Archives

978-1337269964 Chapter 1 Lecture Notes

Chapter 1 Multinational Financial Management: An Overview Lecture Outline Managing the MNC How Business Disciplines Are Used to Manage the MNC Agency Problems Management Structure of an MNC Why Firms Pursue International Business Theory of Comparative Advantage Imperfect Markets Theory […]

978-1337269964 Chapter 1 Solution Manual Part 1

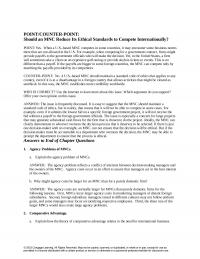

POINT/COUNTER-POINT: Should an MNC Reduce Its Ethical Standards to Compete Internationally? POINT: Yes. When a U.S.-based MNC competes in some countries, it may encounter some business norms there that are not allowed in the U.S. For example, when competing for […]

978-1337269964 Chapter 1 Solution Manual Part 2

23. Valuation of an MNC. Yahoo! has expanded its business by establishing portals in numerous countries, including Argentina, Australia, China, Germany, Ireland, Japan, and the U.K. It has cash outflows associated with the creation and administration of each portal. It […]

978-1337269964 Chapter 10 Lecture Notes

Chapter 10 Measuring Exposure to Exchange Rate Fluctuations Lecture Outline Relevance of Exchange Rate Risk Transaction Exposure Estimating “Net” Cash Flows in Each Currency Transaction Exposure of an MNC’s Portfolio Transaction Exposure Based on Vale-at-Risk Economic Exposure Economic Exposure to […]

978-1337269964 Chapter 10 Solution Manual Part 1

POINT/COUNTER-POINT: Should Investors Care about an MNC’s Translation Exposure? POINT: No. The present value of an MNC’s cash flows is based on the cash flows that the parent receives. Any impact of the exchange rates on the financial statements is […]

978-1337269964 Chapter 11 Lecture Notes

Chapter 11 managing Transaction Exposure Lecture Outline Policies for Hedging Transaction Exposure Hedging Most of the Exposure Selective Hedging Hedging Exposure to Payables Forward or Futures Hedge on Payables Money Market Hedge on Payables Call Option Hedge on Payables Comparison […]

978-1337269964 Chapter 11 Solution Manual Part 1

POINT/COUNTER-POINT: Should an MNC Risk Overhedging? POINT: Yes. MNCs have some “unanticipated” transactions that occur without any advance notice. They should attempt to forecast the net cash flows in each currency due to unanticipated transactions based on the previous net […]

978-1337269964 Chapter 11 Solution Manual Part 2

29. The Long-term Hedge Dilemma. St. Louis Inc., which relies on exporting, denominates its exports in pesos and receives pesos every month. It expects the peso to weaken over time. St. Louis recognizes the limitation of monthly hedging. It also […]

978-1337269964 Chapter 11 Solution Manual Part 3

Your firm in the U.S. expects to need 1 million pounds in one year to pay for imports. You can use any one of the following strategies to deal with the exchange rate risk: a. unhedged strategy b. money market […]

978-1337269964 Chapter 11 Solution Manual Part 4

Strategy (2) – It can establish a hedge TODAY for ALL future receivables (a one-year forward hedge for receivables in one year, a two-year forward hedge for receivables in two years, and so on). a. Assume that the euro depreciates […]

978-1337269964 Chapter 12 Lecture Notes

Chapter 12 Managing Economic Exposure and Translation Exposure Lecture Outline Managing Economic Exposure Assessing Economic Exposure Restructuring to Reduce Economic Exposure Limitations of Restructuring Intended to Reduce Economic Exposure A Case Study on Hedging Economic Exposure Savor Co.’s Assessment of […]

978-1337269964 Chapter 12 Solution Manual Part 1

POINT/COUNTER-POINT: Can an MNC Reduce the Impact of Translation Exposure by Communicating? POINT: Yes. Investors commonly use earnings to derive an MNC’s expected future cash flows. Investors do not necessarily recognize how an MNC’s translation exposure could distort their estimates […]

978-1337269964 Chapter 12 Solution Manual Part 2

Solution to Supplemental Case: Madison Co. a. While economic exposure adversely affected the firm’s performance in a recent period, it should favorably affect the firm’s performance in the future. A weak Canadian dollar (which has been forecasted) would favorably affect […]

