Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 4B-2 (15 minutes)

Service

Departments

Operating

Departments

Admini-

stration

Janitorial

Groceries

Gifts

Total

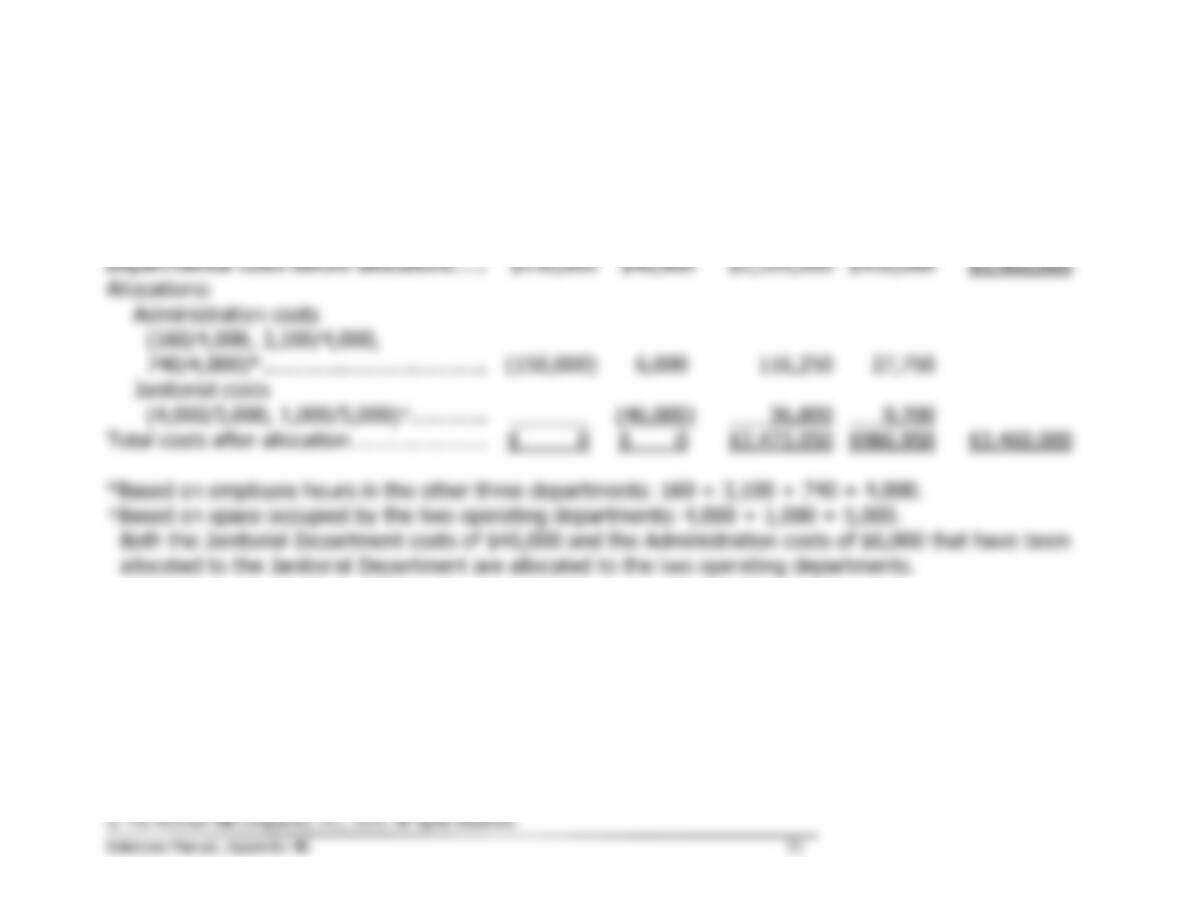

Departmental costs before allocations .....

$150,000

$40,000

$2,320,000

$950,000

$3,460,000

Allocations:

Administration costs

(160/4,000, 3,100/4,000,

740/4,000)* ....................................

(150,000)

6,000

116,250

27,750

Janitorial costs

(4,000/5,000, 1,000/5,000)† ............

(46,000)

36,800

9,200

Total costs after allocation ......................

