Archives

978-1259917059 Bingham Solution Instruction Part 1

For use with McGraw-Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck, Suzanne L. Lowensohn, and Daniel G. Neely Instructions City of Bingham Computerized Cumulative Problem © 2019 by McGraw-Hill Education. This is proprietary material […]

978-1259917059 Bingham Solution Instruction Part 2

4. [Para. 5a-4] A contract for architectural services was signed at an estimated amount of $350,000 for the design of the City Hall Annex. Required: Record the encumbrance in the City Hall Annex Construction. This transaction has no effect at […]

978-1259917059 Chapter 1 Solution Manual

Chapter 01 – Introduction to Accounting and Financial Reporting for Government and Not-for-Profit Entities Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 CHAPTER 1: INTRODUCTION TO ACCOUNTING AND […]

978-1259917059 Chapter 10 Solution Manual

Chapter 10 – Analysis of Government Financial Performance 10-1 CHAPTER 10: ANALYSIS OF GOVERNMENT FINANCIAL PERFORMANCE OUTLINE Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Number Topic Type/Task Status […]

978-1259917059 Chapter 11 Solution Manual Part 1

Chapter 11 – Auditing of Government and Not–for-Profit Organizations 11-1 CHAPTER 11: AUDITING OF GOVERNMENT AND NOT-FOR- PROFIT ORGANIZATIONS OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 11-1 Definition of audit, standard setters Define, explain Same 11-2 GAGAS audit services […]

978-1259917059 Chapter 11 Solution Manual Part 2

11-12 Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Ch. 11, Solutions, Case 11-15 (Cont’d) 2. Partially. The salary for an entry-level law enforcement officer is allowable. However, the […]

978-1259917059 Chapter 12 Solution Manual Part 1

Chapter 12 – Budgeting and Performance Measurement Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 12: BUDGETING AND PERFORMANCE MEASUREMENT 12–1 OUTLINE Number Topic Type/Task Status (re: 17/e) […]

978-1259917059 Chapter 12 Solution Manual Part 2

Chapter 12 – Budgeting and Performance Measurement 12–12 Ch. 12, Solutions, Exercise 12-17 (Cont’d) d. Based upon the information provided, the town presently uses incremental line-item budgeting, probably organized along department lines. Although the new town manager’s effort to introduce […]

978-1259917059 Chapter 13 Solution Manual Part 1

Chapter 13 – Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 13: NOT-FOR-PROFIT ORGANIZATIONS— 13-1 REGULATORY, TAXATION, AND PERFORMANCE ISSUES OUTLINE Number […]

978-1259917059 Chapter 13 Solution Manual Part 2

Chapter 13 – Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues 13-13 Ch. 13, Solutions, Case 13-14 (Cont’d) General Problem Information: Evaluating charity organizations Leaning Objective: 13-5 Topic: Benchmarking and Performance Measures Bloom’s Taxonomy: Evaluate Accreditation Skills tag: AACSB: Analytical Thinking, AICPA: […]

978-1259917059 Chapter 14 Solution Manual Part 1

Chapter 14 – Accounting for Not-for-Profit Organizations Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 14: ACCOUNTING FOR NOT-FOR-PROFIT 14-1 ORGANIZATIONS OUTLINE Number Type/Task Status (re: 17/e) Questions: […]

978-1259917059 Chapter 14 Solution Manual Part 2

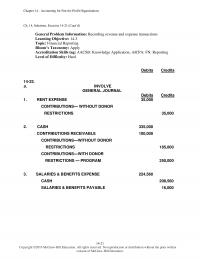

Chapter 14 – Accounting for Not-for-Profit Organizations 14-21 Ch. 14, Solutions, Exercise 14-21 (Cont’d) General Problem Information: Recording revenue and expense transactions Learning Objective: 14-3 Topic: Financial Reporting Bloom’s Taxonomy: Apply Accreditation Skills tag: AACSB: Knowledge Application, AICPA: FN: Reporting […]

978-1259917059 Chapter 14 Solution Manual Part 3

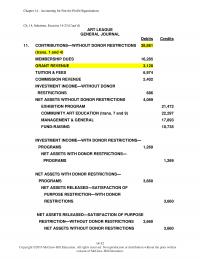

Chapter 14 – Accounting for Not-for-Profit Organizations 14-32 Ch. 14, Solutions, Exercise 14-23 (Cont’d) ART LEAGUE GENERAL JOURNAL Debits Credits 11. CONTRIBUTIONS—WITHOUT DONOR RESTRICTIONS 38,861 (trans. 1 and 4) MEMBERSHIP DUES 16,285 GRANT REVENUE 3,120 TUITION & FEES 6,974 C […]

978-1259917059 Chapter 15 Solution Manual Part 1

Chapter 15 – Accounting for Colleges and Universities Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 15: ACCOUNTING FOR COLLEGES AND UNIVERSITIES 15-1 OUTLINE Number Topic Type/Task Status […]

978-1259917059 Chapter 15 Solution Manual Part 2

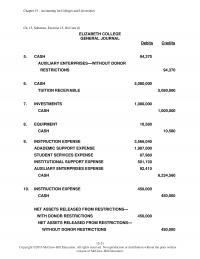

Chapter 15 – Accounting for Colleges and Universities 15-21 Ch. 15, Solutions, Exercise 15-18 (Cont’d) ELIZABETH COLLEGE GENERAL JOURNAL Debits Credits 5. CASH 94,370 AUXILIARY ENTERPRISES—WITHOUT DONOR RESTRICTIONS 94,370 6. CASH 5,080,000 TUITION RECEIVABLE 5,080,000 7. INVESTMENTS 1,000,000 CASH 1,000,000 […]

978-1259917059 Chapter 15 Solution Manual Part 3

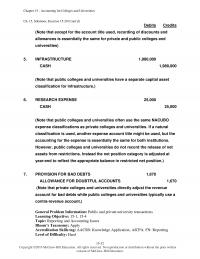

Chapter 15 – Accounting for Colleges and Universities 15-32 Ch. 15, Solutions, Exercise 15-20 (Cont’d) Debits Credits (Note that except for the account title used, recording of discounts and allowances is essentially the same for private and public colleges and […]

978-1259917059 Chapter 16 Solution Manual Part 1

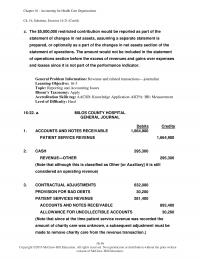

Chapter 16 – Accounting for Health Care Organizations Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 16: ACCOUNTING FOR HEALTH CARE ORGANIZATIONS 16-1 OUTLINE Number Topic Type/Task Status […]

978-1259917059 Chapter 16 Solution Manual Part 2

Chapter 16 – Accounting for Health Care Organizations 16-16 Ch. 16, Solutions, Exercise 16-21 (Cont’d) c. The $5,000,000 restricted contribution would be reported as part of the statement of changes in net assets, assuming a separate statement is prepared, or […]

978-1259917059 Chapter 17 Solution Manual Part 1

Chapter 17 – Accounting and Reporting for the Federal Government 17-1 CHAPTER 17: ACCOUNTING AND REPORTING FOR THE FEDERAL GOVERNMENT OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 17-1 Roles of GOA, Treasury, and OMB in federal financial reporting Explain […]

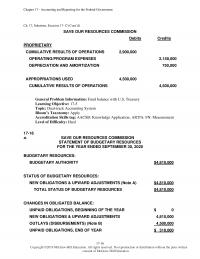

978-1259917059 Chapter 17 Solution Manual Part 2

Chapter 17 – Accounting and Reporting for the Federal Government 17-16 Ch. 17, Solutions, Exercise 17-17 (Cont’d) SAVE OUR RESOURCES COMMISSION Debits Credits PROPRIETARY CUMULATIVE RESULTS OF OPERATIONS 2,900,000 OPERATING/PROGRAM EXPENSES 2,150,000 DEPRECIATION AND AMORTIZATION 750,000 APPROPRIATIONS USED 4,500,000 CUMULATIVE […]

978-1259917059 Chapter 2 Solution Manual

Chapter 02 – Principles of Accounting and Financial Reporting for State and Local Governments 2-1 CHAPTER 2: PRINCIPLES OF ACCOUNTING AND FINANCIAL REPORTING FOR STATE AND LOCAL GOVERNMENTS OUTLINE Copyright ©2019 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

978-1259917059 Chapter 3 Solution Manual Part 1

Chapter 03 – Governmental Operating Statement Accounts; Budgetary Accounting 3-1 CHAPTER 3: GOVERNMENTAL OPERATING STATEMENT ACCOUNTS; BUDGETARY ACCOUNTING OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 3-1 Distinguishing characteristics of fund-based and government-wide financial statements Identify and describe Same 3-2 […]

978-1259917059 Chapter 3 Solution Manual Part 2

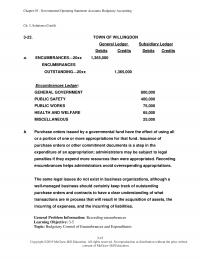

Chapter 03 – Governmental Operating Statement Accounts; Budgetary Accounting 3-15 Ch. 3, Solutions (Cont’d) 3-23. TOWN OF WILLINGDON General Ledger Subsidiary Ledger Debits Credits Debits Credits a. ENCUMBRANCES⎯20xx 1,365,000 ENCUMBRANCES OUTSTANDING⎯20xx 1,365,000 Encumbrances Ledger: GENERAL GOVERNMENT 800,000 PUBLIC SAFETY 400,000 […]

