CHAPTER 6

DISCOUNTED CASH FLOW VALUATION

Answers to Concepts Review and Critical Thinking Questions

1. The four pieces are the present value (PV), the periodic cash flow (C), the discount rate (r), and the

4. It’s deceptive, but very common. The basic concept of time value of money is that a dollar today is

5. If the total money is fixed, you want as much as possible as soon as possible. The team (or, more

8. A freshman receives a larger subsidy. The reason is that the freshman gets to use the money for much

9. The problem is that the subsidy makes it easier to repay the loan, not obtain it. However, ability to

CHAPTER 6 – 2

10. In general, viatical settlements are ethical. In the case of a viatical settlement, it is an exchange of

cash today for payment in the future, although the payment depends on the death of the seller. The

purchaser of the life insurance policy is bearing the risk that the insured individual will live longer

than expected. Although viatical settlements are ethical, they may not be the best choice for an

11. This is a trick question. The future value of a perpetuity is undefined since the payments are

12. The ethical issues surrounding payday loans are more complex than they might first appear. On the

one hand, the interest rates are astronomical, and the people paying those rates are typically among

the worst off financially to begin with. On the other hand, and unfortunately, payday lenders are

$100 might be a bargain compared to the alternatives such as having utilities disconnected or paying

PV = FV/(1 + r)t

CHAPTER 6 – 3

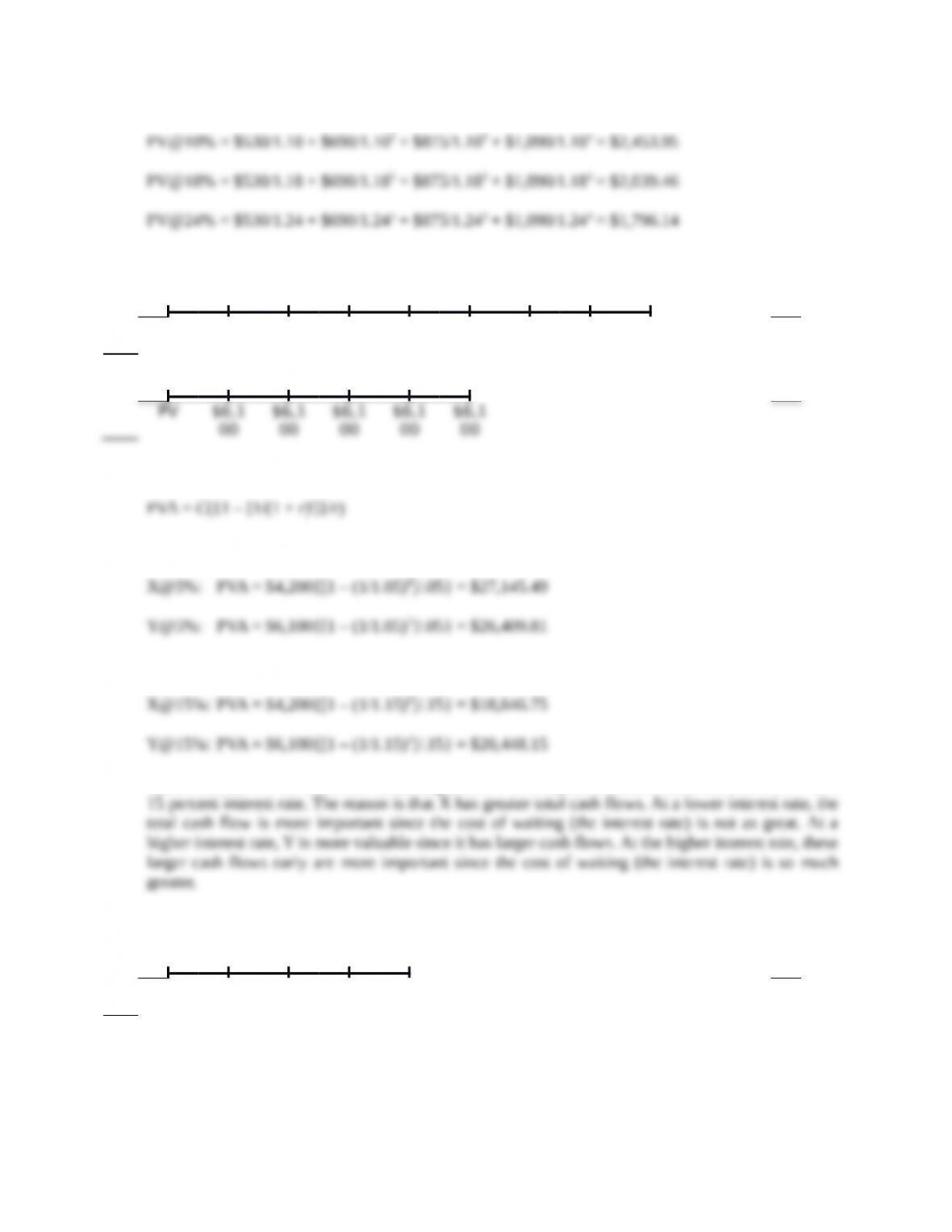

2. The time lines are:

012345678

PV $4,2

00

$4,2

00

$4,2

00

$4,2

00

$4,2

00

$4,2

00

$4,2

00

$4,2

00

012345

To find the PVA, we use the equation:

At a 5 percent interest rate:

And at a 15 percent interest rate:

Notice that the PV of Cash flow X has a greater PV at a 5 percent interest rate, but a lower PV at a

3. The time line is:

01234

$1,0

75

$1,2

10

$1,3

40

$1,4

20

To solve this problem, we must find the FV of each cash flow and add them. To find the FV of a

lump sum, we use:

FV = PV(1 + r)t

CHAPTER 6 – 4

Notice, since we are finding the value at Year 4, the cash flow at Year 4 is added to the FV of the

other cash flows. In other words, we do not need to compound this cash flow.

