43. The time line is:

0 1 2 3 4

0

0

0

We are given the total PV of all four cash flows. If we find the PV of the three cash flows we know, and

PV of Year 1 CF: $1,700/1.09 = $1,559.63

So, the PV of the missing CF is:

0 1 2 3 4

–

1

FV

The question asks for the value of the cash flow in Year 2, so we must find the future value of this

amount. The value of the missing CF is:

44. To solve this problem, we need to find the PV of each lump sum and add them together. It is

important to note that the first cash flow of $1 million occurs today, so we do not need to discount

that cash flow. The PV of the lottery winnings is:

45. Here we are finding the interest rate for an annuity cash flow. We are given the PVA, the number of

The time line is:

0 1

…

360

–

$2,720,0

00

$16,50

0

$16,50

0

$16,50

0

$16,50

0

$16,50

0

$16,50

0

$16,50

0

$16,50

0

$16,500

Using the PVA equation:

Unfortunately this equation cannot be solved to find the interest rate using algebra. To find the

The APR is the monthly interest rate times the number of months in the year, so:

And the EAR is:

46. The time line is:

0 4

PV $145,0

00

The profit the firm earns is just the PV of the sales price minus the cost to produce the asset. We find

the PV of the sales price as the PV of a lump sum:

And the firm’s profit is:

To find the interest rate at which the firm will break even, we need to find the interest rate using the

PV (or FV) of a lump sum. Using the PV equation for a lump sum, we get:

0 4

00

$91,700 = $145,000/(1 + r)4

47. The time line is:

0 123456 …20

PV $4,40

0

$4,40

0

$4,40

0

$4,40

0

We want to find the value of the cash flows today, so we will find the PV of the annuity, and then

bring the lump sum PV back to today. The annuity has 15 payments, so the PV of the annuity is:

Since this is an ordinary annuity equation, this is the PV one period before the first payment, so this

48. The time line is:

0 1

…

180

5

5

5

5

5

5

5

5

This question is asking for the present value of an annuity, but the interest rate changes during the

Note that this is the PV of this annuity exactly seven years from today. Now we can discount this

lump sum to today. The value of this cash flow today is:

Now we need to find the PV of the annuity for the first seven years. The value of these cash flows

today is:

The value of the cash flows today is the sum of these two cash flows, so:

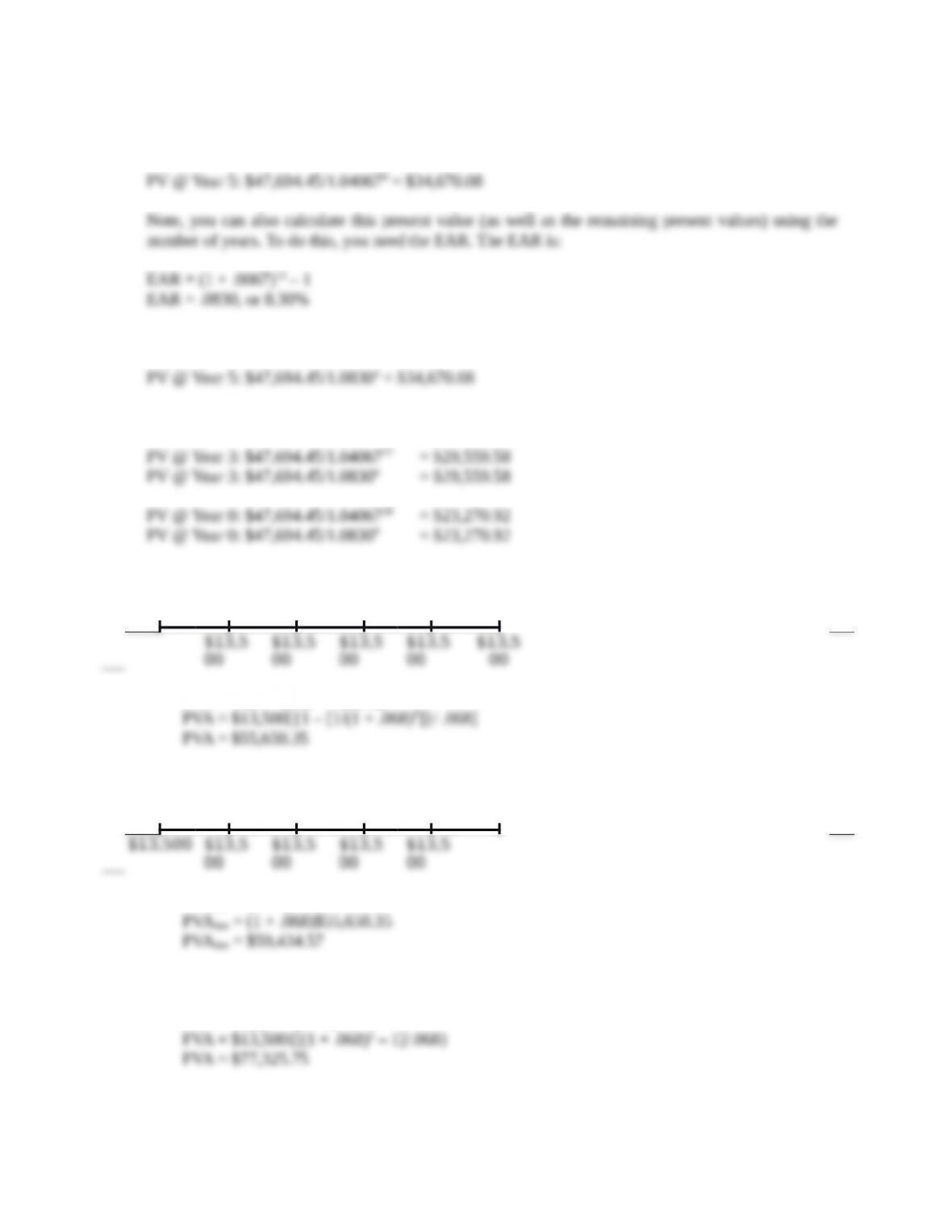

49. The time line for the annuity is:

0 1

…

156

0

0

0

0

0

0

0

0

Here we are trying to find the dollar amount invested today that will equal the FVA with a known

Now we have:

0 1 …13

PV $328,627

.03

So, we need to find the PV of a lump sum that will give us the same FV. Using the FV of a lump sum

with continuous compounding, we get:

FV = $328,627.03 = PVe–.07(13)

50. The time line is:

0 1

…

7

…

14 15 …∞

PV $6,400 $6,400 $6,400 $6,400

To find the value of the perpetuity at t = 7, we first need to use the PV of a perpetuity equation.

Using this equation we find:

0 1

…

7

…

14

PV $120,754

.72

Remember that the PV of a perpetuity (and annuity) equations give the PV one period before the first

51. The time line is:

0 1 …12

0

To find the APR and EAR, we need to use the actual cash flows of the loan. In other words, the

Again, we cannot solve this equation for r, so we need to solve this equation on a financial

calculator, using a spreadsheet, or by trial and error. Using a spreadsheet, we find:

So the APR that would legally have to be quoted is:

And the EAR is:

52. The time line is:

0 1

…

18 19 …28

To get the semiannual interest rate, we can use the EAR equation, but instead of using 12 months as

the exponent, we will use 6 months. The effective semiannual rate is:

Note, this is the value one period (six months) before the first payment, so it is the value at Year 9.

So, the value at the various times the questions asked for uses this value nine years from now.

So, we can find the PV at Year 5 using the following method as well:

The value of the annuity at the other times in the problem is:

53. a. If the payments are in the form of an ordinary annuity, the present value will be:

0 12345

PVA = C({1 – [1/(1 + r)t]}/r))

If the payments are an annuity due, the present value will be:

0 12345

PVAdue = (1 + r)PVA

b. We can find the future value of the ordinary annuity as:

FVA = C{[(1 + r)t – 1]/r}

If the payments are an annuity due, the future value will be:

FVAdue = (1 + r) FVA

c. Assuming a positive interest rate, the present value of an annuity due will always be larger than

54. The time line is:

0 1

…

59 60

–

$57,50

0

CCCCC CCCC

We need to use the PVA due equation, that is:

Using this equation:

Notice, to find the payment for the PVA due we compound the payment for an ordinary annuity

forward one period.

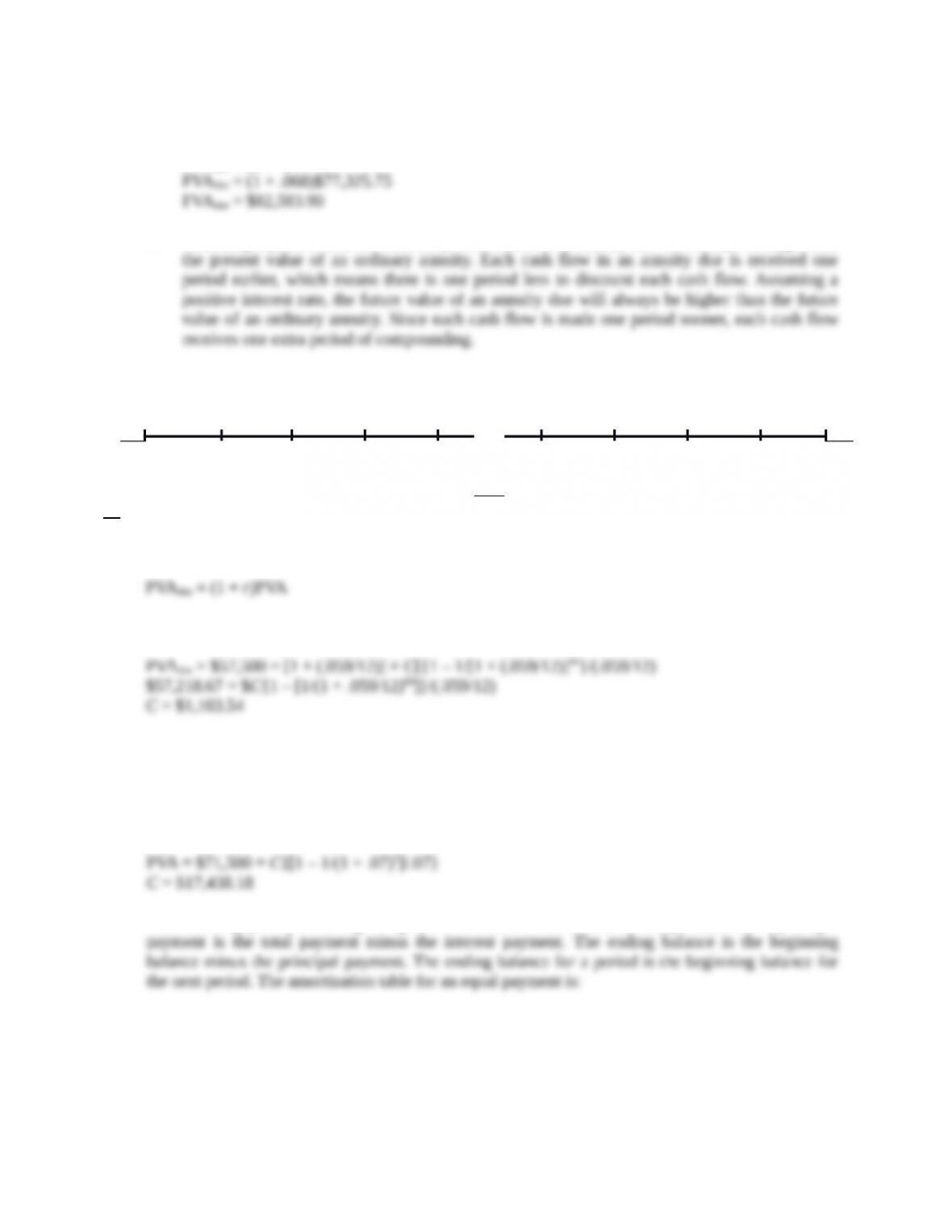

55. The payment for a loan repaid with equal payments is the annuity payment with the loan value as the

PV of the annuity. So, the loan payment will be:

The interest payment is the beginning balance times the interest rate for the period, and the principal

Year

Beginning

Balance

Total

Payment

Interest

Payment

Principal

Payment

Ending

Balance

1 $71,500.00 $17,438.18 $5,005.00 $12,433.18 $59,066.82

56. This amortization table calls for equal principal payments of $14,300 per year. The interest payment

Year

Beginning

Balance

Total

Payment

Interest

Payment

Principal

Payment

Ending

Balance

1 $71,500.00 $19,305.00 $5,005.00 $14,300.00 $57,200.00

2 57,200.00 18,304.00 4,004.00 14,300.00 42,900.00

In the third year, $3,003 of interest is paid.

Challenge

57. The time line is:

0 1

…

120 …360 361 …660

0

The cash flows for this problem occur monthly, and the interest rate given is the EAR. Since the cash

EAR = .10 = [1 + (APR/12)]12 – 1

And the post-retirement APR is:

First, we will calculate how much he needs at retirement. The amount needed at retirement is the PV

of the monthly spending plus the PV of the inheritance. The PV of these two cash flows is:

So, at retirement, he needs:

He will be saving $2,350 per month for the next 10 years until he purchases the cabin. The value of

his savings after 10 years will be:

After he purchases the cabin, the amount he will have left is:

He still has 20 years until retirement. When he is ready to retire, this amount will have grown to:

So, when he is ready to retire, based on his current savings, he will be short:

This amount is the FV of the monthly savings he must make between Years 10 and 30. So, finding

the annuity payment using the FVA equation, we find his monthly savings will need to be:

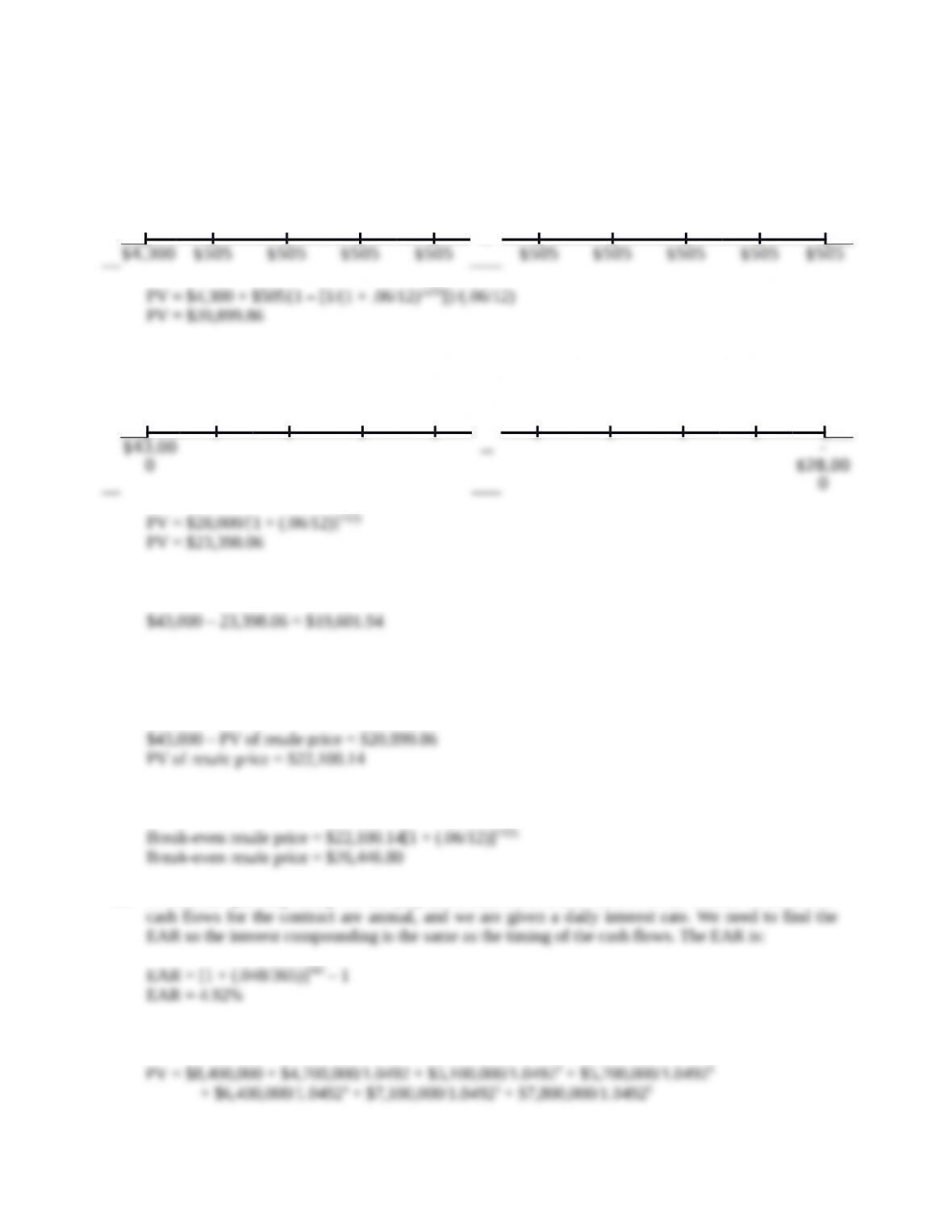

58. To answer this question, we should find the PV of both options, and compare them. Since we are

purchasing the car, the lowest PV is the best option. The PV of leasing is the PV of the lease

payments, plus the $4,300. The interest rate we would use for the leasing option is the same as the

interest rate of the loan. The PV of leasing is:

0 1

…

36

The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV

of the resale price is:

0 1

36

The PV of the decision to purchase is:

In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is

lower. To find the break-even resale price, we need to find the resale price that makes the PV of the

two options the same. In other words, the PV of the decision to buy should be:

The break-even resale price is the FV of this value, so:

59. To find the quarterly salary for the player, we first need to find the PV of the current contract. The

The PV of the current contract offer is the sum of the PV of the cash flows. So, the PV is:

The player wants the contract increased in value by $2,000,000, so the PV of the new contract will

be:

The player has also requested a signing bonus payable today in the amount of $10 million. We can

subtract this amount from the PV of the new contract. The remaining amount will be the PV of the

future quarterly paychecks.

To find the quarterly payments, first realize that the interest rate we need is the effective quarterly

Now we have the interest rate, the length of the annuity, and the PV. Using the PVA equation and

solving for the payment, we get:

60. The time line is:

0 1

$21,275 –

$25,00

0

To find the APR and EAR, we need to use the actual cash flows of the loan. In other words, the

interest rate quoted in the problem is only relevant to determine the total interest under the terms

given. The cash flows of the loan are the $25,000 you must repay in one year, and the $21,275 you

borrow today. The interest rate of the loan is: