Exercise 3B-1 (continued)

Consequently, the income statement would appear as follows:

Wixis Cabinets

Income Statement

Sales …………………………………………….

$43,740

Cost of goods sold (see above) …………..

26,510

Gross margin ………………………………….

17,230

Cost of unused capacity …………………….

$1,920

Selling and administrative expenses …….

8,180

10,100

Net operating income ……………………….

$ 7,130

2. When the predetermined overhead rate is based on capacity, overhead

is ordinarily underapplied because manufacturing overhead ordinarily

contains significant amounts of fixed costs. Suppose, for example, that

Exercise 3B-2 (30 minutes)

1. The overhead applied to Mrs. Brinksi’s account would be computed as

follows:

2012

2013

Estimated overhead cost (a) ………………………..

$310,500

$310,500

Estimated professional staff hours (b) ……………

4,500

4,600

Predetermined overhead rate (a) ÷ (b) …………..

$69.00

$67.50

Professional staff hours charged to Ms. Brinksi’s

account …………………………………………………

× 2.5

× 2.5

Overhead applied to Ms. Brinksi’s account……….

$172.50

$168.75

2. If the actual overhead cost and the actual professional hours charged

turn out to be exactly as estimated there would be no underapplied or

overapplied overhead.

2012

2013

Predetermined overhead rate (see above) ………

$69.00

$67.50

Actual professional staff hours charged to cli-

ents’ accounts (by assumption) ………………….

× 4,500

× 4,600

Overhead applied ………………………………………

$310,500

$310,500

Actual overhead cost incurred (by assumption) ..

310,500

310,500

Underapplied or overapplied overhead ……………

$ 0

$ 0

3. If the predetermined overhead rate is based on the professional staff

hours available, the computations would be:

2012

2013

Estimated overhead cost (a) ………………………….

$310,500

$310,500

Professional staff hours available (b) ……………….

6,000

6,000

Predetermined overhead rate (a) ÷ (b) ……………

$51.75

$51.75

Professional staff hours charged to Ms. Brinksi’s

account ………………………………………………….

× 2.5

× 2.5

Overhead applied to Ms. Brinksi’s account ………..

$129.38

$129.38

Problem 3B-3 (60 minutes)

1. The overhead applied to the Verde Baja job is computed as follows:

2012

2013

Estimated studio overhead cost (a) ……………..

$160,000

$160,000

Estimated hours of studio service (b) ……………

1,000

800

Predetermined overhead rate (a) ÷ (b) …………

$160

$200

Verde Baja job’s studio hours …………………….

× 40

× 40

Overhead applied to the Verde Baja job ……….

$6,400

$8,000

Overhead is underapplied for both years as computed below:

2012

2013

Predetermined overhead rate (see above) (a) ..

$160

$200

Actual hours of studio service provided (b) ……

750

500

Overhead applied (a) × (b) ………………………..

$120,000

$100,000

Actual studio cost incurred …………………………

160,000

160,000

Underapplied overhead ……………………………..

$ 40,000

$ 60,000

2. If the predetermined overhead rate is based on the hours of studio ser–

vice at capacity, the computations would be:

2012

2013

Estimated studio overhead cost at capacity (a)

$160,000

$160,000

Hours of studio service at capacity (b) ………….

1,600

1,600

Predetermined overhead rate (a) ÷ (b) …………

$100

$100

Verde Baja job’s studio hours …………………….

× 40

× 40

Overhead applied to the Verde Baja job ……….

$4,000

$4,000

Overhead is underapplied for both years under this method as well:

2012

2013

Predetermined overhead rate (see above) (a) ..

$100

$100

Actual hours of studio service provided (b) ……

750

500

Overhead applied (a) × (b) ………………………..

$ 75,000

$ 50,000

Actual studio cost incurred …………………………

160,000

160,000

Underapplied overhead ……………………………..

$ 85,000

$110,000

Case 3B-4 (120 minutes)

