Archives: Solution Manual

978-0078025631 Chapter 8 Excel Solution

Chapter 8 Solutions Manual Content 8-1 Chapter 8: Applying Excel The completed worksheet is shown below. Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 8 Solutions Manual […]

978-0078025631 Chapter 7A Lecture Note

Chapter 07A – Lecture Notes 7A-1 I. Appendix 7A: ABC action analysis (slide #1 is a title slide) Learning Objective 6: Prepare an action analysis report using activity-based costing data and interpret the report. A. Key definitions/concepts i. A conventional […]

978-0078025631 Chapter 7 Solution Manual Part 6

Exercise 7A-4 (continued) 2. The activity rates are computed by dividing the costs in the cells of the first-stage allocation above by the total activity from the top of the column. Direct Labor Support Order Processing Customer Support Total activity […]

978-0078025631 Chapter 7 Solution Manual Part 5

Problem 7-20 (continued) 5. Gallatin Carpet Cleaning appears to be losing money on the Flying N Ranch job. However, caution is advised. Some of the costs may not be avoidable and hence would have been incurred even if the Flying […]

978-0078025631 Chapter 7 Solution Manual Part 4

Problem 7-17 (45 minutes) 1. Under the traditional direct labor-hour based costing system, manufacturing overhead is applied to products using the predetermined overhead rate computed as follows: Estimated total manufacturing overhead cost Predetermined = overhead rate Estimated total direct labor […]

978-0078025631 Chapter 7 Solution Manual Part 3

Exercise 7-13 (30 minutes) 1. Activity rates are computed as follows: Activity Cost Pool (a) Estimated Overhead Cost (b) Expected Activity (a) ÷ (b) Activity Rate Machine setups …… $72,000 400 setups $180 per setup Special processing .. $200,000 5,000 […]

978-0078025631 Chapter 7 Solution Manual Part 2

Exercise 7-5 (15 minutes) Sales ($1,850 per standard model glider × 20 standard model gliders + $2,400 per custom designed glider × 3 custom designed gliders) …….. $44,200 Costs: Direct materials ($564 per standard model glider × 20 standard model […]

978-0078025631 Chapter 7 Solution Manual Part 1

Chapter 7 Activity-Based Costing: A Tool to Aid Decision Making Solutions to Questions 7-1 Activity-based costing differs from traditional costing systems in a number of ways. In activity-based costing, nonmanufacturing as well as manufacturing costs may be assigned to products. […]

978-0078025631 Chapter 7 Lecture Note Part 2

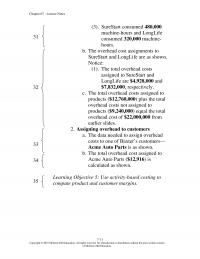

Chapter 07 – Lecture Notes 7-11 (3). SureStart consumed 480,000 machine-hours and LongLife consumed 320,000 machine- hours. b. The overhead cost assignments to SureStart and LongLife are as shown. Notice: (1). The total overhead costs assigned to SureStart and LongLife […]

978-0078025631 Chapter 7 Lecture Note Part 1

Chapter 07 – Lecture Notes 7-1 Chapter 7 Lecture Notes Chapter theme: This chapter introduces students to activity-based costing (ABC) which is a tool that has been embraced by a wide variety of service, manufacturing, and non-profit organizations. I. Activity-based […]

978-0078025631 Chapter 7 Excel Solution

Chapter 7 Solutions Manual Content 7-1 Chapter 7: Applying Excel The completed worksheet is shown below. Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 7 Solutions Manual […]

978-0078025631 Chapter 6A Lecture Note

Chapter 06A – Lecture Notes 6A-1 I. Appendix 6A: super-variable costing (slide #1 is the title slide) Learning Objective 6: Prepare an income statement using super-variable costing and reconcile this approach with variable costing. A. Super-variable costing i. The unit […]

978-0078025631 Chapter 6 Solution Manual Part 8

Exercise 6A-3 (20 minutes) 1 a. Under super–variable costing, the unit product cost for both years includes direct materials of $12. 1 b. Year 1 Year 2 Sales ………………………………………………… $2,000,000 $3,000,000 Variable cost of goods sold (@ $12 per unit) […]

978-0078025631 Chapter 6 Solution Manual Part 7

Case 6-30 (75 minutes) 1. See the segmented statement on the second following page. Supporting computations for the statement are given below: Sales: Membership dues (20,000 × $100) …………………….. $2,000,000 Assigned to Magazine Subscriptions Division (20,000 × $20) ……………………………………………. 400,000 […]

978-0078025631 Chapter 6 Solution Manual Part 6

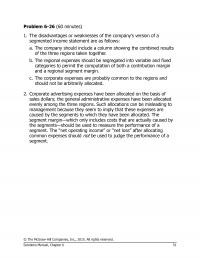

Problem 6-26 (60 minutes) 1. The disadvantages or weaknesses of the company’s version of a segmented income statement are as follows: a. The company should include a column showing the combined results of the three regions taken together. b. The […]

978-0078025631 Chapter 6 Solution Manual Part 5

Problem 6-23 (60 minutes) 1. a. Absorption costing unit product cost is: Direct materials ……………………………. $ 3.50 Direct labor …………………………………. 12.00 Variable manufacturing overhead …….. 1.00 Fixed manufacturing overhead ($300,000 ÷ 30,000 units) …………… 10.00 Absorption costing unit product cost […]

978-0078025631 Chapter 6 Solution Manual Part 4

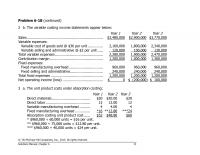

Problem 6-18 (continued) 2 b. The variable costing income statements appear below: Year 1 Year 2 Year 3 Sales ……………………………………………………………… $3,480,000 $2,900,000 $3,770,000 Variable expenses: Variable cost of goods sold @ $36 per unit ………….. 2,160,000 1,800,000 2,340,000 Variable selling […]

978-0078025631 Chapter 6 Solution Manual Part 3

Exercise 6-11 (20 minutes) 1. Division Total Company East Central West Sales ………………………… $1,000,000 $250,000 $400,000 $350,000 Variable expenses ……….. 390,000 130,000 120,000 140,000 Contribution margin …….. 610,000 120,000 280,000 210,000 Traceable fixed expenses . 535,000 160,000 200,000 175,000 Divisional […]

978-0078025631 Chapter 6 Solution Manual Part 2

Exercise 6-4 (10 minutes) Total Company Weedban Greengrow Sales* …………………………….. $300,000 $90,000 $210,000 Variable expenses** ………….. 183,000 36,000 147,000 Contribution margin …………… 117,000 54,000 63,000 Traceable fixed expenses …….. 66,000 45,000 21,000 Product line segment margin .. 51,000 $ 9,000 […]

978-0078025631 Chapter 6 Solution Manual Part 1

Chapter 6 Variable Costing and Segment Reporting: Tools for Management Solutions to Questions 6-1 Absorption and variable costing differ in how they handle fixed manufacturing overhead. Under absorption costing, fixed manufacturing overhead is treated as a product cost and hence […]

978-0078025631 Chapter 6 Lecture Note Part 2

Chapter 06 – Lecture Notes 6-10 fixed cost of the Fritos business segment of PepsiCo. (2). The maintenance cost for the building in which Boeing 747s are assembled is a traceable fixed cost of the 747 business segment of Boeing. […]

978-0078025631 Chapter 6 Lecture Note Part 1

Chapter 06 – Lecture Notes 6-1 Chapter 6 Lecture Notes Chapter theme: Two general approaches are used for valuing inventories and cost of goods sold. One approach, called absorption costing, is generally used for external reporting purposes. The other approach, […]

978-0078025631 Chapter 6 Excel Solution

Chapter 6 Solutions Manual Content 6-1 Chapter 6: Applying Excel The completed worksheet is shown below. Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 6 Solutions Manual […]

978-0078025631 Chapter 5 Solution Manual Part 8

Problem 5-31 (continued) 2. a. Line 3: Remain unchanged. Line 9: Have a steeper slope. Break-even point: Decrease. b. Line 3: Have a flatter slope. Line 9: Remain unchanged. Break-even point: Decrease. c. Line 3: Shift upward. Line 9: Remain […]

978-0078025631 Chapter 5 Solution Manual Part 7

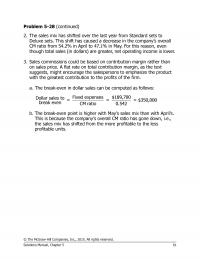

Problem 5-28 (continued) 2. The sales mix has shifted over the last year from Standard sets to Deluxe sets. This shift has caused a decrease in the company’s overall CM ratio from 54.2% in April to 47.1% in May. For […]

978-0078025631 Chapter 5 Solution Manual Part 6

Problem 5-25 (45 minutes) 1. The contribution margin per unit on the first 16,000 units is: Per Unit Sales price …………………….. $3.00 Variable expenses ……………. 1.25 Contribution margin …………. $1.75 The contribution margin per unit on anything over 16,000 units […]

