61. The time line is:

–24 –23

…

–12 –11

…

0 1 …60

0

Here we have cash flows that would have occurred in the past and cash flows that will occur in the

To find the value today of the back pay from two years ago, we will find the FV of the annuity, and

then find the FV of the lump sum. Doing so gives us:

Notice we found the FV of the annuity with the effective monthly rate, and then found the FV of the

lump sum with the EAR. Alternatively, we could have found the FV of the lump sum with the

effective monthly rate as long as we used 12 periods. The answer would be the same either way.

Now, we need to find the value today of last year’s back pay:

Next, we find the value today of the five years’ future salary:

The value today of the jury award is the sum of salaries, plus the compensation for pain and

suffering, and court costs. The award should be for the amount of:

As the plaintiff, you would prefer a lower interest rate. In this problem, we are calculating both the

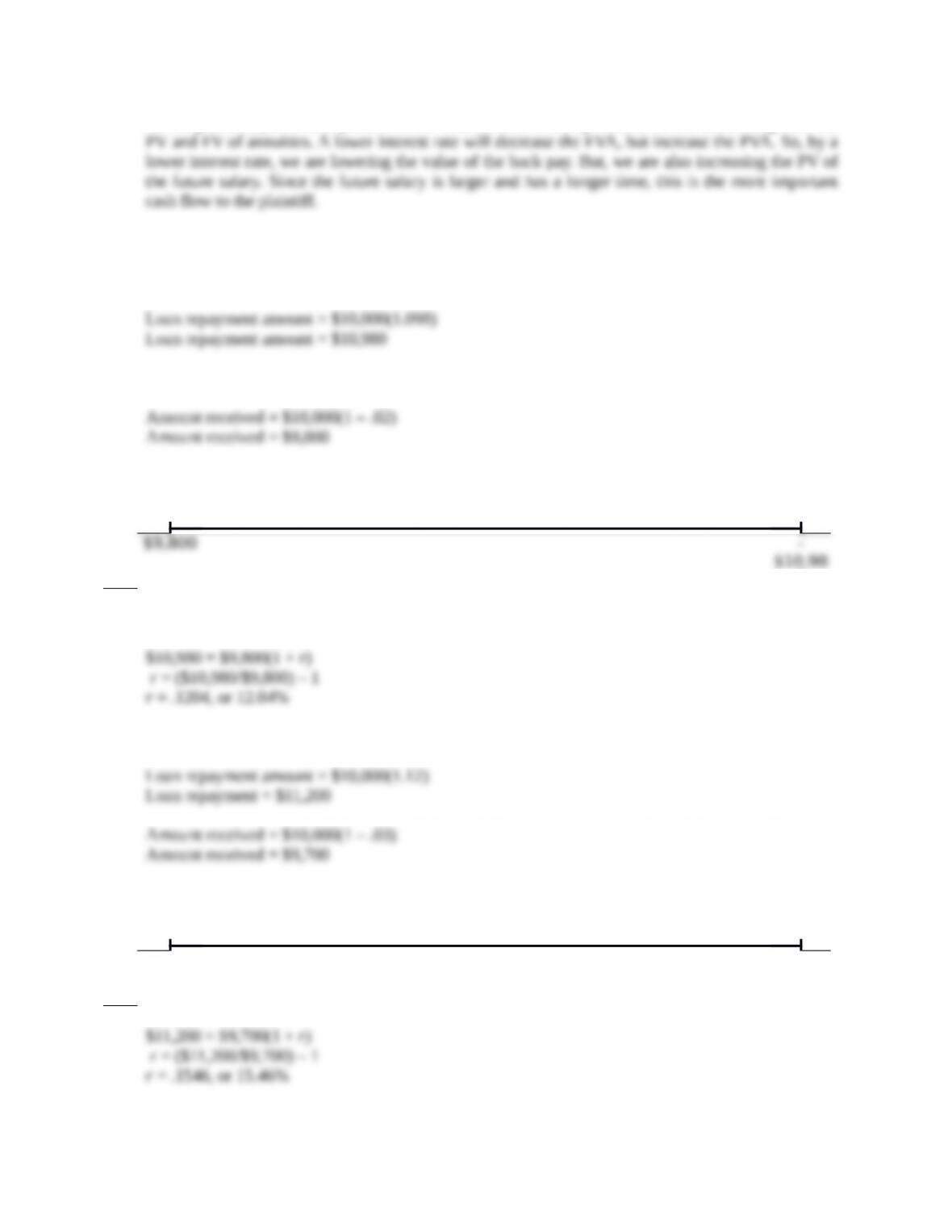

62. Again, to find the interest rate of a loan, we need to look at the cash flows of the loan. Since this loan

is in the form of a lump sum, the amount you will repay is the FV of the principal amount, which

will be:

The amount you will receive today is the principal amount of the loan times one minus the points.

The time line is:

0 1

$10,98

0

Now, we find the interest rate for this PV and FV.

63. This is the same question as before, with different values. So:

The time line is:

0 1

$9,700 –

$11,20

0

The effective rate is not affected by the loan amount since it drops out when solving for r.

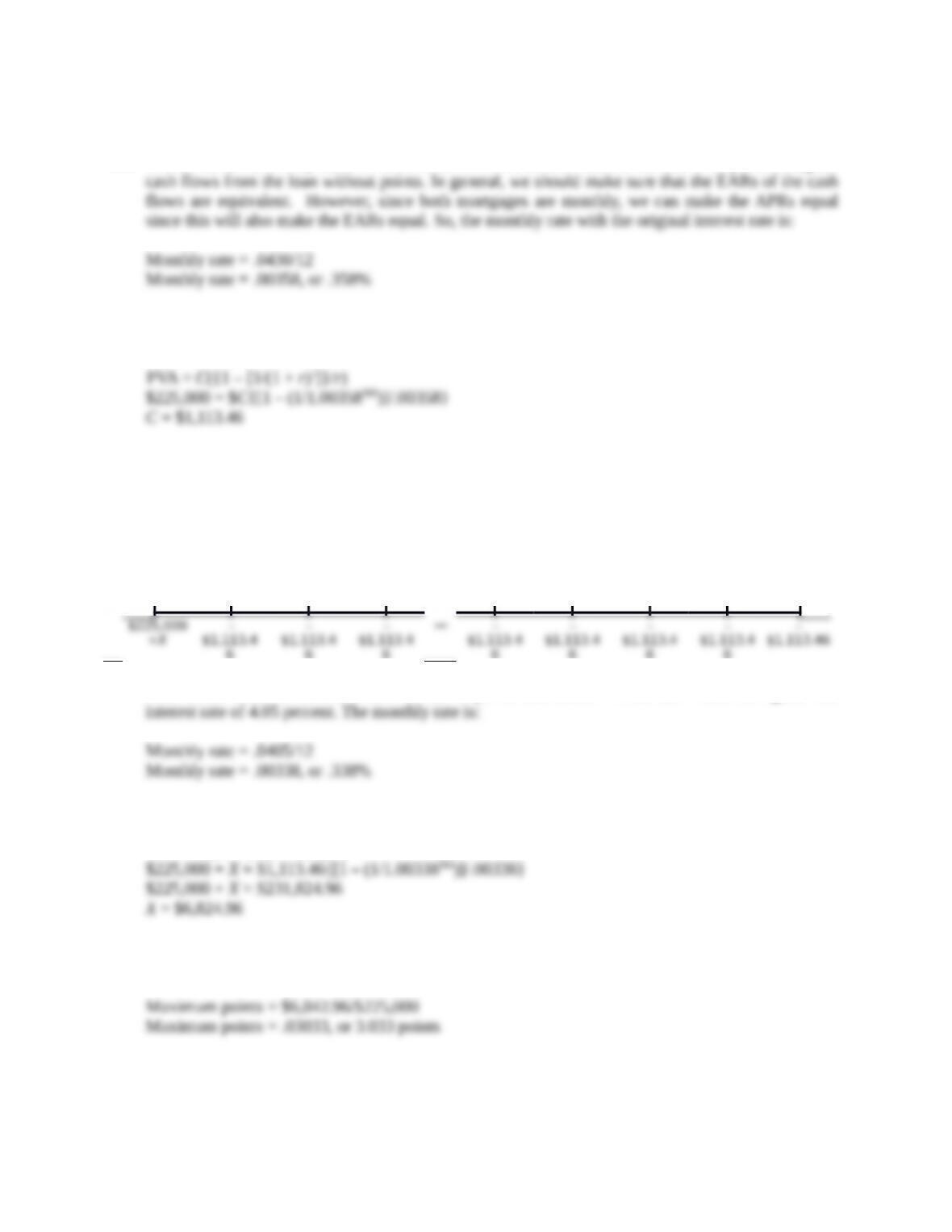

64. To find the break-even points, we need to solve for the interest rate for the loan with points using the

The payments for the loan with the points is based off the original amount borrowed and the original

interest rate will be:

The amount actually received up front on the mortgage is the amount borrowed plus the points.