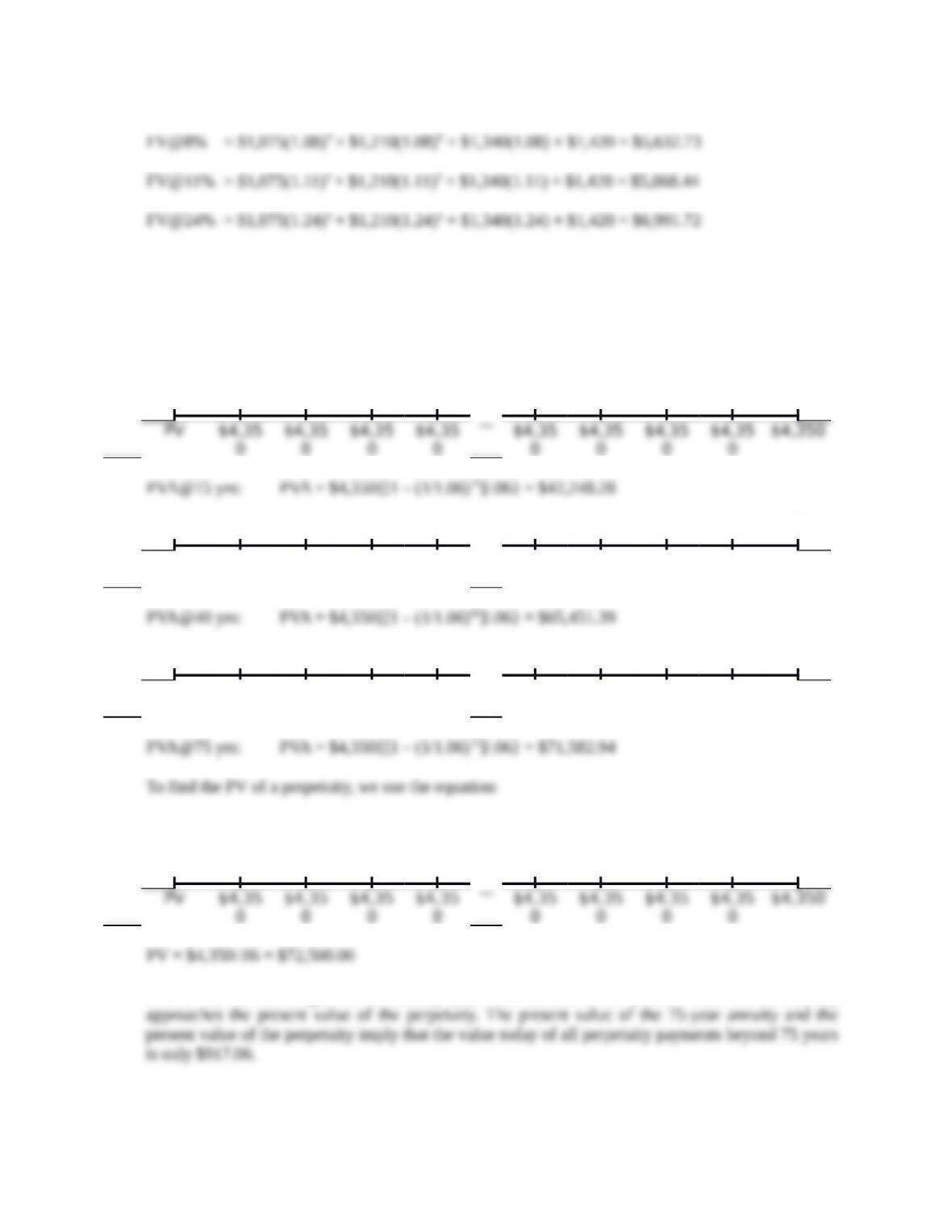

4. To find the PVA, we use the equation:

PVA = C({1 – [1/(1 + r) t]}/r)

0 1

…

15

0

0

0

0

0

0

0

0

0 1

…

40

PV $4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,350

0 1

…

75

PV $4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,35

0

$4,350

PV = C/r

0 1

…

∞

Notice that as the length of the annuity payments increases, the present value of the annuity