978-1259917059 Chapter 4 Solution Manual Part 1

Chapter 04 – Accounting for Governmental Operating Activities—Illustrative Transactions and Financial Statements 4-1 CHAPTER 4: ACCOUNTING FOR GOVERNMENTAL OPERATING ACTIVITIES⎯ILLUSTRATIVE TRANSACTIONS AND FINANCIAL STATEMENTS OUTLINE Number Topic Type/Task Status (re: 18/e) Questions: 4-1 Appropriate choice of governmental fund Analyze New […]

978-1259917059 Chapter 4 Solution Manual Part 2

Chapter 04 – Accounting for Governmental Operating Activities—Illustrative Transactions and Financial Statements 4-21 Ch. 4, Solutions, Exercise 4-23 (Cont’d) General Problem Information: Special revenue fund and voluntary nonexchange transactions Learning Objective: 4-1, 4-4, 4-7 Topic: Special Revenue Funds Bloom’s Taxonomy: […]

978-1259917059 Chapter 4 Solution Manual Part 3

Chapter 04 – Accounting for Governmental Operating Activities—Illustrative Transactions and Financial Statements 4-37 Ch. 4, Solutions (Cont’d) c. JEDVILLE TOWNSHIP—JOURNAL ENTRIES GOVERNMENTAL ACTIVITIES 1. NO JOURNAL ENTRY REQUIRED 2. INVENTORY OF SUPPLIES 850,000 CASH 850,000 3. EXPENSES 780,000 4. NO […]

978-1259917059 Chapter 5 Solution Manual Part 1

Chapter 05 – Accounting for General Capital Assets and Capital Projects 5-1 CHAPTER 5: ACCOUNTING FOR GENERAL CAPITAL ASSETS AND CAPITAL PROJECTS OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 5-1 Defining and reporting general capital assets Define and explain […]

978-1259917059 Chapter 5 Solution Manual Part 2

Chapter 05 – Accounting for General Capital Assets and Capital Projects 5-19 Chapter 5, Solutions, Exercise 5-22 (Cont’d) Debits Credits 6. Capital Projects Fund: To close nominal accounts: OTHER FINANCING SOURCES— PROCEEDS OF BONDS 6,000,000 OTHER FINANCING SOURCES— INTERFUND TRANSFERS […]

978-1259917059 Chapter 6 Solution Manual Part 1

Chapter 06 – Accounting for General Long-term Liabilities and Debt Service 6-1 CHAPTER 6: ACCOUNTING FOR GENERAL LONG-TERM LIABILITIES AND DEBT SERVICE OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 6-1 Defining general long–term liabilities; financial reporting Define, explain Same […]

978-1259917059 Chapter 6 Solution Manual Part 2

Chapter 06 – Accounting for General Long-term Liabilities and Debt Service 6-18 Ch. 6, Solutions, Exercise 6-19 (Cont’d) Debits Credits b. Debt Service Fund: CASH 100,000 OTHER FINANCING SOURCES—PREMIUM ON BONDS ($8,000,000 × .01) 80,000 REVENUES 20,000 Governmental Activities: CASH […]

978-1259917059 Chapter 7 Solution Manual Part 1

Chapter 07 – Accounting for the Business-type Activities of State and Local Governments 7-1 CHAPTER 7: ACCOUNTING FOR THE BUSINESS-TYPE ACTIVITIES OF STATE AND LOCAL GOVERNMENTS OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 7-1 Proprietary funds Explain Same 7-2 […]

978-1259917059 Chapter 7 Solution Manual Part 2

Chapter 07 – Accounting for the Business-type Activities of State and Local Governments 7-21 Ch. 7, Solutions, Exercise 7-20 (Cont’d) Debits Credits 3. Internal Service Fund: SALARIES AND WAGES EXPENSE 235,000 CASH 235,000 Governmental Activities: EXPENSES—GENERAL GOVERNMENT 235,000 CASH 235,000 […]

978-1259917059 Chapter 7 Solution Manual Part 3

Chapter 07 – Accounting for the Business-type Activities of State and Local Governments 7-35 Ch. 7, Solutions, Exercise 7-24 (Cont’d) c. No. The explanation notes that there is no long-term debt. Thus, the activity of the fund is not financed […]

978-1259917059 Chapter 8 Solution Manual Part 1

Chapter 08 – Accounting for Fiduciary Activities—Custodial and Trust Funds 8-1 CHAPTER 8: ACCOUNTING FOR FIDUCIARY ACTIVITIES— CUSTODIAL AND TRUST FUNDS OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 8-1 Determining a fiduciary relationship Explain New 8-2 Distinction between custodial […]

978-1259917059 Chapter 8 Solution Manual Part 2

Chapter 08 – Accounting for Fiduciary Activities—Custodial and Trust Funds 8-15 Ch. 8, Solutions, Exercise 8-20 b. (Cont’d) Debits Credits 4. DEDUCTIONS—PAYMENT OF PRINCIPAL TO BONDHOLDERS 500,000 DEDUCTIONS—PAYMENT OF INTEREST TO BONDHOLDERS 250,000 ADDITIONS—PRINCIPAL & INTEREST COLLECTIONS 750,000 c. Assets […]

978-1259917059 Chapter 9 Solution Manual Part 1

Chapter 09 – Financial Reporting of State and Local Governments 9-1 CHAPTER 9: FINANCIAL REPORTING OF STATE AND LOCAL GOVERNMENTS OUTLINE Number Topic Type/Task Status (re: 17/e) Questions: 9-1 Primary governments Identify 9-2 9-2 Interim reports Explain 9-3 9-3 Financial […]

978-1259917059 Chapter 9 Solution Manual Part 2

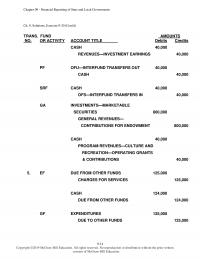

Chapter 09 – Financial Reporting of State and Local Governments 9-14 Ch. 9, Solutions, Exercise 9-20 (Cont’d) TRANS. FUND AMOUNTS NO. OR ACTIVITY ACCOUNT TITLE Debits Credits CASH 40,000 REVENUES—INVESTMENT EARNINGS 40,000 PF OFU—INTERFUND TRANSFERS OUT 40,000 CASH 40,000 SRF […]

978-1259917059 Journals And Ledgers Bingham Solution Part 1

1 For use with McGraw–Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck, Suzanne L. Lowensohn, and Daniel G. Neely Journals and Ledgers City of Bingham Computerized Cumulative Problem © 2019 by McGraw–Hill Education. This […]

978-1259917059 Journals And Ledgers Bingham Solution Part 2

Year Ref Account Description Debits Credits Balance Dr(Cr) 2020 104 6b-10 4,000 1,359,600 2020 104 6b-11 600,000 759,600 Taxes Receivable-Current 2020 103 6b-2 705,000 705,000 2020 103 6b-6 675,000 30,000 2020 105 6b-12 30,000 0 Allowance for Uncollectible Current Taxes […]

978-1259917059 Journals And Ledgers Bingham Solution Part 3

Year Ref Poste dAcct# – Name Descriptio nDebits Credits 2019 101 X 1260 – Buildings 2d 11,020,000 2019 101 X 1270 – Accumulated Depreciation-Buildings 2d 3,100,000 2019 101 X 1280 – Equipment 2d 8,360,000 2019 101 X 1290 – Accumulated […]

978-1259917059 Smithville Full Version Instruction Part 1

For use with McGraw-Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck and Suzanne L. Lowensohn Instructions City of Smithville Full Version Computerized Cumulative Problem © 2019 by McGraw-Hill Education. This is proprietary material solely […]

978-1259917059 Smithville Full Version Instruction Part 2

9. [Para. 5-a-9] In July 2020, the contractor for the Elm Street Project reported that the project was one-half completed and requested a progress payment of $1,200,000. This amount was paid in late July, less the contractual retention of 5 […]

978-1259917059 Smithville Short Version Instruction Part 1

For use with McGraw-Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck, Suzanne L. Lowensohn, and Daniel G. Neely Instructions City of Smithville Short Version Computerized Cumulative Problem © 2019 by McGraw-Hill Education. This is […]

978-1259917059 Smithville Short Version Instruction Part 2

7. [Para. 4-a-7] During FY 2020, the City of Smithville received notification that the state government would send $150,000 at the beginning of the next fiscal year. Based on the city’s definition of “available for use,” the city considers the […]

978-1259917059 Solution Set Bingham Solution Part 1

For use with McGraw–Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck, Suzanne L. Lowensohn, and Daniel G. Neely Solution Set City of Bingham Computerized Cumulative Problem © 2019 by McGraw–Hill Education. This is proprietary […]

978-1259917059 Solution Set Bingham Solution Part 2

Debits Credits Cash $ 746,018 Restricted Cash-Customer Deposits 70,098 Customer Accounts Receivable 253,274 Accumulated Provision for Uncollectible Accounts $ 5,820 Inventory of Supplies 141,299 Due from Other Funds 50,000 Utility Plant in Service 22,163,213 Accumulated Depreciation-Utility Plant 5,186,691 Construction Work […]

978-1259917059 Solution Set Bingham Solution Part 3

Requirement 9d. Primary Government Governmental Business-type Component Assets Activities Activities Total Units (none) Cash 1,714,522$ 746,018$ 2,460,540$ Receivables (net) 412,920 247,454 660,374 Internal balances (50,000) 50,000 – Investments 200,000 200,000 Inventories 12,000 141,299 153,299 Restricted cash 70,098 70,098 Capital assets […]

