Problem 7-17 (45 minutes)

1. Under the traditional direct labor-hour based costing system,

manufacturing overhead is applied to products using the predetermined

overhead rate computed as follows:

Estimated total manufacturing overhead cost

Predetermined =

overhead rate Estimated total direct labor –hours

$1,980,000

= = $16.50 per DLH

120,000 DLHs *

*20,000 units of Xtreme @ 2.00 DLH per unit + 80,000 units of the

Pathfinder@ 1.0 DLH per unit = 40,000 DLHs + 80,000 DLHs = 120,000

DLHs.

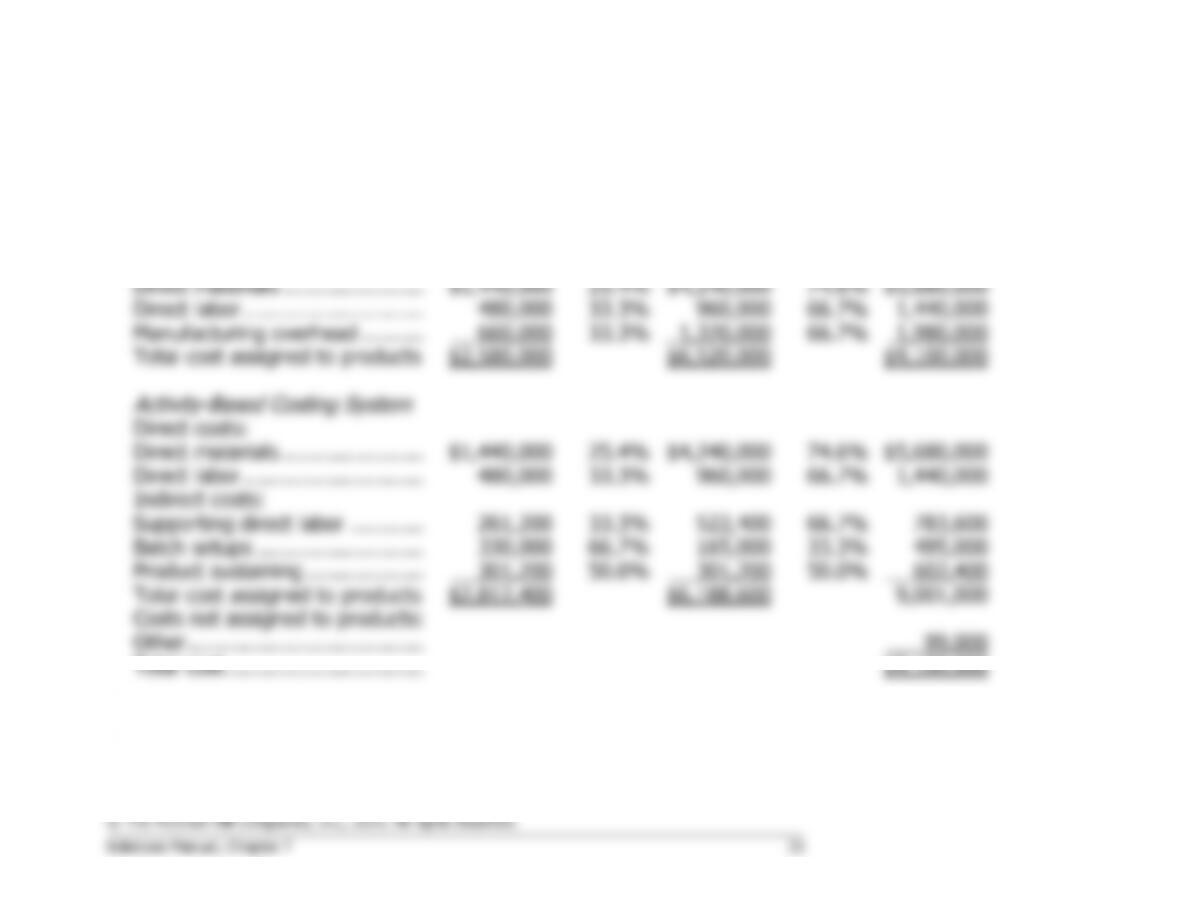

Consequently, the product margins using the traditional approach would

be computed as follows:

Xtreme

Pathfinder

Total

Sales ……………………………..

$2,800,000

$7,920,000

$10,720,000

Direct materials ………………..

1,440,000

4,240,000

5,680,000

Direct labor ……………………..

480,000

960,000

1,440,000

Manufacturing overhead

applied @ $16.50 per

direct labor-hour …………….

660,000

1,320,000

1,980,000

Total manufacturing cost ……

2,580,000

6,520,000

9,100,000

Product margin ………………..

$ 220,000

$1,400,000

$ 1,620,000

Problem 7-17 (continued)

2. The first step is to determine the activity rates:

Activity Cost Pools

(a)

Total

Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Supporting direct

labor ……………….

$783,600

120,000

DLH

$6.53

per DLH

Batch setups ……….

$495,000

300

setups

$1,650

per setup

Product sustaining ..

$602,400

2

products

$301,200

per product

*The Other activity cost pool is not shown above because it includes

organization-sustaining and idle capacity costs that should not be

assigned to products.

Under the activity-based costing system, the product margins would be

computed as follows:

Xtreme

Pathfinder

Total

Sales …………………………..

$2,800,000

$7,920,000

$10,720,000

Direct materials ……………..

1,440,000

4,240,000

5,680,000

Direct labor …………………..

480,000

960,000

1,440,000

Supporting direct labor ……

261,200

522,400

783,600

Batch setups …………………

330,000

165,000

495,000

Product sustaining ………….

301,200

301,200

602,400

Total cost …………………….

2,812,400

6,188,600

9,001,000

Product margin ……………..

$ (12,400)

$1,731,400

$ 1,719,000

Problem 7-17 (continued)

The traditional and activity-based cost assignments differ for two

reasons. First, the traditional system assigns all $1,980,000 of

66.7% of all overhead to the Pathfinder product line. The ABC system

assigns 66.7% of Batch setup costs (a batch-level activity) to the

Problem 7-18 (continued)