978-0078025631 Chapter 5 Solution Manual Part 5

Problem 5-20 (continued) c. This problem illustrates the difficulty faced by some companies. When variable labor costs increase, it is often difficult to pass these cost increases along to customers in the form of higher prices. Thus, companies are forced […]

978-0078025631 Chapter 5 Solution Manual Part 4

Exercise 5-17 (30 minutes) 1. Profit = Unit CM × Q − Fixed expenses $0 = ($50 − $32) × Q − $108,000 $0 = ($18) × Q − $108,000 $18Q = $108,000 Q = $108,000 ÷ $18 Q = […]

978-0078025631 Chapter 5 Solution Manual Part 2

Exercise 5-3 (continued) 2. Looking at the graph, the break-even point appears to be 3,200 units. This can be verified as follows: Profit = Unit CM × Q − Fixed expenses = $5 × Q − $16,000 = $5 × […]

978-0078025631 Chapter 5 Solution Manual Part 1

Chapter 5 Cost-Volume-Profit Relationships Solutions to Questions 5-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It can also be expressed as the ratio of the contribution margin per unit to […]

978-0078025631 Chapter 5 Lecture Note Part 2

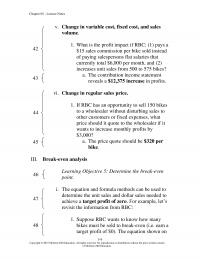

Chapter 05 – Lecture Notes 5-9 v. Change in variable cost, fixed cost, and sales volume. 1. What is the profit impact if RBC: (1) pays a $15 sales commission per bike sold instead of paying salespersons flat salaries that […]

978-0078025631 Chapter 5 Lecture Note Part 1

Chapter 05 – Lecture Notes 5-1 Chapter 5 Lecture Notes Chapter theme: Cost-volume-profit (CVP) analysis helps managers understand the interrelationships among cost, volume, and profit by focusing their attention on the interactions among the prices of products, volume of activity, […]

978-0078025631 Chapter 5 Excel Solution

Chapter 5 Solutions Manual Content 5-1 Chapter 5: Applying Excel The completed worksheet is shown below. Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 5 Solutions Manual […]

978-0078025631 Chapter 4B Lecture Note

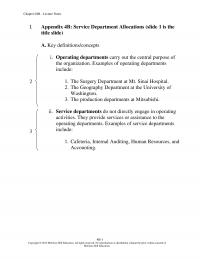

Chapter 04B – Lecture Notes 4B-1 I. Appendix 4B: Service Department Allocations (slide 1 is the title slide) A. Key definitions/concepts i. Operating departments carry out the central purpose of the organization. Examples of operating departments include: 1. The Surgery […]

978-0078025631 Chapter 4A Lecture Note

Appendix 04A – Lecture Notes 4A-1 I. Appendix 4A: FIFO method (slide 1: title slide) A. FIFO vs. weighted-average method i. The FIFO method (generally considered more accurate than the weighted-average method) differs from the weighted-average method in two ways: […]

978-0078025631 Chapter 4 Solution Manual Part 6

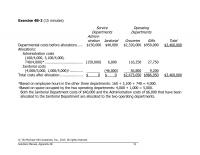

Exercise 4B-2 (15 minutes) Service Departments Operating Departments Admini- stration Janitorial Groceries Gifts Total Departmental costs before allocations ….. $150,000 $40,000 $2,320,000 $950,000 $3,460,000 Allocations: Administration costs (160/4,000, 3,100/4,000, 740/4,000)* ……………………………… (150,000) 6,000 116,250 27,750 Janitorial costs (4,000/5,000, 1,000/5,000)† ………… […]

978-0078025631 Chapter 4 Solution Manual Part 5

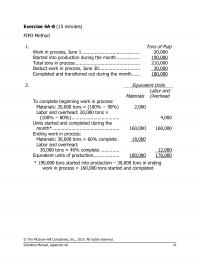

Exercise 4A-8 (15 minutes) FIFO Method 1. Tons of Pulp Work in process, June 1 …………………………………… 20,000 Started into production during the month …………….. 190,000 Total tons in process ……………………………………….. 210,000 Deduct work in process, June 30 ………………………… 30,000 Completed […]

978-0078025631 Chapter 4 Solution Manual Part 4

Case 4-20 (continued) The percentage of completion, X, affects the cost of goods sold by its effect on the unit cost, which can be determined as follows: Unit cost = $187.50 + $20,807,500 200,000 + 10,000X And the cost of […]