978-1259917059 Solution Set SmithvilleFullVersionSolution Part 1

Solution Set City of Smithville To Accompany18th Edition of Accounting for Governmental & Nonprofit Entities Description Debit Credit Cash 376,290 Taxes Receivable-Delinquent 391,756 Allowance for Uncollectible Delinquent Taxes 11,752 Interest and Penalties Receivable on Taxes 40,126 Allowance for Uncollectible Interest […]

978-1259917059 Solution Set SmithvilleFullVersionSolution Part 2

Requirement 6b. Variance Actual with Final Original Final Amounts Budget Revenues: Accrued interest on bonds sold 12,500$ 12,500$ 12,500$ –$ Expenditures: Interest on bonds 25,000 25,000 25,000 – Excess of Expenditures over Revenues (12,500) (12,500) (12,500) – Other Financing Sources: […]

978-1259917059 Solution Set SmithvilleFullVersionSolution Part 3

Requirement 9c. Debits Credits Cash $ 495,959 Taxes Receivable-Delinquent 377,899 Allowance for Uncollectible Delinquent Taxes $ 32,176 Interest and Penalties Receivable on Taxes 43,269 Allowance for Uncollectible Interest and Penalties 3,772 Due from State Government 150,000 Inventory of Supplies 64,420 […]

978-1259917059 Solution Set SmithvilleShortVersionSolution Part 1

Solution Set Short Version City of Smithville To accompany18th Edition Accounting for Governmental & Nonprofit Entities Description Debit Credit Cash 376,290 Taxes Receivable-Delinquent 391,756 Allowance for Uncollectible Delinquent Taxes 11,752 Interest and Penalties Receivable on Taxes 40,126 Allowance for Uncollectible […]

978-1259917059 Solution Set SmithvilleShortVersionSolution Part 2

Requirement 6b. Debits Credits City of Smithville Street Improvement Bond Debt Service Fund Post-closing Trial Balance For year 2020 Cash $ 7,500 Fund Balance-Restricted $ 7,500 Totals for all accounts $ 7,500 $ 7,500 Requirement 6b. As of December 31, […]

978-1259917059 Test Bank Chapter 1 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 1 Introduction to Accounting and Financial Reporting for Government and Not-for-Profit Entities 1) Special purpose governments generally provide a wider range of services to their residents than do general purpose governments. […]

978-1259917059 Test Bank Chapter 1 Part 2

31) Which of the following is identified by the GASB as the “cornerstone” of all financial reporting in government? A) Decision usefulness. B) Stewardship. C) Accountability. D) Interperiod equity. Answer: C Difficulty: 1 Easy Topic: Objectives of financial reporting Learning […]

978-1259917059 Test Bank Chapter 1 Part 3

49) The FASB requires that a statement showing the relationship of functional expenses to natural classifications of expense be prepared by which of the following entities? A) Colleges and universities. B) Health care entities. C) Voluntary health and welfare entities. […]

978-1259917059 Test Bank Chapter 10 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 10 Analysis of Government Financial Performance 1) An effective system for evaluating financial performance helps management to assess whether financial performance can meet creditor and service obligations. Answer: TRUE Difficulty: 1 […]

978-1259917059 Test Bank Chapter 10 Part 2

35) Which of the following is a measure of the extent to which the government’s business-type activities are self-supporting? A) Unrestricted net position/total revenues. B) Business-type activities revenues/business-type activities expenses. C) Total net position (governmental activities and business-type activities) less […]

978-1259917059 Test Bank Chapter 10 Part 3

18 49) For each of the following financial ratios that are based on comprehensive annual financial report (CAFR) information by selecting the appropriate letter of the explanation for that ratio. Answers can only be used once. A. An indicator of […]

978-1259917059 Test Bank Chapter 11 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 11 Auditing of Government and Not-for-Profit Organizations 1) When financial statements are accompanied by the report of an independent auditor, users have the assurance that the statements have been prepared in […]

978-1259917059 Test Bank Chapter 11 Part 2

28) The single audit requirement applies to: A) All audits of state and local government reporting entities. B) Financial audits of all not-for-profit entities. C) Most audits of state and local governments expending federal grant funds. D) Only those governments […]

978-1259917059 Test Bank Chapter 11 Part 3

48) The fundamental ethical principles identified under generally accepted government auditing standards (GAGAS) include all of the following except: A) Public interest. B) Proper use of government information, resources, and position. C) Oath of office. D) Professional behavior. Answer: C […]

978-1259917059 Test Bank Chapter 11 Part 4

57) Each of the following activities could be performed by an independent auditor. Select whether generally accepted government auditing standards deem each activity Acceptable (A), Prohibited (P), or Require conceptual framework assessment (R) in regarding to independence. ________ 1. Reporting […]

978-1259917059 Test Bank Chapter 12 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 12 Budgeting and Performance Measurement 1) Budgeting is an important part of a manager’s planning and control responsibilities in both public and private organizations. Answer: TRUE Difficulty: 1 Easy Topic: Objectives […]

978-1259917059 Test Bank Chapter 12 Part 2

35) Effective capital budgeting for general capital assets of a government requires: A) Intermediate and long-range capital improvement plans for general capital assets. B) Nonfinancial information on physical measures and service condition of capital assets of component units. C) Consideration […]

978-1259917059 Test Bank Chapter 12 Part 3

51) For each of the following definitions, indicate the key term from the list that best matches by placing the appropriate definition. A. Efficiency measures B. Effectiveness measures C. Planning-programming-budgeting system D. Zero-based budgeting E. Program budgeting F. Flexible budgeting […]

978-1259917059 Test Bank Chapter 13 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 13 Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues 1) A state has the obligation to monitor and regulate a not-for-profit (NFP) organization because it granted the NFP tax-exempt status through the not-for-profit […]

978-1259917059 Test Bank Chapter 13 Part 2

31) Which of the following not-for-profit organizations is most likely to be tax-exempt under IRC Sec. 501(c)(3)? A) Beta Kappa Alpha Sorority. B) Peaceful Dreams Cemetery Association. C) Regional Association of Tree Trimmers. D) Survivors of Breast Cancer Club. Answer: […]

978-1259917059 Test Bank Chapter 13 Part 3

50) Which of the following defines an appeal to the public to take action on a legislative matter? A) Grass-roots lobbying. B) Propaganda. C) Lobbying. D) Political influence. Answer: A Difficulty: 1 Easy Topic: Federal regulation Learning Objective: 13-03 Identify […]

978-1259917059 Test Bank Chapter 14 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 14 Accounting for Not-for-Profit Organizations 1) Under current accounting and reporting standards, nongovernmental not-for-profit organizations must utilize the fund accounting structure set forth in the AICPA Audit and Accounting Guide Not-for-Profit […]

978-1259917059 Test Bank Chapter 14 Part 2

32) Goodwill created because a not-for-profit organization obtains control of another organization is always recorded as an asset. Answer: FALSE Difficulty: 1 Easy Topic: Consolidations Learning Objective: 14-04 Explain accounting for NFP consolidations and combinations. Bloom’s: Remember AACSB: Knowledge Application […]

978-1259917059 Test Bank Chapter 14 Part 3

53) A not-for-profit organization that follows FASB standards must display the changes in all classes of net assets on which of the following statements? A) Statement of activities. B) Statement of financial position. C) Statement of cash flows. D) Statement […]

978-1259917059 Test Bank Chapter 14 Part 4

69) Record the journal entry that would be made by a nongovernmental, not-for-profit organization involved in medical research. (If no entry is required for a transaction/event, select “No Journal Entry Required” in the first account field.) 1. The entity received […]

978-1259917059 Test Bank Chapter 15 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 15 Accounting for Colleges and Universities 1) Nongovernmental (private) colleges and universities should follow FASB standards; governmental (public) colleges and universities should follow GASB standards. Answer: TRUE Difficulty: 1 Easy Topic: […]

978-1259917059 Test Bank Chapter 15 Part 2

31) A private college would report which of the following assets differently than a public college? A) Land. B) Intangible assets. C) Collections. D) Equipment. Answer: B Difficulty: 2 Medium Topic: Statement of Net Position or Financial Position Learning Objective: […]

978-1259917059 Test Bank Chapter 15 Part 3

51) Which of the following measures may be useful to decision makers evaluating the financial condition of a college or university? A) Number of graduates. B) Composite financial index. C) Faculty productivity. D) Graduation rate. Answer: B Difficulty: 1 Easy […]

978-1259917059 Test Bank Chapter 16 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 16 Accounting for Health Care Organizations 1) Financial reporting standards for all hospitals are established by the FASB. Answer: FALSE Difficulty: 1 Easy Topic: GAAP for health care providers Learning Objective: […]

978-1259917059 Test Bank Chapter 16 Part 2

33) Which of the following statements is true about diagnosis-related groups (DRGs)? A) DRGs are the basis for a cost accounting method that groups costs together by departments performing the services. B) A DRG is a case-mix classification scheme that […]

978-1259917059 Test Bank Chapter 16 Part 3

53) For each of the following definitions, indicate the key term from the list that best matches by placing the appropriate definition. A. Contractual adjustments B. Capitation fees C. Charity care D. Diagnosis-related groups E. Prospective payment system F. Health […]

978-1259917059 Test Bank Chapter 17 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 17 Accounting and Reporting for the Federal Government 1) Responsibility for setting accounting and reporting standards for federal agencies rests primarily with the Federal Accounting Standards Advisory Board. Answer: FALSE Difficulty: […]

978-1259917059 Test Bank Chapter 17 Part 2

33) A certain federal agency placed an order for office supplies at an estimated cost of $14,400. Later in the same fiscal year these supplies were received at an actual cost of $14,800. Assume commitment accounting is not used by […]

978-1259917059 Test Bank Chapter 17 Part 3

53) The Federal Monuments Commission began operations on October 1, 2020. Prepare journal form all entries that should be made in budgetary and proprietary accounts of the agency. (If no entry is required for a transaction/event, select “No Journal Entry […]

978-1259917059 Test Bank Chapter 2 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 2 Principles of Accounting and Financial Reporting for State and Local Governments 1) According to the guidance of GASB Concepts Statement 3, financial information can be communicated by recognition in the […]

978-1259917059 Test Bank Chapter 2 Part 2

33) According to the GASB definition, which of the following represents an inflow of resources? A) Expenditures. B) Revenues. C) Assets. D) Deferred inflows. Answer: B Difficulty: 1 Easy Topic: Conceptual Framework-Providing Useful Financial Reports Learning Objective: 02-01 Describe the […]

978-1259917059 Test Bank Chapter 2 Part 3

54) The measurement focus and basis of accounting that are most unlike those used by business entities are those used by A) Governmental funds. B) Fiduciary funds. C) Proprietary funds. D) Contribution funds. Answer: A Difficulty: 2 Medium Topic: Financial […]

978-1259917059 Test Bank Chapter 2 Part 4

67) For each of the following scenarios, indicate how they would be classified for fund balance reporting purposes using the classification list. A. Nonspendable B. Restricted C. Committed D. Assigned E. Unassigned ________ 1. Bond proceeds of $15,000,000 that must […]

978-1259917059 Test Bank Chapter 3 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 3 Governmental Operating Statement Accounts; Budgetary Accounting 1) The government-wide statement of net position displays the net expense or revenue for each function or program of the government. Answer: FALSE Difficulty: […]

978-1259917059 Test Bank Chapter 3 Part 2

32) Extraordinary items and special items are reported on the government-wide statement of activities. A) With normal recurring general revenues. B) As separate line items in the Function/Programs section of the statement of activities. C) As separate line items below […]

978-1259917059 Test Bank Chapter 3 Part 3

Bloom’s: Apply AACSB: Knowledge Application AICPA: FN Reporting 59) When the budget for the General Fund is recorded, the required journal entry will include: A) A credit to Estimated Revenues. B) A debit to Encumbrances. C) A debit to Appropriations. […]

978-1259917059 Test Bank Chapter 3 Part 4

F. Miscellaneous ________ 1. Capital grant received by a city from a state ________ 2. Property tax levied by city ________ 3. Library use fees ________ 4. Building permit Answer: 1. C, 2. A, 3. D, 4. B Explanation: No […]

978-1259917059 Test Bank Chapter 4 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 4 Accounting for Governmental Operating Activities–Illustrative Transactions and Financial Statements 1) The government-wide statement of net position is prepared using the same measurement focus and basis of accounting as the General […]

978-1259917059 Test Bank Chapter 4 Part 2

35) The City of Pringle purchased a vehicle for the police department. If the operations of the police department are financed by general revenues, an asset would be recorded in which journal(s)? General Fund Governmental Activities A) Yes No B) […]

978-1259917059 Test Bank Chapter 4 Part 3

54) The City of Island Grove uses encumbrance accounting and its fiscal year ends on June 30. On May 6, a purchase order was approved and issued for supplies in the amount of $6,000. Island Grove received these supplies on […]

978-1259917059 Test Bank Chapter 4 Part 4

79) The county received a $10,000,000 endowment, the terms of which indicate that earnings on the endowment are to be used by health and welfare to provide medical services to low-income children. Where would the $10,000,000 be recorded? A) Special […]

978-1259917059 Test Bank Chapter 4 Part 5

38 89) During fiscal year 2020, the Town of Tonawanda issued purchase orders to various vendors in the amounts shown for the following functions of the town: General Government $ 82,500 Public Safety 148,700 Public Works 130,400 Culture and Recreation […]

978-1259917059 Test Bank Chapter 5 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 5 Accounting for General Capital Assets and Capital Projects 1) General capital assets should be distinguished from capital assets that are specifically associated with activities financed by proprietary and fiduciary funds, […]

978-1259917059 Test Bank Chapter 5 Part 2

37) During the year, a wealthy local merchant donated a building to the City of Rosewood. The original cost of the building was $300,000. Accumulated depreciation at the date of the gift amounted to $250,000. The appraised value of the […]