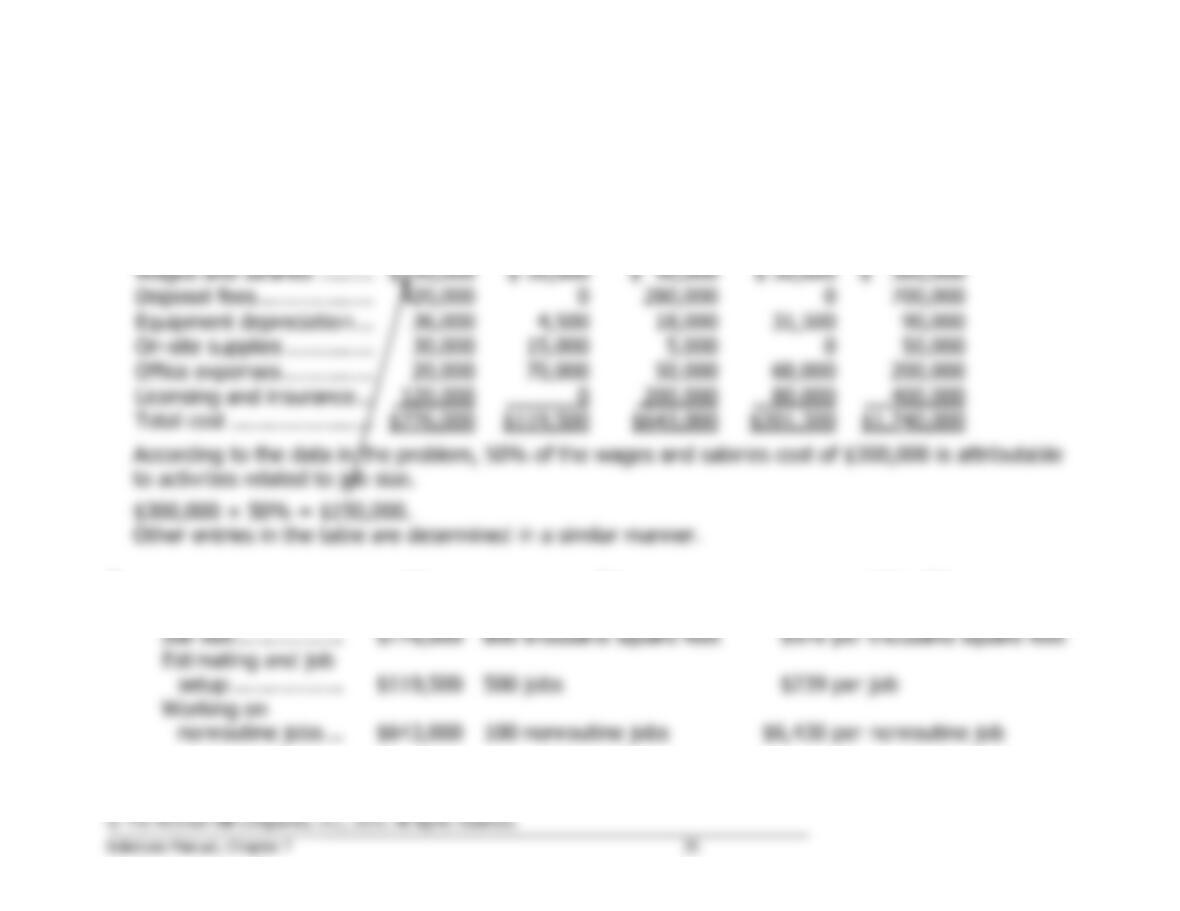

3. The costs of each of the jobs can be computed as follows using the activity rates computed above:

a.

Routine one thousand square foot job:

Job size (1 thousand square feet @ $970 per thousand square feet) ….

$ 970.00

Estimating and job setup (1 job @ $239 per job) …………………………..

239.00

Nonroutine job (not applicable) ………………………………………………….

0

Total cost of the job ………………………………………………………………..

$1,209.00

Cost per thousand square feet ($1,209 ÷ 1 thousand square feet) …….

$1,209.00

b.

Routine two thousand square foot job:

Job size (2 thousand square feet @ $970 per thousand square feet) ….

$1,940.00

Estimating and job setup (1 job @ $239 per job) …………………………..

239.00

Nonroutine job (not applicable) ………………………………………………….

0

Total cost of the job ………………………………………………………………..

$2,179.00

Cost per thousand square feet ($2,179 ÷ 2 thousand square feet) …….

$1,089.50

c.

Nonroutine two thousand square foot job:

Job size (2 thousand square feet @ $970 per thousand square feet) ….

$1,940.00

Estimating and job setup (1 job @ $239 per job) …………………………..

239.00

Nonroutine job ……………………………………………………………………….

6,430.00

Total cost of the job ………………………………………………………………..

$8,609.00

Cost per thousand square feet ($8,609 ÷ 2 thousand square feet) …….

$4,304.50

Problem 7-19 (20 minutes)

1. The cost of serving the local commercial market according to the ABC model can be determined as

follows:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Animation concept ……..

$6,040

per proposal

25

proposals

$151,000

Animation production ….

$7,725

per minute of animation

5

minutes

38,625

Contract administration .

$6,800

per contract

10

contracts

68,000

$257,625

2. The margin earned serving the local commercial market is negative, as shown below:

Profitability Analysis

Sales ……………………………………………

$180,000

Costs:

Animation concept …………………………

$151,000

Animation production ……………………..

38,625

Contract administration …………………..

68,000

257,625

Margin ………………………………………….

$(77,625)

3. It appears that the local commercial market is losing money and the company would be better off

dropping this market segment. However, as discussed in the previous problem, not all of the costs

Problem 7-20 (continued)

2. The activity rates are computed as follows:

Activity Cost Pool

(a)

Total Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Cleaning carpets…

$161,000

20,000

hundred

square feet

$8.05

per hundred

square feet

Travel to jobs …….

$78,000

60,000

miles

$1.30

per mile

Job support ……….

$59,000

2,000

jobs

$29.50

per job

3. The cost for the Flying N Ranch job is computed as follows:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Cleaning carpets …

$8.05

per hundred

square feet

5

hundred

square feet

$ 40.25

Travel to jobs …….

$1.30

per mile

75

miles

97.50

Job support ……….

$29.50

per job

1

job

29.50

Total ………………..

$167.25

4. The margin earned on the job can be easily computed by using the

costs calculated in part (3) above.

Sales ……………………

$140.00

Costs:

Cleaning carpets …..

$40.25

Travel to jobs ………

97.50

Job support …………

29.50

167.25

Margin ………………….

$(27.25)