Problem 6-18 (continued)

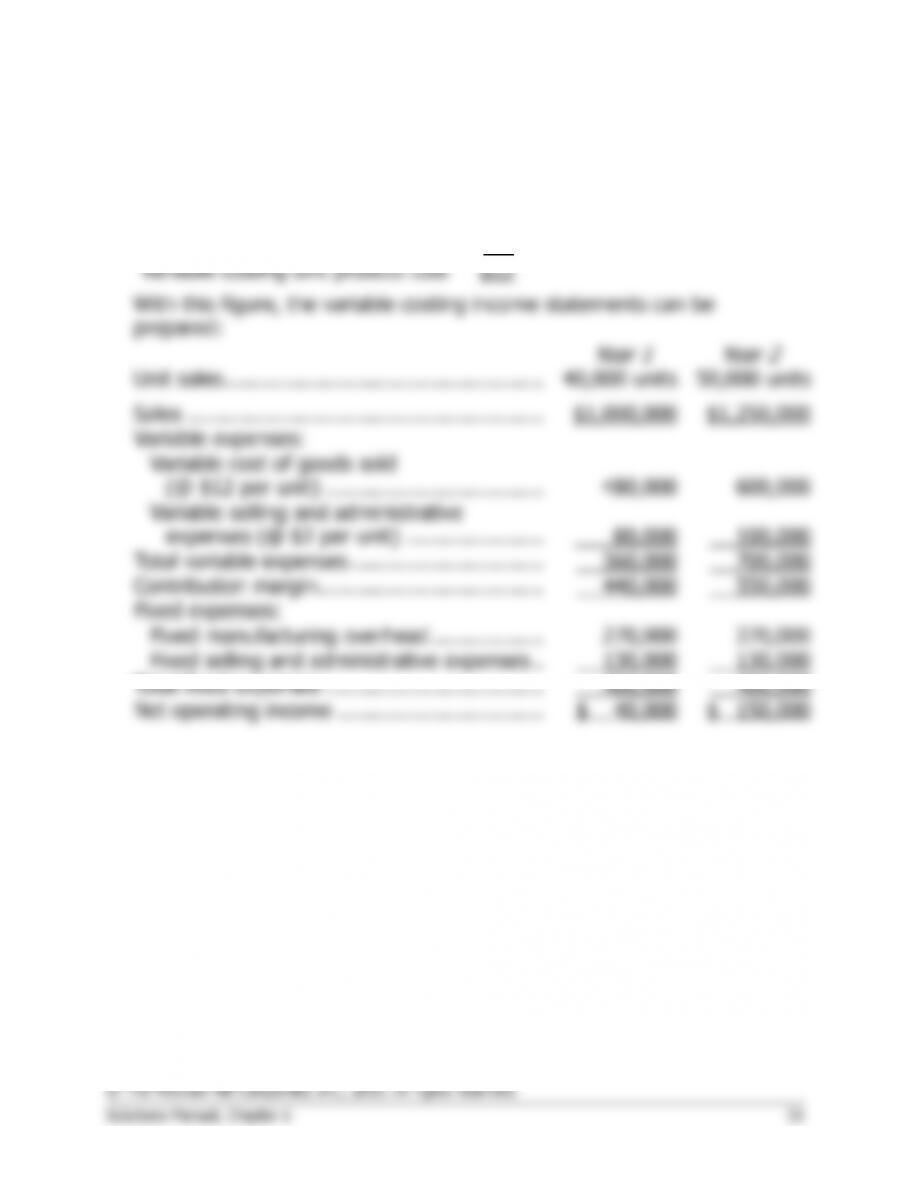

2 b. The variable costing income statements appear below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$3,480,000

$2,900,000

$3,770,000

Variable expenses:

Variable cost of goods sold @ $36 per unit …………..

2,160,000

1,800,000

2,340,000

Variable selling and administrative @ $2 per unit …..

120,000

100,000

130,000

Total variable expenses ………………………………………

2,280,000

1,900,000

2,470,000

Contribution margin …………………………………………..

1,200,000

1,000,000

1,300,000

Fixed expenses:

Fixed manufacturing overhead …………………………..

960,000

960,000

960,000

Fixed selling and administrative ………………………….

240,000

240,000

240,000

Total fixed expenses ………………………………………….

1,200,000

1,200,000

1,200,000

Net operating income (loss) ………………………………..

$ 0

$ (200,000)

$ 100,000

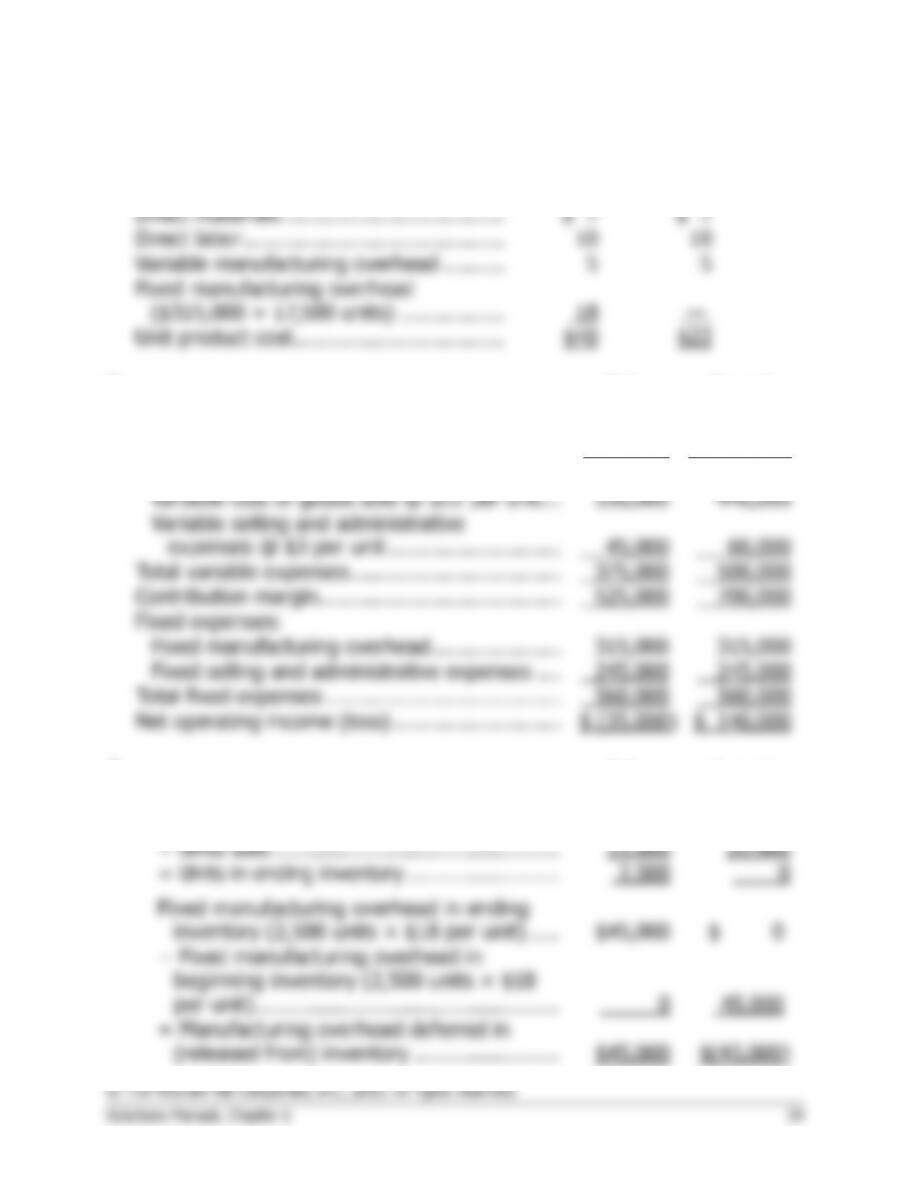

3 a. The unit product costs under absorption costing:

Year 1

Year 2

Year 3

Direct materials ………………………………

$20

$20.00

$20

Direct labor ……………………………………

12

12.00

12

Variable manufacturing overhead ……….

4

4.00

4

Fixed manufacturing overhead …………..

*16

**12.80

***24

Absorption costing unit product cost ……

$52

$48.80

$60

* $960,000 ÷ 60,000 units = $16 per unit.

** $960,000 ÷ 75,000 units = $12.80 per unit.

*** $960,000 ÷ 40,000 units = $24 per unit.