978-1259917059 Test Bank Chapter 5 Part 3

56) Which of the following statements is correct concerning interest expenditures incurred during the period of construction of capital projects? A) Interest expenditures may not be capitalized as part of the cost of general capital assets reported in governmental activities. […]

978-1259917059 Test Bank Chapter 5 Part 4

76) For each of the following definitions, select the key term from the list that relate to general capital assets and capital projects. A. Bond anticipation notes B. Infrastructure assets C. Service Concession Arrangements D. General capital assets E. Capital […]

978-1259917059 Test Bank Chapter 6 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 6 Accounting for General Long-Term Liabilities and Debt Service 1) The use of long-term debt is a traditional part of the fiscal policy of state and local governments. Answer: TRUE Difficulty: […]

978-1259917059 Test Bank Chapter 6 Part 2

34) Which of the following statements is true? A) Debt margin is reported in the governmental activities column of the government-wide statements. B) Debt limit represents the total amount of indebtedness of specified kinds that is allowed by law to […]

978-1259917059 Test Bank Chapter 6 Part 3

56) On June 1, Brooktown levied special assessments in the amount of $500,000, payable in 10 equal annual installments beginning on June 30. The assessment installments are intended to pay principal and interest on special assessment bonds for which the […]

978-1259917059 Test Bank Chapter 6 Part 4

68) In the current fiscal year, St. George County issued $3,000,000 in general obligation term bonds for 102. The county is required to use any accrued interest or premiums for servicing the debt issue. a. How would the bond issue […]

978-1259917059 Test Bank Chapter 7 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 7 Accounting for the Business-type Activities of State and Local Governments 1) For proprietary funds, governments generally present a statement of net position in a format that displays assets, plus deferred […]

978-1259917059 Test Bank Chapter 7 Part 2

37) The comprehensive annual financial report (CAFR) of a government should contain a statement of revenues, expenses, and changes in fund net position for: A) Both proprietary and governmental funds. B) Proprietary but not governmental funds. C) Governmental but not […]

978-1259917059 Test Bank Chapter 7 Part 3

61) How should financial information for internal service funds be reported in the government-wide financial statements? A) As part of governmental activities. B) As part of business-type activities. C) Amounts allocated proportionately between governmental and business-type activities. D) Usually as […]

978-1259917059 Test Bank Chapter 7 Part 4

70) “Enterprise funds should not be permitted to accumulate unrestricted net position, since to do so would indicate overpricing of its services.” Do you agree? Why or why not? Answer: No. It is in the best interest of taxpayers that […]

978-1259917059 Test Bank Chapter 8 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 8 Accounting for Fiduciary Activities—Custodial and Trust Funds 1) According to the GASB, control of an asset means the government must have the asset in its possession. Answer: FALSE Difficulty: 1 […]

978-1259917059 Test Bank Chapter 8 Part 2

35) The GASB provides three criteria for determining if a fiduciary relationship exists. Which of the following four is not one of the three criterion listed by the GASB? A) The assets are controlled by the government. B) The government […]

978-1259917059 Test Bank Chapter 8 Part 3

60) In financial reporting for proprietary funds and at the government-wide level, the employer’s pension expense for the period is equal to: A) The employer’s contribution. B) Annual required contribution. C) The change in the net pension liability adjusted for […]

978-1259917059 Test Bank Chapter 9 Part 1

Accounting for Governmental and Nonprofit Entities, 18e (Reck) Chapter 9 Financial Reporting of State and Local Governments 1) In accordance with GASB standards, both a general purpose government and a special purpose government can be considered primary governments if certain […]

978-1259917059 Test Bank Chapter 9 Part 2

30) Combining financial statements for nonmajor funds of a government should be included: A) In the basic financial statements. B) In the notes to the financial statements. C) As a part of the financial section of the comprehensive annual financial […]

978-1259917059 Test Bank Chapter 9 Part 3

54) On the statement of revenues, expenditures, and changes in fund balance for governmental funds, how are capital outlays reported? A) As a separate line item in the expenditures section of the statement. B) Capital outlays are allocated to the […]

978-1259917059 User Guide For Chromebook Bingham Solution

Cities of Smithville and Bingham – User Guide for Chromebook For use with McGraw-Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck | Suzanne L. Lowensohn | Daniel G. Neely Table of Contents Introduction ………………………………………………………………………………………………………………..2 […]

978-1259917059 User Guide For Windows Mac Bingham Solution

Cities of Smithville and Bingham – User Guide for Windows/Mac For use with McGraw-Hill Education Accounting for Governmental & Nonprofit Entities 18th Edition By Jacqueline L. Reck | Suzanne L. Lowensohn | Daniel G. Neely Table of Contents Introduction ………………………………………………………………………………………………………………..2 […]