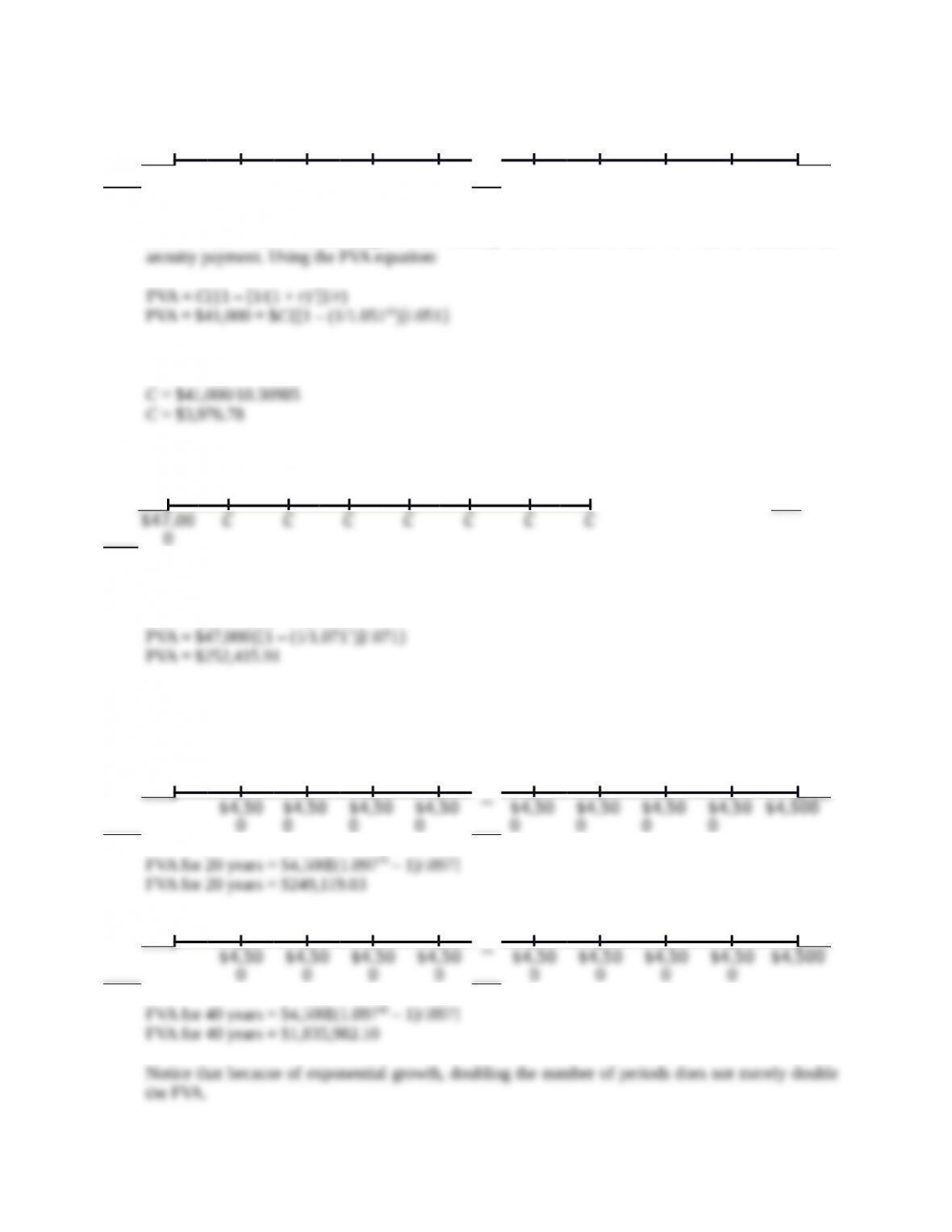

5. The time line is:

CHAPTER 6 – 5

0 1

…

15

$41,000 C C C C C C C C C

Here we have the PVA, the length of the annuity, and the interest rate. We want to calculate the

We can now solve this equation for the annuity payment. Doing so, we get:

6. The time line is:

01234567

0

To find the PVA, we use the equation:

PVA = C({1 – [1/(1 + r) t]}/r)

7. Here we need to find the FVA. The equation to find the FVA is:

FVA = C{[(1 + r)t – 1]/r}

0 1

…

20

0 1

…

40

CHAPTER 6 – 6

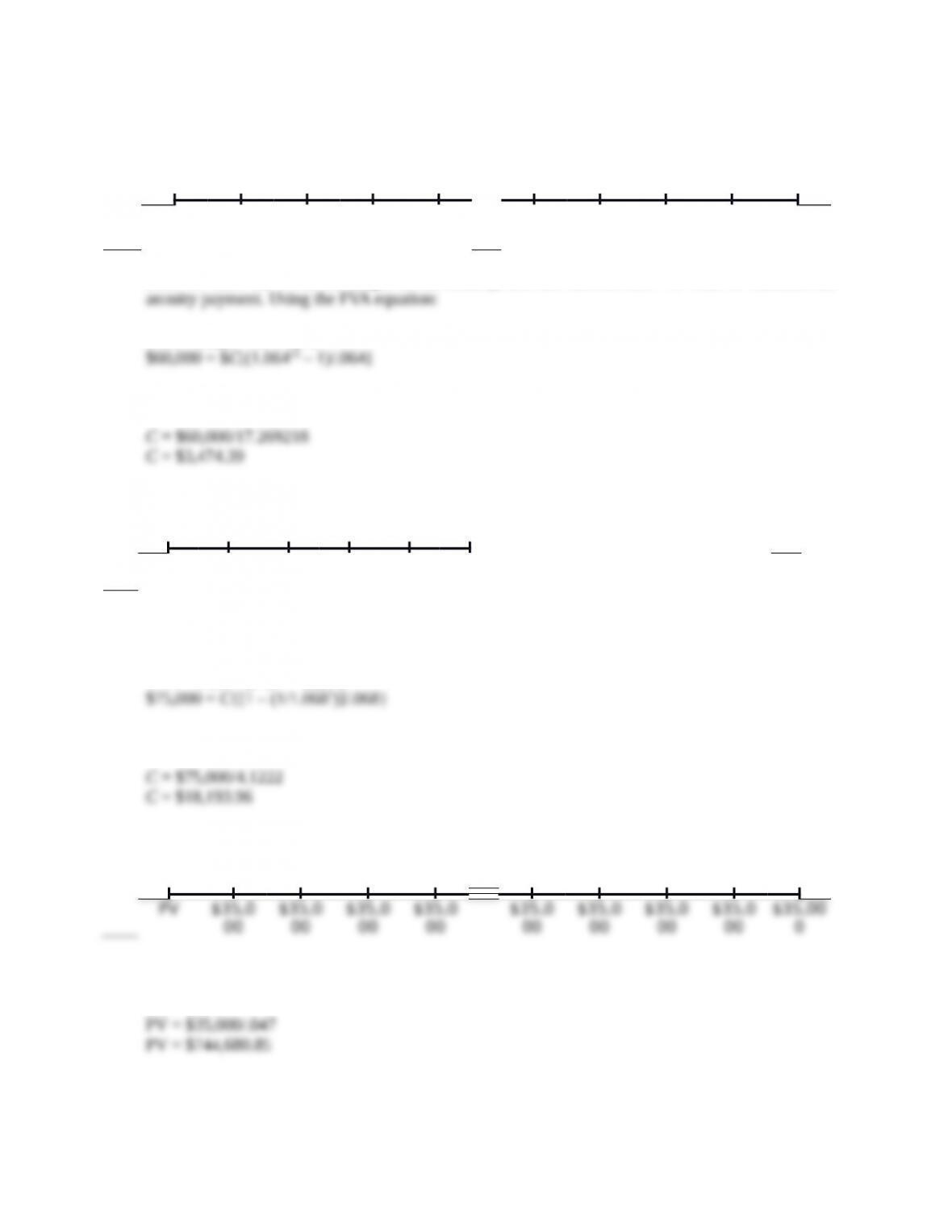

8. The time line is:

0 1

…

12

$60,000

C C C C C C C C C

Here we have the FVA, the length of the annuity, and the interest rate. We want to calculate the

FVA = C{[(1 + r)t – 1]/r}

We can now solve this equation for the annuity payment. Doing so, we get:

9. The time line is:

012345

$75,00

0

CCCCC

Here we have the PVA, the length of the annuity, and the interest rate. We want to calculate the

annuity payment. Using the PVA equation:

PVA = C({1 – [1/(1 + r)t]}/r)

We can now solve this equation for the annuity payment. Doing so, we get:

10. The time line is:

0 1 …∞

This cash flow is a perpetuity. To find the PV of a perpetuity, we use the equation:

PV = C/r

11. The time line is:

CHAPTER 6 – 7

0 1 …∞

0

Here we need to find the interest rate that equates the perpetuity cash flows with the PV of the cash

flows. Using the PV of a perpetuity equation:

PV = C/r

CHAPTER 6 – 8

We can now solve for the interest rate as follows:

12. For discrete compounding, to find the EAR, we use the equation:

EAR = [1 + (APR/m)]m – 1

To find the EAR with continuous compounding, we use the equation:

EAR = eq – 1

13. Here we are given the EAR and need to find the APR. Using the equation for discrete compounding:

We can now solve for the APR. Doing so, we get:

APR = m[(1 + EAR)1/m – 1]

Solving the continuous compounding EAR equation:

EAR = eq – 1

We get:

14. For discrete compounding, to find the EAR, we use the equation:

CHAPTER 6 – 9

Notice that the higher APR does not necessarily result in the higher EAR. The number of

compounding periods within a year will also affect the EAR.

