22. The time line is:

0 1

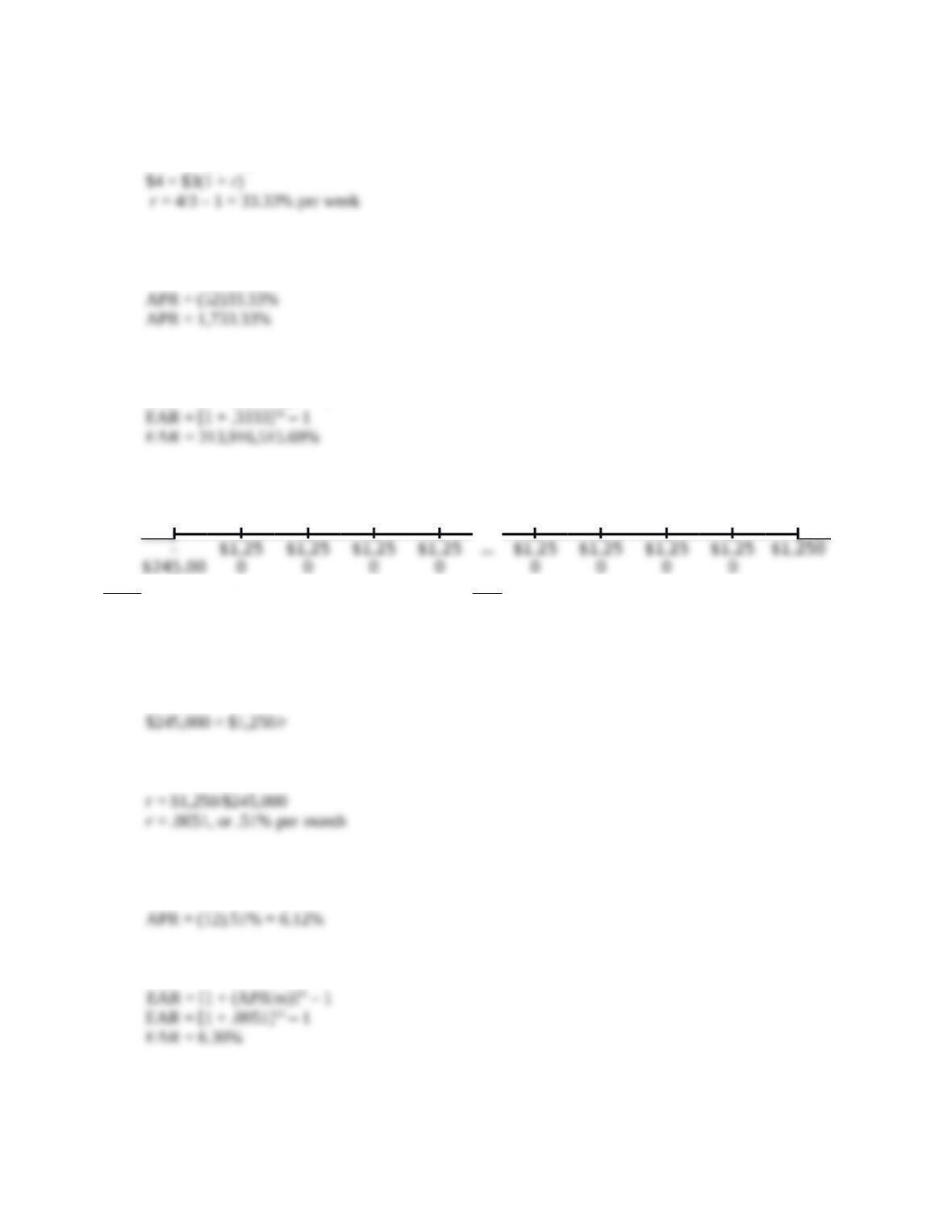

Here we are trying to find the interest rate when we know the PV and FV. Using the FV equation:

FV = PV(1 + r)

The interest rate is 33.33% per week. To find the APR, we multiply this rate by the number of weeks

in a year, so:

And using the equation to find the EAR:

EAR = [1 + (APR/m)]m – 1

23. The time line is:

0 1

∞

$245,00

0

0

0

0

0

0

0

0

0

Here we need to find the interest rate that equates the perpetuity cash flows with the PV of the cash

flows. Using the PV of a perpetuity equation:

PV = C/r

We can now solve for the interest rate as follows:

The interest rate is .51% per month. To find the APR, we multiply this rate by the number of months

in a year, so:

And using the equation to find an EAR:

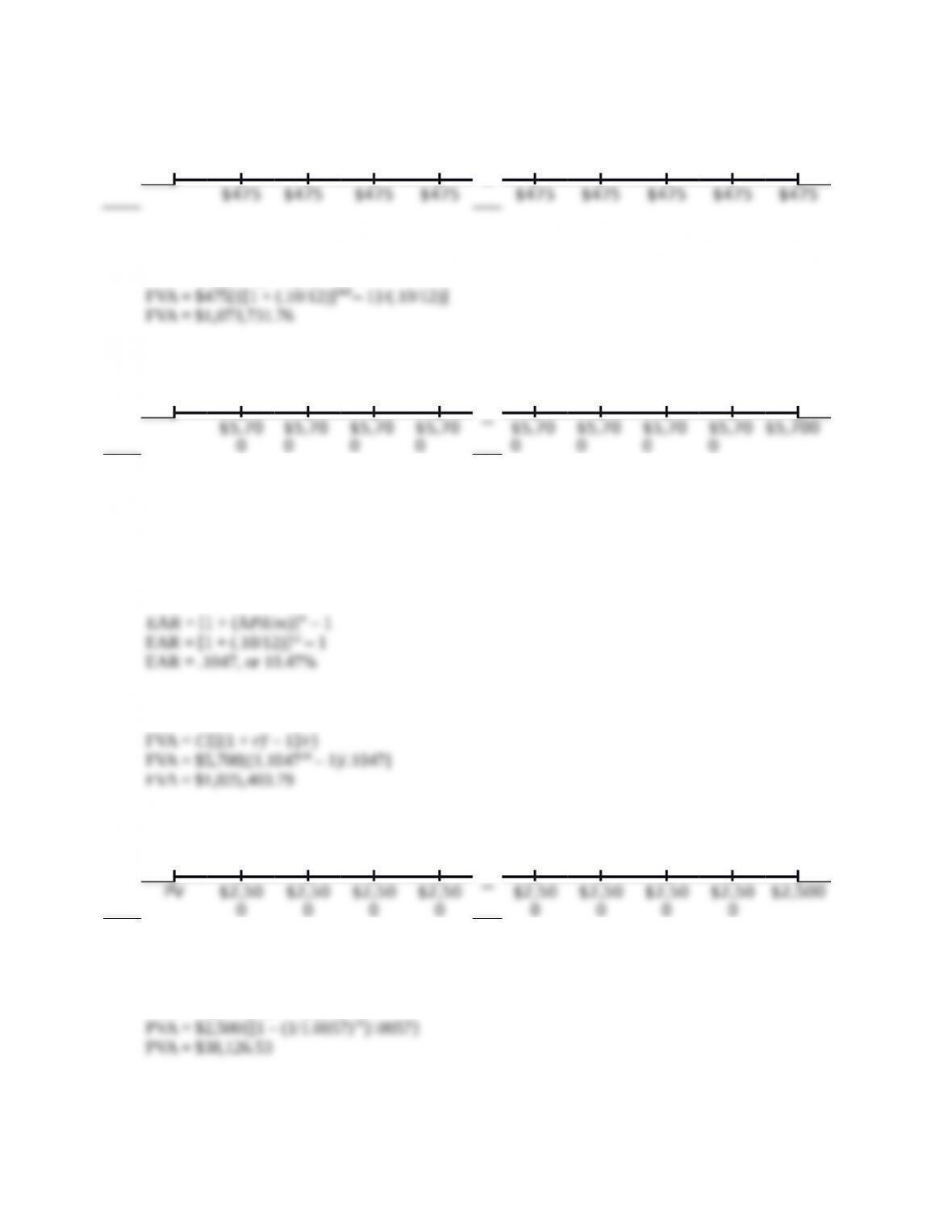

24. The time line is:

0 1

…

360

This problem requires us to find the FVA. The equation to find the FVA is:

FVA = C{[(1 + r)t – 1]/r}

25. The time line is:

0 1

…

30

0

0

0

0

0

0

0

0

In the previous problem, the cash flows are monthly and the compounding period is monthly. The

compounding periods are still monthly, but since the cash flows are annual, we need to use the EAR

to calculate the future value of annual cash flows. It is important to remember that you have to make

sure the compounding periods of the interest rate are the same as the timing of the cash flows. In this

case, we have annual cash flows, so we need the EAR since it is the true annual interest rate you will

earn. So, finding the EAR:

Using the FVA equation, we get:

26. The time line is:

0 1

…

16

0

0

0

0

0

0

0

0

The cash flows are an annuity with four payments per year for four years, or 16 payments. We can

use the PVA equation:

PVA = C({1 – [1/(1 + r)t]}/r)

27. The time line is:

01234

The cash flows are annual and the compounding period is quarterly, so we need to calculate the EAR

EAR = [1 + (APR/m)]m – 1

And now we use the EAR to find the PV of each cash flow as a lump sum and add them together:

28. The time line is:

01234

Here the cash flows are annual and the given interest rate is annual, so we can use the interest rate

Intermediate

29. The total interest paid by First Simple Bank is the interest rate per period times the number of

(1 + r)10 – 1

Setting the two equal, we get:

30. Here we need to convert an EAR into interest rates for different compounding periods. Using the

equation for the EAR, we get:

EAR = [1 + (APR/m)]m – 1

Notice that the effective six-month rate is not twice the effective quarterly rate because of the effect

of compounding.

31. Here we need to find the FV of a lump sum, with a changing interest rate. We must do this problem

in two parts. After the first six months, the balance will be:

This is the balance in six months. The FV in another six months will be:

The problem asks for the interest accrued, so, to find the interest, we subtract the beginning balance

from the FV. The interest accrued is:

32. Although the stock and bond accounts have different interest rates, we can draw one time line, but

we need to remember to apply different interest rates. The time line is:

0 1

…

360

…

660

We need to find the annuity payment in retirement. Our retirement savings ends and the retirement

Stock account:

Bond account:

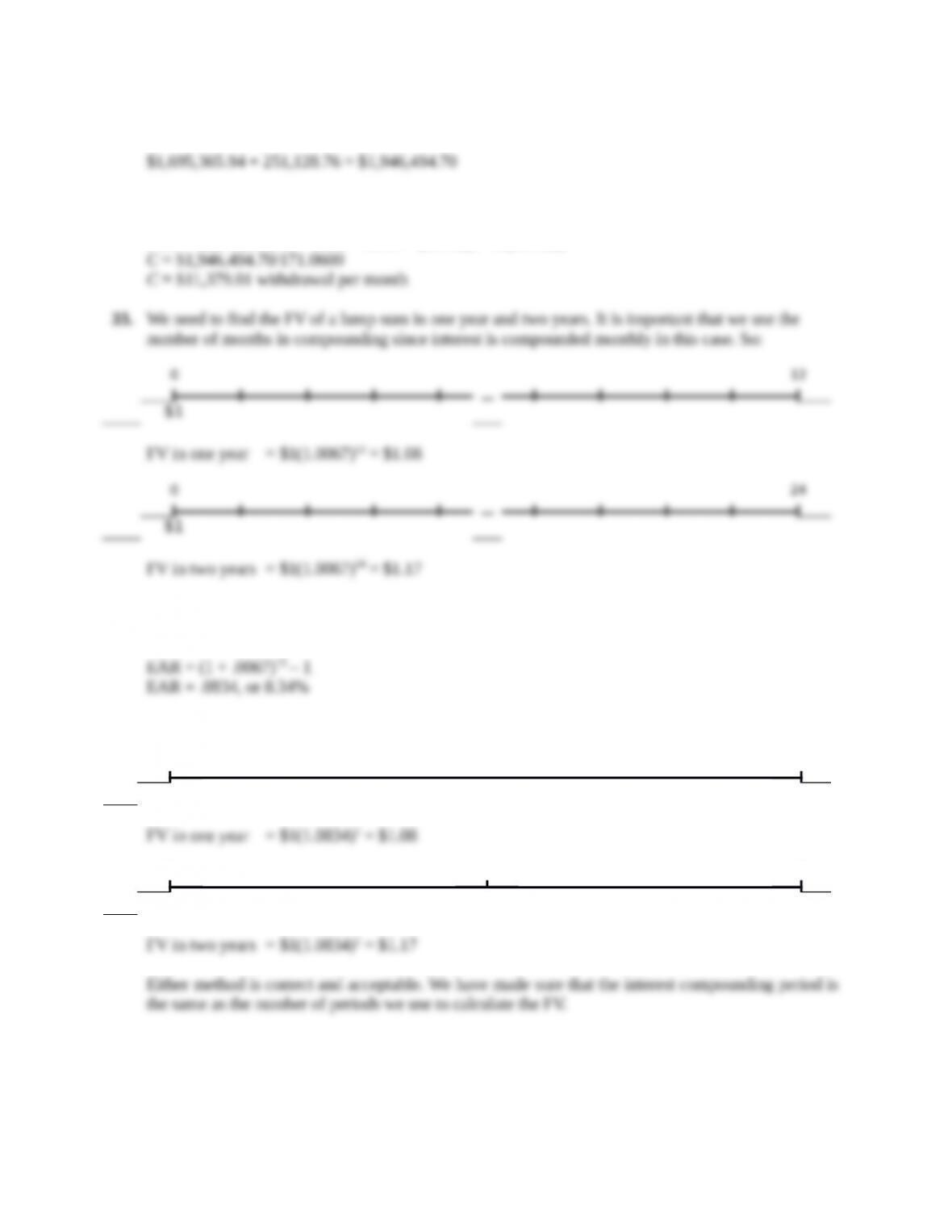

So, the total amount saved at retirement is:

Solving for the withdrawal amount in retirement using the PVA equation gives us:

0

…

24

$1

There is also another common alternative solution. We could find the EAR, and use the number of

years as our compounding periods. So we will find the EAR first:

Using the EAR and the number of years to find the FV, we get:

0 1

$1 FV

0 1 2

$1 FV

34. Here we are finding the annuity payment necessary to achieve the same FV. The interest rate given is

an APR of 9.7 percent, with monthly deposits. We must make sure to use the number of months in

the equation. So, using the FVA equation:

Starting today:

0 1 …480

$1,000,0

00

CCCC CCCC C

Starting in 10 years:

0 1

…

120 121

…

480

$1,000,0

00

CCCCCC C

Starting in 20 years:

0 1 …240 241 …480

$1,000,0

00

C C C C C

Notice that a deposit for half the length of time, i.e., 20 years versus 40 years, does not mean that the

annuity payment is doubled. In this example, by reducing the savings period by one-half, the deposit

necessary to achieve the same ending value is about 8 times as large.

35. The time line is:

0 4

$1 $3

Since we are looking to triple our money, the PV and FV are irrelevant as long as the FV is three

times as large as the PV. The number of periods is four, the number of quarters per year. So:

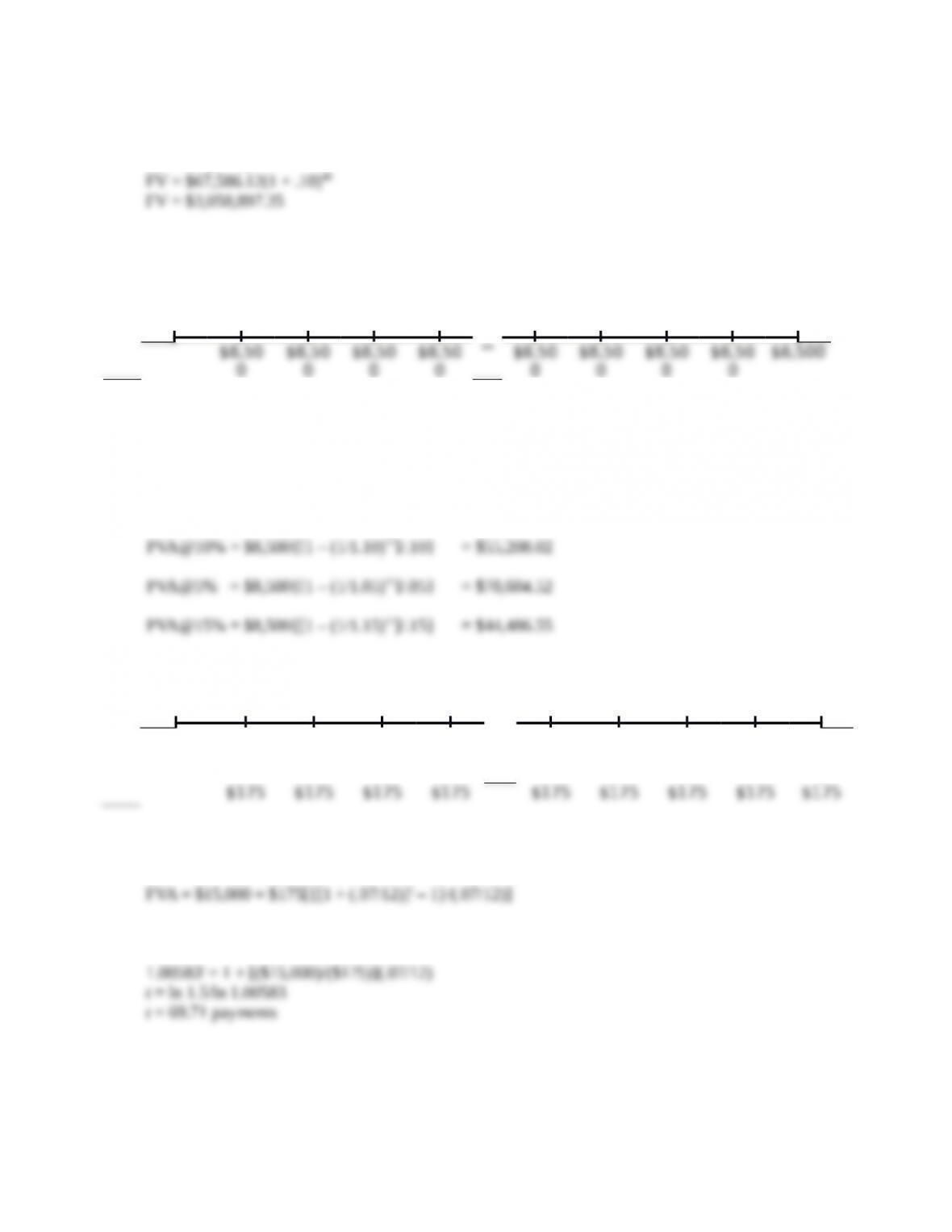

36. Here we need to compare two cash flows, so we will find the value today of both sets of cash flows.

We need to make sure to use the monthly cash flows since the salary is paid monthly. Doing so, we

find:

0 1

…

24

0 1

…

24

37. We can use the present value of a growing annuity equation to find the value of your winnings today.

Doing so, we find:

PV = C{[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]t}

38. Since your salary grows at 3 percent per year, your salary next year will be:

This means your deposit next year will be:

Since your salary grows at 3 percent, your deposit will also grow at 3 percent. We can use the present

value of a growing annuity equation to find the value of your deposits today. Doing so, we find:

Now, we can find the future value of this lump sum in 40 years. We find:

FV = PV(1 + r)t

This is the value of your savings in 40 years.

39. The time line is:

0 1

…

11

0

0

0

0

0

0

0

0

The relationships between the present value of an annuity and the interest rate are:

PVA falls as r increases, and PVA rises as r decreases

FVA rises as r increases, and FVA falls as r decreases

The present values of $8,500 per year for 11 years at the various interest rates given are:

40. The time line is:

0 1

…

?