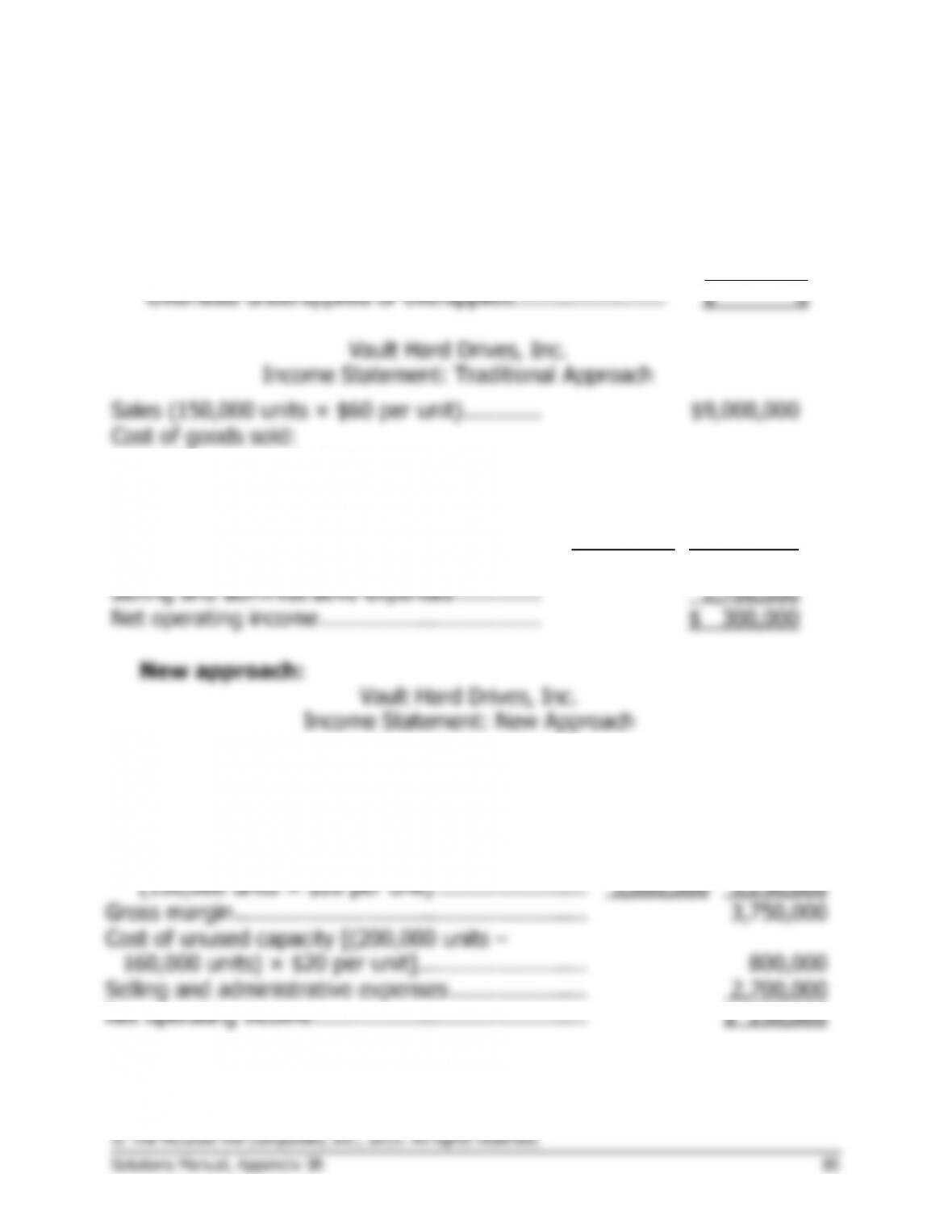

1. Traditional approach:

Actual total manufacturing overhead cost incurred

(assumed to equal the original estimate) ……………..

$4,000,000

Manufacturing overhead applied

(160,000 units × $25 per unit) ………………………….

4,000,000

Overhead underapplied or overapplied …………………..

$ 0

Vault Hard Drives, Inc.

Income Statement: Traditional Approach

Sales (150,000 units × $60 per unit) …………

$9,000,000

Cost of goods sold:

Variable manufacturing

(150,000 units × $15 per unit) ……………

$2,250,000

Manufacturing overhead applied

(150,000 units × $25 per unit) ……………

3,750,000

6,000,000

Gross margin ……………………………………….

3,000,000

Selling and administrative expenses ………….

2,700,000

Net operating income …………………………….

$ 300,000

New approach:

Vault Hard Drives, Inc.

Income Statement: New Approach

Sales (150,000 units × $60 per unit) ………………..

$9,000,000

Cost of goods sold:

Variable manufacturing

(150,000 units × $15 per unit) …………………..

$2,250,000

Manufacturing overhead applied

(150,000 units × $20 per unit) …………………..

3,000,000

5,250,000

Gross margin ………………………………………………

3,750,000

Cost of unused capacity [(200,000 units –

160,000 units) × $20 per unit] ……………………..

800,000

Selling and administrative expenses …………………

2,700,000

Net operating income …………………………..……….

