CHAPTER 18

SHORT-TERM FINANCE AND PLANNING

Answers to Concepts Review and Critical Thinking Questions

1. These are firms with relatively long inventory periods and/or relatively long receivables periods.

2. These are firms that have a relatively long time between the time purchased inventory is paid for and

3. a. Use: The cash balance declined by $200 to pay the dividend.

b. Source: The cash balance increased by $500, assuming the goods bought on payables credit

were sold for cash.

4. Carrying costs will decrease because they are not holding goods in inventory. Shortage costs will

5. Since the cash cycle equals the operating cycle minus the accounts payable period, it is not possible

6. It lengthened its payables period, thereby shortening its cash cycle. It will have no effect on the

8. It is sometimes argued that large firms take advantage of smaller firms by threatening to take their

9. They would like to! The payables period is a subject of much negotiation, and it is one aspect of the

CHAPTER 18 – 2

10. BlueSky will need less financing because it is essentially borrowing more from its suppliers. Among

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. a. No change. A dividend paid for by the sale of debt will not change cash since the cash raised

from the debt offer goes immediately to shareholders.

b. No change. The real estate is paid for by the cash raised from the debt, so this will not change

the cash balance.

CHAPTER 18 – 3

2. The total liabilities and equity of the company are the value of equity, plus current liabilities and

long-term debt, so:

We have NWC other than cash. Since NWC is current assets minus current liabilities, NWC other

than cash is:

NWC other than cash = Accounts receivable + Inventory – Current liabilities

$2,750 = Accounts receivable + Inventory – $2,025

Since total assets must equal total liabilities and equity, we can solve for cash as:

Cash = Total assets – Fixed assets – (Accounts receivable + Inventory)

So, the current assets are:

3. a. Increase. If receivables go up, the time to collect the receivables would increase, which

b. Increase. If credit repayment times are increased, customers will take longer to pay their bills,

4. a. Increase; Increase. If the terms of the cash discount are made less favorable to customers, the

b. Increase; No change. This will shorten the accounts payable period, which will increase the

CHAPTER 18 – 4

c. Decrease; Decrease. If more customers pay in cash, the accounts receivable period will

d. Decrease; Decrease. Assume the accounts payable period does not change. Fewer raw materials

e. Decrease; No change. If more raw materials are purchased on credit, the accounts payable

period will tend to increase, which would decrease the cash cycle. We should say that this may

f. Increase; Increase. If more goods are produced for inventory, the inventory period will increase.

5. a. A 45-day collection period implies all receivables outstanding from the previous quarter are

Q1 Q2 Q3 Q4

Beginning receivables $365.00 $425.00 $440.00 $480.00

b. A 60-day collection period implies all receivables outstanding from the previous quarter are

collected in the current quarter, and:

Q1 Q2 Q3 Q4

Beginning receivables $365.00 $566.67 $586.67 $640.00

CHAPTER 18 – 5

c. A 30-day collection period implies all receivables outstanding from the previous quarter are

collected in the current quarter, and:

Q1 Q2 Q3 Q4

Beginning receivables $365.00 $283.33 $293.33 $320.00

6. The operating cycle is the inventory period plus the receivables period. The inventory turnover and

inventory period are:

Inventory turnover = COGS/Average inventory

Inventory period = 365 days/Inventory turnover

And the receivables turnover and receivables period are:

Receivables turnover = Credit sales/Average receivables

Receivables period = 365 days/Receivables turnover

So, the operating cycle is:

The cash cycle is the operating cycle minus the payables period. The payables turnover and payables

period are:

Payables turnover = COGS/Average payables

Payables period = 365 days/Payables turnover

CHAPTER 18 – 6

So, the cash cycle is:

7. If we factor immediately, we receive cash an average of 31 days sooner. The number of periods in a

year are:

The EAR of this arrangement is:

EAR = (1 + Periodic rate)m – 1

8. a. The payables period is zero since the company pays immediately. The payment in each period

is 30 percent of next period’s sales, so:

Q1 Q2 Q3 Q4

b. Since the payables period is 90 days, the payment in each period is one-third of the current

period’s sales, so:

Q1 Q2 Q3 Q4

c. Since the payables period is 60 days, the payment in each period is two-thirds of last quarter’s

orders, plus one-third of this quarter’s orders, or:

Q1 Q2 Q3 Q4

CHAPTER 18 – 7

9. Since the payables period is 60 days, the payables in each period will be:

Q1 Q2 Q3 Q4

Payment of accounts $1,351.25 $1,485.00 $1,287.50 $1,271.25

10. a. The November sales must have been the total uncollected sales minus the uncollected sales

from December, divided by the collection rate two months after the sale, so:

b. The December sales are the uncollected sales from December divided by the collection rate of

the previous months’ sales, so:

c. The collections each month for this company are:

CHAPTER 18 – 8

11. The sales collections each month will be:

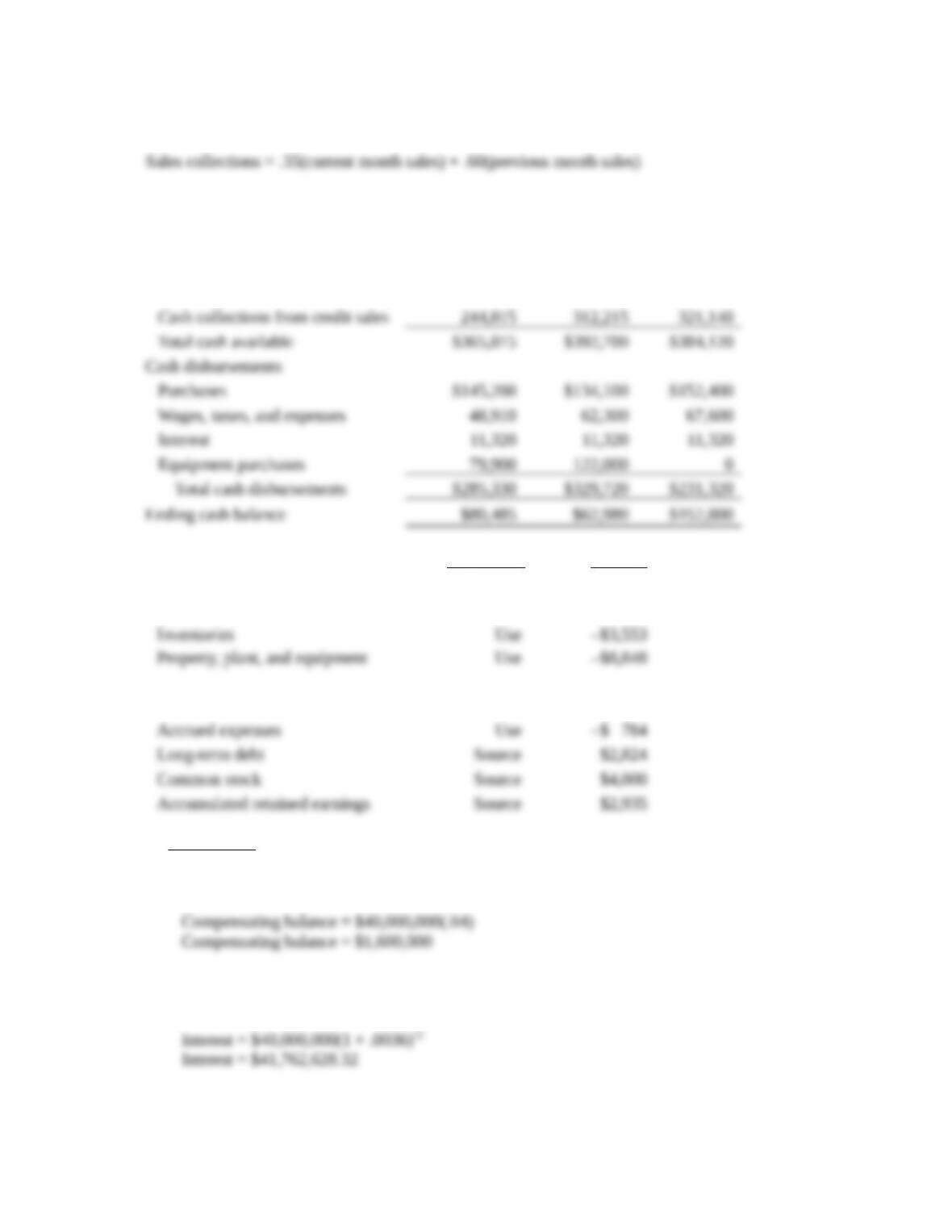

Given this collection, the cash budget will be:

April May June

Beginning cash balance $121,000 $80,485 $62,980

Cash receipts

12. Item Source/Use Amount

Cash Source $1,021

Accounts receivable Use –$4,163

Accounts payable Source $1,487

Intermediate

13. a. If you borrow $40,000,000, the compensating balance will be:

Your total repayment will be based on the full amount of the loan including the compensating

balance, so at the end of the year you will owe:

CHAPTER 18 – 9

You will receive your compensating balance back at the end, so the year-end cash flow will be:

However, with the compensating balance, you will only get the use of:

This means the periodic interest rate is:

FV = PV(1 + R)

b. To end up with $13,000,000, you must borrow:

The total interest you will pay on the loan is:

14. a. The EAR of your investment account is:

b. To calculate the EAR of the loan, we can divide the interest on the loan by the amount of the

And the interest you will pay to the bank on the loan is:

So, the EAR of the loan in the amount of $30 million is:

CHAPTER 18 – 10

c. The compensating balance is only applied to the unused portion of the credit line, so the EAR

of a loan on the full credit line is: