Problem 5-31 (continued)

2.

a.

Line 3:

Remain unchanged.

Line 9:

Have a steeper slope.

Break-even point:

Decrease.

b.

Line 3:

Have a flatter slope.

Line 9:

Remain unchanged.

Break-even point:

Decrease.

c.

Line 3:

Shift upward.

Line 9:

Remain unchanged.

Break-even point:

Increase.

d.

Line 3:

Remain unchanged.

Line 9:

Remain unchanged.

Break-even point:

Remain unchanged.

e.

Line 3:

Shift downward and have a steeper slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is uncertain.

f.

Line 3:

Have a steeper slope.

Line 9:

Have a steeper slope.

Break-even point:

Remain unchanged in terms of units; increase

in terms of total dollars of sales.

g.

Line 3:

Shift upward.

Line 9:

Remain unchanged.

Break-even point:

Increase.

h.

Line 3:

Shift upward and have a flatter slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is uncertain.

Case 5-32 (60 minutes)

Note: This is a problem that will challenge the very best students’ conceptual

1. The overall break-even sales can be determined using the CM ratio.

Velcro

Metal

Nylon

Total

Sales ……………………….

$165,000

$300,000

$340,000

$805,000

Variable expenses ………

125,000

140,000

100,000

365,000

Contribution margin …….

$ 40,000

$160,000

$240,000

440,000

Fixed expenses…………..

400,000

Net operating income ….

$ 40,000

Contribution margin $440,000

CM ratio = = = 0.5466

Sales $805,000

Fixed expenses $400,000

Dollar sales to = = = $732,000 (rounded)

