Archives: Solution Manual

978-1260153590 Chapter 6 Solutions Manual Part 7

52. Monthly rate = .08/12 = .00667; semiannual rate = (1.00667)6 – 1 = 4.067% Enter 10 4.067% $5,900 N I/Y PV PMT FV Solve for $47,694.45 53. a. Enter 5 6.8% $13,500 N I/Y PV PMT FV Solve for […]

978-1260153590 Chapter 6 Solutions Manual Part 6

19. NOM EFF C/Y Solve for 1,660.53% 20. Enter 60 5.2%/12 $84,500 N I/Y PV PMT FV Solve for $1,602.37 Enter 5.2% 12 NOM EFF C/Y Solve for 5.33% 21. Enter 1.3% $18,000 $450 N I/Y PV PMT FV Solve […]

978-1260153590 Chapter 6 Solutions Manual Part 5

74. The cash flows in this problem occur every two years, so we need to find the effective two-year rate. One way to find the effective two-year rate is to use an equation similar to the EAR, except use the […]

978-1260153590 Chapter 6 Solutions Manual Part 4

61. The time line is: –24 –23 … –12 –11 … 0 1 …60 0 Here we have cash flows that would have occurred in the past and cash flows that will occur in the future. We need to bring […]

978-1260153590 Chapter 6 Solutions Manual Part 3

43. The time line is: 0 1 2 3 4 0 0 0 We are given the total PV of all four cash flows. If we find the PV of the three cash flows we know, and subtract them from […]

978-1260153590 Chapter 6 Solutions Manual Part 2

22. The time line is: 0 1 –$3 $4 Here we are trying to find the interest rate when we know the PV and FV. Using the FV equation: FV = PV(1 + r) The interest rate is 33.33% per […]

978-1260153590 Chapter 6 Solutions Manual Part 1

CHAPTER 6 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and the 4. It’s deceptive, but very common. […]

978-1260153590 Chapter 6 Case Solutions

CHAPTER 6 THE MBA DECISION 1. Age is obviously an important factor. The younger an individual is, the more time there is for the 2. Perhaps the most important nonquantifiable factors would be whether or not he is married and […]

978-1260153590 Chapter 5 Solutions Manual Part 2

20. The time line is: 0 2 ? – $10,00 0 $60,000 To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. […]

978-1260153590 Chapter 5 Solutions Manual Part 1

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 2. Compounding refers to the growth of a dollar amount through time via reinvestment of interest earned. It is also the process […]

978-1260153590 Chapter 4 Solutions Manual Part 3

27. The pro forma income statements for all three growth rates will be: Pro Forma Income Statement 15 % Sales Growth 20% Sales Growth 25% Sales Growth Sales $1,127,874 $1,176,912 $1,225,950 Costs 911,904 951,552 991,200 We will calculate the EFN […]

978-1260153590 Chapter 4 Solutions Manual Part 2

19. We are given the profit margin. Remember that: ROA = PM(TAT) We can calculate the ROA from the internal growth rate formula, and then use the ROA in this equation to find the total asset turnover. The retention ratio […]

978-1260153590 Chapter 4 Solutions Manual Part 1

CHAPTER 4 LONG-TERM FINANCIAL PLANNING AND GROWTH Answers to Concepts Review and Critical Thinking Questions 1. The reason is that, ultimately, sales are the driving force behind a business. A firm’s assets, 2. Two assumptions of the sustainable growth formula […]

978-1260153590 Chapter 4 Case Solutions

CHAPTER 4 PLANNING FOR GROWTH AT S&S AIR 1. To calculate the internal growth rate, we first need to find the ROA and the retention ratio, so: ROA = NI/TA b = Addition to RE/NI b = $1,612,789/$2,317,789 b = […]

978-1260153590 Chapter 3 Solutions Manual Part 2

20. The solution to this problem requires a number of steps. First, remember that Current assets + Net Current ratio = Current assets/Current liabilities Current assets = Current ratio(Current liabilities) Current assets = 1.30($955) Current assets = $1,241.50 To find […]

978-1260153590 Chapter 3 Solutions Manual Part 1

CHAPTER 3 WORKING WITH FINANCIAL STATEMENTS Answers to Concepts Review and Critical Thinking Questions 1. a. If inventory is purchased with cash, then there is no change in the current ratio. If inventory is purchased on credit, then there is […]

978-1260153590 Chapter 3 Case Solutions

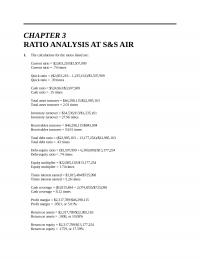

CHAPTER 3 RATIO ANALYSIS AT S&S AIR 1. The calculations for the ratios listed are: Current ratio = $2,603,218/$3,507,909 Current ratio = .74 times Quick ratio = ($2,603,218 – 1,235,161)/$3,507,909 Quick ratio = .39 times Cash ratio = $524,963/$3,507,909 Cash […]

978-1260153590 Chapter 27 Solutions Manual

CHAPTER 27 LEASING Answers to Concepts Review and Critical Thinking Questions 1. Some key differences are: (a) Lease payments are fully tax-deductible, but only the interest portion 2. The less profitable corporation because leasing provides, among other things, a mechanism […]

978-1260153590 Chapter 27 Case Solutions

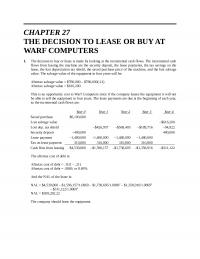

CHAPTER 27 THE DECISION TO LEASE OR BUY AT WARF COMPUTERS 1. The decision to buy or lease is made by looking at the incremental cash flows. The incremental cash This is an opportunity cost to Warf Computers since if […]

978-1260153590 Chapter 26 Solutions Manual

CHAPTER 26 MERGERS AND ACQUISITIONS Answers to Concepts Review and Critical Thinking Questions 1. Since both companies are in the liquor industry, this is a horizontal acquisition. A major factor that may have led Beam to be relatively more attractive […]

978-1260153590 Chapter 26 Case Solutions

CHAPTER 26 THE BIRDIE GOLF-HYBRID GOLF MERGER 1. As with any other merger analysis, we need to examine the present value of the incremental cash flows. The cash flow today from the acquisition is the acquisition costs plus the dividends […]

978-1260153590 Chapter 25 Solutions Manual Part 2

20. a. Using the Black-Scholes model to value the equity, we get: d2 = .6810 – (.41 √ 5 ) = –.2357 N(d1) = .7521 N(d2) = .4068 Putting these values into Black-Scholes: Equity = C = $15,900,000(.7521) – […]

978-1260153590 Chapter 25 Solutions Manual Part 1

CHAPTER 25 OPTION VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Increasing the time to expiration increases the value of an option. The reason is that the option gives 3. Interest rate increases are good for calls and […]

978-1260153590 Chapter 25 Case Solutions

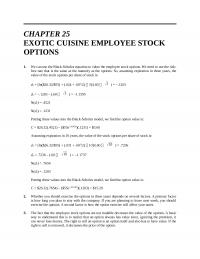

CHAPTER 25 EXOTIC CUISINE EMPLOYEE STOCK OPTIONS 1. We can use the Black-Scholes equation to value the employee stock options. We need to use the risk- d1 = [ln($26.32/$55) + (.024 + .602/2) 3]/(.60 √ 3 ) = […]

978-1260153590 Chapter 24 Solutions Manual Part 2

15. a. If the project is a success, the present value of the future cash flows will be: From the previous question, if the quantity sold is 3,900, we would abandon the project, and the cash flow would be $1,200,000. […]

978-1260153590 Chapter 24 Solutions Manual Part 1

CHAPTER 24 OPTIONS AND CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put […]

978-1260153590 Chapter 24 Case Solutions

CHAPTER 24 S&S AIR’S CONVERTIBLE BOND 1. We can use the PE ratio to calculate the current stock price. Doing so, we get: PE = Price/EPS This means the conversion premium of the bond is: Conversion premium = ($25 – […]

978-1260153590 Chapter 23 Solutions Manual

CHAPTER 23 ENTERPRISE RISK MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. Since the firm is selling futures, it wants to be able to deliver the lumber; therefore, it is a supplier. 2. Buying call options gives the […]

978-1260153590 Chapter 23 Case Solutions

CHAPTER 23 CHATMAN MORTGAGE, INC. 1. Mike’s mortgage payments form a 25-year annuity with monthly payments, discounted at the long- 2. The most significant risk that she faces is interest rate risk. If the current market rate of interest rises […]

978-1260153590 Chapter 22 Solutions Manual

CHAPTER 22 BEHAVIORAL FINANCE: IMPLICATIONS FOR FINANCIAL MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. The least likely limit to arbitrage is firm-specific risk. For example, in the 3Com/Palm case, the 2. Overconfidence is the belief that one’s […]

978-1260153590 Chapter 22 Case Solutions

CHAPTER 22 YOUR 401(k) ACCOUNT AT S&S AIR 1. Before the fact, you would expect that mutual fund’s managers would be able to outperform the market. This is due, in part, to the Darwinian nature of the business. Good performing […]

978-1260153590 Chapter 21 Solutions Manual

CHAPTER 21 INTERNATIONAL CORPORATE FINANCE Answers to Concepts Review and Critical Thinking Questions 1. a. The dollar is selling at a premium because it is more expensive in the forward market than in b. The franc is expected to depreciate […]

978-1260153590 Chapter 21 Case Solutions

CHAPTER 21 S&S AIR GOES INTERNATIONAL At the current exchange rate of $1.37/€, the EBT in euros will be converted to dollars in the amount of: Dollar EBT = €5,415,000($1.09/€) Dollar EBT = $5,902,350 S&S Air has production costs equal […]

978-1260153590 Chapter 20 Solutions Manual Part 2

16. If the cost of subscribing to the credit agency is less than the savings from collection of the bad debts, the company should subscribe. The cost of the subscription is: Cost of the subscription = $1,000 + $8.95(125) Cost […]

978-1260153590 Chapter 20 Solutions Manual Part 1

CHAPTER 20 CREDIT AND INVENTORY MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. a. A sight draft is a commercial draft that is payable immediately. 3. Credit costs: cost of debt, probability of default, and the cash discount […]

978-1260153590 Chapter 20 Case Solutions

CHAPTER 20 CREDIT POLICY AT HOWLETT INDUSTRIES To decide on the optimal credit policy, we need to calculate the NPV of each policy. We will begin with the calculation of the NPV of the current policy. Current Policy First, we […]

978-1260153590 Chapter 2 Solutions Manual

CHAPTER 2 FINANCIAL STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. Liquidity measures how quickly and easily an asset can be converted to cash without significant loss in value. It’s desirable for firms to […]

978-1260153590 Chapter 2 Case Solutions

CHAPTER 2 CASH FLOWS AND FINANCIAL STATEMENTS AT SUNSET BOARDS Below are the financial statements that you are asked to prepare. 1. The income statement for each year will look like this: Income Statement 2017 2018 Sales $501,441 $611,224 Cost […]

978-1260153590 Chapter 19 Solutions Manual

CHAPTER 19 CASH AND LIQUIDITY MANAGEMENT Answers to Concepts Review and Critical Thinking Questions 1. Yes. Once a firm has more cash than it needs for operations and planned expenditures, the excess 2. If it has too much cash, it […]

978-1260153590 Chapter 19 Case Solutions

CHAPTER 19 CASH MANAGEMENT AT WEBB CORP. 1. The amount the company will have available is the future value of the transfers, which are an 2. The bank will accept the ACH transfers from the four different banks, so the […]

978-1260153590 Chapter 18 Solutions Manual Part 2

15. a. A 45-day collection period means sales collections each quarter are: A 36-day payables period means payables each quarter are: Payables = 3/5 current orders + 2/5 prior quarter’s orders So, the cash inflows and disbursements each quarter are: […]

978-1260153590 Chapter 18 Solutions Manual Part 1

CHAPTER 18 SHORT-TERM FINANCE AND PLANNING Answers to Concepts Review and Critical Thinking Questions 1. These are firms with relatively long inventory periods and/or relatively long receivables periods. 2. These are firms that have a relatively long time between the […]

978-1260153590 Chapter 18 Case Solutions

CHAPTER 18 PIEPKORN MANUFACTURING WORKING CAPITAL MANAGEMENT 1. The cash flow each quarter will consist of the sales collection, minus the suppliers paid, expenses, dividends, interest, and capital outlays. The individual cash flows are calculated as follows: Accounts receivable collected […]

978-1260153590 Chapter 17 Solutions Manual

CHAPTER 17 DIVIDENDS AND DIVIDEND POLICY Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. 2. A stock repurchase reduces equity while leaving debt unchanged. The […]

978-1260153590 Chapter 17 Case Solutions

CHAPTER 17 ELECTRONIC TIMING, INC. 1. The value of the company will decline by the amount of the dividend. Ignoring taxes, shareholders’ 2. The value of the company could increase or decrease. If the company is over-levered, paying off debt […]

978-1260153590 Chapter 16 Solutions Manual Part 2

11. If there are corporate taxes, the value of an unlevered firm is: VU = EBIT(1 – TC)/RU The WACC remains at 8.4 percent. Due to taxes, EBIT for an all-equity firm would have to be higher for the firm […]

978-1260153590 Chapter 16 Solutions Manual Part 1

CHAPTER 16 FINANCIAL LEVERAGE AND CAPITAL STRUCTURE POLICY Answers to Concepts Review and Critical Thinking Questions 1. Business risk is the equity risk arising from the nature of the firm’s operating activity and is directly related to the systematic risk […]

978-1260153590 Chapter 16 Case Solutions

CHAPTER 16 STEPHENSON REAL ESTATE RECAPITALIZATION 1. If Stephenson wishes to maximize the overall value of the firm, it should use debt to finance the $85 2. Since Stephenson is an all-equity firm with 8 million shares of common stock […]

978-1260153590 Chapter 15 Solutions Manual

CHAPTER 15 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company’s internally generated cash flow provides a source of equity financing. For a profitable 2. From the previous question, economies of scale are part of the […]

978-1260153590 Chapter 15 Case Solutions

CHAPTER 15 S&S AIR GOES PUBLIC 1. The main difference in the costs is the reduced possibility of underpricing in a Dutch auction. As to which is better, we don’t actually know. In theory, the Dutch auction should be better […]