Exercise 6A-3 (20 minutes)

1 a. Under super–variable costing, the unit product cost for both years

includes direct materials of $12.

1 b.

Year 1

Year 2

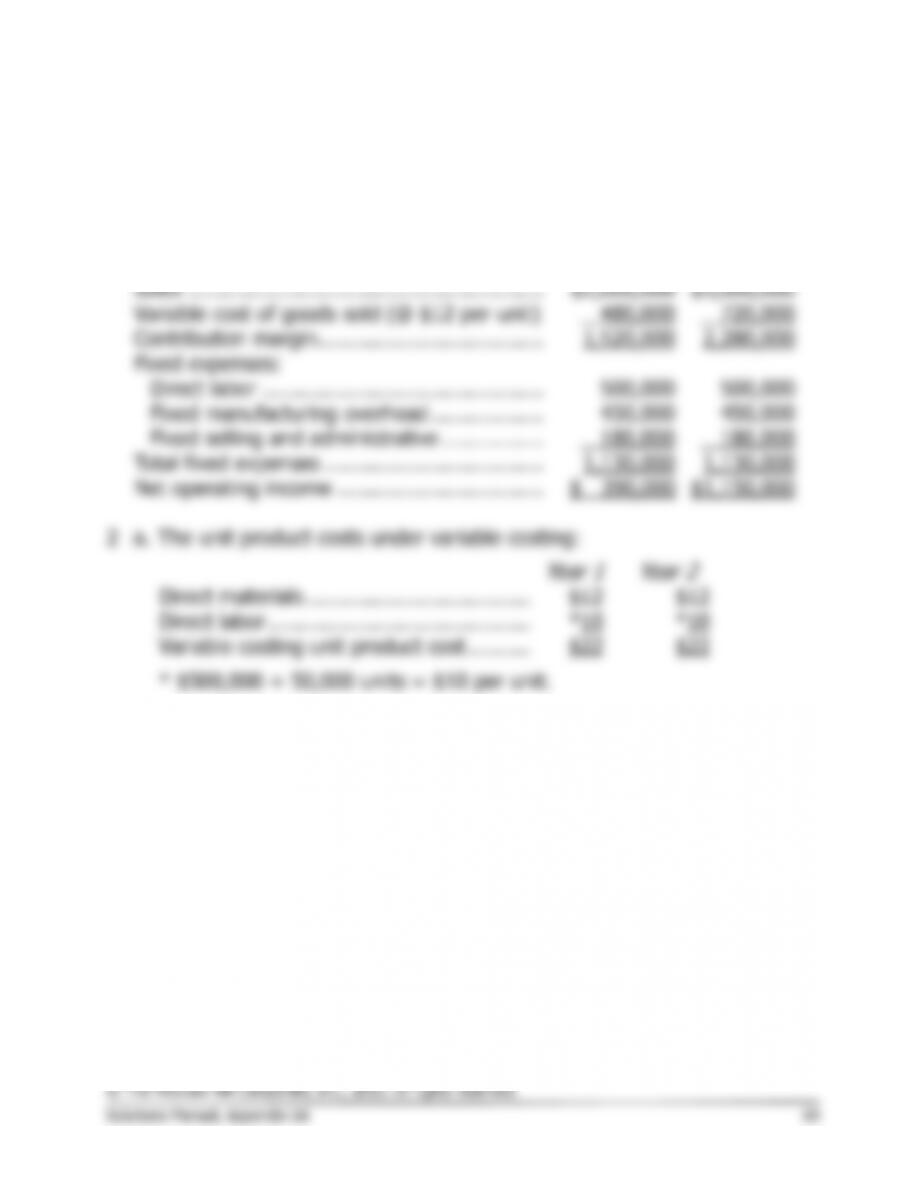

Sales …………………………………………………

$2,000,000

$3,000,000

Variable cost of goods sold (@ $12 per unit)

480,000

720,000

Contribution margin ………………………………

1,520,000

2,280,000

Fixed expenses:

Direct labor ………………………………………

500,000

500,000

Fixed manufacturing overhead ………………

450,000

450,000

Fixed selling and administrative …………….

180,000

180,000

Total fixed expenses ……………………………..

1,130,000

1,130,000

Net operating income …………………………...

$ 390,000

$1,150,000

2 a. The unit product costs under variable costing:

Year 1

Year 2

Direct materials ………………………………

$12

$12

Direct labor ……………………………………

*10

*10

Variable costing unit product cost ……….

$22

$22

* $500,000 ÷ 50,000 units = $10 per unit.

