Chapter 10

Flexible Budgets and Performance Analysis

Solutions to Questions

10-1 The planning budget is prepared for the

10-2 A flexible budget can be adjusted to

and is not subsequently adjusted.

10-3 Actual results can differ from the budget

in how effectively resources are managed.

10-4 As noted in 10–3 above, a difference

From a manager’s perspective, a variance that is

due to a change in activity is very different from

very different actions from a variance of the

second kind. Consequently, these two kinds of

are lumped together.

10-5 An activity variance is the difference

to the difference in the level of activity assumed

in the planning budget and the actual level of

labels are perhaps misleading for activity

variances that involve costs. A “favorable”

level of activity. An “unfavorable” activity

variance for a cost occurs because the cost has

10-6 A revenue variance is the difference

between how much the revenue should have

revenue variance occurs because the revenue is

greater than expected for the actual level of

activity. An unfavorable revenue variance occurs

10-7 A spending variance is the difference

between how much a cost should have been,

straight-forward. A favorable spending variance

occurs because the cost is lower than expected

activity.

10-8 In a flexible budget performance report,

and actual results. The differences between the

static planning budget and the flexible budget

budget performance report cleanly separates the

differences between the static planning budget

the effectiveness with which resources are

managed (the revenue and spending variances).

When two cost drivers exist, some costs may be

a function of the first cost driver, some costs

10–10 When the static planning budget is

This assumption is valid only for fixed costs.

However, it is unlikely that all costs are fixed.

Some are likely to be variable or mixed.

and then directly compared to actual results, it

is implicitly assumed that costs should change in

mixed.

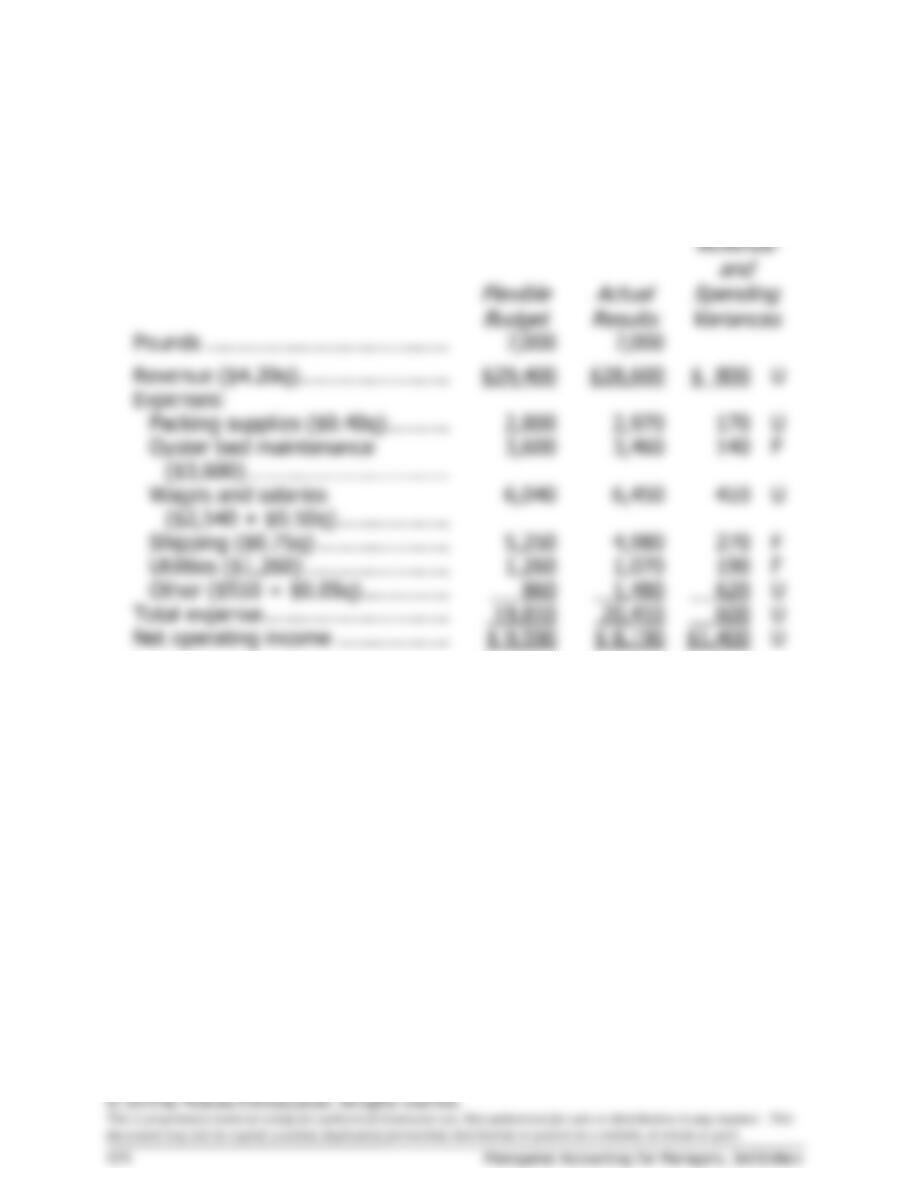

Exercise 10–1 (10 minutes)

Gator Divers

Flexible Budget

For the Month Ended March 31

Actual diving-hours …………………………………

190

Revenue ($380.00q) ……………………………….

