CHAPTER 16

STEPHENSON REAL ESTATE

RECAPITALIZATION

1. If Stephenson wishes to maximize the overall value of the firm, it should use debt to finance the $85

2. Since Stephenson is an all-equity firm with 8 million shares of common stock outstanding, worth

So, the market value balance sheet before the land purchase is:

Market value balance sheet

3. a. As a result of the purchase, the firm’s pretax earnings will increase by $14.125 million per year

Since Stephenson is an all-equity firm, the appropriate discount rate is the firm’s unlevered cost

of equity, so the NPV of the purchase is:

CHAPTER 16 C-2

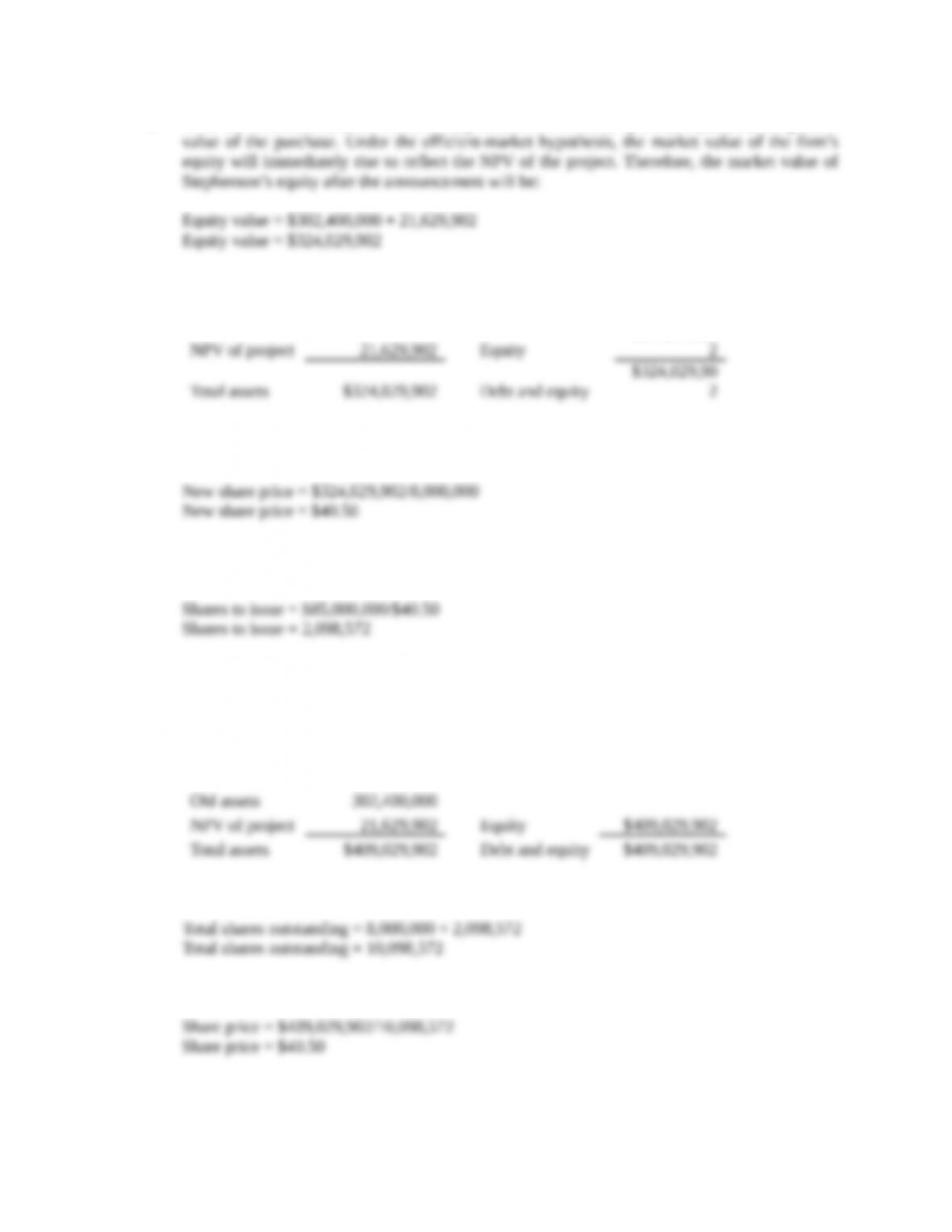

b. After the announcement, the value of Stephenson will increase by $21,629,902, the net present

Market value balance sheet

Old assets $302,400,000

$324,029,90

Since the market value of the firm’s equity is $324,029,902 and the firm has 8 million shares of

common stock outstanding, Stephenson’s stock price after the announcement will be:

Since Stephenson must raise $85 million to finance the purchase and the firm’s stock is worth

$40.50 per share, Stephenson must issue:

c. Stephenson will receive $85 million in cash as a result of the equity issue. This will increase the

firm’s assets and equity by $85 million. So, the new market value balance sheet after the stock

issue will be:

Market value balance sheet

Cash $85,000,000

The stock price will remain unchanged. To show this, Stephenson will now have:

So, the share price is:

CHAPTER 16 C-3

d. The project will generate $14.125 million of additional annual pretax earnings forever. These

earnings will be taxed at a rate of 23 percent. Therefore, after taxes, the project increases the

annual earnings of the firm by $10,876,250. So, the aftertax present value of the earnings

increase is:

So, the market value balance sheet of the company will be:

Market value balance sheet

Old assets $302,400,000

4. a. Modigliani-Miller Proposition I states that in a world with corporate taxes:

As was shown in Question 3, Stephenson will be worth $409,029,902 if it finances the purchase

b. After the announcement, the value of Stephenson will immediately rise by the present value of

the project. Since the market value of the firm’s debt is $85 million and the value of the firm is

Market value balance sheet

Value unlevered $409,029,902 Debt $ 85,000,000

Since the market value of Stephenson’s equity is $343,579,902 and the firm has 8 million

shares of common stock outstanding, Stephenson’s stock price after the debt issue will be:

5. If Stephenson uses equity in order to finance the project, the firm’s stock price will remain at $40.50