Problem 6A–4 (30 minutes)

1 a. and b. The unit product cost for all three years under super-variable costing would include direct

materials of $16 per unit. The super-variable costing income statements appear below:

Year 1

Year 2

Year 3

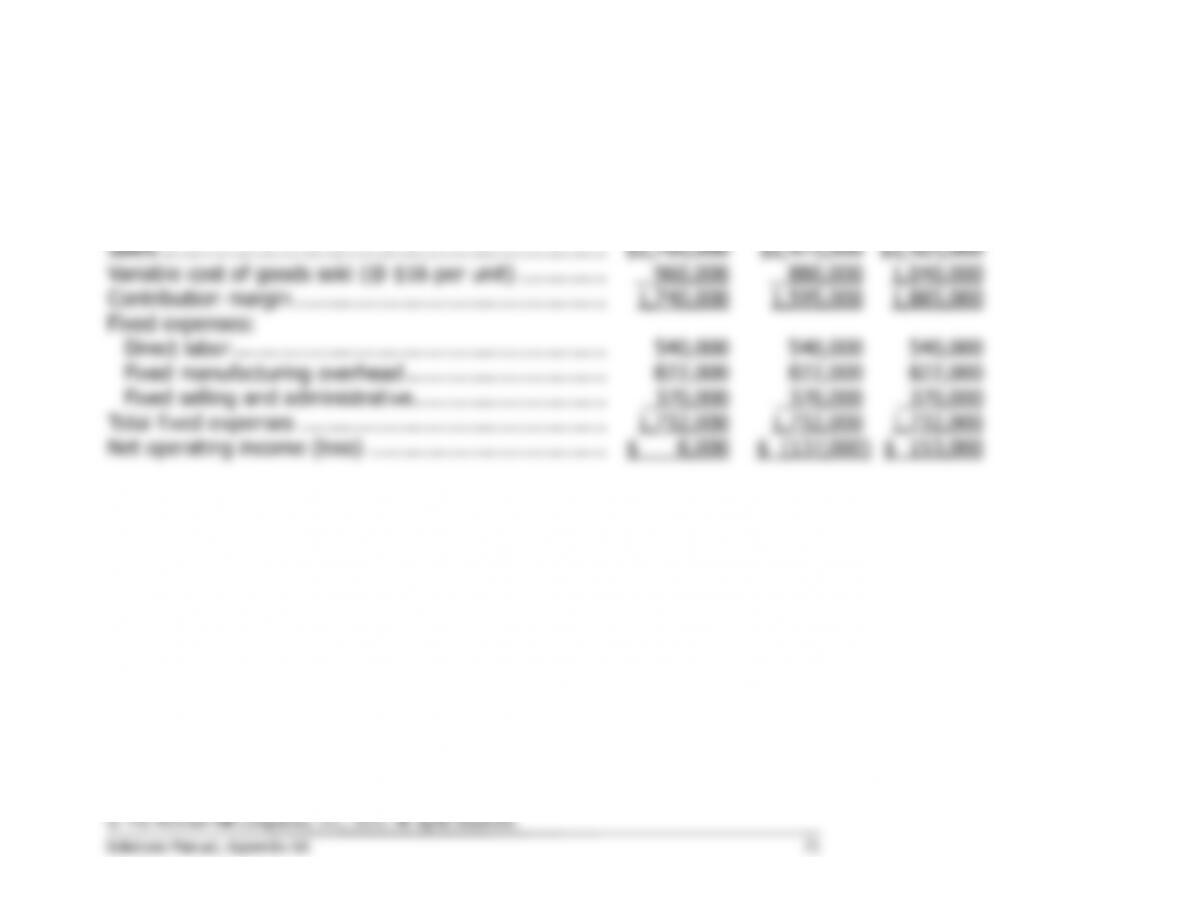

Sales ………………………………………………………………

$2,700,000

$2,475,000

$2,925,000

Variable cost of goods sold (@ $16 per unit) …………..

960,000

880,000

1,040,000

Contribution margin …………………………………………..

1,740,000

1,595,000

1,885,000

Fixed expenses:

Direct labor ……………………………………………………

540,000

540,000

540,000

Fixed manufacturing overhead …………………………..

822,000

822,000

822,000

Fixed selling and administrative ………………………….

370,000

370,000

370,000

Total fixed expenses ………………………………………….

1,732,000

1,732,000

1,732,000

Net operating income (loss) ………………………………..

$ 8,000

$ (137,000)

$ 153,000

Problem 6A–4 (continued)

2 a. The unit product costs under variable costing:

Year 1

Year 2

Year 3

Direct materials …………………………………….

$16

$16

$16

Direct labor* ………………………………………..

9

9

9

Variable costing unit product cost ……………..

$25

$25

$25

*Direct labor cost per unit for each year: $540,000 ÷ 60,000 units = $9.

2 b. The variable costing income statements appears below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$2,700,000

$2,475,000

$2,925,000

Variable cost of goods sold (@ $25 per unit) …………..

1,500,000

1,375,000

1,625,000

Contribution margin …………………………………………..

1,200,000

1,100,000

1,300,000

Fixed expenses:

Fixed manufacturing overhead …………………………..

822,000

822,000

822,000

Fixed selling and administrative ………………………….

370,000

370,000

370,000

Total fixed expenses …………………………..……………..

1,192,000

1,192,000

1,192,000

Net operating income (loss) ………………………………..

$ 8,000

$ (92,000)

$ 108,000

Problem 6A-5 (continued)

Super-variable costing net operating income …………

$8,000

Add direct labor and fixed manufacturing overhead

cost deferred in inventory under absorption

costing ……………………………………………………….

55,000

Absorption costing net operating income ……………..

$63,000