$ 0

$ 0

$2,473,050

$986,950

$3,460,000

*Based on employee hours in the other three departments: 160 + 3,100 + 740 = 4,000.

†Based on space occupied by the two operating departments: 4,000 + 1,000 = 5,000.

Both the Janitorial Department costs of $40,000 and the Administration costs of $6,000 that have been

allocated to the Janitorial Department are allocated to the two operating departments.

Exercise 4B-3 (20 minutes)

Service

Departments

Operating

Departments

Admini-

stration

Janitorial

Mainte-

nance

Binding

Printing

Total

Costs ..............................................

$140,000

$105,000

$ 48,000

$275,000

$430,000

$998,000

Allocations:

Administration costs1:

(35/700, 140/700, 315/700,

210/700) ....................................

(140,000)

7,000

28,000

63,000

42,000

Janitorial costs2:

(20/160, 40/160, 100/160) ..........

(112,000)

14,000

28,000

70,000

Maintenance costs3: (30/90, 60/90)

(90,000)

30,000

60,000

Total cost after allocations ................

$ 0

$ 0

$ 0

$396,000

$602,000

$998,000

1Allocation base: 35 employees + 140 employees + 315 employees + 210 employees = 700 employees

2Allocation base: 20,000 square feet + 40,000 square feet + 100,000 square feet = 160,000 square feet

3Allocation base: 30,000 hours + 60,000 hours = 90,000 hours

Exercise 4B-4 (20 minutes)

Service

Departments

Operating

Departments

Admini-

stration

Janitorial

Mainte-

nance

Binding

Printing

Total

Overhead costs ............................

$140,000

$105,000

$ 48,000

$275,000

$430,000

$998,000

Allocation:

Administration costs1:

(315/525, 210/525) ................

(140,000)

84,000

56,000

Janitorial costs2:

(40/140, 100/140) ..................

(105,000)

30,000

75,000

Maintenance costs3:

(30/90, 60/90) .......................

(48,000)

16,000

32,000

Total overhead costs after

allocations ................................