break even CM ratio 0.5466

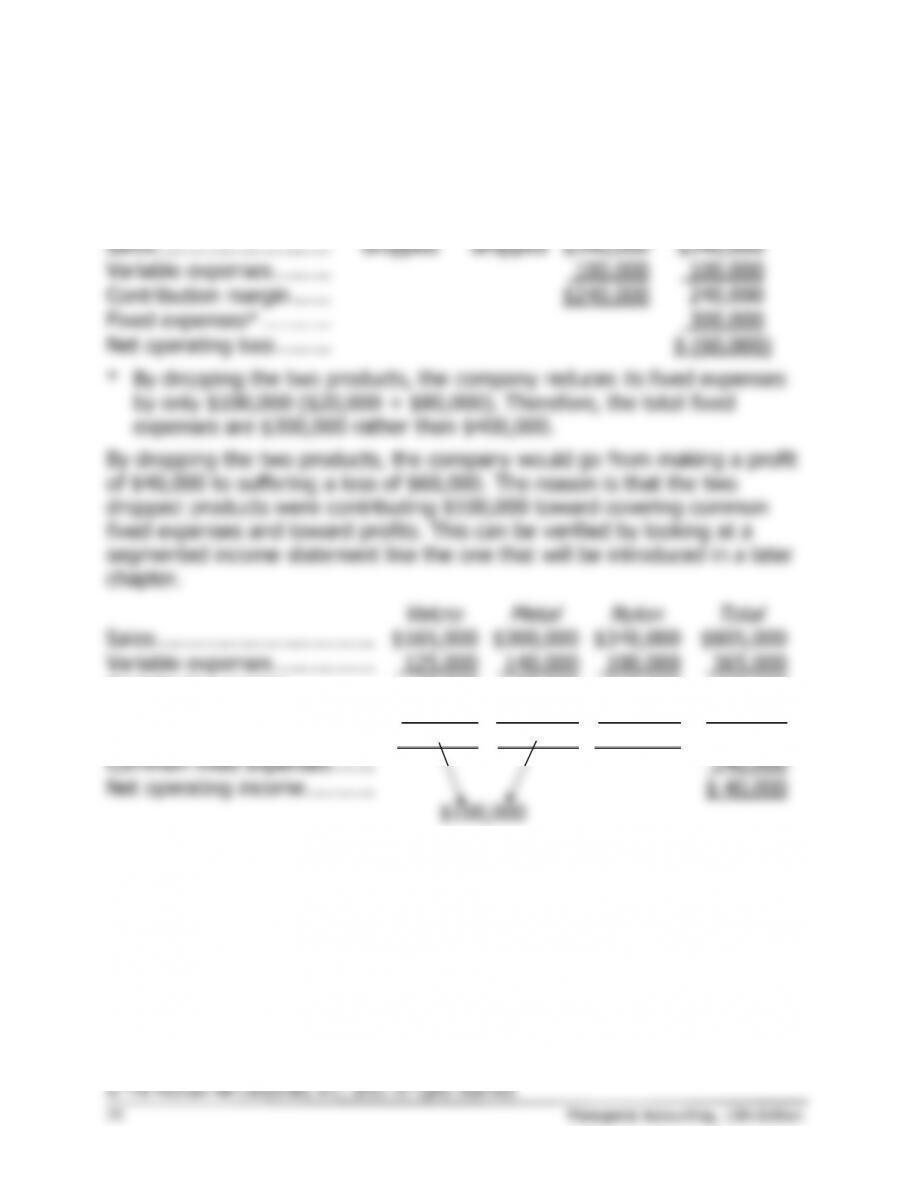

2. The issue is what to do with the common fixed cost when computing

the break-evens for the individual products. The correct approach is to

ignore the common fixed costs. If the common fixed costs are included

in the computations, the break-even points will be overstated for

Velcro

Metal

Nylon

Unit selling price ……………………………..

$1.65

$1.50

$0.85

Variable cost per unit ……………………….

1.25

0.70

0.25

Unit contribution margin (a) ………………

$0.40

$0.80

$0.60

Product fixed expenses (b)………………..

$20,000

$80,000

$60,000

Unit sales to break even (b) ÷ (a) ………

50,000

100,000

100,000

Case 5-32 (continued)

Allocation of common fixed expenses on the basis of sales revenue:

Velcro

Metal

Nylon

Total

Sales ……………………………..

$165,000

$300,000

$340,000

$805,000

Percentage of total sales ……

20.497%

37.267%

42.236%

100.0%

Allocated common fixed

expense* ……………………..

$49,193

$ 89,441

$101,366

$240,000

Product fixed expenses ……..

20,000

80,000

60,000

160,000

Allocated common and

product fixed expenses (a)

$69,193

$169,441

$161,366

$400,000

Unit contribution margin (b) .

$0.40

$0.80

$0.60

“Break–even” point in units

sold (a) ÷ (b) ………………..

172,983

211,801

268,943

*Total common fixed expense × percentage of total sales

If the company sells 172,983 units of the Velcro product, 211,801 units of

the Metal product, and 268,943 units of the Nylon product, the company

will indeed break even overall. However, the apparent break-evens for two

of the products are higher than their normal annual sales.

Velcro

Metal

Nylon

Normal annual sales volume ….

100,000

200,000

400,000

“Break–even” annual sales …….

172,983

211,801

268,943

“Strategic” decision ……………..

drop

drop

retain

It would be natural for managers to interpret a break-even for a product as

the level of sales below which the company would be financially better off

Case 5-33 (75 minutes)

