Archives

Chapter 1 Instructors Manual The Finance Function Accounting Information

information LO2— Compare and contrast managerial accounting with financial accounting and distinguish between the information needs of external and internal users LO3— Recognize the role of relevant factors in decision making LO4— Understand sources of ethical issues in business and […]

Chapter 1 Regardless Fault Henry Powell Inc Should Immediately

or ten years have resulted in the automation of traditional accounting functions involving data collection, data entry, and data reporting and a corresponding shifting of those functions from managerial accountants to clerical staff. Consequently, many managerial accountants now focus on […]

Chapter 1 Introduction to Managerial Accounting Multiple Choice

Chapter 1 Introduction to Managerial Accounting Multiple Choice 1. (LO 1—Users of accounting information) Answer: D 2. (LO 1—Knowledge management) Answer: C 3. (LO 2—Users of accounting information) Answer: A 4. (LO 2—Managerial vs. financial accounting) Answer: B 5. (LO […]

Chapter 10 Answer Direct Material Variable overhead efficiency variance

Chapter 10 Variance Analysis—A Tool for Cost Control and Performance Evaluation Multiple Choice 1. (LO 1—Standard cost) Answer: B 2. (LO 2—Flexible versus static budgets) Answer: C 3. (LO 2—Flexible budget: calculation of net income) Answer: D Flexible budget Actual […]

Chapter 10 Ideal standards assume that every area of the production

A static budget is prepared for only one level of activity. The flexible budget is adjusted for changes in the level of output or activity. various levels of activity and make an evaluation or comparison of actual results to planned […]

Chapter 10 Selling And Administrative Expense Variance The Selling

• The flexible budget variance is the difference between the flexible budget operating income and the actual operating income. • Sales price variances result from changing sales prices that are different from those that were planned. • Purchasing managers are […]

Chapter 11 Investment Centers Are Typically Major Divisions Branch

• Businesses are often broken into cost, revenue, and profit centers as a means to evaluate managers’ performance levels. • Evaluating investment centers requires focusing on the level of investment required for generating a segment’s profit. • Evaluating the performance […]

Chapter 11 There Strong Basis For The Perception That

control. The impact on decision making is to tie results of operations to the manager who has control and responsibility over a particular area. It also limits managers to making decisions within their area of responsibility. capital. Investment center managers […]

Chapter 11 Decentralization, Performance Evaluation, and the Balanced Scorecard

Chapter 11 Decentralization, Performance Evaluation, and the Balanced Scorecard Multiple Choice 1. (LO 1—Centralized organizations) Answer: A 2. (LO 1—Drawbacks of decentralized organizations) Answer: A 3. (LO 2—Responsibility accounting) Answer: C 4. (LO 3—Revenue center) Answer: D 5. (LO 3—Types […]

Chapter 12 Current Ratio Current Assets Current Liabilities Current

Chapter 12 Financial Statement Analysis Multiple Choice 1. (LO 1—Financial statement analysis) Answer: A 2. (LO 1—Limitations of financial statement analysis) Answer: B 3. (LO 2—Horizontal analysis) Answer: A 4. (LO 2—Trend analysis) Answer: C 5. (LO 3—Vertical analysis: Calculation […]

Chapter 12 Quick Ratio Quick Assets Current Liabilities Quick

• Rather than focus on a single ratio, decision makers need to evaluate a company by comparing ratios to those of previous years, budgeted amounts, and industry standards. • Vertical analysis uses common-size financial statements to remove size as a […]

Chapter 12 Ratio analysis by itself does not indicate the various

statements. Inventory methods such as LIFO or FIFO are an example of this. If a company has changed accounting methods, period-to-period comparisons may be difficult. In addition, comparing companies of different size and complexity as well as companies in different […]

Chapter 13 An understanding of the effects of different types

organization, the statement of cash flows and the related cash budget (Chapter 9) are useful tools for managerial decision making. 13 – 1 CHAPTER THIRTEEN The Statement of Cash Flows This chapter presents an in-depth discussion of the preparation and […]

Chapter 13 The purpose of the statement of cash flows

Chapter 13 The Statement of Cash Flows Multiple Choice 1. (LO 1—The purpose of the statement of cash flows) Answer: B 2. (LO 1—The purpose of the statement of cash flows) Answer: B 3. (LO 1—Cash flows from financing activities) […]

Chapter 13 It is combined with the cash account on the statement

time whereas the income statement reports revenues earned and expenses incurred for a period of time. While cash flows are often associated with some of the revenues and expenses shown on the income statement, some may not involve a cash […]

Chapter 2 Environment Answer With WIP Finished Goods

MC2–1 Chapter 2 Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows Multiple Choice 1. (LO 1—Characteristics of traditional manufacturing environment) 2. (LO 1—Characteristics of traditional manufacturing environment) Answer: A 3. (LO 2—JIT environment) Answer: C 4. (LO 2—Lean manufacturing) […]

Chapter 2 Processes Cost Terminology And Cost Flows Lo4cost

and products are pulled through the manufacturing process. In contrast, traditional systems are called push systems because raw materials, work in process and finished goods are pushed through the manufacturing process regardless of whether a customer has been identified for […]

Chapter 2 Provide Many Benefits Including Improved Production

LO2— Identify the key characteristics and benefits of lean production and JIT manufacturing LO3— Distinguish manufacturing costs from nonmanufacturing costs and classify manufacturing costs as direct materials, direct labor, or overhead LO4— Diagram the flow of costs in manufacturing, merchandising, […]

Chapter 3 Regression Analysis Least Squares Regression Analysis Used

LO3— Illustrate the impact of income taxes on costs and decision making LO4— Identify the difference between variable costing and absorption costing LO5—Identify the impact on the income statement of variable costing and absorption costing 3 – 1 CHAPTER THREE […]

Chapter 3 Since the numbers of units produced and sold are equal

MC3–1 Chapter 3 Cost Behavior Multiple Choice 1. (LO 1—Fixed cost behavior) Answer: A 2. (LO 1—Variable cost behavior) 3. (LO1—Variable cost behavior) Answer: B The cost is a variable cost. It varies in direct proportion to the volume and […]

Chapter 3 while relevant costs are avoidable or can be eliminated

cost, the dependent variable in regression analysis is the total cost (represented by y in the equation y = a + bx. The independent variable is the activity level or production level (represented by x in the equation y = […]

Chapter 4 The Allocation Costs From Service Dept Based

company, whereas process costing is a system that accumulates costs for each process and then assigns those costs equally to each unit produced. Job order costing may be used by custom home contractors, custom furniture manufacturers, attorneys, and architects. Process […]

Chapter 4 The total equivalent units completed during the year

MC4–1 Chapter 4 Job Costing, Process Costing, and Operations Costing Multiple Choice 1. (LO 1—Job costing) 2. (LO 2—Job costing) Answer: B 3. (LO 2—Normal spoilage) Answer: A 4. (LO 2—Overtime premiums) Answer: C 5. (LO 3—Manufacturing overhead and cost […]

Chapter 4 With More Than One Type Product Allocate

• Overhead cannot be directly tracked to products and services but must instead be allocated using cost drivers. • Understanding what causes overhead costs to be incurred (what drives them) is the key to allocating overhead. • In order to […]

Chapter 5 Although there are common activities that drive overhead

• Although there are common activities that drive overhead cost, every company should evaluate its activities carefully. • Volume-based costing systems often result in overcosting high-volume products and undercosting low-volume products. This cross subsidy is eliminated by the use of […]

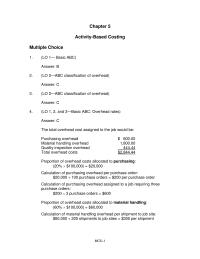

Chapter 5 Proportion of overhead costs allocated to purchasing:

MC5–1 Chapter 5 Activity-Based Costing Multiple Choice 1. (LO 1— Basic ABC) 2. (LO 2—ABC classification of overhead) Answer: C 3. (LO 2—ABC classification of overhead) Answer: C 4. (LO 1, 2, and 3—Basic ABC: Overhead rates) Answer: C The […]

Chapter 5 The first stage of cost allocation is the identification

rather than the volume or number of units produced. The activities are procedures or processes that cause work to be accomplished. Activities consume resources and products require activities to be performed. overhead costs to each activity. In many cases, this […]

Chapter 6 A thorough understanding of fixed and variable

analysis provides marketing and operations managers with useful information concerning sales that is necessary in order to break even or to earn a target profit. It illustrates how profit is affected when the costs, volume, or prices of products or […]

Chapter 6 Contribution margin will not change because a change

selling costs per unit. One might also consider contribution margin to be total sales minus total variable costs. Contribution margin (ratio) can also be expressed as a percentage of the sales price. Assuming no change in fixed costs, a decrease […]

Chapter 6 If sales increase by 20 percent, income will increase

MC6–1 Chapter 6 Cost-Volume-Profit Analysis Multiple Choice 1. (LO 1—Cost behavior) 2. (LO 1—Cost behavior and contribution margin) Answer: D 3. (LO 1—Format of contribution margin statement) Answer: B 4. (LO 1—Contribution margin and net income) Answer: D 5. (LO […]

Chapter 7 Given The Limited Resource Stuffing Hours Soft

include the variable costs (direct material, direct labor, variable overhead and perhaps variable selling and administrative costs) of producing the special order. There are not likely to be any opportunity costs. source, the variable costs of making the product that […]

Chapter 7 Product Planning Decisions The Decision Outsource

• A product should continue to be made internally if the avoidable costs are less than the additional costs that will be incurred by buying or outsourcing. • A product should be dropped when the fixed costs that are avoided […]

Chapter 7 The relevant costs of selling hotdogs include

MC7–1 Chapter 7 Relevant Costs and Product Planning Decisions Multiple Choice 1. (LO 1—Special order) Answer: B The relevant costs of selling hotdogs include only $1.00 of variable costs. 2. (LO 1—Special order: Quantitative and qualitative factors) Answer: D 3. […]

Chapter 8 Investment is less than the discount rate used in the NPV

Chapter 8 Long-Term (Capital Investment) Decisions Multiple Choice 1. (LO 1—NPV) Answer: C If the van costs $51,200, the net present value (NPV) of the project will be zero and the investment will provide a return of exactly 20 percent. […]

Chapter 8 Long-term decisions require a consideration of

• The internal rate of return (IRR) is the actual yield, or return, earned by an investment. • The time value of money is considered in capital investment decisions by using one of two techniques: the net present value (NPV) […]

Chapter 8 When projects are of the same magnitude

If the NPV is negative, the actual rate of return (IRR) is less than the discount rate used in the analysis. by dividing the present value of the cash inflows by the initial investment. An index of 1.0 or greater […]

Chapter 9 Desired ending inventory Total budgeted production needs

Chapter 9 The Use of Budgets in Planning and Decision Making Multiple Choice 1. (LO 1—Budgets) Answer: A 2. (LO 1—Advantages of budgeting) Answer: C 3. (LO 2—Sales budget) Answer: C 4. (LO 3—Production budget) Answer: C Projected sales (hats) […]

Chapter 9 The impact of product changes or changes in the mix

sources (gifts, parents, student loans, scholarships, interest and dividends, etc.). Cash outflows might be broken down into categories for school related expenses (tuition, fees, books), living expenses (rent or house payment, utilities, food, car payments, gasoline, clothes, etc.) and finally, […]

Chapter 9 The Usual Starting Point Sales Forecasting Last

• The sales forecast (budget) is the starting point in the production budget. • Preparing budgets for material purchases direct labor, overhead, and selling and administrative expenses is critical because these budgets often require companies to commit to expenditures months […]

Management Chapter 1 Which of the following is true regarding managerial

Chapter 1—Introduction to Managerial Accounting MULTIPLE CHOICE 1. The main focus of managerial accounting is: a. decision making. b. the preparation of financial statements. c. the preparation of budgets. d. documenting cash flows. ANS: A PTS: 1 DIF: Easy OBJ: […]

Management Chapter 10 Employees Took Shorter Amount Time Produce The

Chapter 10—Variance Analysis—A Tool for Cost Control and Performance Evaluation MULTIPLE CHOICE 1. A budget for a single unit of a product or service is called a: a. fixed cost. b. real cost. c. standard cost. d. full cost. ANS: […]

Management Chapter 10 Fixed overhead is applied to units produced

NARRBEGIN: Atkinson Landscaping Atkinson Landscaping Atkinson Landscaping applies variable overhead based on direct labor hours. At the beginning of the current year, Atkinson had estimated the following: Estimated variable overhead $56,000 Estimated units of production 10,000 units Standard direct labor […]

Management Chapter 11 external failure costs can never be reduced

92. Which types of quality costs are incurred in the course of inspecting, identifying, and isolating defective products and services before they reach the customer? a. Appraisal (detection) costs b. Prevention costs c. External failure costs d. Internal failure costs […]

Management Chapter 11 How does the balanced scorecard approach differ

16. What are the three types of compensation that managers typically receive? ANS: • Cash compensation • Stock-based compensation (ex. stock options) • Noncash benefits and perks (ex. company car, club memberships, etc.) PTS: 1 DIF: Easy OBJ: 11.8 NAT: […]

Management Chapter 11 Refer The Carson Inc Information Above What

Chapter 11—Decentralization, Performance Evaluation, and the Balanced Scorecard MULTIPLE CHOICE 1. A decentralized organization is one in which: a. each employee in the organization is given permission to make decisions about their company. b. only top-level management is given decision-making […]

Management Chapter 12 Which of the following is not a limitation

Chapter 12—Financial Statement Analysis MULTIPLE CHOICE 1. Which of the following statements regarding financial analysis is true? a. Financial analysis will show how a company is guaranteed to perform in the future. b. Financial analysis should not be relied upon […]

Management Chapter 12 Which ratio gives an indication of how investors

76. Refer to the Grogan Inc. information above. Grogan had an average of 5,000 shares of common stock outstanding during 2009. At the end of the year, the market price per share was $100. The company’s price earnings (P/E) ratio […]

Management Chapter 13 Cash received from the issuance of capital

Chapter 13—The Statement of Cash Flows MULTIPLE CHOICE 1. The main purpose of the statement of cash flows is: a. to provide information about revenues and expenses for a period of time. b. to provide information about assets, liabilities, and […]

Management Chapter 13 The Direct Method Reports Major Classes Gross

Clyde’s accounts payable balances are composed solely of amounts due to suppliers for purchases of inventory. What is the amount of cash payments for inventory that Clyde should report on its 2009 statement of cash flows assuming that the direct […]

Management Chapter 2 Johnson Manufacturing has the following selected

61. In a traditional manufacturing environment, as the cost of goods sold account increases, which account is most likely decreasing? a. Work-in-process inventory b. Finished goods inventory c. Raw materials inventory d. Cash ANS: B PTS: 1 DIF: Medium OBJ: […]

Management Chapter 2 Overtime Pay Factory Supervisor Insurance Factory

Chapter 2—Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows MULTIPLE CHOICE 1. Which of the following types of organizations is most likely to have a raw materials inventory account? a. A retailer b. A manufacturer c. A service provider […]

Management Chapter 3 when comparing net income using absorption

66. Under variable costing, which of the following is not considered a product cost? a. Direct materials b. Direct labor c. Fixed manufacturing overhead d. Variable manufacturing overhead ANS: C PTS: 1 DIF: Easy OBJ: 3.6 NAT: AACSB: Analytic | […]