978-1337269964 Chapter 13 Lecture Notes

Chapter 13 Direct Foreign Investment Lecture Outline Motives for Direct Foreign Investment (DFI) Revenue-Related Motives Cost-Related Motives Comparing Benefits of DFI Among Countries Measuring an MNC’s Benefits of DFI Benefits of International Diversification Diversification Analysis of International Projects Diversification Among […]

978-1337269964 Chapter 13 Solution Manual

POINT/COUNTER-POINT: Should MNCs Avoid DFI in Countries without Child Labor Laws? POINT: Yes. An MNC should maintain its hiring standards, regardless of what country it is in. Even if a foreign country allows children to work, an MNC should not […]

978-1337269964 Chapter 14 Lecture Notes

Chapter 14 Multinational Capital Budgeting Lecture Outline Subsidiary versus Parent Perspective Tax Differentials Restrictions on Remitted Earnings Exchange Rate Movements Summary of Factors That Distinguish the Parent Perspective Input for Multinational Capital Budgeting Multinational Capital Budgeting Example Background Analysis Other […]

978-1337269964 Chapter 14 Solution Manual Part 1

POINT/COUNTER-POINT Should MNCs Use Forward Rates to Estimate Dollar Cash Flows of Foreign Projects? POINT: Yes. An MNC’s parent should use the forward rate for each year in which it will receive net cash flows in a foreign currency. The […]

978-1337269964 Chapter 14 Solution Manual Part 2

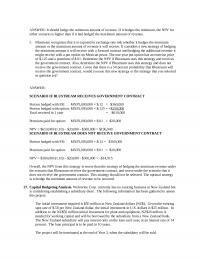

ANSWER: It should hedge the minimum amount of revenue. If it hedges the minimum, the NPV for either scenario is higher than if it had hedged the maximum amount of revenue. f. Blustream recognizes that it is exposed to exchange […]

978-1337269964 Chapter 14 Solution Manual Part 3

Multinational Capital Budgeting 1 ANSWER: (See spreadsheet attached.) The spreadsheet shows that an annual depreciation of 5 percent of the Thai baht will result in a positive NPV of $5,620,315. Since this is a worst case scenario, Blades should […]

978-1337269964 Chapter 15 Lecture Notes

Chapter 15 International Corporate Governance and Control Lecture Outline International Corporate Governance Governance by Board Members Governance by Institutional Investors Governance by Shareholder Activists International Corporate Control Motives for International Acquisitions Trends in International Acquisitions Barriers to International Corporate Control […]

978-1337269964 Chapter 15 Solution Manual Part 1

International Corporate Governance and Control 1 POINT/COUNTER-POINT: Can a Foreign Target Be Assessed Like Any Other Asset? POINT: Yes. The value of a foreign target to an MNC is the present value of the future cash flows to the […]

978-1337269964 Chapter 15 Solution Manual Part 2

23. Impact of Country Perspective on Target Valuation. Targ Co. of the U.S. has been targeted by 3 firms that consider acquiring it: (1) Americo (from the U.S.), Japino (of Japan), and Canzo (of Canada). These 3 firms do not […]

978-1337269964 Chapter 16 Lecture Notes

Chapter 16 Country Risk Analysis Lecture Outline Country Risk Characteristics Political Risk Characteristics Financial Risk Characterisitcs Measuring Country Risk Techniques to Assess Country Risk Deriving a Country Risk Rating Incorporating Country Risk in Capital Budgeting Adjustment of the Discount Rate […]

978-1337269964 Chapter 16 Solution Manual Part 1

Topics to Stimulate Class Discussion 1. How would you rate the country risk of the U.S.? Would your rating change if you lived in a foreign country? Why? 2. Some people say that you cannot separate the political and financial […]

978-1337269964 Chapter 16 Solution Manual Part 2

20. How Country Risk Affects NPV. In the previous question, assume that instead of adjusting the estimated cash flows of the project, Monk had decided to adjust the discount rate from 12 percent to 17 percent. Reevaluate the NPV of […]

978-1337269964 Chapter 17 Lecture Notes

Chapter 17 Multinational Cost of Capital and Capital Structure Lecture Outline Components of Capital Retained Earnings Sources of Debt External Sources of Equity The MNC’s Capital Structure Decision Influence of Corporate Characteristics Influence of Host Country Characteristics Response to Changing […]

