29. The Long-term Hedge Dilemma. St. Louis Inc., which relies on exporting, denominates its exports in

pesos and receives pesos every month. It expects the peso to weaken over time. St. Louis recognizes the

limitation of monthly hedging. It also recognizes that it could remove its transaction exposure by

denominating the exports in dollars but that it is still would be subject to economic exposure. The long-

term hedging techniques are limited and the firm does not know how many pesos it will receive in the

future, so it would have difficulty even if a long-term hedging method was available. How can this

business realistically deal with this dilemma to reduce its exposure over the long-term?

30. Long-term Hedging. Since Obisbo Inc. conducts much business in Japan, it is likely to have cash

flows in yen that will periodically be remitted by its Japanese subsidiary to the U.S. parent. What are

the limitations of hedging these remittances one year in advance over each of the next 20 years?

What are the limitations of creating a hedge today that will hedge these remittances over each of the

next 20 years?

31. Hedging during a Crisis. Describe how a crisis in Asia could reduce the cash flows of a U.S. firm

that exports products (denominated in U.S. dollars) to Asian countries. How could a U.S. firm that

exports products (denominated in U.S. dollars) to Asia insulate itself from any currency effects of a

future crisis while continuing to export to Asia?

Advanced Questions

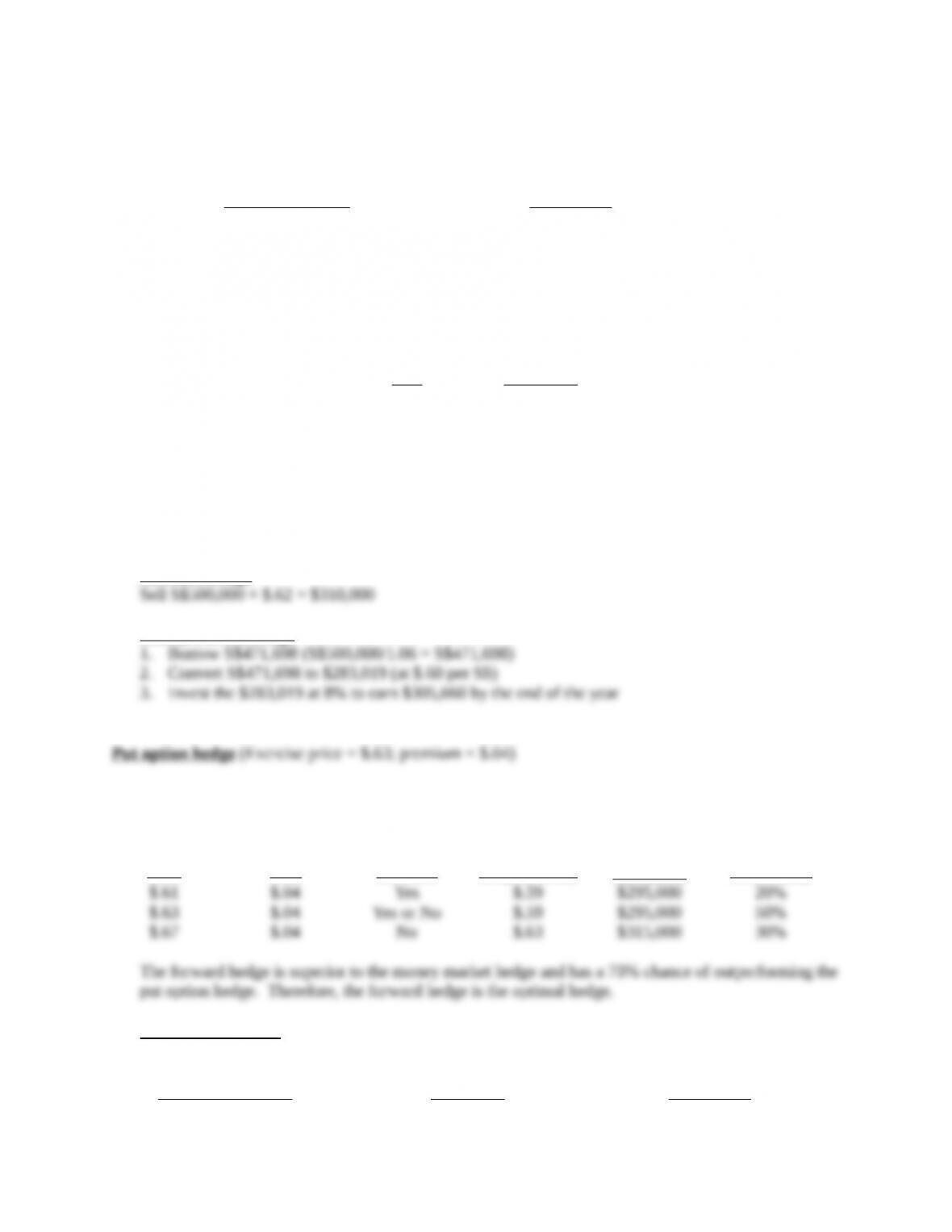

32. Comparison of Techniques for Hedging Receivables.

a. Assume that Carbondale Co. expects to receive S$500,000 in one year. The existing spot rate of

the Singapore dollar is $.60. The one-year forward rate of the Singapore dollar is $.62.

Carbondale created a probability distribution for the future spot rate in one year as follows:

Future Spot Rate Probability

$.61 20%

.63 50

.67 30

Assume that one-year put options on Singapore dollars are available, with an exercise price of

$.63 and a premium of $.04 per unit. One-year call options on Singapore dollars are available

with an exercise price of $.60 and a premium of $.03 per unit. Assume the following money

market rates:

U.S. Singapore

Deposit rate 8% 5%

Borrowing rate 9 6

Given this information, determine whether a forward hedge, money market hedge, or a currency

options hedge would be most appropriate. Then compare the most appropriate hedge to an

unhedged strategy, and decide whether Carbondale should hedge its receivables position.

ANSWER:

Forward hedge

Money market hedge

Possible Spot

Rate

Option

Premium per

Unit Exercise

Amount

Received per

Unit (also

accounting

for premium)

Total Amount

Received for

S$500,000 Probability

Unhedged Strategy

Possible Spot Rate

Total Amount Received for

S$500,000 Probability

b. Assume that Baton Rouge, Inc. expects to need S$1 million in one year. Using any relevant

information in part (a) of this question, determine whether a forward hedge, a money market

hedge, or a currency options hedge would be most appropriate. Then, compare the most

appropriate hedge to an unhedged strategy, and decide whether Baton Rouge should hedge its

payables position.

ANSWER:

Forward hedge

Money market hedge

Amount Paid Total

Option per Unit Amount

Possible Premium Exercise (including Paid for

Spot Rate per Unit Option? the premium) S$1,000,000 Probability

Unhedged Strategy

Total

Possible Amount Paid

Spot Rate for S$500,000 Probability

33. Techniques for Hedging Receivables. SMU Corp. has future receivables of 4,000,000 New Zealand

dollars (NZ$) in one year. It must decide whether to use options or a money market hedge to hedge

this position. Use any of the following information to make the decision. Verify your answer by

determining the estimate (or probability distribution) of dollar revenue to be received in one year for

each type of hedge.

Spot rate of NZ$ = $.54

One-year call option: Exercise price = $.50; premium = $.07

One-year put option: Exercise price = $.52; premium = $.03

U.S. New Zealand

One-year deposit rate 9% 6%

One-year borrowing rate 11 8

Rate Probability

Forecasted spot rate of NZ$ $.50 20%

.51 50

.53 30

ANSWER:

Put option hedge (Exercise price = $.52; premium = $.03)

Possible Spot

Rate

Put Option

Premium

Exercise

Option?

Amount per

Unit Received

Accounting

for Premium

Total Amount

Received

for

NZ$4,000,000 Probability

Money market hedge

34. Exposure to September 11.If you were a U.S. importer of products from Europe, explain whether

the September 11, 2001 terrorist attack on the U.S. would have caused you to hedge your payables

(denominated in euros) due a few months later. Keep in mind that the attack was followed by a

reduction in U.S. interest rates.

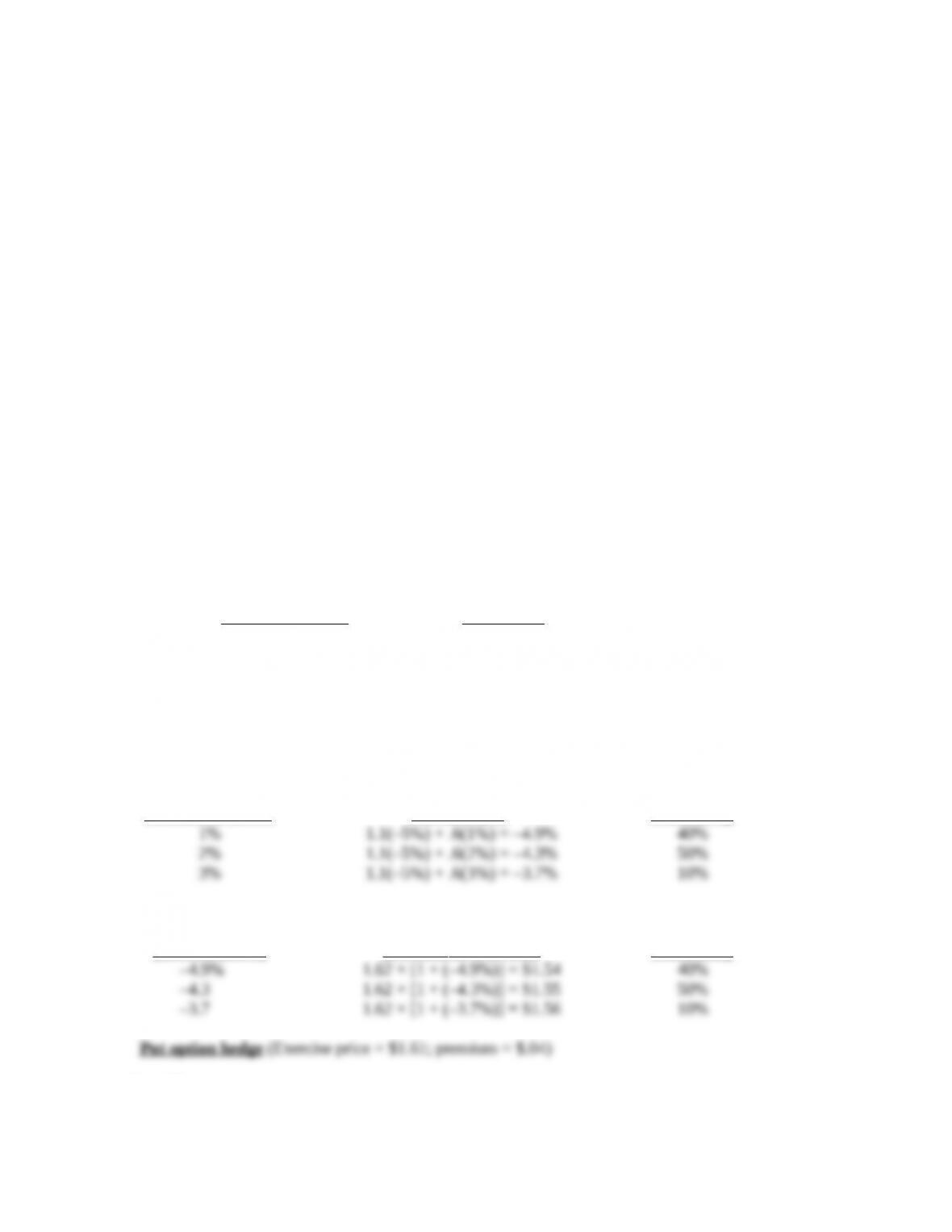

35. Hedging with Forward versus Option Contracts. As treasurer of Tempe Corp., you are confronted

with the following problem. Assume the one-year forward rate of the British pound is $1.59. You

plan to receive 1 million pounds in one year. A one-year put option is available. It has an exercise

price of $1.61. The spot rate as of today is $1.62, and the option premium is $.04 per unit. Your

forecast of the percentage change in the spot rate was determined from the following regression

model:

et = a0 + a1DINFt-1 + a2DINTt + u

where et= percentage change in British pound value over period t

DINFt-1 = differential in inflation between the United States and the United

Kingdom in period t–1

DINTt= average differential between U.S. interest rate and British

interest rate over period t

a0, a1, and a2= regression coefficients

u = error term

The regression model was applied to historical annual data, and the regression coefficients were

estimated as follows:

a0 =0.0

a1 =1.1

a2 =0.6

Assume last year’s inflation rates were 3 percent for the United States and 8 percent for the United

Kingdom. Also assume that the interest rate differential (DINTt) is forecasted as follows for this year:

Forecast of DINTtProbability

1% 40%

2 50

3 10

Using any of the available information, should the treasurer choose the forward hedge or the put

option hedge? Show your work.

ANSWER:

Forecast of DINTtForecast of et Probability

Approximate

Forecast of etForecasted Spot Rate

(derived above) of Pound in One Year Probability

Possible

Spot Rate of Amount

Pound in Received

One Year Put per Unit Total Amount

(derived Option Exercise (accounting Received for One

above) Premium Option? for premium) Million Pounds Probability

Forward hedge

36. Hedging Decision. You believe that IRP presently exists. The nominal annual interest rate in Mexico

is 14%. The nominal annual interest rate in the U.S. is 3%. You expect that annual inflation will be

about 4% in Mexico and 5% in the U.S. The spot rate of the Mexican peso is $.10. Put options on

pesos are available with a one-year expiration date, an exercise price of $.1008, and a premium of

$0.014 per unit.

You will receive 1 million pesos in one year.

a. Determine the amount of dollars that you will receive if you use a forward hedge.

ANSWER: According to IRP, the forward premium on the peso should be (1.03)/(1.14) – 1 = –.0965

c. Determine the amount of dollars that you will expect to receive if you use a currency put option

hedge. Account for the premium you would pay on the put option.

ANSWER: Since the expected spot rate is $.10096 based on PPP, you could receive $.10096 per unit

37. Forecasting with IFE and Hedging. Assume that Calumet Co. will receive 10 million pesos in

15 months. It does not have a relationship with a bank at this time, and therefore can not obtain a

forward contract to hedge its receivables at this time. However, in three months, it will be able to

obtain a one-year (12-month) forward contract to hedge its receivables. Today the three-month U.S.

interest rate is 2% (not annualized), the 12-month U.S. interest rate is 8%, the three-month Mexican

peso interest rate is 5% (not annualized), and the 12-month peso interest rate is 20%. Assume that

interest rate parity exists. Assume the international Fisher effect exists. Assume that the existing

interest rates are expected to remain constant over time. The spot rate of the Mexican peso today is

$.10. Based on this information, estimate the amount of dollars that Calumet Co. will receive in 15

months.

38. Forecasting from Regression Analysis and Hedging. You apply a regression model to annual data

in which the annual percentage change in the British pound is the dependent variable, and INF

(defined as annual U.S. inflation minus U.K. inflation) is the independent variable. Results of the

regression analysis show an estimate of 0.0 for the intercept and +1.4 for the slope coefficient. You

believe that your model will be useful to predict exchange rate movements in the future.

You expect that inflation in the U.S. will be 3%, versus 5% in the U.K. There is an 80% chance of

that scenario. However, you think that oil prices could rise, and if so, the annual U.S. inflation rate

will be 8% instead of 3% (and the annual U.K. inflation will still be 5%). There is a 20% chance that

this scenario will occur. You think that the inflation differential is the only variable that will affect the

British pound’s exchange rate over the next year.

The spot rate of the pound as of today is $1.80. The annual interest rate in the U.S. is 6% versus an annual

interest rate in the U.K. of 8%. Call options are available with an exercise price of $1.79, an expiration

date of one year from today, and a premium of $.03 per unit