$ 250,000

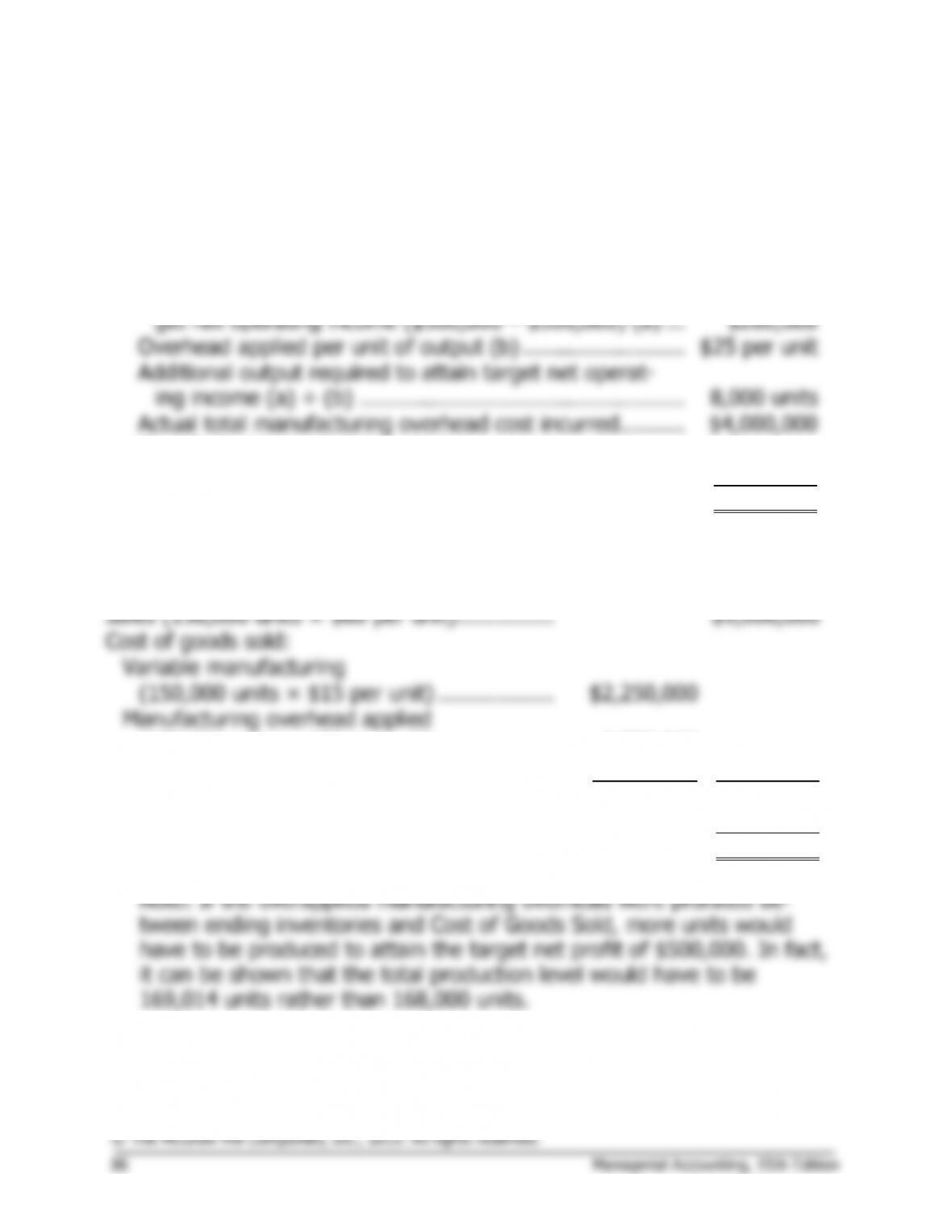

Case 3B-4 (continued)

New approach:

Under the new approach, the reported net operating income can be in-

creased by increasing the production level. This results in less of a deduc–

Additional net operating income required to attain target

net operating income ($500,000 – $250,000) (a) ……….

$250,000

Overhead applied per unit of output (b) ……………………..

$20 per unit

Additional output required to attain target net operating

income (a) ÷ (b) …………………………………………………

12,500 units

Estimated number of units produced …………………………

160,000 units

Actual number of units to be produced ………………………

172,500 units

Vault Hard Drives, Inc.

Income Statement: New Approach

Sales (150,000 units × $60 per unit) ……………….

$9,000,000

Cost of goods sold:

Variable manufacturing

(150,000 units × $15 per unit) ………………….

$2,250,000

Manufacturing overhead applied

(150,000 units × $20 per unit) ………………….

3,000,000

5,250,000

Gross margin ……………………………………………..

3,750,000

Cost of unused capacity [(200,000 units –

172,500 units) × $20 per unit] …………………….

550,000

Selling and administrative expenses ………………..

2,700,000

Net operating income …………………………………..

$ 500,000