$72,200

Expenses:

Wages and salaries ($12,000 + $130.00q) …

36,700

Supplies ($5.00q) …………………………………

950

Equipment rental ($2,500 + $26.00q) ………

7,440

Insurance ($4,200) ……………………………….

4,200

Miscellaneous ($540 + $1.50q) ……………….

825

Total expense ……………………………….……….

50,115

Net operating income ……………………..……….

$22,085

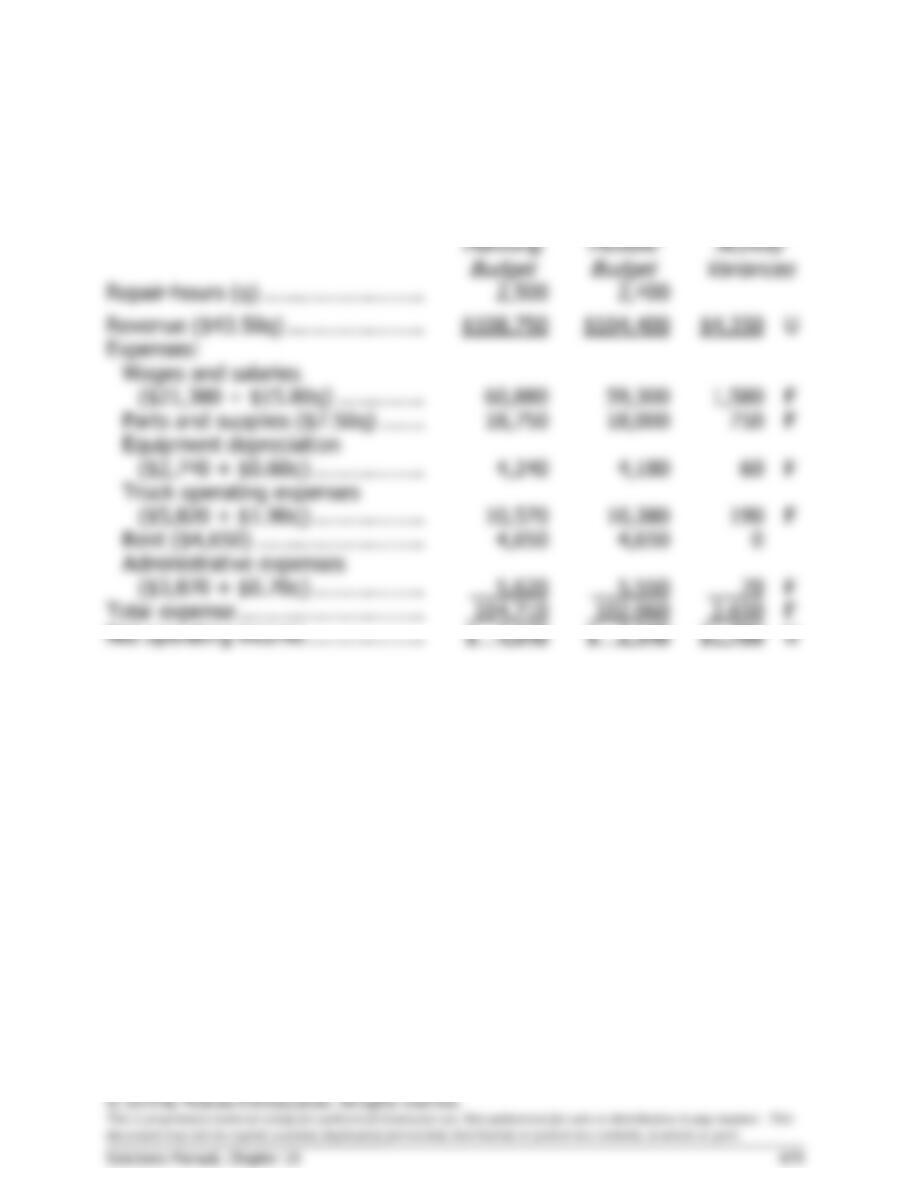

Exercise 10-4 (20 minutes)

1.

Mt. Hood Air

Flexible Budget Performance Report

For the Month Ended August 31

Planning

Budget

Activity

Variances

Flexible

Budget

Revenue

and

Spending

Variances

Actual

Results

Flights (q) ………………………………..

50

52

52

Revenue ($360.00q) …………………..

$18,000

$720

F

$18,720

$1,740

U

$16,980

Expenses:

Wages and salaries

($3,800 + $92.00q) ……..………..

8,400

184

U

8,584

44

F

8,540

Fuel ($34.00q) ………………………..

1,700

68

U

1,768

162

U

1,930

Airport fees ($870 + $35.00q) ……

2,620

70

U

2,690

0

2,690

Aircraft depreciation ($11.00q) …..

550

22

U

572

0

572

Office expenses ($230 + $1.00q) ..

280

2

U

282

168

U

450

Total expense …………………………...

13,550

346

U

13,896

286

U

14,182

Net operating income …………………

$ 4,450

$374

F

$ 4,824

$2,026

U

$ 2,798

2. The overall activity variance is $374 favorable and is due to an increase in activity. The $1,740

unfavorable revenue variance is very large relative to the company’s net operating income and should

be investigated. Was this due to discounts given or perhaps a lower average number of passengers

per flight than usual? The other variances are relatively small, but are worth some management

attention—particularly if they recur next month.