15. a. If the project is a success, the present value of the future cash flows will be:

From the previous question, if the quantity sold is 3,900, we would abandon the project, and the

The NPV is the present value of the expected value in one year minus the cost of the

equipment, so:

b. If we couldn’t abandon the project, the present value of the future cash flows when the quantity

is 3,900 will be:

The gain from the option to abandon is the abandonment value minus the present value of the

cash flows if we cannot abandon the project, so:

We need to find the value of the option to abandon times the likelihood of abandonment. So, the

value of the option to abandon today is:

16. If the project is a success, the present value of the future cash flows will be:

If the sales are only 3,900 units, from Problem 14, we know we will abandon the project, with a

The NPV is the present value of the expected value in one year minus the cost of the equipment, so:

The gain from the option to expand is the present value of the cash flows from the additional units

sold, so:

We need to find the value of the option to expand times the likelihood of expansion. We also need to

find the value of the option to expand today, so:

17. a. The value of the call is the maximum of the stock price minus the present value of the exercise

price, or zero, so:

The option isn’t worth anything.

b. The stock price is too low for the option to finish in the money. The minimum return on the

stock required to get the option in the money is:

which is much higher than the risk-free rate of interest.

18. B is the more typical case; A presents an arbitrage opportunity. You could buy the bond for $800 and

19. a. The conversion ratio is given at 18. The conversion price is the par value divided by the

conversion ratio, so:

The conversion premium is the percent increase in stock price that results in no profit when the

bond is converted, so:

b. The straight bond value is:

And the conversion value is the conversion ratio times the stock price, so:

c. We need to set the straight bond value equal to the conversion ratio times the stock price, and

solve for the stock price, so:

d. There are actually two option values to consider with a convertible bond. The conversion option

20. a. The NPV of the project is the sum of the present value of the cash flows generated by the

project. The cash inflows from this project are an annuity, so the NPV is:

b. The company should abandon the project if the PV of the revised cash flows for the next seven

years is less than the project’s aftertax salvage value. Since the option to abandon the project occurs in

Aftertax salvage value = C2(PVIFA11%,7)

Challenge

21. The straight bond value today is:

And the conversion value of the bond today is:

We expect the bond to be called when the conversion value increases to $1,300, so we need to find

the number of periods it will take for the current conversion value to reach the expected value at

which the bond will be converted. Doing so, we find:

The bond value is the present value of the expected cash flows. The cash flows will be the annual

coupon payments plus the conversion price. The present value of these cash flows is:

22. We will use the bottom up approach to calculate the operating cash flow. Assuming we operate the

project for all four years, the cash flows are:

Year 0 1 2 3 4

Sales $10,100,000 $10,100,000 $10,100,000 $10,100,000

Change in NWC –$900,000 0 0 0 $900,000

There is no salvage value for the equipment. The NPV is:

b. The cash flows if we abandon the project after one year are:

Year 0 1

Sales $10,100,000

EBT $2,800,000

Change in NWC –$900,000 $900,000

The book value of the equipment is:

So, the taxes on the salvage value will be:

This makes the aftertax salvage value:

The NPV if we abandon the project after one year is:

If we abandon the project after two years, the cash flows are:

Year 0 1 2

Sales $10,100,000 $10,100,000

Change in NWC –$900,000 0 $900,000

The book value of the equipment is:

So the taxes on the salvage value will be:

This makes the aftertax salvage value:

The NPV if we abandon the project after two years is:

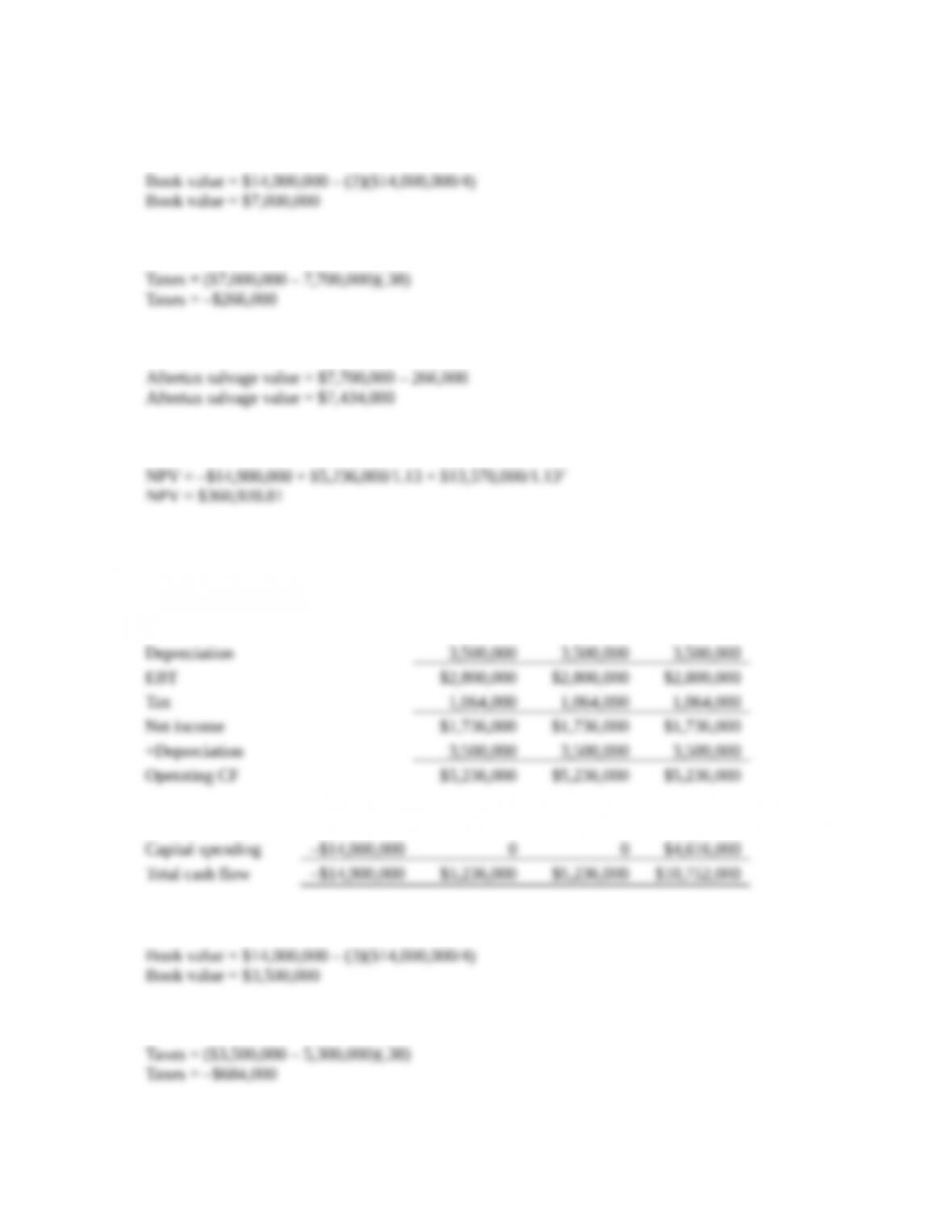

If we abandon the project after three years, the cash flows are:

Year 0 1 2 3

Sales $10,100,000 $10,100,000 $10,100,000

Operating costs 3,800,000 3,800,000 3,800,000

Change in NWC –$900,000 0 0 $900,000

The book value of the equipment is:

So the taxes on the salvage value will be:

This makes the aftertax salvage value:

The NPV if we abandon the project after three years is:

We should abandon the equipment after three years since the NPV of abandoning the project after

three years has the highest NPV.