Management Chapter 3 You are given the following cost and volume

Chapter 3—Cost Behavior MULTIPLE CHOICE 1. ____ are costs that do not change in total when production volume increases or decreases within the relevant range. a. Variable costs b. Relevant costs c. Fixed costs d. Period costs ANS: C PTS: […]

Management Chapter 4 All of the following statements about service

76. Refer to the Nunez Products Inc. information above. If Nunez uses the weighted-average method of computing equivalent units and assigning product costs, what is the cost per equivalent unit? (round to nearest penny) a. $7.43 b. $7.47 c. $7.96 […]

Management Chapter 4 Companies that produce large numbers of standardized

Chapter 4—Job Costing, Process Costing, and Operations Costing MULTIPLE CHOICE 1. The accumulating, tracking, and assigning of production costs to the goods and services produced is called a: a. pricing system. b. managerial system. c. product costing system. d. manufacturing […]

Management Chapter 5 As companies experience a shift from labor-intensive

Chapter 5—Activity-Based Costing MULTIPLE CHOICE 1. Activity-based costing is a method of cost allocation that is useful for assigning ____ costs to products or services. a. direct materials b. direct labor c. manufacturing overhead d. direct materials and direct labor […]

Management Chapter 5 Cross Subsidies Will Result Less Accurate Product

53. Jones Construction currently uses traditional costing where overhead is applied based on direct labor hours. Using traditional costing, the applied overhead rate is $20 per direct labor hour. They are considering a switch to activity-based costing (ABC). The company […]

Management Chapter 6 Harrison Manufacturing has the following product

Managerial ACCT Test Bank Chapter 6 19 79. Harrison Manufacturing has the following product information available: Sales price $50 per unit Variable costs $26 per unit Fixed costs $87,600 If Harrison is in the 35% tax bracket, how many units […]

Management Chapter 6 What Will The Anticipated Effect Net income a Net

Chapter 6—Cost-Volume-Profit Analysis MULTIPLE CHOICE 1. The traditional income statement focuses on: a. cost function b. cost behavior c. contribution margin. d. variable costing. ANS: A PTS: 1 DIF: Easy OBJ: 6.1 NAT: AACSB: Analytic | IMA: Decision Analysis 2. […]

Management Chapter 7 A local vendor at the county fair sells

Chapter 7—Relevant Costs and Product Planning Decisions MULTIPLE CHOICE 1. Which of the following statements is true regarding special order decisions? a. Special order decisions are long-run decisions. b. Whether or not the company has excess capacity is seldom a […]

Management Chapter 7 What factors does a company consider when

Managerial ACCT Test Bank Chapter 7 15 NARRBEGIN: Wright Manufacturing Wright Manufacturing Wright Manufacturing makes picnic tables in three sizes: small, medium, and large. The picnic tables can be sold with or without a finishing stain. The following information is […]

Management Chapter 8 A local day spa is considering investing

60. Siddon Inc. is considering investing in equipment that costs $20,000. The equipment would be depreciated using the straight-line method with no half-year convention over five years and have no salvage value. If the company has a 40 percent income […]

Management Chapter 8 NPV calculations generally require which of the

Chapter 8—Long-Term (Capital Investment) Decisions MULTIPLE CHOICE 1. The time value of money concept focuses on: a. revenues. b. expenses. c. cash flows. d. net income. ANS: C PTS: 1 DIF: Easy OBJ: 8.1 NAT: AACSB: Analytic | IMA: Investment […]

Management Chapter 9 Pellini Products Inc. is a manufacturer of

What is the cash balance at the end of June expected to be? a. $15,000 b. $12,000 c. $26,000 d. $29,000 ANS: A PTS: 1 DIF: Hard OBJ: 9.5 NAT: AACSB: Analytic | IMA: Budget Preparation 71. Which of the […]

Management Chapter 9 The comparison of actual outcomes with desired

Chapter 9—The Use of Budgets in Planning and Decision Making MULTIPLE CHOICE 1. Budgets are: a. future oriented b. for managers only c. required by GAAP d. typically not used by small business ANS: A PTS: 1 DIF: Easy OBJ: […]