978-1337269964 Chapter 17 Solution Manual Part 1

POINT/COUNTER-POINT: Should the Reduced Tax Rate on Dividends Affect an MNC’s Capital Structure? POINT: No. The change in the tax law reduces the taxes that investors pay on dividends. It does not change the taxes paid by the MNC. Thus, […]

978-1337269964 Chapter 17 Solution Manual Part 2

23. Financing with Foreign Equity. Orlando Co. has its U.S. business funded in dollars with a capital structure of 60% debt and 40% equity. It has its Thailand business funded in Thai baht with a capital structure of 50% debt […]

978-1337269964 Chapter 18 Lecture Notes

Chapter 18 Long-Term Debt Financing Lecture Outline Debt Denomination Decision of Foreign Subsidiaries Foreign Subsidiary Borrows Its Local Currency Foreign Subsidiary Borrows Dollars Debt Denomination Analysis: A Case Study Identifying Debt Denomination Alternatives Analyzing Debt Denomination Alternatives Estimating the Cost […]

978-1337269964 Chapter 18 Solution Manual Part 1

Topics to Stimulate Class Discussion 1. Why would U.S. firms consider issuing bonds denominated in a foreign currency? 2. What are the desirable characteristics related to a currency’s interest rate (high or low) and value (strong or weak) that would […]

978-1337269964 Chapter 18 Solution Manual Part 2

Solution to Continuing Case Problem: Blades, Inc. 1. Given that Blades expects to use the cash flows generated by the Thai subsidiary to pay the interest and principal of the notes, would the effective financing cost of the baht-denominated notes […]

978-1337269964 Chapter 19 Lecture Notes

Chapter 19 Financing International Trade Lecture Outline Payment Methods for International Trade Prepayment Letters of Credit Drafts Consignment Open Account Impact of the Credit Crisis on Payment Methods Trade Finance Methods Accounts Receivable Financing Factoring Letters of Credit Banker’s Acceptances […]

978-1337269964 Chapter 19 Solution Manual

Topics to Stimulate Class Discussion 1. Assume that you receive a call from an old friend who has set up a computer parts store. He says that he plans to begin exporting these parts soon. What potential complications should he […]

978-1337269964 Chapter 2 Lecture Notes

Chapter 2 International Flow of Funds Lecture Outline Balance of Payments Current Account Financial Account Capital Account Growth in International Trade Events That Increased Trade Volume Impact of Outsourcing on Trade Trade Volume Among Countries Trend in U.S.Balance of Trade […]

978-1337269964 Chapter 2 Solution Manual

POINT/COUNTER-POINT: Should Trade Restrictions be Used to Influence Human Rights Issues? POINT: Yes. Some countries do not protect human rights in the same manner as the U.S. At times, the U.S. should threaten to restrict U.S. imports from or investment […]

978-1337269964 Chapter 20 Lecture Notes

Chapter 20 Short-Term Financing Lecture Outline Sources of Foreign Financing Internal Short-term Financing External Short-term Financing Access to Funding During a Credit Crisis Financing with a Foreign Currency Motivation for Financing with a Foreign Currency Potential Cost Savings from Financing […]

978-1337269964 Chapter 20 Solution Manual

Topics to Stimulate Class Discussion 1. If a firm consistently exports to a country with low interest rates and needs to consistently borrow funds, explain how it could coordinate its invoicing and financing to reduce its financing costs. 2. What […]

978-1337269964 Chapter 21 Lecture Notes

Chapter 21 International Cash Management Lecture Outline Multinational Working Capital Management Subsidiary Expenses Subsidiary Revenue Subsidiary Dividend Payments Subsidiary Liquidity Management Centralized Cash Management Accommodating Cash Shortages Optimizing Cash Flows Accelerating Cash Inflows Minimizing Currency Conversion Costs Managing Blocked Funds […]

978-1337269964 Chapter 21 Solution Manual Part 1

Topics to Stimulate Class Discussion 1. Should international cash management be conducted at the subsidiary level or at the centralized level? Elaborate. 2. What is the use of netting to an MNC? 3. How can a firm deal with blocked […]