$ 0

$ 0

$ 0

$405,000

$593,000

$998,000

1Allocation base: 315 employees + 210 employees = 525 employees

2Allocation base: 40,000 square feet + 100,000 square feet = 140,000 square feet

3Allocation base: 30,000 hours + 60,000 hours = 90,000 hours

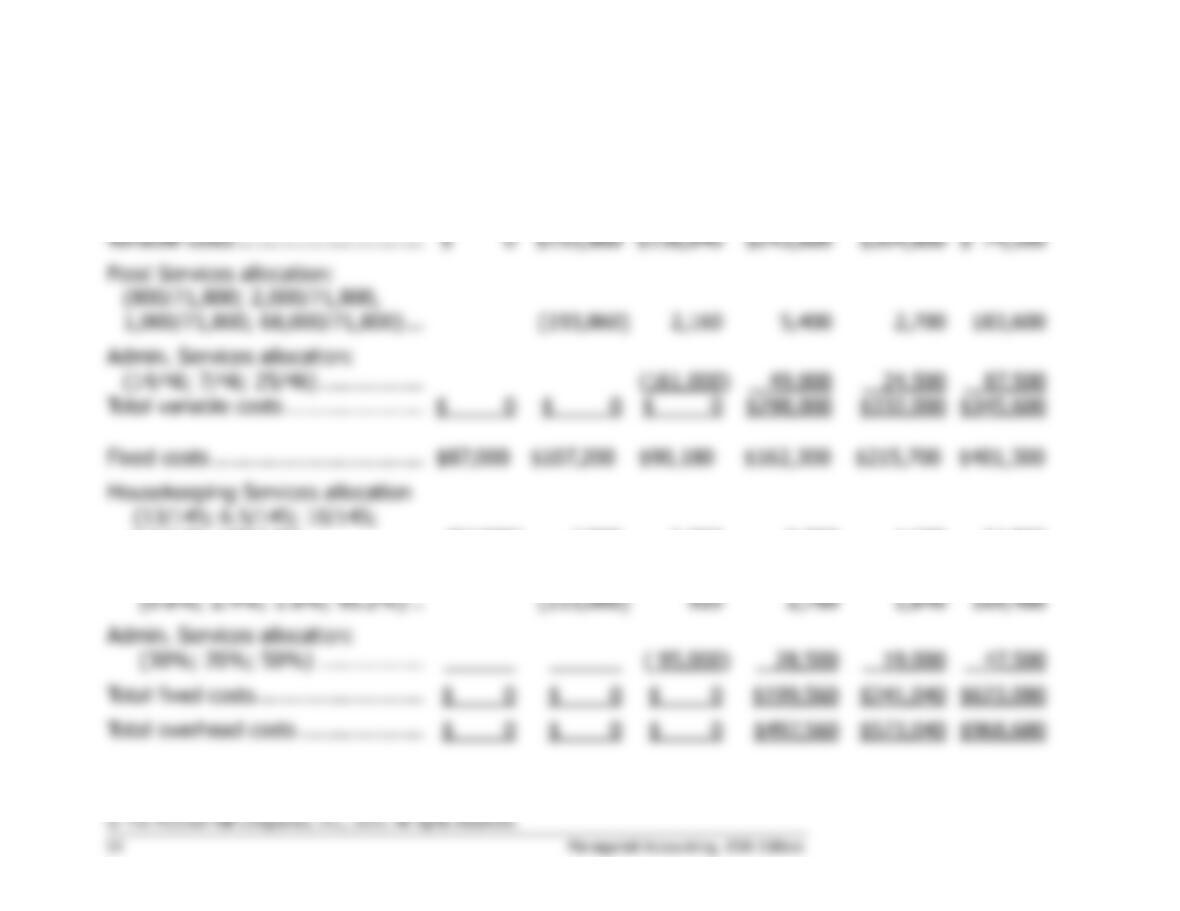

Problem 4B-5 (45 minutes)

House-

keeping

Services

Food

Services

Admini-

strative

Services

Laboratory

Radiology

General

Hospital

Variable costs ..............................

$ 0

$193,860

$158,840

$243,600

$304,800

$ 74,500

Food Services allocation:

(800/71,800; 2,000/71,800,

1,000/71,800; 68,000/71,800) ...

(193,860)

2,160

5,400

2,700

183,600

Admin. Services allocation:

(14/46; 7/46; 25/46) .................

(161,000)

49,000

24,500

87,500

Total variable costs ......................

$ 0

$ 0

$ 0

$298,000

$332,000

$345,600

Fixed costs ..................................

$87,000

$107,200

$90,180

$162,300

$215,700

$401,300

Housekeeping Services allocation

(13/145; 6.5/145; 10/145;

7.5/145; 108/145) ...................

(87,000)

7,800

3,900

6,000

4,500

64,800

Food Services allocation:

(0.8%; 2.4%; 1.6%; 95.2%) ..

(115,000)

920

2,760

1,840

109,480

Admin. Services allocation:

(30%; 20%; 50%) .................

( 95,000)

28,500

19,000

47,500

Total fixed costs ...........................

$ 0

$ 0

$ 0

$199,560

$241,040

$623,080

Total overhead costs ....................

$ 0

$ 0

$ 0

$497,560

$573,040

$968,680

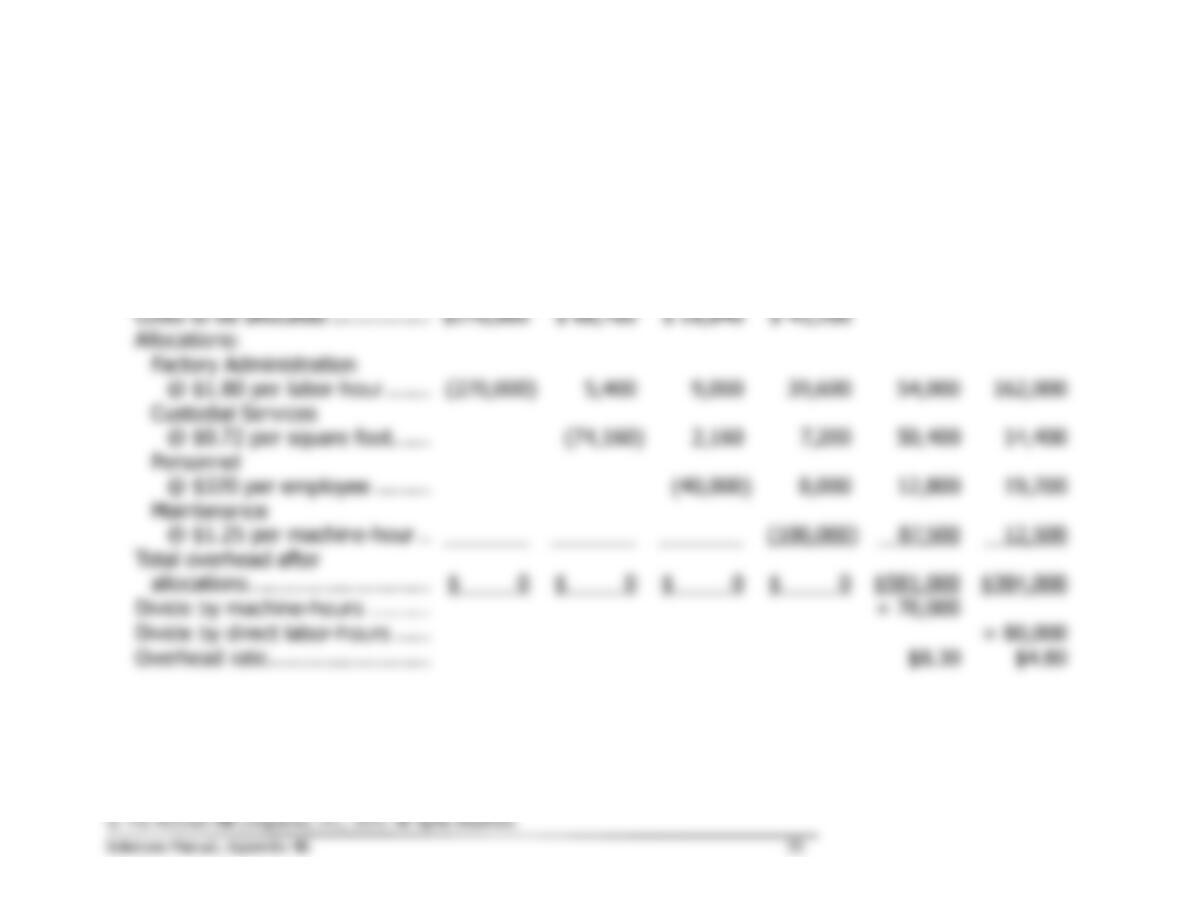

Problem 4B-6 (60 minutes)

1.

Factory

Admini-

stration

Custodial

Services

Personnel

Mainte-

nance

Machining

Assembly

Step-down method

Operating department costs ......

$376,300

$175,900

Costs to be allocated ................

$270,000

$ 68,760

$ 28,840

$ 45,200

Allocations:

Factory Administration

@ $1.80 per labor-hour .......

(270,000)

5,400

9,000

39,600

54,000

162,000

Custodial Services

@ $0.72 per square foot. .....

(74,160)

2,160

7,200

50,400

14,400

Personnel

@ $320 per employee .........

(40,000)

8,000

12,800

19,200

Maintenance

@ $1.25 per machine-hour ..

(100,000)

87,500

12,500

Total overhead after

allocations .............................

$ 0

$ 0

$ 0

$ 0

$581,000

$384,000

Divide by machine-hours ..........

÷ 70,000

Divide by direct labor-hours ......

÷ 80,000

Overhead rate ..........................