–

$15,00

0

Here we are given the FVA, the interest rate, and the amount of the annuity. We need to solve for the

number of payments. Using the FVA equation:

Solving for t, we get:

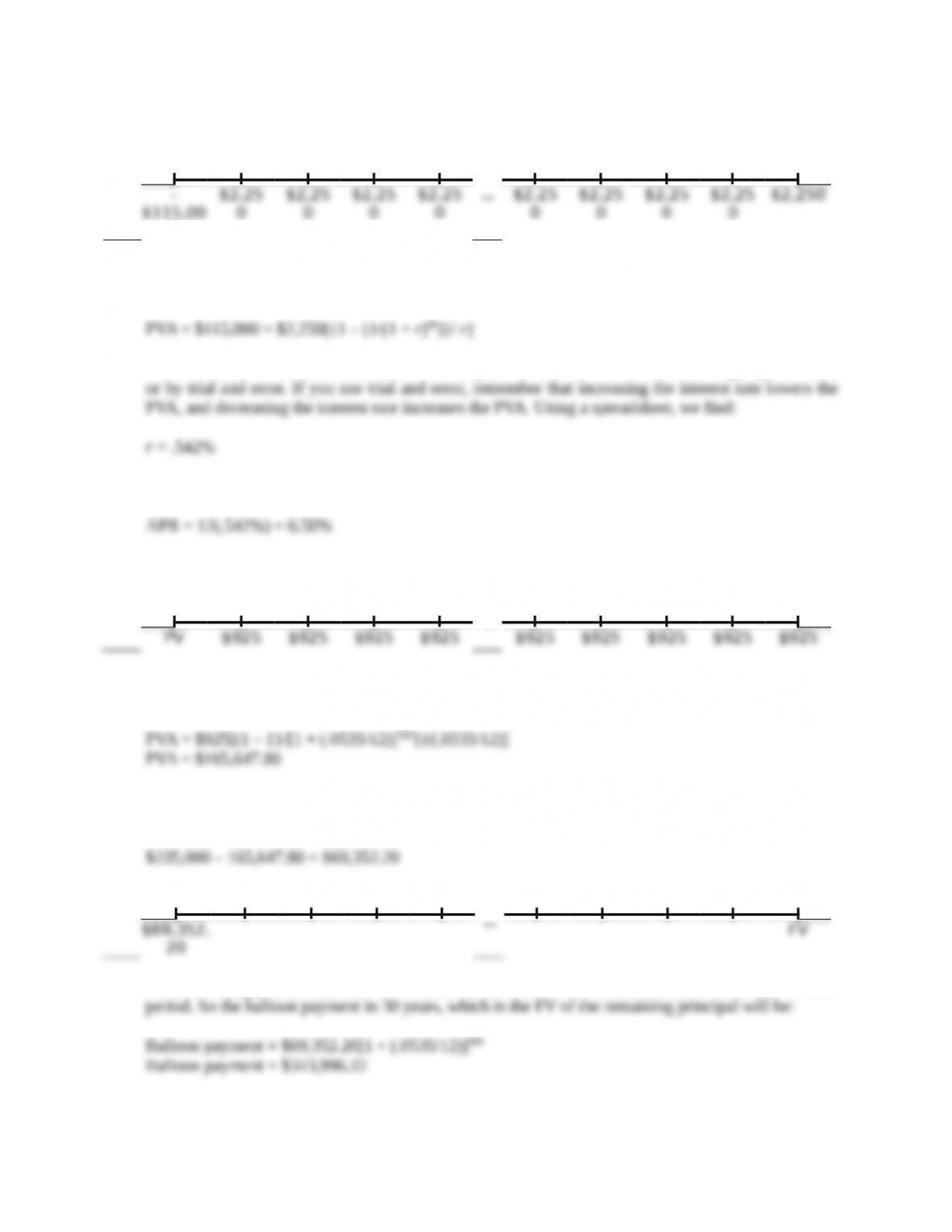

41. The time line is:

0 1

60

$115,00

0

0

0

0

0

0

0

0

0

Here we are given the PVA, number of periods, and the amount of the annuity. We need to solve for

the interest rate. Using the PVA equation:

To find the interest rate, we need to solve this equation on a financial calculator, using a spreadsheet,

The APR is the periodic interest rate times the number of periods in the year, so:

42. The time line is:

0 1

…

360

The amount of principal paid on the loan is the PV of the monthly payments you make. So, the

present value of the $925 monthly payments is:

The monthly payments of $925 will amount to a principal payment of $165,647.80. The amount of

principal you will still owe is:

0 1

…

360

This remaining principal amount will increase at the interest rate on the loan until the end of the loan