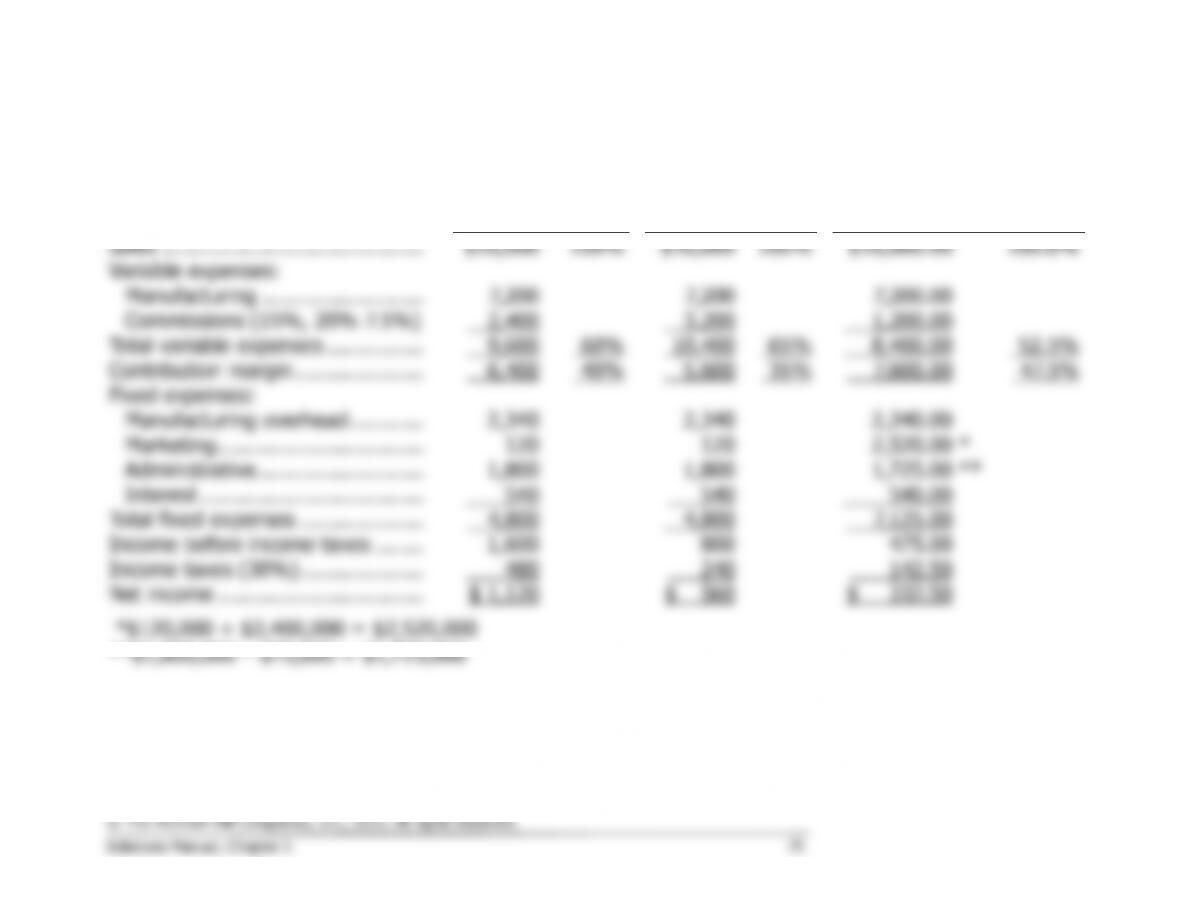

Before proceeding with the solution, it is helpful first to restructure the data into contribution format for

each of the three alternatives. (The data in the statements below are in thousands.)

15% Commission

20% Commission

Own Sales Force

Sales ……………………………………

$16,000

100%

$16,000

100%

$16,000.00

100.0%

Variable expenses:

Manufacturing ……………………..

7,200

7,200

7,200.00

Commissions (15%, 20% 7.5%)

2,400

3,200

1,200.00

Total variable expenses …………….

9,600

60%

10,400

65%

8,400.00

52.5%

Contribution margin …………………

6,400

40%

5,600

35%

7,600.00

47.5%

Fixed expenses:

Manufacturing overhead …………

2,340

2,340

2,340.00

Marketing …………………………...

120

120

2,520.00

*

Administrative ………………………

1,800

1,800

1,725.00

**

Interest ………………………………

540

540

540.00

Total fixed expenses ………………..

4,800

4,800

7,125.00

Income before income taxes ……..

1,600

800

475.00

Income taxes (30%) ………………..

480

240

142.50

Net income …………………………...

$ 1,120

$ 560

$ 332.50

*$120,000 + $2,400,000 = $2,520,000

**$1,800,000 – $75,000 = $1,725,000

Case 5-33 (continued)

X =

Total sales revenue

0.65X + $4,800,000 =

0.525X + $7,125,000

0.125X =

$2,325,000

X =

$2,325,000 ÷ 0.125

X =

$18,600,000

Thus, at a sales level of $18,600,000 either plan would yield the same

income before taxes and net income. Below this sales level, the

commission plan would yield the largest net income; above this sales

level, the sales force plan would yield the largest net income.

4. a., b., and c.

15%

Commission

20%

Commission

Own

Sales Force

Contribution margin (Part 1) (a) ….

$6,400,000

$5,600,000

$7,600,000

Income before taxes (Part 1) (b) …

$1,600,000

$800,000

$475,000

Degree of operating leverage:

(a) ÷ (b) ……………………………..

4

7

16

5. We would continue to use the sales agents for at least one more year,

and possibly for two more years. The reasons are as follows:

First, use of the sales agents would have a less dramatic effect on

net income.