978-0078025631 Chapter 4 Solution Manual Part 3

Problem 4-15 (45 minutes) Weighted-Average Method 1. Equivalent units of production: Materials Conversion Transferred to next department …………………… 160,000 160,000 Ending work in process: Materials: 40,000 units x 100% complete ……. 40,000 Conversion: 40,000 units x 25% complete …… 10,000 […]

978-0078025631 Chapter 4 Solution Manual Part 2

Exercise 4-7 (10 minutes) Work in Process—Cooking ………… 42,000 Raw Materials Inventory ……… 42,000 Work in Process—Cooking ………… 50,000 Work in Process—Molding ………… 36,000 Wages Payable ………………….. 86,000 Work in Process—Cooking ………… 75,000 Work in Process—Molding ………… 45,000 Manufacturing Overhead […]

978-0078025631 Chapter 4 Lecture Note Part 2

Chapter 04 – Lecture Notes 4-8 i. Characteristics of the weighted-average method: 1. This method makes no distinction between work done in the prior and current periods. It blends together units and costs from the prior and current periods. 2. […]

978-0078025631 Chapter 4 Lecture Note Part 1

Chapter 04 – Lecture Notes 4-1 Chapter 4 Lecture Notes Chapter theme: Managers need to assign costs to products to facilitate external financial reporting and internal decision making. This chapter illustrates an absorption costing approach to calculating product costs known […]

978-0078025631 Chapter 4 Excel Solution

Chapter 4 Solutions Manual Content 4-1 Chapter 4: Applying Excel The completed worksheet is shown below. Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Chapter 4 Solutions Manual […]

978-0078025631 Chapter 3B Lecture Note

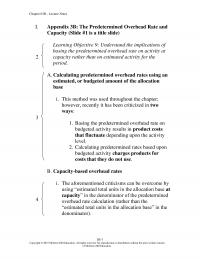

Chapter 03B – Lecture Notes 3B-1 I. Appendix 3B: The Predetermined Overhead Rate and Capacity (Slide #1 is a title slide) Learning Objective 9: Understand the implications of basing the predetermined overhead rate on activity at capacity rather than on […]

978-0078025631 Chapter 3A Lecture Note

Chapter 03A – Lecture Notes 3A-1 I. Appendix 3A: Activity-Based Absorption Costing (Slide 1 is the title slide) Learning Objective 8: Use activity-based absorption costing to compute unit product costs. A. Key definitions/concepts i. Activity-based absorption costing assigns all manufacturing […]

978-0078025631 Chapter 3 Solution Manual Part 9

Exercise 3B-1 (continued) Consequently, the income statement would appear as follows: Wixis Cabinets Income Statement Sales ……………………………………………. $43,740 Cost of goods sold (see above) ………….. 26,510 Gross margin …………………………………. 17,230 Cost of unused capacity ……………………. $1,920 Selling and administrative expenses […]

978-0078025631 Chapter 3 Solution Manual Part 8

Problem 3A-5 (60 minutes) 1. The company’s estimated direct labor-hours can be computed as fol- lows: Deluxe model: 5,000 units × 2 DLHs per unit ….. 10,000 DLHs Regular model: 40,000 units × 1 DLH per unit … 40,000 DLHs […]

978-0078025631 Chapter 3 Solution Manual Part 7

Exercise 3A-2 (45 minutes) 1. The unit product costs under the company’s conventional costing system would be computed as follows: Rascon Parcel Total Number of units produced (a) ………………… 20,000 80,000 Direct labor-hours per unit (b) ………………… 0.40 0.20 Total […]

978-0078025631 Chapter 3 Solution Manual Part 6

Problem 3-28 (60 minutes) 1. and 2. Cash Accounts Receivable Bal. 63,000 (m) 785,000 Bal. 102,000 (l) 850,000 (l) 850,000 (k) 925,000 Bal. 128,000 Bal. 177,000 Raw Materials Prepaid Insurance Bal. 30,000 (b) 200,000 Bal. 9,000 (g) 7,000 (a) 185,000 […]

978-0078025631 Chapter 3 Solution Manual Part 5

Problem 3-25 (continued) 2. Gitano Products Schedule of Cost of Goods Manufactured Direct materials: Raw materials inventory, beginning …………… $ 20,000 Add purchases of raw materials ………………… 510,000 Total raw materials available ……………………. 530,000 Deduct raw materials inventory, ending ……… […]