Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

35. Impact of Arbitrage on the Forward Rate. Assume that the annual U.S. interest rate is currently

6 percent and Germany’s annual interest rate is currently 8 percent. The spot rate of the euro is $1.10

and the one-year forward rate of the euro is $1.10. Assume that as covered interest arbitrage occurs,

the interest rates are not affected, and the spot rate is not affected. Explain how the one-year forward

rate of the euro will change in order to restore interest rate parity, and why it will change Your

explanation should specify which type of investor (German or U.S.) would be engaging in covered

interest arbitrage, whether they are buying or selling euros forward, and how that affects the forward

rate of the euro.

36. IRP and Changes in the Forward Rate. Assume that interest rate parity exists. As of this

morning, the 1-month interest rate in Canada was lower than the 1-month interest rate in the

U.S.. Assume that as a result of the Fed’s monetary policy this afternoon, the one-month interest

rate in the U.S. declined this afternoon, but was still higher than the Canadian one-month interest

rate. The one-month interest rate in Canada remained unchanged. Based on the information, the

forward rate of the Canadian dollar exhibited a ________ [discount or premium] this morning

that _________[increased or decreased] this afternoon. Explain.

37. Deriving the Forward Rate Premium. Assume that the spot rate of the Brazilian real is $.30

today. Assume that interest rate parity exists. Obtain the interest rate data you need from

Bloomberg.com to derive the one-year forward rate premium (or discount), and then determine the one-

year forward rate of the Brazilian real.

38. Change in the Forward Premium Over Time. Assume that interest rate parity exists and

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 2

will continue to exist. As of today, the one-year interest rate of Singapore is 4% versus 7% in the

U.S. The Singapore central bank is expected to decrease interest rates in the future so that as of

December 1, you expect that the one-year interest rate in Singapore will be 2%. The U.S.

interest rate is not expected to change over time. Based on the information, explain how the

forward premium (or discount) is expected to change by December 1.

ANSWER: The forward premium will become larger. For all situations in which the foreign

interest is less than the US, the forward rate should exhibit a premium that is the same as the

difference in interest rates. The differential is expected to increase over time, so the premium will

become larger.

39. Forward Rates for Different Time Horizons. Assume that interest rate parity (IRP) exists, along with

the followinginformation:

Spot rate of British pound = $1.80

6-month forward rate of pound=$1.82

12-month forward rate of pound=$1.78

a. Is the annualized 6-month U.S. risk-free interest rate above, below, or equal to the British risk-free

interest rate?

b. Is the 12-month U.S. risk-free interest rate above, below, or equal to the British risk-free interest

rate?

ANSWER:

40. Interpreting Forward Rate Information. Assume that interest rate parity exists. The 6-month

forward rate of the Swiss franc has a premium while the 12-month forward rate of the Swiss franc has

a discount. What does this tell you about the relative level of Swiss interest rates versus U.S. interest

rates?

41. IRP and Speculation in Currency Futures. Assume that interest rate parity exists. The spot rate

of the Argentine peso is $.40. The one-year interest rate in the U.S. is 7% versus 12% in Argentina.

Assume the futures price is equal to the forward rate. An investor purchased futures contracts on

Argentine pesos, representing a total of 1,000,000 pesos. Determine the total dollar amount of profit or

loss from this futures contract based on the expectation that the Argentine peso will be worth $.42 in

one year.

ANSWER:

42. Profit from Covered Interest Arbitrage. Today, the one-year U.S. interest rate is 4%,

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 3

while the one-year interest rate in Argentina is 17%. The spot rate of the Argentine peso (AP) is

$.44. The one-year forward rate of the AP exhibits a 14% discount. Determine the yield

(percentage retrun on investment) to an investor from Argentina who engages in covered interest

arbitrage.

ANSWER:

43. Assessing Whether IRP Exists. Assume zero transactions costs. As of now, the Japanese one-year

interest rate is 3 percent, and the U.S. one-year interest rate is 9 percent. The spot rate of the Japanese

yen is $.0090 and the one-year forward rate of the Japanese yen is $.0097.

a. Determine whether interest rate parity exists, or whether the quoted forward rate is quoted too high

or too low.

b. Based on the information provided in (a), is covered interest arbitrage feasible for U.S. investors,

for Japanese investors, for both types of investors, or for neither type of investor?

ANSWER:

44. Change in Forward Rate Due to Arbitrage. Earlier this morning, the annual U.S. interest rate

was 6 percent and Mexico’s annual interest rate was 8 percent. The spot rate of the Mexican peso was

$.16. The one-year forward rate of the peso was $.15. Assume that as covered interest arbitrage

occurred this morning, the interest rates were not affected, and the spot rate was not affected, but the

forward rate was affected, and consequently interest rate parity now exists. Explain which type of

investor (Mexican or U.S.) engaged in covered interest arbitrage, whether they were buying or selling

pesos forward, and how that affected the forward rate of the peso.

ANSWER:

45. IRP Relationship. Assume that interest rate parity (IRP) exists, along with the following information:

Spot rate of Swiss franc = $.80

6-month forward rate of Swiss franc = $.78

12-month forward rate of Swiss franc = $.81

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 4

Assume that the annualized U.S. interest rate is 7% for a six-month maturity and a 12-month maturity.

Do you think the Swiss interest rate for a 6-month maturity is greater than, equal to, or less than the

U.S. interest rate for a 6-month maturity? Explain.

46. Impact of Arbitrage on Forward Rate. Assume that the annual U.S. interest rate is currently

8 percent and Japan’s annual interest rate is currently 7 percent. The spot rate of the Japanese yen is

$.01. The one-year forward rate of the Japanese yen is $.01. Assume that as covered interest arbitrage

occurs, the interest rates are not affected, and the spot rate is not affected. Explain how the one-year

forward rate of the yen will change in order to restore interest rate parity, and why it will change [your

explanation should specify which type of investor (Japanese or U.S.) would be engaging in covered

interest arbitrage and whether these investors are buying or selling yen forward, and how that affects

the forward rate of the yen.]

ANSWER: Japanese investors will be able to engage in covered interest rate arbitrage and take

47. Profit from Triangular Arbitrage. The bank is willing to buy dollars for 0.9 euros per dollar.

It is willing to sell dollars for .91 euros per dollar.

You can sell Australian dollars (A$) to the bank for $.72.

You can buy Australian dollars from the bank for $.74.

The bank is willing to buy Australian dollars (A$) for 0.68 euros per A$.

The bank is willing to sell Australian dollars (A$) for 0.70 euros per A$.

You have $100,000. Estimate your profit or loss if you were to attempt triangular arbitrage by

converting your dollars to Australian dollars, and then convertubg Australian dollars to euros, and then

converting euros to U.S. dollars.

ANSWER:

48. Profit from Triangular Arbitrage. Alabama Bank is willing to buy or sell British pounds for $1.98.

The bank is willing to buy or sell Mexican pesos at an exchange rate of 10 pesos per dollar. The bank

is willing to purchase British pounds at an exchange rate of 1 peso = .05 British pounds. Show how

you can make a profit from triangular arbitrage and what your profit would be if you had $100,000.

ANSWER:

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 5

49. Cross-rate and Forward Rate. Biscayne Co. will be receiving Mexican pesos and today and will need

to convert them into Australian dollars. Today, a U.S. dollar can be exchanged for 10 Mexican pesos.

Also, an Australian dollar is worth one-half of a U.S. dollar.

a. What is the spot rate of a Mexican peso in Australian dollars?

b. Assume that interest rate parity exists and that the annual risk-free interest rate in the U.S.,

Australia, and Mexico is 7 percent. What is the one-year forward rate of a Mexican peso in

Australian dollars?

ANSWER:

50. Changes in the Forward Rate. Assume that interest rate parity exists and will continue to exist. As of

this morning, the 1-month interest rate in the U.S. was higer than the 1-month interest rate in the

eurozone. Assume that as a result of the European Central Bank’s monetary policy this afternoon, the

one-month interest rate of the euro increased, and is now higher than the U.S. one-month interest rate.

The one-month interest rate in the U.S. remained unchanged.

a. Based on the information, do you think the one-month forward rate of the euro exhibited a discount

or premium this morning?

b. How did the forward premium change this afternoon?

ANSWER:

51. Forces of Triangular Arbitrage. You obtain the following quotes from different banks. One bank is

willing to buy or sell Japanese yen at an exchange rate of 110 yen per dollar. A second bank is willing

to buy or sell the Argentine peso at an exchange rate of $.37 per peso. A third bank is willing to

exchange Japanese yen at an exchange rate of 1 Argentine peso = 40 yen.

a. Show how you can make a profit from triangular arbitrage and what your profit would be if you

had $1,000,000.

b. As investors engage in triangular arbitrage, explain the effect on each of the exchange rates until

triangular arbitrage would no longer be possible.

ANSWER:

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 6

52. Return Due to Covered Interest Arbitrage. Interest rate parity exists between the U.S. and Poland

(its currency is the zloty). The one-year risk-free CD (deposit) rate in the U.S. is 7%. The one-year

risk-free CD rate in Poland is 5% and denominated in zloty. Assume that there is zero probability of

any financial or political problem in either country such as a bank default or government restrictions on

bank deposits or currencies. Myron is from Poland and plans to invest in the U.S. What is Myron’s

return if he invests in the U.S. and covers the risk of his investment with a forward contract?

53. Forces of Covered Interest Arbitrage. As of now, the nominal interest rate is 6% in the U.S. and 6%

in Australia. The spot rate of the Australian dollar is $.58, while the one-year forward rate of the

Australian dollar exhibits a discount of 2%. Assume that as covered interest arbitrage occurred this

morning, the interest rates were not affected, and the spot rate of the Australian dollar was not affected,

but the forward rate of the Australian dollar was affected, and consequently interest rate parity now

exists. Explain the forces that caused the forward rate of the Australian dollar to change by completing

this sentence: The ___________ [Australian or U.S.?] investors could benefit from engaging in covered

interest arbitrage; their arbitrage would involve ___________ [buying or selling?] Australia dollars

forward, which would cause the forward rate of the Australian dollar to ____________ [increase or

decrease?].]

54. Change in Forward Premium Over Time. Assume that the one-year interest rate in the U.K.. is 9

percent, while the one-year interest in the U.S is 4%. The spot rate of the pound is $1.50. Assume that

interest rate parity exists. The quoted one-year interest in the U.K. is expected to rise consistently over

the next month. Meanwhile, the quoted one-year interest rate in the U.S. is expected to decline

consistently over the next month. Assume that the spot rate does not change over the month. Based on

this information, how will the quoted one-year forward rate change over the next month?

55. Forward Rate Premiums Among Maturities. Today, the annualized interest rate in the U.S. is 4% for any

debt maturity. The annualized interest rate in Australia is 4% for debt maturities of 3 months or less, is 5% for

debt maturities between 3 months and 6 months, and is 6% for debt maturities more than 6 months. Assume

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 7

that interest rate parity exists. Does the forward rate quoted today for the Australian dollar exhibit a premium,

or a discount, or does your answer vary with specific conditions? Briefly explain.

56. Explaining Movements in Forward Premiums. Assume that interest rate parity holds and will

continue to hold in the future. At the beginning of the month, the spot rate of the British pound is $1.60,

while the one-year forward rate is $1.50. Assume that U.S. annual interest rate remains steady over the

month. At the end of the month, the one-year forward rate of the British pound exhibits a discount of 1

percent. Explain how the British annual interest rate changed over the month, and whether it is higher,

lower, or equal to the U.S. rate at the end of the month.

57. Forces of Covered Interest Arbitrage. Assume that the one-year interest rate in Canada is 4 percent.

The one-year U.S. interest rate is 8 percent. The spot rate of the Canadian dollar (C$) is $.94. The

forward rate of the Canadian dollar is $.98.

a. Is covered interest arbitrage feasible for U.S. investors? Show the results if a U.S. firm engages in

covered interest arbitrage to support your answer.

b. Assume that the spot rate and interest rates remain unchanged as coverage interest arbitrage is

attempted by U.S. investors. Do you think the forward rate of the Canadian dollar will be affected?

If so, state whether it will increase or decrease, and explain why.

ANSWER:

CRITICAL THINKING

IRP Implications Since the International Credit Crisis During the period from 2008 (when the

international credit crisis occurred) and 2014, the U.S. government maintained interest rates at extremely

low levels. Assume that interest rate parity existed over that time period. Write a short essay on what the

interest rate conditions in the U.S. imply about the forward rate of the Australian dollars over this period.

ANSWER

Given that interest rate parity exists, and that U.S. interest rates are lower than the Australian interest rates,

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 8

Solution to Continuing Case Problem: Blades, Inc.

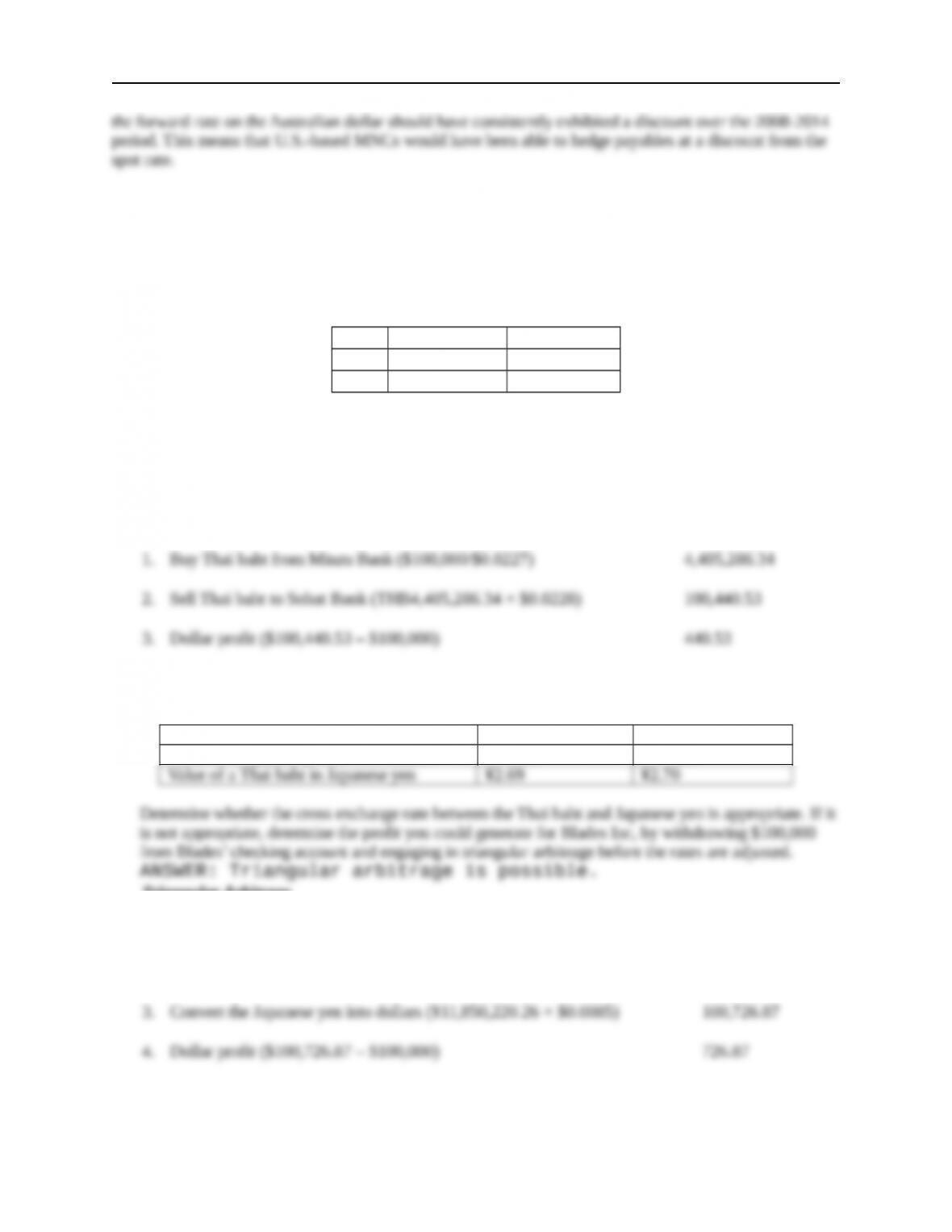

1. The first arbitrage opportunity relates to locational arbitrage. Holt has obtained spot rate quotations

from two banks in Thailand, Minzu Bank and Sobat Bank, both located in Bangkok. The bid and ask

prices of Thai baht for each bank are displayed in the table below:

Minzu Bank Sobat Bank

Bid $0.0224 $0.0228

Ask $0.0227 $0.0229

Determine whether the foreign exchange quotations are appropriate. If they are not appropriate,

determine the profit you could generate by withdrawing $100,000 from Blades’ checking account and

engaging in arbitrage before the rates are adjusted.

ANSWER: Locational arbitrage is possible:

Locational Arbitrage

2. Besides the bid and ask quotes for the Thai baht provided in the previous question, Minzu Bank has

provided the following quotations for the U.S. dollar and the Japanese yen:

Quoted Bid Price Quoted Ask Price

Value of a Japanese yen in U.S. dollars $0.0085 $0.0086

Triangular Arbitrage

1. Exchange dollars for Thai baht ($100,000/$0.0227) 4,405,286.34

2. Convert the Thai baht into Japanese yen (THB4,405,286.34 × ¥2.69) 11,850,220.25

3. Ben Holt has obtained several forward contract quotations for the Thai baht to determine whether

covered interest arbitrage may be possible. He was quoted a forward rate of $0.0225 per Thai baht for

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 9

a 90-day forward contract. The current spot rate is $0.0227. Ninety-day interest rates available to

Blades in the U.S. are 2 percent, while 90-day interest rates in Thailand are 3.75 percent (these rates

are not annualized). Holt is aware that covered interest arbitrage, unlike locational and triangular

arbitrage, requires an investment of funds. Thus, he would like to be able to estimate the dollar profit

resulting from arbitrage over and above the dollar amount available on a 90-day U.S. deposit.

Determine whether the forward rate is priced appropriately. If it is not priced appropriately, determine

the profit you could generate for Blades by withdrawing $100,000 from Blades’ checking account and

engaging in covered interest arbitrage. Measure the profit as the excess amount above what you could

generate by investing in the U.S. money market.

Covered Interest Arbitrage

4. Why are arbitrage opportunities likely to disappear soon after they have been discovered? To illustrate

your answer, assume that covered interest arbitrage involving the immediate purchase and forward sale

of baht is possible. Discuss how the baht’s spot and forward rates would adjust until covered interest

arbitrage is no longer possible. What is the resulting equilibrium state called?

ANSWER: Arbitrage opportunities are likely to disappear soon after they have been discovered

because of market forces. Due to the actions taken by arbitrageurs, supply and demand for the foreign

Solution to Supplemental Case: Crayson Co.

a. Crayson could invest its $5 million in 10 million zyn, earn 2% over the quarter, and would receive

10,200,000 at the end of the quarter. This should convert to 5,100,000 euros at the end of the quarter.

When investing at the beginning of the quarter, Crayson would simultaneously sell 5,100,000 euros

forward. Assuming that the zyn remained tied to the euro, Crayson’s forward sale would perfectly

hedge its exposure. The 5,100,000 euros convert to $5,100,000, which would result in a quarterly

return of 2%.

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Arbitrage and Interest Rate Parity 10

b. The strategy described in the previous answer could backfire if the zyn does not remain tied to the euro

over the quarter when Crayson Co. invested funds. If the zyn suddenly is devalued against the euro, the

strategy described in the previous answer would result in a lower return, and may even result in a

substantial loss.

Small Business Dilemma

Assessment of Prevailing Spot and Forward Rates by the Sports Exports Company

1. Do you think Jim will be able to find a bank that provides him with a more favorable spot rate than his

local bank? Explain.

2. Do you think that Jim’s bank is likely to provide more reasonable quotations for the spot rate of the

British pound if it is the only bank in town that provides foreign exchange services? Explain.

3. Jim is considering using a forward contract to hedge the anticipated receivables in pounds next month.

His local bank quoted him a spot rate of $1.65 and a one-month forward rate of $1.6435. Before Jim

decides to sell pounds one month forward, he wants to be sure that the forward rate is reasonable, given

the prevailing spot rate. A one-month Treasury security in the United States currently offers a yield

(not annualized) of 1 percent, while a one-month Treasury security in the United Kingdom offers a

yield of 1.4 percent. Do you believe that the one-month forward rate is reasonable given the spot rate

of $1.65?

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.