CHAPTER 23

ENTERPRISE RISK MANAGEMENT

Answers to Concepts Review and Critical Thinking Questions

1. Since the firm is selling futures, it wants to be able to deliver the lumber; therefore, it is a supplier.

2. Buying call options gives the firm the right to purchase pork bellies; therefore, it must be a consumer

3. Forward contracts are usually designed by the parties involved for their specific needs and are rarely

sold in the secondary market; forwards are somewhat customized financial contracts. All gains and

losses on the forward position are settled at the maturity date. Futures contracts are standardized to

4. The firm is hurt by declining oil prices, so it should sell oil futures contracts. The firm may not be

able to create a perfect hedge because the quantity of oil it needs to hedge doesn’t match the standard

5. The firm is directly exposed to fluctuations in the price of natural gas, since it is a natural gas user. In

6. Buying the call options is a form of insurance policy for the firm. If cotton prices rise, the firm is

protected by the call, while if prices actually decline, they can just allow the call to expire worthless.

7. The put option on the bond gives the owner the right to sell the bond at the option’s strike price. If

8. The company would like to lock in the current low rates, or at least be protected from a rise in rates,

9. A swap contract is an agreement between parties to exchange assets over several time intervals in the

future. The swap contract is usually an exchange of cash flows, but not necessarily so. Since a

10. The firm will borrow at a fixed rate of interest, receive fixed-rate payments from the dealer as part of

11. Transactions exposure is the short-term exposure due to uncertain prices in the near future.

Economic exposure is the long-term exposure due to changes in overall economic conditions. There

12. The risk is that the dollar will strengthen relative to the yen, since the fixed yen payments in the

13. a. Buy oil and natural gas futures contracts, since these are probably your primary resource costs.

If it is a coal-fired plant, a cross-hedge might be implemented by selling natural gas futures,

b. Buy sugar and cocoa futures, since these are probably your primary commodity inputs.

e. Sell natural gas futures, since excess supply in the market implies low prices.

h. Buy Swiss franc futures, since the risk is that the dollar will weaken relative to the franc over

14. There are two sides to this story. As one money manager said: “There’s just no reason that these

entities should be playing with this stuff. They don’t have the capacity to evaluate these instruments.

They are totally lost.” The argument that investment banks were wrong in selling swaps to

15. Buying insurance on your house is similar to buying a put option on the house. For example, suppose

16. Even with the replacement rider, insurance is still like buying a put option. However, this is an

“always at the money” put option since the strike price is reset every time the price of the underlying

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. The initial price is $1,974 per metric ton and each contract is for 10 metric tons, so the initial

contract value is:

And the final contract value is:

So, your gain/loss on this futures position is:

2. The price quote is $17.741 per ounce and each contract is for 5,000 ounces, so the initial contract

value is:

Since this is a short position, there is a net loss of:

Since you sold five contracts, the net loss is:

At a final price of $17.64 per ounce, the value of the position is:

Since this is a short position, there is a net gain of:

Since you sold five contracts, the net gain is:

With a short position, you make a profit when the price falls and incur a loss when the price rises.

3. The price quote is 12 5/8 cents, or $.12625 per bushel and each contract is for 5,000 bushels, so the

cost per contract is:

If the price of corn at expiration is $3.74 per bushel, the call is out of the money since the strike price

If the price of corn at expiration is $4.13 per bushel, the call is in the money since the price per

And the profit is the payoff minus the initial cost of the contract, or:

4. The call options give the manager the right to purchase oil futures contracts at a futures price of $57

Oil futures price: $52 $55 $57 $59 $62

5. The price quote is 12 7/8 cents, or $.12875, per bushel and each contract is for 5,000 bushels, so the

cost per contract is:

If the price of corn at expiration is $3.61 per bushel, the put is in the money since the strike price is

greater than the spot price. The payoff on your position is the strike price minus the current price,

times the 5,000 bushels per contract, or:

And the profit is the payoff minus the initial cost of the contract, or:

If the price of corn at expiration is $3.97 per bushel, the put is out of the money since the strike price

Intermediate

6. The expected loss is the value of the asset times the probability of a loss. In this case, the expected

loss will be:

Expected loss = Asset value × Probability of loss

7. a. You’re concerned about a rise in corn prices, so you would buy May contracts. Since each

contract is for 5,000 bushels, the number of contracts you would need to buy is:

By doing so, you’re effectively locking in the settle price in May 2017 of $3.7725 per bushel of

corn, or:

b. If the price of corn at expiration is $3.69 per bushel, the value of your futures position is:

Ignoring any transaction costs, your loss on the futures position will be:

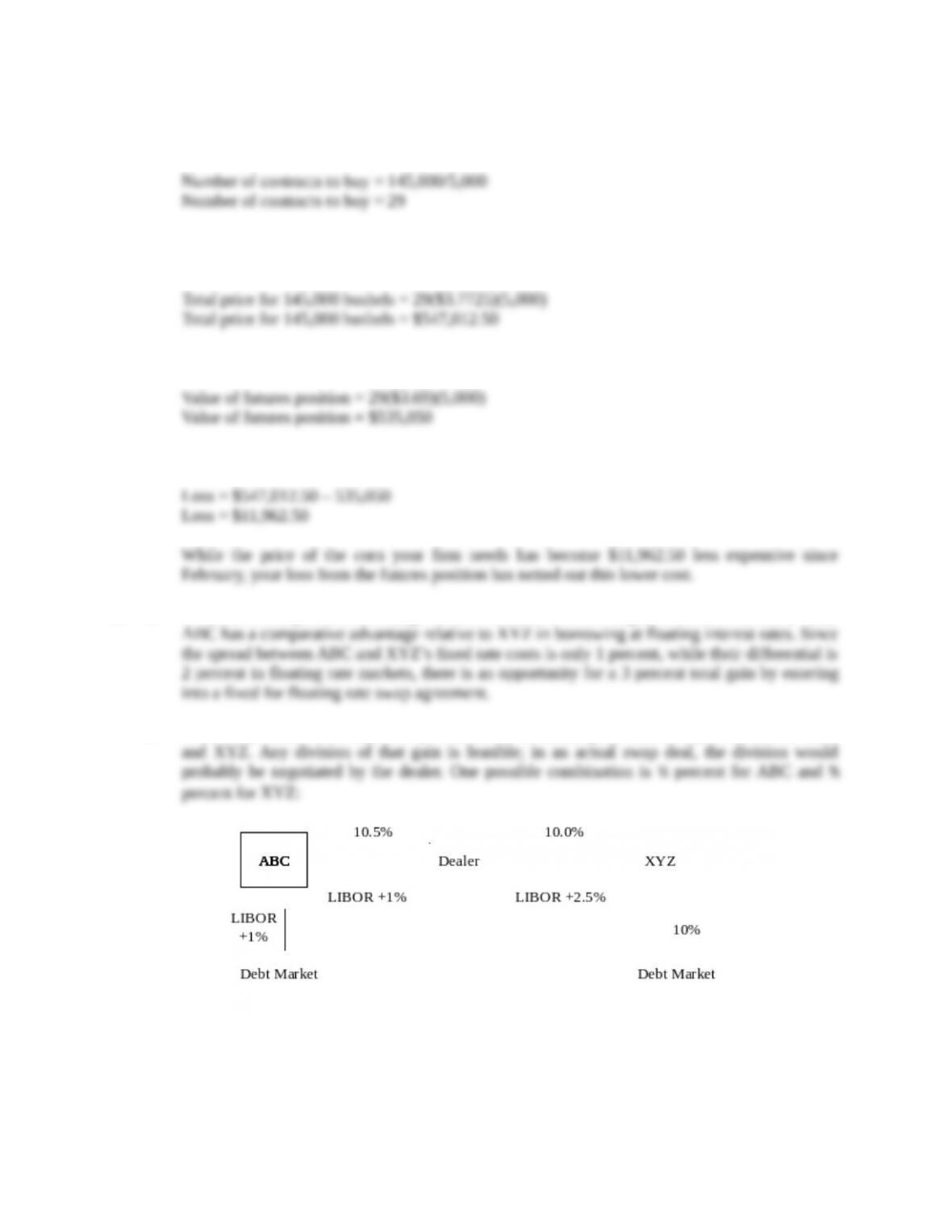

8. a. XYZ has a comparative advantage relative to ABC in borrowing at fixed interest rates, while

b. If the swap dealer must capture 2 percent of the available gain, there is 1 percent left for ABC

Challenge

9. The financial engineer can replicate the payoffs of owning a put option by selling a forward contract

and buying a call. For example, suppose the forward contract has a settle price of $50 and the

exercise price of the call is also $50. The payoffs below show that the position is the same as owning

a put with an exercise price of $50:

Price of coal futures: $40 $45 $50 $55 $60

The payoffs for the combined position are exactly the same as those of owning a put. This means

10. a. The actuarially fair insurance premium is the present value of the expected loss. So:

Insurance premium = (Asset value × Probability of loss)/(1 + R)

b. The most you would be willing to pay is the difference between the insurance premium before

the modifications and the insurance premium after the modifications. The actuarially fair

insurance premium after the modifications will be:

Insurance premium = (Asset value × Probability of loss)/(1 + R)

So, the most you would pay is: