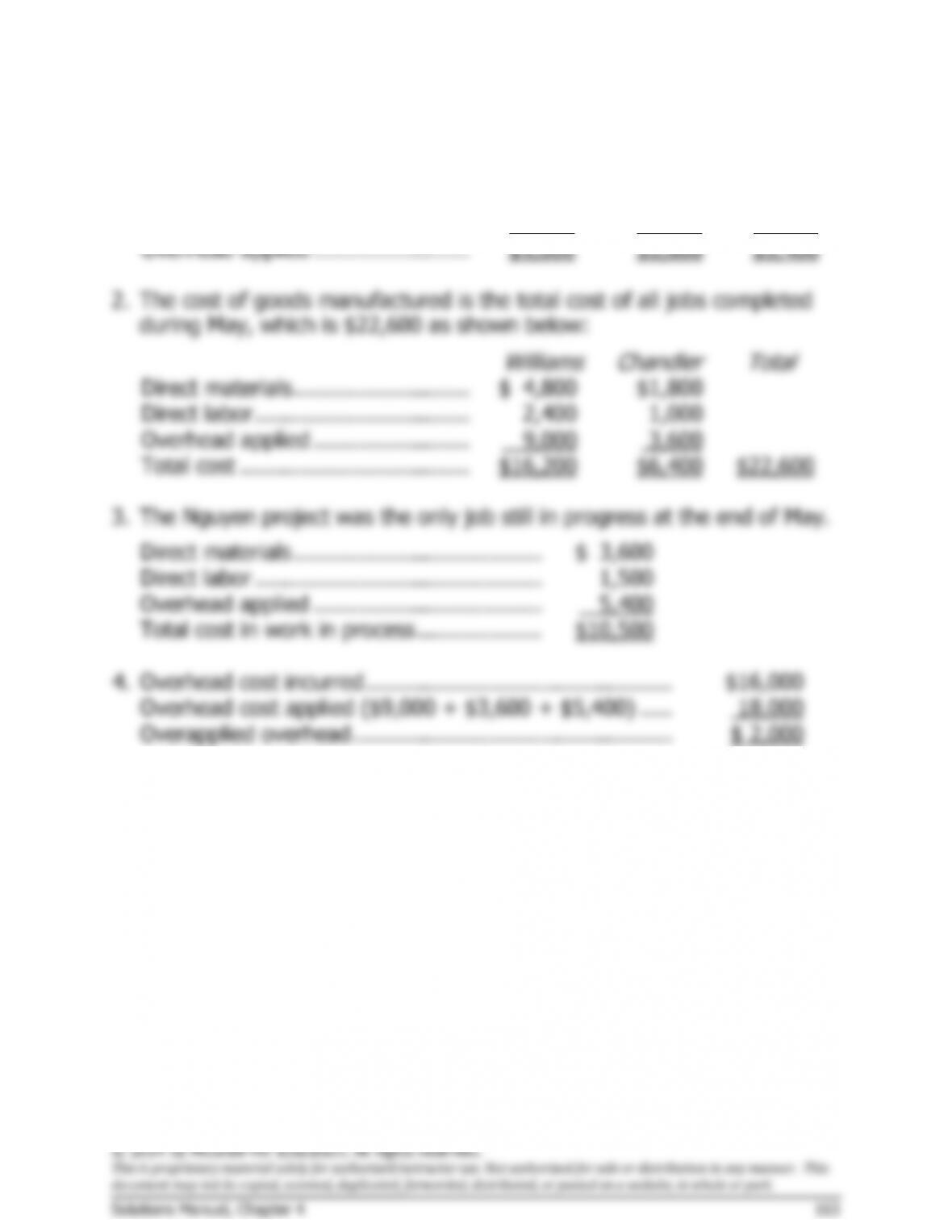

2. The cost of goods sold for the year (before adjustment for underapplied

or overapplied overhead) is $475,000—the total cost to manufacture the

goods that were sold according to their job cost sheets. The adjusted

cost of goods sold is computed as follows:

Unadjusted cost of goods sold ………………….

$475,000

Deduct: Overapplied overhead ..………………..

12,000

Cost of goods sold ………………………………….

$463,000

The selling and administrative expenses for the year were:

Reference

(b)

Sales commissions …………………………….

$ 10,000

(b)

Administrative salaries ……………………….

25,000

(d)

Insurance ……………………………………….

1,000

(e)

Advertising ………………………………………

50,000

(f)

Depreciation ……………………………………

9,000

Total selling and administrative expense ..

$95,000