Problem 3-28 (60 minutes)

1. and 2.

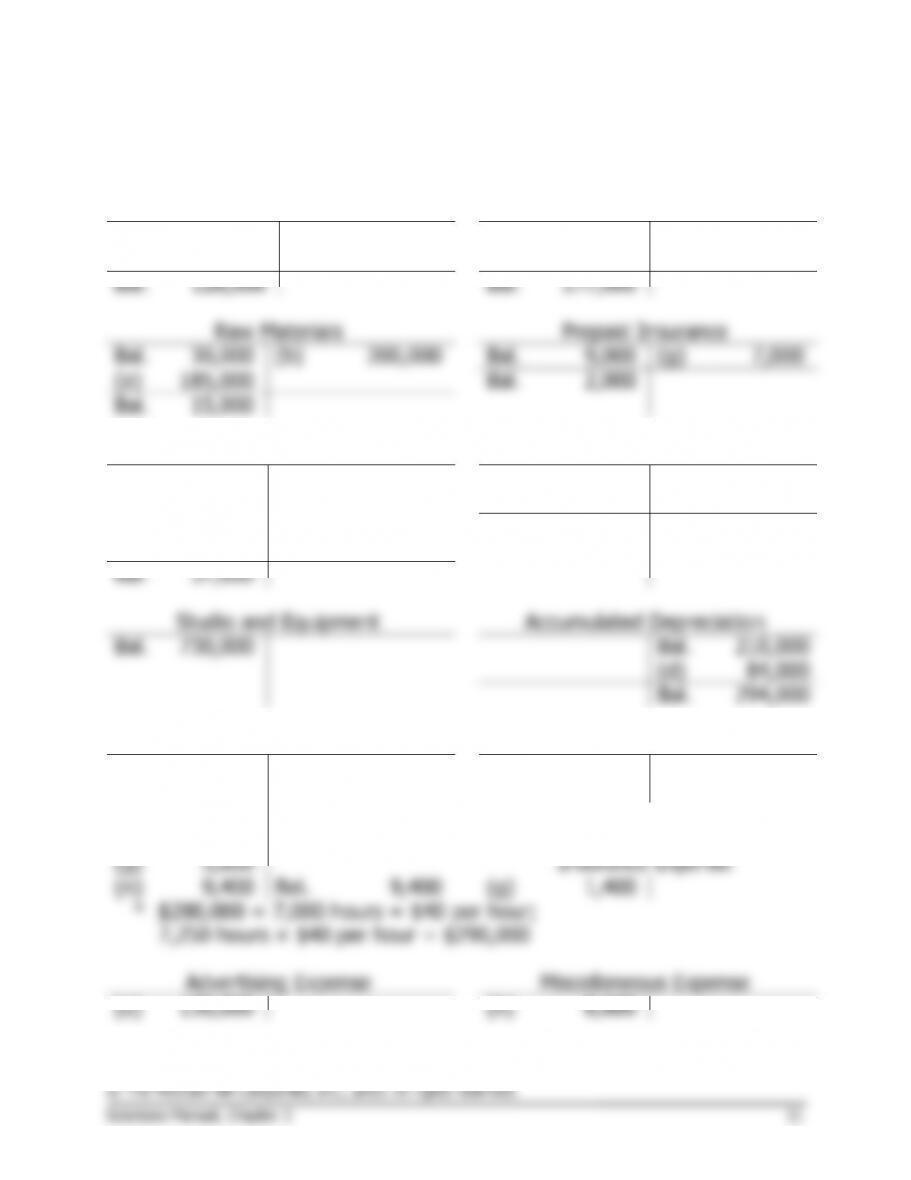

Cash

Accounts Receivable

Bal.

63,000

(m)

785,000

Bal.

102,000

(l)

850,000

(l)

850,000

(k)

925,000

Bal.

128,000

Bal.

177,000

Raw Materials

Prepaid Insurance

Bal.

30,000

(b)

200,000

Bal.

9,000

(g)

7,000

(a)

185,000

Bal.

2,000

Bal.

15,000

Videos in Process

Finished Goods

Bal.

45,000

(j)

550,000

Bal.

81,000

(k)

600,000

(b)

170,000

(j)

550,000

(f)

82,000

Bal.

31,000

(i)

290,000

Bal.

37,000

Bal.

Bal.

(d)

Bal.

(b)

30,000

* (i)

290,000

(d)

21,000

(c)

72,000

(d)

63,000

(f)

(n)

9,400

Bal.

(g)

1,400

(e)

130,000

(h)

8,600

Case 3-29 (45 minutes)

1. Shaving 5% off the estimated direct labor-hours in the predetermined

overhead rate will result in an artificially high overhead rate. The artifi–

2. This question may generate lively debate. Where should Terri Ronsin’s

loyalties lie? Is she working for the general manager of the division or

for the corporate controller? Is there anything wrong with the “Christ-

mas bonus”? How far should Terri go in bucking her boss on a new job?

cuss this situation with her immediate supervisor in the controller’s of-

Case 3-30 (60 minutes)

1.

a.

Estimated total manufacturing overhead cost

Predetermined =

overhead rate Estimated total amount of the allocation base

$840,000 140% of direct

= = labor cost

$600,000 direct labor cost

b. $9,500 × 140% = $13,300

2.

a.

Fabricating

Department

Machining

Department

Assembly

Department

Estimated manufacturing

overhead cost (a) ………

$350,000

$400,000

$ 90,000

Estimated direct labor

cost (b) ……………………

$200,000

$100,000

$300,000

Predetermined overhead

rate (a) ÷ (b) ……………

175%

400%

30%

b.

Fabricating Department:

$2,800 × 175% ………………………..

$4,900

Machining Department:

$500 × 400% …………………………..

2,000

Assembly Department:

$6,200 × 30% ………………………….

1,860

Total applied overhead …………………

$8,760

3. The bulk of the labor cost on the Koopers job is in the Assembly De-

partment, which incurs very little overhead cost. The department has an

overhead rate of only 30% of direct labor cost as compared to much

Case 3-30 (continued)

b.

Department

Fabricating

Machining

Assembly

Total Plant

Actual overhead

cost ………………….

$360,000

$420,000

$84,000

$864,000

Applied overhead

cost: …………………

$210,000 × 175% .

367,500

$108,000 × 400% .

432,000

$262,000 × 30% …

78,600

878,100

Underapplied (over-

applied) overhead

cost ………………….

$ (7,500)

$ (12,000)

$ 5,400

$ (14,100)

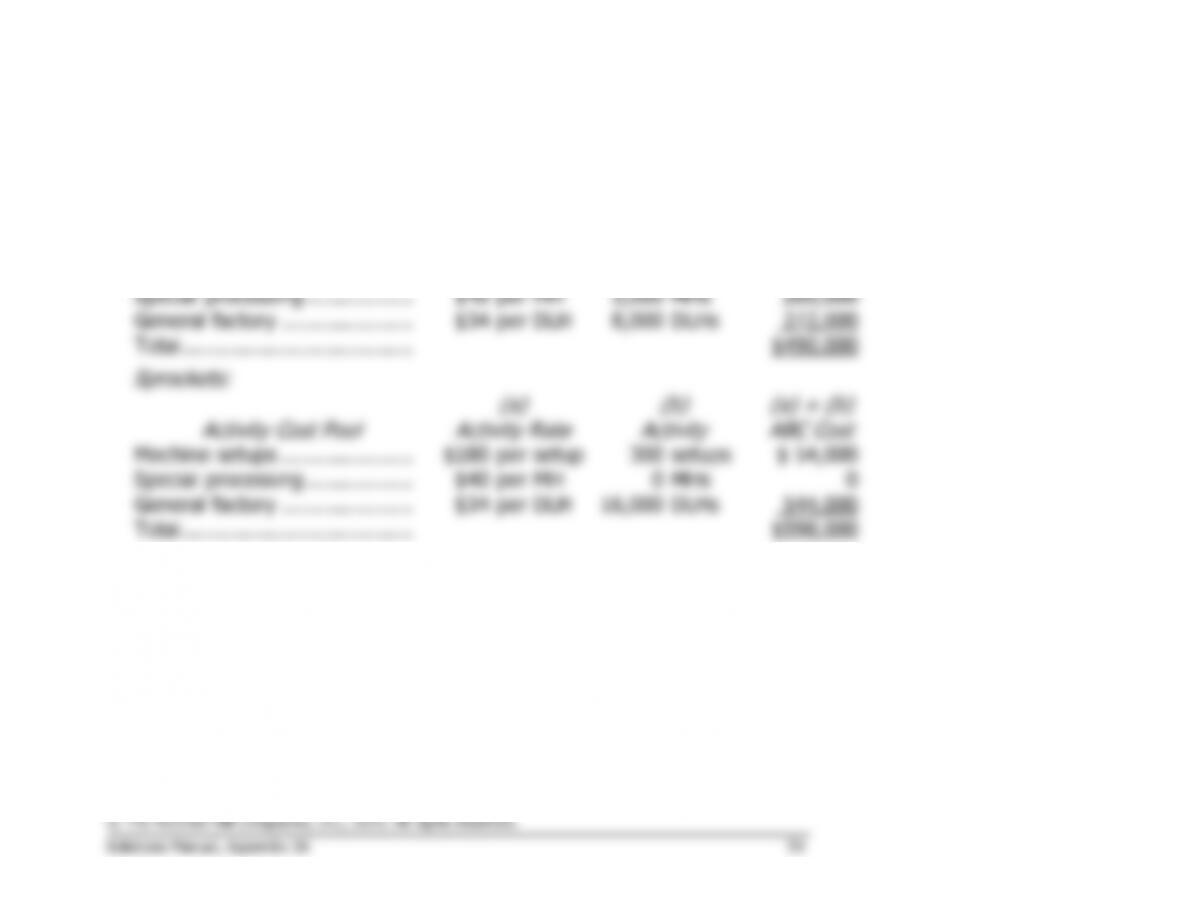

Appendix 3A

Activity-Based Absorption Costing

Exercise 3A-1 (20 minutes)

1. Activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Machine setups ……

$72,000

400

setups

$180

per setup

Special processing ..

$200,000

5,000

MHs

$40

per MH

General factory ……

$816,000

24,000

DLHs

$34

per DLH

Exercise 3A-1 (continued)

2. Overhead is assigned to the two products as follows:

Hubs:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Machine setups …………………

$180

per setup

100

setups

$ 18,000

Special processing ……………..

$40

per MH

5,000

MHs

200,000

General factory …………………

$34

per DLH

8,000

DLHs

272,000

Total ……………………………….

$490,000

Sprockets:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Machine setups …………………

$180

per setup

300

setups

$ 54,000

Special processing ……………..

$40

per MH

0

MHs

0

General factory …………………

$34

per DLH

16,000

DLHs

544,000

Total ……………………………….

$598,000