$8.30

$4.80

Problem 4B-6 (continued)

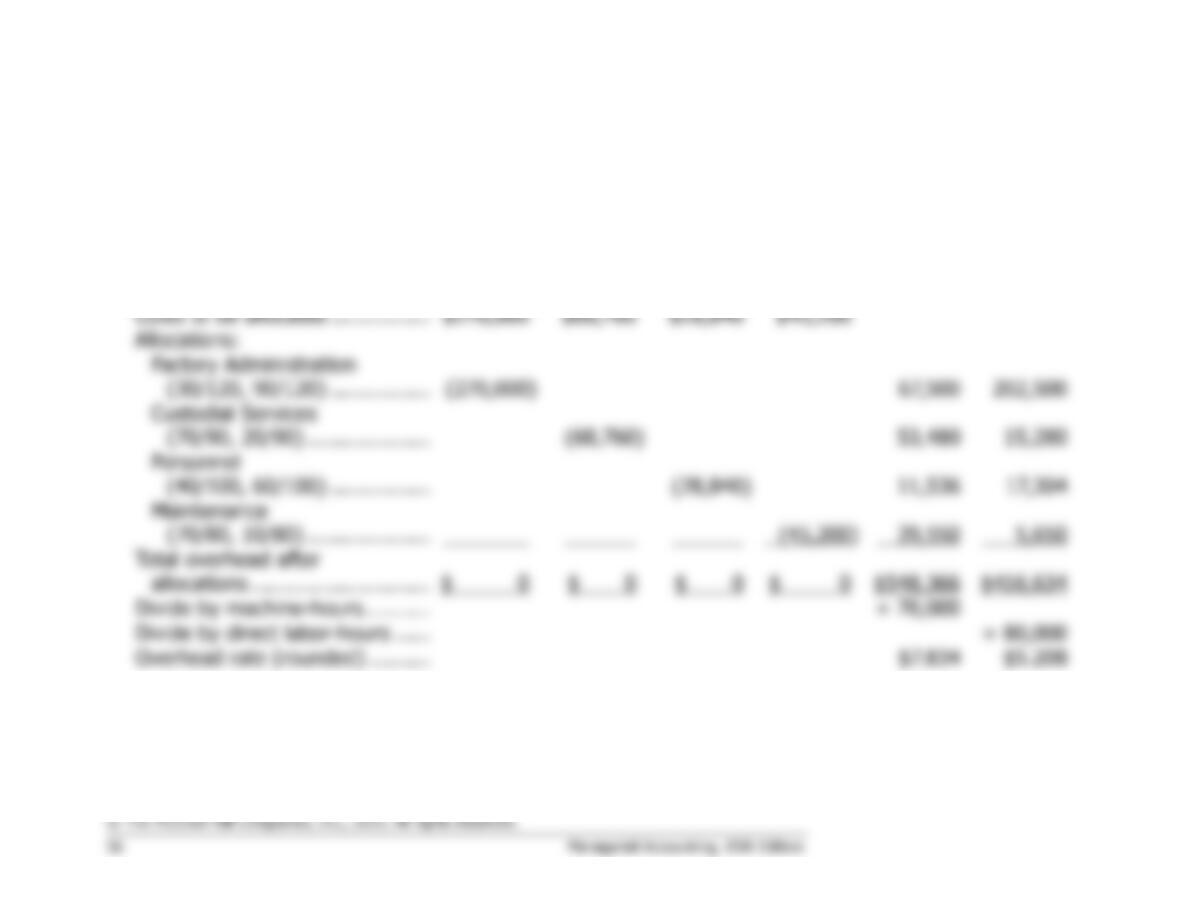

2.

Factory

Admini-

stration

Custodial

Services

Personnel

Mainte-

nance

Machining

Assembly

Direct method

Operating department costs ......

$376,300

$175,900

Costs to be allocated ................

$270,000

$68,760

$28,840

$45,200

Allocations:

Factory Administration

(30/120, 90/120) ................

(270,000)

67,500

202,500

Custodial Services

(70/90, 20/90) ....................

(68,760)

53,480

15,280

Personnel

(40/100, 60/100) ................

(28,840)

11,536

17,304

Maintenance

(70/80, 10/80) ....................

(45,200)

39,550

5,650

Total overhead after

allocations .............................

$ 0

$ 0

$ 0

$ 0

$548,366

$416,634

Divide by machine-hours...........

÷ 70,000

Divide by direct labor-hours ......

÷ 80,000

Overhead rate (rounded) ..........

$7.834

$5.208

Problem 4B-6 (continued)

3.

Plantwide rate

Total overhead cost

Overhead rate= Total direct labor-hours

$965,000

= = $9.65 per DLH

100,000 DLHs

4. The amount of overhead cost assigned to the job would be:

Step-down method:

Machining Department: $8.30 per machine-hour ×

190 machine-hours ..................................................

$1,577

Assembly Department: $4.80 per direct labor-hour ×

75 direct labor-hours ...............................................

360

Total overhead cost ......................................................

$1,937

Direct method:

Machining Department: $7.834 per machine-hour ×

190 machine-hours ..................................................

$1,488

Assembly department: $5.208 per direct labor-hour ×

75 direct labor-hours ...............................................

391

Total overhead cost ......................................................

$1,879

Plantwide method:

$9.65 per direct labor-hour × 100 direct labor-hours ....

$965

The plantwide method, which is based on direct labor-hours, assigns

very little overhead cost to the job because it requires little labor time.

Assuming that Factory Administrative costs really do vary in proportion

to labor-hours, Custodial Services with square feet occupied, and so on,

the company will tend to undercost such jobs if a plantwide overhead

rate is used (and it will tend to overcost jobs requiring large amounts of

Case 4B-7 (60 minutes)

1. Step-down method:

Personnel

Custodial

Services

Mainte-

nance

Printing

Binding

Total cost before allocations ............................

$360,000

$141,000

$201,000

$525,000

$373,500

Allocations:

Personnel (15/200, 25/200, 40/200,

120/200)1..................................................

(360,000)

27,000

45,000

72,000

216,000

Custodial services

(20/140, 80/140, 40/140)2 .........................

(168,000)

24,000

96,000

48,000

Maintenance (150/180, 30/180)3 ...................

(270,000)

225,000

45,000

Total overhead cost after allocations ................

$ 0

$ 0

$ 0

$918,000

$682,500

Divide by machine-hours .................................

150,000

Divide by direct labor-hours .............................

175,000

Predetermined overhead rate ..........................

$6.12

$3.90

1

Based on 15 + 25 + 40 + 120 = 200 employees

2

Based on 20,000 + 80,000 + 40,000 = 140,000 square feet

3

Based on 150,000 + 30,000 = 180,000 machine-hours

Case 4B-7 (continued)

2. Direct method:

Personnel

Custodial

Services

Mainte-

nance

Printing

Binding

Total costs before allocations ...........................

$360,000

$141,000

$201,000

$525,000

$373,500

Allocations:

Personnel (40/160, 120/160)1 .......................

(360,000)

90,000

270,000

Custodial Services (80/120, 40/120)2 .............

(141,000)

94,000

47,000

Maintenance (150/180, 30/180)3 ...................

(201,000)

167,500

33,500

Total overhead cost after allocations ................

$ 0

$ 0

$ 0

$876,500

$724,000

Divide by machine-hours .................................

150,000

Divide by direct labor-hours .............................

175,000

Predetermined overhead rate ..........................

$5.84

$4.14

1

Based on 40 + 120 = 160 employees

2

Based on 80,000 + 40,000 = 120,000 square feet

3

Based on 150,000 + 30,000 = 180,000 machine-hours

Case 4B-7 (continued)

3. a. The amount of overhead cost assigned to the job would be:

Step-down method

:

Printing department:

$6.12 per machine-hour × 15,400 machine-hours .......

$ 94,248

Binding department:

$3.90 per direct labor-hour × 2,000 direct labor-hours

7,800

Total overhead cost ......................................................

$102,048

Direct method

:

Printing department:

$5.84 per machine-hour × 15,400 machine-hours .......

$ 89,936

Binding department:

$4.14 per direct labor-hour × 2,000 direct labor-hours

8,280

Total overhead cost ......................................................

$ 98,216

b. The step-down method provides a better basis for computing

predetermined overhead rates than the direct method because it

gives recognition to services provided between service departments.

If this interdepartmental service is not recognized, then either too

much or too little of a service department’s costs may be allocated to

a producing department. The result will be an inaccuracy in the

producing department’s predetermined overhead rate.

Inaccuracies in the predetermined overhead rate can cause

corresponding inaccuracies in bids for jobs. Because the direct

method in this case understates the overhead rate in the Printing

Department and overstates the overhead rate in the Binding