15. The reported rate is the APR, so we need to convert the EAR to an APR as follows:

EAR = [1 + (APR/m)]m – 1

16. The time line is:

0 1

…

34

$3,100 FV

It is important to note that compounding occurs semiannually. To account for this, we will divide the

interest rate by two (the number of compounding periods in a year), and multiply the number of

periods by two. Doing so, we get:

17. For this problem, we need to find the FV of a lump sum using the equation:

FV = PV(1 + r)t

0 1

…

5(365)

$6,500 FV

CHAPTER 6 – 10

0 1

…

10(365

)

$6,500 FV

0 1

…

20(365

)

$6,500 FV

18. The time line is:

0 1

…

10(365

)

PV $80,000

PV = FV/(1 + r)t

It is important to note that compounding occurs daily. To account for this, we will divide the interest

rate by 365 (the number of days in a year, ignoring leap year), and multiply the number of periods by

365. Doing so, we get:

19. The APR is the interest rate per period times the number of periods in a year. In this case, the interest

rate is 27 percent per month, and there are 12 months in a year, so we get:

To find the EAR, we use the EAR formula:

Notice that we didn’t need to divide the APR by the number of compounding periods per year. We do

this division to get the interest rate per period, but in this problem we are already given the interest

rate per period.

CHAPTER 6 – 11

20. The time line is:

0 1

…

60

$84,500 C C C C C C C C C

We first need to find the annuity payment. We have the PVA, the length of the annuity, and the

interest rate. Using the PVA equation:

Solving for the payment, we get:

21. The time line is:

0 1

…

?

–

$18,000

$450 $450 $450 $450 $450 $450 $450 $450 $450

Here we need to find the length of an annuity. We know the interest rate, the PVA, and the payments.

Using the PVA equation:

Now we solve for t:

1/1.013t = 1 – ($18,000/$450)(.013)