Problem 4-15 (45 minutes)

Weighted-Average Method

1.

Equivalent units of production:

Materials

Conversion

Transferred to next department ……………………

160,000

160,000

Ending work in process:

Materials: 40,000 units x 100% complete …….

40,000

Conversion: 40,000 units x 25% complete ……

10,000

Equivalent units of production ……………………..

200,000

170,000

2.

Cost per Equivalent Unit

Materials

Conversion

Cost of beginning work in process …………….

$ 25,200

$ 24,800

Cost added during the period …………………..

334,800

238,700

Total cost (a) ……………………………………….

$360,000

$263,500

Equivalent units of production (b) …………….

200,000

170,000

Cost per equivalent unit, (a) ÷ (b) ……………

$1.80

$1.55

3.

Applying costs to units:

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

40,000

10,000

Cost per equivalent unit …….

$1.80

$1.55

Cost of ending work in process

inventory ………………………

$72,000

$15,500

$87,500

Units completed and transferred out:

Units transferred to the next

department …………………..

160,000

160,000

Cost per equivalent unit …….

$1.80

$1.55

Cost of units completed and

transferred out ……………….

$288,000

$248,000

$536,000

Problem 4-15 (continued)

4.

Cost reconciliation:

Costs to be accounted for:

Cost of beginning work in process inventory

($25,200 + $24,800) …………………………….

$ 50,000

Costs added to production during the period

($334,800 + $238,700) …………………………

573,500

Total cost to be accounted for …………………..

$623,500

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 87,500

Cost of units completed and transferred out ..

536,000

Total cost accounted for ………………………….

$623,500

Problem 4-16 (45 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department* ………………….

95,000

95,000

Ending work in process:

Materials: 15,000 units x 60% complete ………

9,000

Conversion: 15,000 units x 20% complete ……

3,000

Equivalent units of production ……………………..

104,000

98,000

*Units transferred to the next department = Units in beginning work in

process + Units started into production − Units in ending work in

process = 10,000 + 100,000 − 15,000 = 95,000

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

$ 1,500

$ 7,200

Cost added during the period …………………..

154,500

90,800

Total cost (a) ……………………………………….

$156,000

$98,000

Equivalent units of production (b) …………….

104,000

98,000

Cost per equivalent unit, (a) ÷ (b) ……………

$1.50

$1.00

3.

Cost of ending work in process inventory and units transferred out

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production…

9,000

3,000

Cost per equivalent unit ………..

$1.50

$1.00

Cost of ending work in process

inventory ………………………….

$13,500

$3,000

$16,500

Units completed and transferred out:

Units transferred to the next

department ………………………

95,000

95,000

Cost per equivalent unit ………..

$1.50

$1.00

Cost of units completed and

transferred out …………………..

$142,500

$95,000

$237,500

Problem 4-16 (continued)

4.

Cost Reconciliation

Costs to be accounted for:

Cost of beginning work in process inventory

($1,500 + $7,200) ……………………………….

$ 8,700

Costs added to production during the period

($154,500 + $90,800) …………………………..

245,300

Total cost to be accounted for …………………..

$254,000

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 16,500

Cost of units completed and transferred out ..

237,500

Total cost accounted for ………………………….

$254,000

Problem 4-17 (45 minutes)

Weighted-Average Method

1.

a.

Work in Process—Refining Department ………

495,000

Work in Process—Blending Department ……..

115,000

Raw Materials ………………………………….

610,000

b.

Work in Process—Refining Department ………

72,000

Work in Process—Blending Department ……..

18,000

Salaries and Wages Payable ……………….

90,000

c.

Manufacturing Overhead ………………………..

225,000

Accounts Payable ……………………………..

225,000

d.

Work in Process—Refining Department ………

181,000

Manufacturing Overhead ……………………

181,000

d.

Work in Process—Blending Department ……..

42,000

Manufacturing Overhead ……………………

42,000

e.

Work in Process—Blending Department ……..

740,000

Work in Process—Refining Department …

740,000

f.

Finished Goods …………………………………….

950,000

Work in Process—Blending Department …

950,000

g.

Accounts Receivable ………………………………

1,500,000

Sales ……………………………………………..

1,500,000

Cost of Goods Sold ………………………………..

900,000

Finished Goods ………………………………..

900,000

Problem 4-17 (continued)

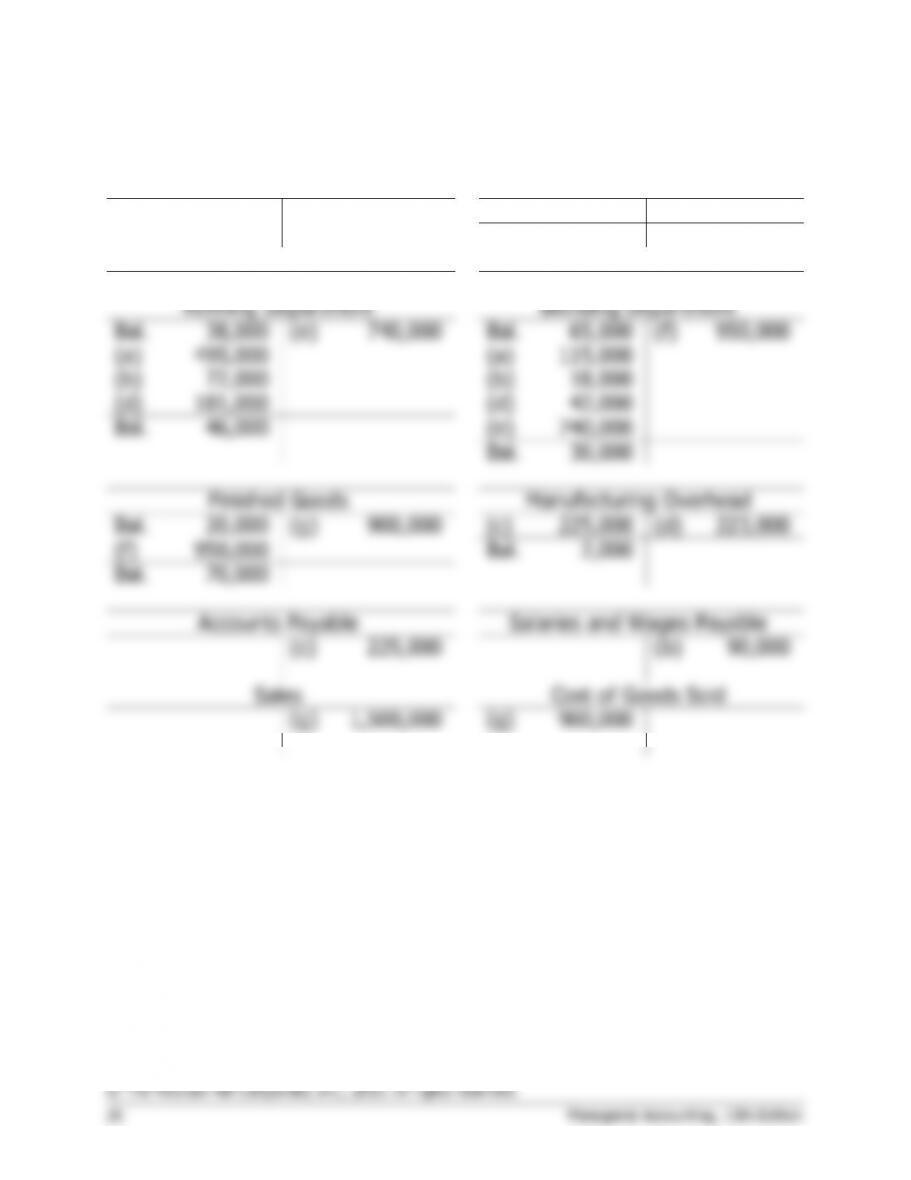

2.

Accounts Receivable

Raw Materials

(g)

1,500,000

Bal.

618,000

(a)

610,000

Bal.

8,000

Work in Process

Refining Department

Work in Process

Blending Department

Bal.

38,000

(e)

740,000

Bal.

65,000

(f)

950,000

(a)

495,000

(a)

115,000

(b)

72,000

(b)

18,000

(d)

181,000

(d)

42,000

Bal.

46,000

(e)

740,000

Bal.

30,000

Finished Goods

Manufacturing Overhead

Bal.

20,000

(g)

900,000

(c)

225,000

(d)

223,000

(f)

950,000

Bal.

2,000

Bal.

70,000

Accounts Payable

Salaries and Wages Payable

(c)

225,000

(b)

90,000

Sales

Cost of Goods Sold

(g)

1,500,000

(g)

900,000

© The McGraw-Hill Companies, Inc., 2015. All rights reserved.

Solutions Manual, Chapter 4 27

Problem 4-18 (30 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department ……………………

190,000

190,000

Ending work in process:

Materials: 40,000 units x 75% complete ………

30,000

Conversion: 40,000 units x 60% complete ……

24,000

Equivalent units of production ……………………..

220,000

214,000

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

$ 67,800

$ 30,200

Cost added during the period …………………..

579,000

248,000

Total cost (a) ……………………………………….

$646,800

$278,200

Equivalent units of production (b) …………….

220,000

214,000

Cost per equivalent unit, (a) ÷ (b) ……………

$2.94

$1.30

3.

Total units transferred …………………………...

190,000

Less units in the beginning inventory …………

30,000

Units started and completed during April ……

160,000

Note: This answer assumes that the units in the beginning inventory

are completed before any other units are completed.

4. No, the manager should not be rewarded for good cost control. The

Mixing Department’s low unit cost for April occurred because the costs

Case 4-19 (45 minutes)

Weighted-Average Method

1. The revised computations follow:

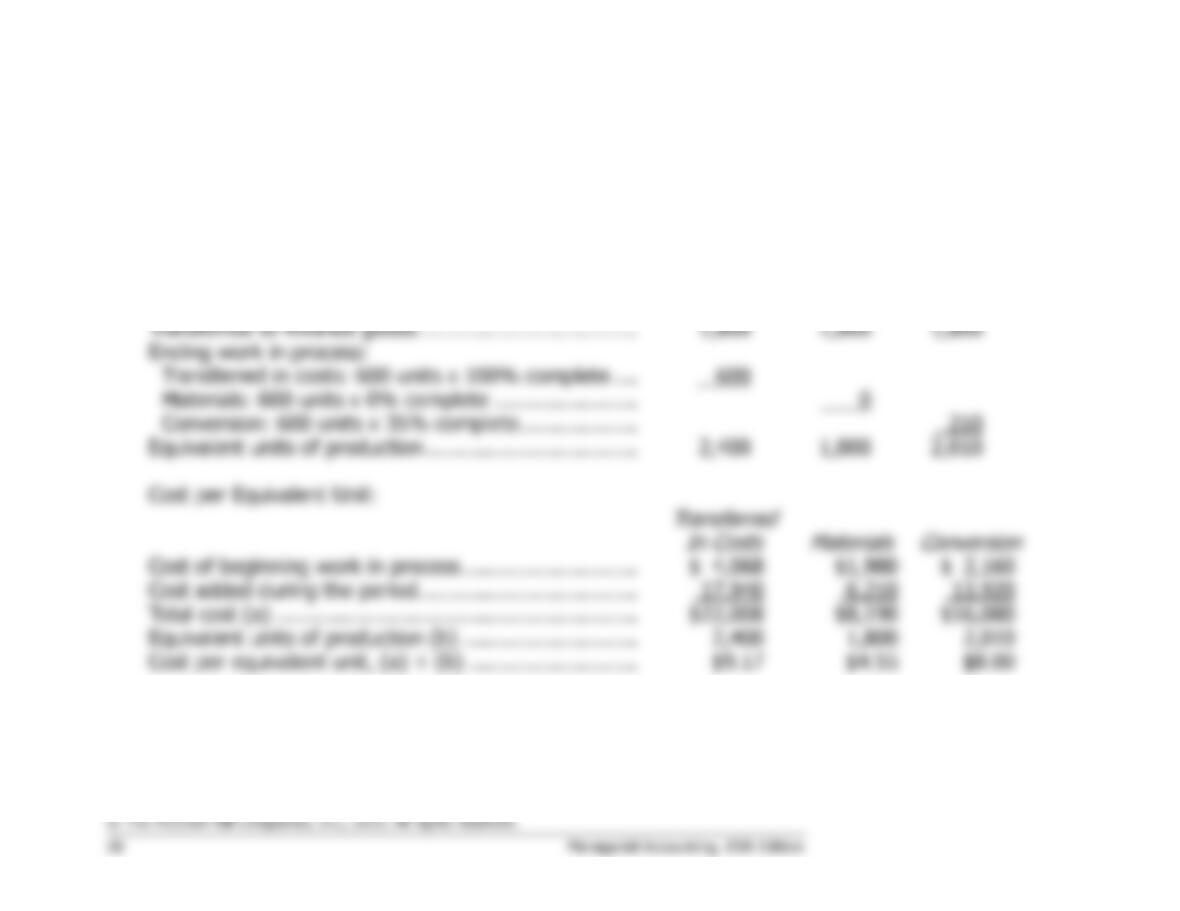

Equivalent Units of Production:

Transferred

In Costs

Materials

Conversion

Transferred to finished goods ……………………………..

1,800

1,800

1,800

Ending work in process:

Transferred in costs: 600 units x 100% complete ….

600

Materials: 600 units x 0% complete …………………..

0

Conversion: 600 units x 35% complete……………….

210

Equivalent units of production …………………………....

2,400

1,800

2,010

Cost per Equivalent Unit:

Transferred

In Costs

Materials

Conversion

Cost of beginning work in process ……………………….

$ 4,068

$1,980

$ 2,160

Cost added during the period ……………………………..

17,940

6,210

13,920

Total cost (a) ………………………………………………….

$22,008

$8,190

$16,080

Equivalent units of production (b) ……………………….

2,400

1,800

2,010

Cost per equivalent unit, (a) ÷ (b) ………………………

$9.17

$4.55

$8.00

Case 4-19 (continued)

Transferred

In Costs

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production (see above) ..

600

0

210

Cost per equivalent unit ………………………..

$9.17

$4.55

$8.00

Cost of ending work in process inventory ….

$5,502

$0

$1,680

$7,182

Units completed and transferred out:

Units transferred to finished goods ……..

1,800

1,800

1,800

Cost per equivalent unit ………………………..

$9.17

$4.55

$8.00

Cost of units completed and transferred out

$16,506

$8,190

$14,400

$39,096

2. The unit cost computed above is $21.72 (= $9.17 + $4.55 + $8.00) versus $25.71 on the original

Case 4-20 (90 minutes)

• This case is difficult—particularly part 3, which requires analytical skills.

1.

Computation of the Cost of Goods Sold:

Transferred In

Conversion

Units completed and sold …………………..

200,000

200,000

Ending work in process:

Transferred in:

10,000 units × 100% complete ……….

10,000

Conversion:

10,000 units × 30% complete …………

3,000

Equivalent units of production …………….

210,000

203,000

Transferred In

Conversion

Cost of beginning work in process ……….

$ 0

$ 0

Cost added during the period ……………..

39,375,000

20,807,500

Total cost (a) ………………………………….

$39,375,000

$20,807,500

Equivalent units of production (b) ……….

210,000

203,000

Cost per equivalent unit, (a) ÷ (b) ………

$187.50

$102.50

Cost of goods sold = 200,000 units × ($187.50 per unit + $102.50 per

unit) = $58,000,000

2. The estimate of the percentage completion of ending work in process

inventories affects the unit costs of finished goods and therefore the

3. Increasing the percentage of completion can increase net operating

income by reducing the cost of goods sold. To increase net operating