978-1337269964 Chapter 21 Solution Manual Part 2

Currency Spot Exchange Rate Forecasted Annual Percentage Change in Exchange Rates Australian dollar $.70 –4% Canadian dollar .80 –2 New Zealand dollar .60 +3 Japanese yen .008 0 1. Determine the investment portfolio composition for Kent’s eastern branch that would […]

978-1337269964 Chapter 21 Solution Manual Part 3

ANSWER: a. You should be concerned about your exposure, because you can not assume that the inflation rate c. The demand for your business would likely be affected if you shift the invoice policy. If the peso weakens, your clients […]

978-1337269964 Chapter 3 Lecture Notes

Chapter 3 International Financial Markets Lecture Outline Foreign Exchange Market History of Foreign Exchange Foreign Exchange Transactions Foreign Exchange Quotations Interpreting Foreign Exchange Quotations Currency Derivatives International Money Market European and Asian Markets Money Market Interest Rates Among Currencies Risk […]

978-1337269964 Chapter 3 Solution Manual

POINT/COUNTER-POINT: Should Firms That Go Public Engage in International Offerings? POINT: Yes. When a U.S. firm issues stock to the public for the first time in an initial public offering (IPO), it is naturally concerned about whether it can place […]

978-1337269964 Chapter 4 Lecture Notes

Chapter 4 Exchange Rate Determination Lecture Outline Measuring Exchange Rate Movements Exchange Rate Equilibrium Demand for a Currency Supply of a Currency for Sale Equilibrium Exchange Rate Change in the Equilibrium Exchange Rate Factors that Influence Exchange Rates Relative Inflation […]

978-1337269964 Chapter 4 Solution Manual Part 1

POINT/COUNTER-POINT: How Can Persistently Weak Currencies Be Stabilized? POINT: The currencies of some Latin American countries depreciate against the U.S. dollar on a consistent basis. The governments of these countries need to attract more capital flows by raising interest rates […]

978-1337269964 Chapter 4 Solution Manual Part 2

22. Relative Importance of Factors Affecting Exchange Rate Risk. Assume that the level of capital flows between the U.S. and the country of Krendo is negligible (close to zero) and will continue to be negligible. There is a substantial amount […]

978-1337269964 Chapter 5 Lecture Notes

Chapter 5 Currency Derivatives Lecture Outline Forward Market How MNCs Use Forward Contracts Bank Quotations on Forward Rates Premium or Discount on Forward Rate Offsetting a Forward Contract Using Forward Contracts for Swap Transactions Non-Deliverable Forward Contracts Currency Futures Market […]

978-1337269964 Chapter 5 Solution Manual Part 1

POINT/COUNTER-POINT: Should Speculators Use Currency Futures or Options? POINT: Speculators should use currency futures because they can avoid a substantial premium. To the extent that they are willing to speculate, they must have confidence in their expectations. If they have […]

978-1337269964 Chapter 5 Solution Manual Part 2

27. Currency Straddles. Reska, Inc., has constructed a long euro straddle. A call option on euros with an exercise price of $1.10 has a premium of $.025 per unit. A euro put option has a premium of $.017 per unit. […]

978-1337269964 Chapter 5 Solution Manual Part 3

37. Bullspreads and Bearspreads. Two British pound (₤) put options are available with exercise prices of $1.60 and $1.62. The premiums associated with these options are $.03 and $.04 per unit, respectively. (See Appendix B in this chapter.) a. Describe […]

978-1337269964 Chapter 6 Lecture Notes

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange Rate System Dollarization Black Market for Currencies A Single European Currency Impact […]

978-1337269964 Chapter 6 Solution Manual Part 1

POINT/COUNTER-POINT: Should China Be Forced to Alter the Value of Its Currency? POINT: U.S. politicians frequently suggest that China needs to increase the value of the Chinese yuan against the U.S. dollar, even since China has allowed the yuan to […]

978-1337269964 Chapter 6 Solution Manual Part 2

27. Intervention and Pegged Exchange Rates. Interest rate parity exists and will continue to exist. The one-year interest rate in the U.S. and in the eurozone is 6% and will continue to be 6%. Assume that the country of Latvia’s […]

978-1337269964 Chapter 7 Lecture Notes

Chapter 7 International Arbitrage and Interest Rate Parity Lecture Outline Locattional Arbitrage Gains from Locational Arbitrage Realignment Due to Locational Arbitrage Covered Interest Arbitrage Comparison of Arbitrage Effects Triangular Arbitrage Gains from Triangular Arbitrage Realignment due to Triangular Arbitrage Covered […]

978-1337269964 Chapter 7 Solution Manual Part 1

POINT/COUNTER-POINT: Does Arbitrage Destabilize Foreign Exchange Markets? POINT: Yes. Large financial institutions have the technology to recognize when one participant in the foreign exchange market is trying to sell a currency for a higher price than another participant. They also […]

978-1337269964 Chapter 7 Solution Manual Part 2

35. Impact of Arbitrage on the Forward Rate. Assume that the annual U.S. interest rate is currently 6 percent and Germany’s annual interest rate is currently 8 percent. The spot rate of the euro is $1.10 and the one-year forward […]

978-1337269964 Chapter 8 Lecture Notes

Chapter 8 Relationships Among Inflation, Interest Rates, and Exchange Rates Lecture Outline Purchasing Power Parity (PPP) Interpretations of PPP Rationale Behind PPP Theory Derivation of PPP Using PPP to Estimate Exchange Rate Effects Graphic Analysis of PPP Testing the PPP […]

978-1337269964 Chapter 8 Solution Manual Part 1

POINT/COUNTER-POINT: Does PPP Eliminate Concerns about Long-Term Exchange Rate Risk? POINT: Yes. Studies have shown that exchange rate movements are related to inflation differentials in the long run. Based on PPP, the currency of a high-inflation country will depreciate against […]

978-1337269964 Chapter 8 Solution Manual Part 2

. 33. IRP Versus IFE. You believe that interest rate parity and the international Fisher effect hold. Assume the U.S. interest rate is presently much higher than the New Zealand interest rate. You have receivables of 1 million New Zealand […]

978-1337269964 Chapter 9 Lecture Notes

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Assessment of Forecast Performance Measurement of Forecast Error Forecast Errors Among Time Horizons Forecast Errors over Time Periods […]

978-1337269964 Chapter 9 Solution Manual Part 1

POINT/COUNTER-POINT: Which Exchange Rate Forecast Technique Should MNCs Use? POINT: Use the spot rate to forecast. When a U.S.-based MNC firm conducts financial budgeting, it must estimate the values of its foreign currency cash flows that will be received by […]

978-1337269964 Chapter 9 Solution Manual Part 2

23. Forecasting Latin American Currencies. The value of each Latin American currency relative to the dollar is dictated by supply and demand conditions between that currency and the dollar. The values of Latin American currencies have generally declined substantially against […]

Chapter 1 If the home currency begins to appreciate against

Chapter 01: Multinational Financial Management: An Overview ANSWER: d DIFFICULTY: Easy LEARNING OBJECTIVES: INFM.MADU.15.01.03 NATIONAL STANDARDS: United States – BUSPROG.INFM .MADU.15.03 STATE STANDARDS: United States – OH – DISC.INFM.MADU.15.02 KEYWORDS: Bloom’s: Knowledge 44. Assume that an American firm wants to […]

Chapter 1 That Would Likely Have The

Chapter 01: Multinational Financial Management: An Overview 1. The commonly accepted goal of an MNC is to: a. maximize short-term earnings. b. maximize shareholder wealth. c. minimize risk. d. A and C. e. maximize international sales. ANSWER: b DIFFICULTY: Easy […]

Chapter 10 Belgium Majestic Co Subject Toa Economic Exposure

Chapter 10: Measuring Exposure to Exchange Rate Fluctuations ANSWER: b POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: INFM.MADU.15.10.02 NATIONAL STANDARDS: United States – BUSPROG.INFM.MADU.15.03 STATE STANDARDS: United States – OH – DISC.INFM.MADU.15.02 KEYWORDS: Bloom’s: Comprehension 41. The Canadian dollar’s volatility has […]

Chapter 10 Which firm hasa high exposure to exchange rate risk?

Chapter 10: Measuring Exposure to Exchange Rate Fluctuations 1. Translation exposure reflects: a. the exposure of a firm’s international transactions to exchange rate fluctuations. b. the exposure of a firm’s local currency value to transactions between foreign exchange traders. c. […]

Chapter 11 Hedging the position of individual subsidiaries is generally necessary

Chapter 11: Managing Transaction Exposure Copyright Cengage Learning. Powered by Cognero. Page 15 38. Since the results of both a money market hedge and a forward hedge are known beforehand, an MNC can implement the one that is more feasible. […]

Chapter 11 Purchase a currency put option in British pounds

Chapter 11: Managing Transaction Exposure 1. Assume zero transaction costs. If the 90-day forward rate of the euro is an accurate estimate of the spot rate 90 days from now, then the real cost of hedging payables will be: a. […]

Chapter 12 Which of the following is an example of economic exposure

Chapter 12: Managing Economic Exposure and Translation Exposure 1. Depreciation of the euro relative to the U.S. dollar will cause a U.S.-based MNC’s reported earnings (from the consolidated income statement) to ____. If a firm desired to protect against this […]

Chapter 13 All The Above Are Truee And Are

Chapter 13: Direct Foreign Investment 1. Which of the following purchases does not represent direct foreign investment? a. machinery to be used in manufacturing b. a tract of land c. bonds and other financial assets d. a manufacturing plant ANSWER: […]

Chapter 14 Assume the parent of a U.S.-based MNC plans to completely

Chapter 14: Multinational Capital Budgeting 1. If a U.S. parent is setting up a French subsidiary, and funds from the subsidiary will be periodically sent to the parent, the ideal situation from the parent’s perspective is a ____ after the […]

Chapter 15 Based on economic and political considerations, only one eligible

Chapter 15: International Corporate Governance and Control 1. International governance is achieved by all of the following except: a. poison pills. b. board of directors. c. institutional investors. d. blockholders. e. All of the above achieve governance. ANSWER: a POINTS: […]

Chapter 15 Which of the following would not enhance the value of a target from the acquirer’s

Chapter 15: International Corporate Governance and Control DIFFICULTY: Moderate LEARNING OBJECTIVES: INFM.MADU.15.15.06 NATIONAL STANDARDS: United States – BUSPROG.INFM.MADU.15.03 STATE STANDARDS: United States – OH – DISC.INFM.MADU.15.09 KEYWORDS: Bloom’s: Knowledge 36. When U.S. firms acquire publically-traded target firms in foreign countries, […]

Chapter 16 Hire Local Labord Borrow Local Fundse All

Chapter 16: Country Risk Analysis 1. A macro-assessment of country risk: a. is adjusted for the particular business of the firm involved. b. excludes aspects relevant to a particular firm or project. c. A and B d. none of the […]

Chapter 17 the combination of the capital structures of the parent

Chapter 17: Multinational Cost of Capital and Capital Structure 1. An argument for an MNC to have a debt-intensive capital structure is that: a. it can reduce the MNC’s exposure to exchange rate risk on earnings remitted by subsidiaries to […]

Chapter 18 Simulation is useful in the debt denomination decision since it

Chapter 18: Long-Term Debt Financing 1. If an MNC finances with a currency different from its invoice currency, it would prefer that the loan be denominated in a currency that: a. exhibits a low interest rate and is expected to […]

Chapter 19 This should cause the popularity of trade finance

Chapter 19: Financing International Trade 1. Which of the following is a reason why commercial banks may facilitate international trade? a. The exporter may not wish to accept the credit risk of the importer. b. The government may impose foreign […]

Chapter 2 Knowledge The Primary Component The Capital Account

Chapter 02: International Flow of Funds 38. The value of financial assets transferred across country borders by people who move to a different country is included in the balance of payments in the capital account. a. True b. False ANSWER: […]

Chapter 2 The World Bank was established to reduce poverty

Chapter 02: International Flow of Funds 1. Recently, the U.S. experienced an annual balance of trade representing a ____. a. large surplus (exceeding $100 billion) b. small surplus c. level of zero d. deficit ANSWER: d POINTS: 1 DIFFICULTY: Easy […]

Chapter 20 Also assume the pound’s forward rate of$1.75 equals

Chapter 20: Short-Term Financing 1. MNCs may be able to lock in a lower cost by financing in a low-interest rate foreign currency if they have: a. future cash inflows in that foreign currency. b. future cash outflows in that […]

Chapter 21 Assume that there are several foreign currencies that

Chapter 21: International Cash Management 1. The Mexican one-year interest rate is 9 percent, while the U.S. one-year interest rate is 3 percent. Assume that interest rate parity exists. If a U.S. firm uses the forward rate to forecast the […]

Chapter 3 If a U.S. firm will need C$200,000 in 90 days to

Chapter 03: International Financial Markets 1. Assume that a bank’s bid rate on Swiss francs is $.45 and its ask rate is $.47. Its bid/ask percentage spread is: a. about 4.44%. b. about 4.26%. c. about 4.03%. d. about 4.17%. […]

Chapter 3 The Loans Are Only Denominated Us Dollarsc

Chapter 03: International Financial Markets a. 48.90 b. 146.70 c. 55.21 d. none of the above ANSWER: b RATIONALE: 3 30 $1.63 = $146.70 POINTS: 1 DIFFICULTY: Moderate LEARNING OBJECTIVES: INFM.MADU.15.03.05 NATIONAL STANDARDS: United States – BUSPROG.INFM.MADU.15.03 STATE […]

Chapter 4 The change in interest rates will place

Chapter 04: Exchange Rate Determination 1. The value of the Australian dollar (A$) today is $0.73. Yesterday, the value of the Australian dollar was $0.69. The Australian dollar ____ by ____ percent a. depreciated; 5.80 b. depreciated; 4.00 c. appreciated; […]

Chapter 5 Currency futures contracts sold on an exchange contain

Chapter 05: Currency Derivatives 1. Kalons, Inc. is a U.S.-based MNC that frequently imports raw materials from Canada. Kalons is typically invoiced for these goods in Canadian dollars and is concerned that the Canadian dollar will appreciate in the near […]

Chapter 5 It negotiated a 3-month forward contract to obtain 100 million

Chapter 05: Currency Derivatives of this option expiration is expected to be $1.51. Speculators could profit by: a. writing a put option. b. buying a put option. c. buying a call option d. writing a call option and buying a […]

Chapter 5 Your company expects to receive 5,000,000 Japanese

Chapter 05: Currency Derivatives b. The currency options offered by commercial banks are more liquid and have a smaller bid/ask spread than the options traded on an exchange. c. When transaction costs are controlled for, the currency options market is […]

Chapter 6 the establishment of the European Monetary System

Chapter 06: Government Influence on Exchange Rates 1. To force the value of the pound to appreciate against the dollar, the Federal Reserve should: a. sell dollars for pounds in the foreign exchange market and the European Central Bank (ECB) […]

Chapter 6 The European Central Bank is responsible for

Chapter 06: Government Influence on Exchange Rates KEYWORDS: Bloom’s: Knowledge 59. The Smithsonian Agreement was an agreement to allow currencies of major countries to float without any barriers. a. True b. False ANSWER: b POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: […]

Chapter 7 Triangular arbitrage tends to force a relationship

Chapter 07: International Arbitrage and Interest Rate Parity Copyright Cengage Learning. Powered by Cognero. Page 16 43. Refer to Exhibit 7-1 above. If you conduct covered interest arbitrage, what is your percentage return after 180 days? Is covered interest arbitrage […]

Chapter 7 Us Dollars Should Appreciate The Pound Value

Chapter 07: International Arbitrage and Interest Rate Parity 1. Due to ____, market forces should realign the relationship between the interest rate differential of two currencies and the forward premium (or discount) on the forward exchange rate between the two […]

Chapter 8 Because there are a variety of factors in addition to inflation that

Chapter 08: Relationships among Inflation, Interest Rates, and Exchange Rates 1. Assume a two-country world: Country A and Country B. Which of the following is correct about purchasing power parity (PPP) as related to these two countries? a. If Country […]

Chapter 9 Assume That Inft Percent However The interest

Chapter 09: Forecasting Exchange Rates 1. Which of the following forecasting techniques would be most likely to use today’s forward exchange rate to forecast the future exchange rate? a. fundamental forecasting b. market-based forecasting c. technical forecasting d. interval forecasting […]

Chapter 9 Canadian Dollars Forward And Put Pressure

Chapter 09: Forecasting Exchange Rates the same amount as the forward premium or discount, respectively. a. True b. False ANSWER: a POINTS: 1 DIFFICULTY: Easy LEARNING OBJECTIVES: INFM.MADU.15.09.02 NATIONAL STANDARDS: United States – BUSPROG.INFM.MADU.15.03 STATE STANDARDS: United States – OH […]