Letting X be the dollar amount of the points, we get:

Amount borrowed = $225,000 + X

So, the time line is:

0 1

360

6

6

6

6

6

6

6

Now we can solve for the maximum number of points that results in these cash flows having the new

Solving the cash flows for the maximum points, we find:

PVA = C({1 – [1/(1 + r) t]}/r)

Since this is the maximum dollar amount we would pay and the points are a percentage of the

amount borrowed, we find:

65. We will have the same loan payments as in the previous problem for the first 8 years, but now there

will be a balloon payment at the end of 8 years. Since there will be 22 years, or 264 months, of

payments not made, the balloon payment will be:

PVA = C({1 – [1/(1 + r) t]}/r)

So, the time line is:

0 1

96

To find the maximum number of points we would be willing to pay, we need to set the APR (and

EAR) of the loan with points equal to the APR (and EAR) of the loan without points, which is:

PVA = C({1 – [1/(1 + r) t]}/r)

Since this is the maximum dollar amount we would pay and the points are a percentage of the

amount borrowed, we find:

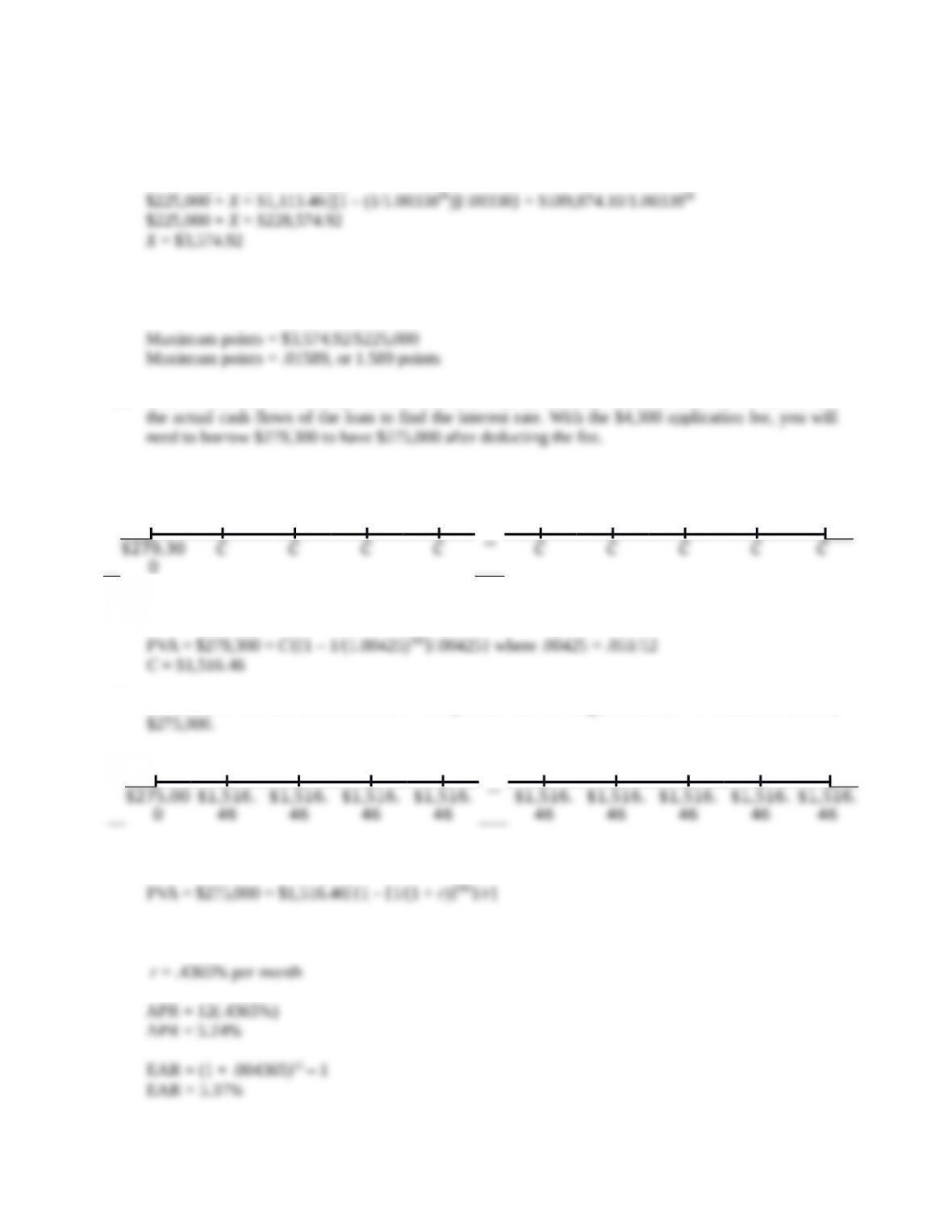

66. First we will find the APR and EAR for the loan with the refundable fee. Remember, we need to use

The time line is:

0 1

…

360

0

Solving for the payment under these circumstances, we get:

We can now use this amount in the PVA equation with the original amount we wished to borrow,

0 1

…

360

Solving for r, we find:

Solving for r with a spreadsheet, on a financial calculator, or by trial and error, gives:

With the nonrefundable fee, the APR of the loan is the quoted APR since the fee is not

considered part of the loan. So:

APR = 5.10%

67. The time line is:

0 1

…

36

Be careful of interest rate quotations. The actual interest rate of a loan is determined by the cash

Solving for r with a spreadsheet, on a financial calculator, or by trial and error, gives:

It’s called add-on interest because the interest amount of the loan is added to the principal amount of

the loan before the loan payments are calculated.

68. The payments are a growing annuity, so we use the equation for the present value of a growing

annuity. The payment growth rate is 2 percent and the EAR 11 percent. Since the payments are

quarterly, we need the APR, which is:

EAR = (1 + APR/m)m – 1

And the quarterly interest rate is:

So, the present value of the payments is:

When we add the payment made today, we get:

69. We will calculate the number of periods necessary to repay the balance with no fee first. We need to

use the PVA equation and solve for the number of payments.

Without fee and annual rate = 17.50%:

Solving for t, we get:

Without fee and annual rate = 8.9%:

Solving for t, we get:

So, you will pay off your new card:

Note that we do not need to calculate the time necessary to repay your current credit card with a fee

With fee and annual rate = 8.9%:

Solving for t, we get:

1/1.007417t = 1 – ($15,300/$250)(.007417)

So, you will pay off your new card:

70. We need to find the FV of the premiums to compare with the cash payment promised at age 65. We

have to find the value of the premiums at Year 6 first since the interest rate changes at that time. So:

FV1 = $700(1.10)5 = $1,127.36

FV2 = $700(1.10)4 = $1,024.87

Finding the FV of this lump sum at the child’s 65th birthday:

The policy is not worth buying; the future value of the deposits is $328,996.36, but the policy

Note, we could also compare the PV of the two cash flows. The PV of the premiums is:

And the value today of the $300,000 at age 65 is:

The premiums still have the higher cash flow. At time zero, the difference is $302.23. Whenever you

Here is a question for you: Suppose you invest $302.23, the difference in the cash flows at time zero,

71. The monthly payments with a balloon payment loan are calculated assuming a longer amortization

schedule, in this case, 30 years. The payments based on a 30-year repayment schedule would be:

Now, at Time 8, we need to find the PV of the payments which have not been made. The balloon

payment will be:

72. Here we need to find the interest rate that makes the PVA, the college costs, equal to the FVA, the

savings. The PVA of the college costs are:

And the FV of the savings is:

Setting these two equations equal to each other, we get:

Reducing the equation gives us:

Now we need to find the roots of this equation. We can solve using trial and error, a root-solving

calculator routine, or a spreadsheet. Using a spreadsheet, we find:

73. Here we need to find the interest rate that makes us indifferent between an annuity and a perpetuity.

And the PV of the annuity is:

Setting these two equations equal and solving for r, we get:

$35,000/r = $47,000[{1 – [1/(1 + r)15]}/r ]