27. Currency Straddles. Reska, Inc., has constructed a long euro straddle. A call option on euros with an

exercise price of $1.10 has a premium of $.025 per unit. A euro put option has a premium of $.017 per

unit. Some possible euro values at option expiration are shown in the following table. (See Appendix

B in this chapter.)

Value of Euro at Option Expiration

$.90 $1.05 $1.50 $2.00

Call

Put

Net

a. Complete the worksheet and determine the net profit per unit to Reska Inc. for each possible

future spot rate.

b. Determine the break-even point(s) of the long straddle. What are the break-even points of a short

straddle using these options?

ANSWER:

a.

Value of Euro at Option Expiration

$.90 $1.05 $1.50 $2.00

b. The break-even points for a long straddle can be found by subtracting and adding both premiums

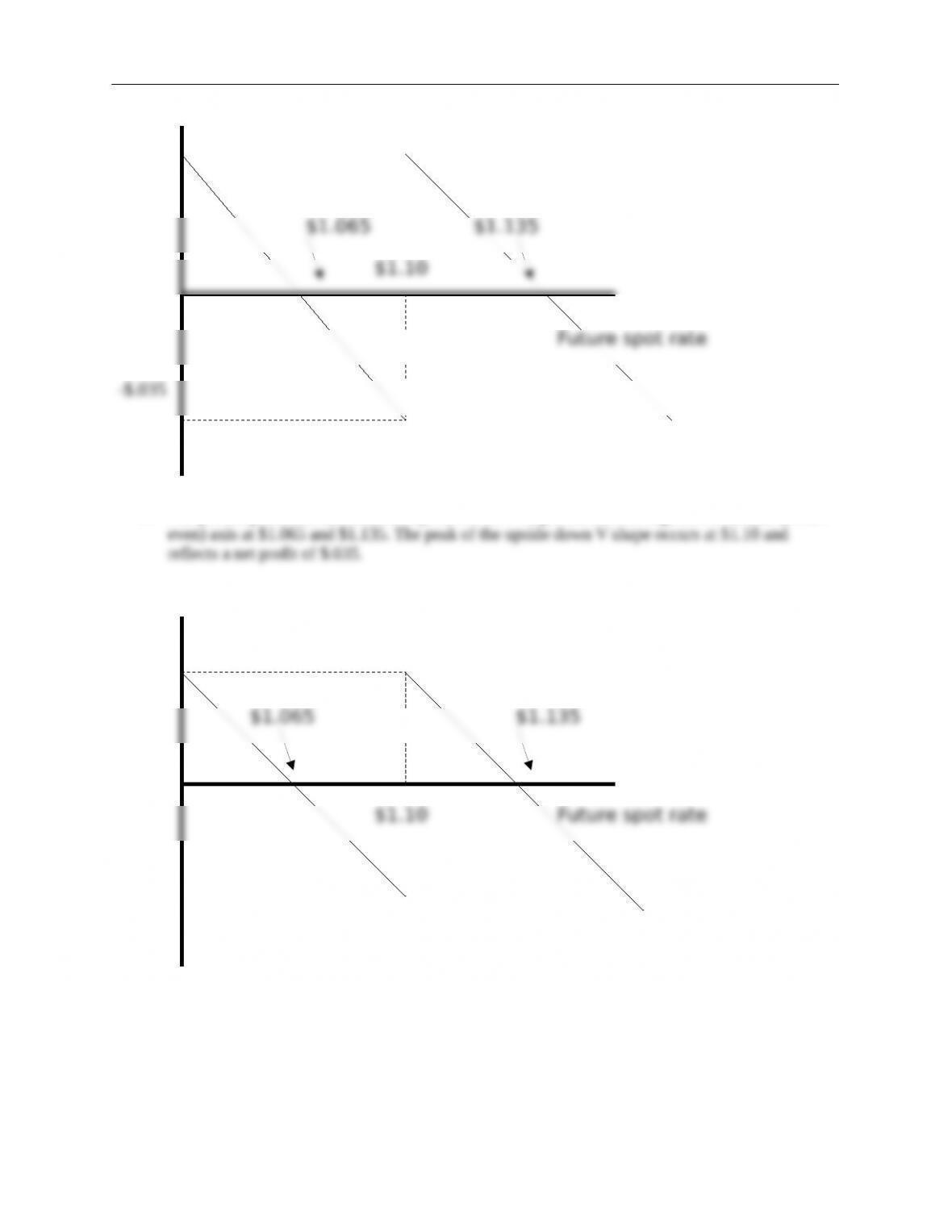

28. Currency Straddles. Refer to the previous question, but assume that the call and put option

premiums are $.02 per unit and $.015 per unit, respectively. (See Appendix B in this chapter.)

a. Construct a contingency graph for a long euro straddle.

b. Construct a contingency graph for a short euro straddle.

ANSWER:

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$1.065 $1.135

$1.10

Currency Derivatives 2

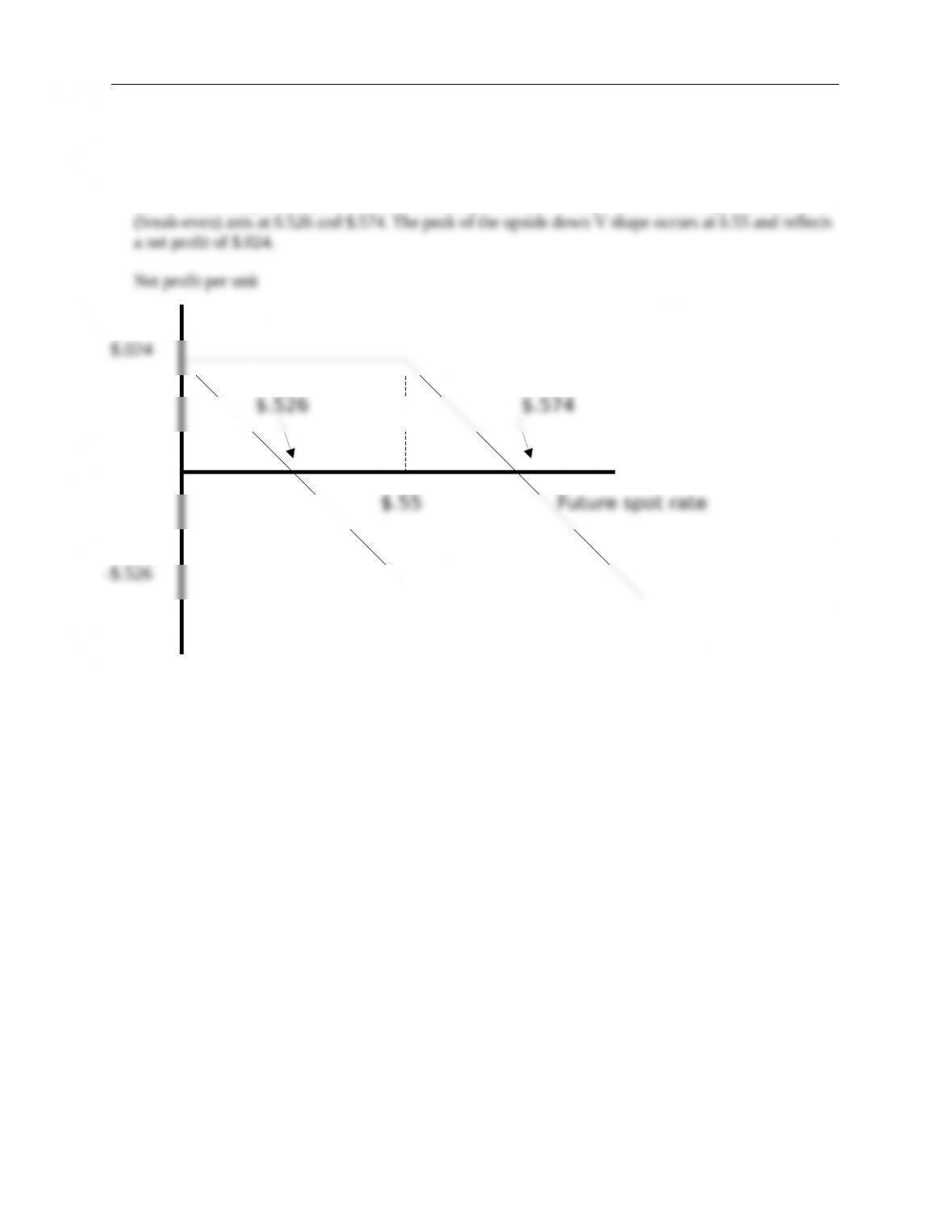

29. Currency Option Contingency Graphs. (See Appendix B in this chapter.) The current spot rate of

the Singapore dollar (S$) is $.50. The following option information is available:

Call option premium on Singapore dollar (S$) = $.015

Put option premium on Singapore dollar (S$) = $.009

Call and put option strike price = $.55

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$1.065

-$1.065

$.526 $.574

Currency Derivatives 3

One option contract represents S$70,000

Construct a contingency graph for a short straddle using these options.

ANSWER: The plotted points should create an upside down V shape that cuts through the horizontal

30. Speculating with Currency Straddles. Maggie Hawthorne is a currency speculator. She has noticed

recently that the euro has appreciated substantially against the U.S. dollar. The current exchange rate

of the euro is $1.15. After reading a variety of articles on the subject, she believes that the euro will

continue to fluctuate substantially in the months to come. Although most forecasters believe that the

euro will depreciate against the dollar in the near future, Maggie thinks that there is also a good

possibility of further appreciation. Currently, a call option on euros is available with an exercise price

of $1.17 and a premium of $.04. A euro put option with an exercise price of $1.17 and a premium of

$.03 is also available. (See Appendix B in this chapter.)

a. Describe how Maggie could use straddles to speculate on the euro’s value.

b. At option expiration, the value of the euro is $1.30. What is Maggie’s total profit or loss from a

long straddle position?

c. What is Maggie’s total profit or loss from a long straddle position if the value of the euro is $1.05

at option expiration?

d. What is Maggie’s total profit or loss from a long straddle position if the value of the euro at

option expiration is still $1.15?

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

-$.526

$.024

Currency Derivatives 4

e. Given your answers to the questions above, when is it advantageous for a speculator to engage in

a long straddle? When is it advantageous to engage in a short straddle?

ANSWER:

a. Since Maggie believes the euro will either appreciate or depreciate substantially, she may

b.

Per Unit Per Contract

c.

Per Unit Per Contract

d.

Per Unit Per Contract

Selling Price of € $1.17 $73,125 ($1.17 × 62,500 units)

e. It is advantageous for a speculator to engage in a long straddle if the underlying currency is

expected to fluctuate drastically, in either direction, prior to option expiration. This is because the

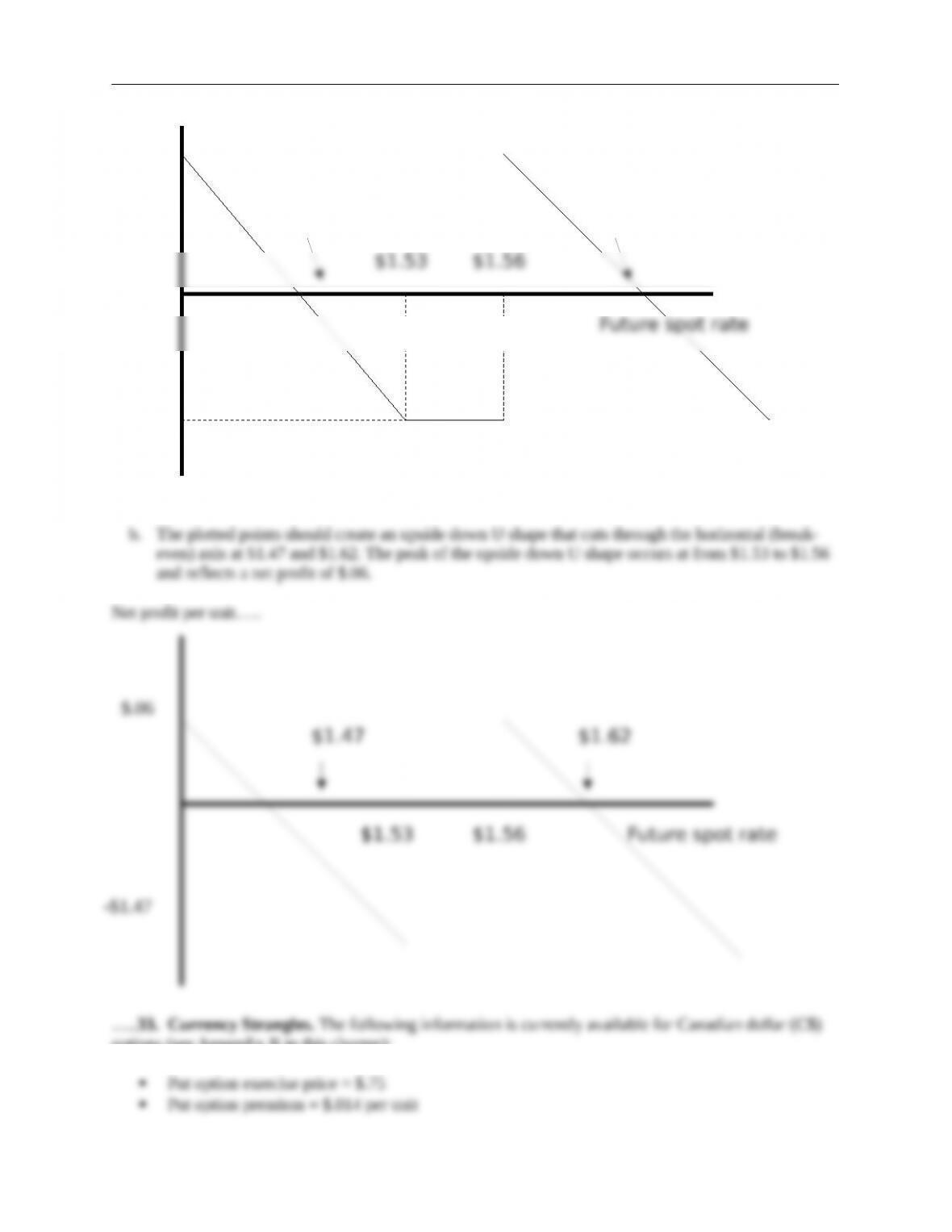

31. Currency Strangles. (See Appendix B in this chapter.) Assume the following options are currently

available for British pounds (₤):

Call option premium on British pounds = $.04 per unit

Put option premium on British pounds = $.03 per unit

Call option strike price = $1.56

Put option strike price = $1.53

One option contract represents ₤31,250.

a. Construct a worksheet for a long strangle using these options.

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Currency Derivatives 5

b. Determine the break-even point(s) for a strangle.

c. If the spot price of the pound at option expiration is $1.55, what is the total profit or loss to the

strangle buyer?

d. If the spot price of the pound at option expiration is $1.50, what is the total profit or loss to the

strangle writer?

ANSWER:

a. Many different worksheets are possible, but one worksheet is shown below.

Value of Pound at Option Expiration

$1.40 $1.53 $1.56 $1.65

b. The break-even points for a strangle are located below the lower exercise price and above the

c. Since $1.55 is between the two exercise prices, neither option will be exercised, and the strangle

d. If the spot price is $1.50, the put option will be exercised, but the call option will expire. On the

put option, the strangle writer will lose $.03 = $1.53 – $1.50. The writer will also collect the

32. Currency Strangles. Refer to the previous question, but assume that the call and put option

premiums are $.035 per unit and $.025 per unit, respectively. (See Appendix B in this chapter.)

a. Construct a contingency graph for a long pound strangle.

b. Construct a contingency graph for a short pound strangle.

ANSWER:

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$1.47 $1.62

Currency Derivatives 6

options (see Appendix B in this chapter):

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$1.47

-$.06

Currency Derivatives 7

a. What is the maximum possible gain the purchaser of a strangle can achieve using these options?

b. What is the maximum possible loss the writer of a strangle can incur?

c. Locate the break-even point(s) of the strangle.

ANSWER:

34. Currency Strangles. For the following options available on Australian dollars (A$), construct a

worksheet and contingency graph for a long strangle. Locate the break-even points for this strangle.

(See Appendix B in this chapter.)

Put option strike price = $.67

Call option strike price = $.65

Put option premium = $.01 per unit

Call option premium = $.02 per unit

ANSWER:

Note that the put strike price exceeds the call strike price in this case.

Value of Australian dollar at Option Expiration

$.60 $.65 $.67 $.70

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

35. Speculating with Currency Options. Barry Egan is a currency speculator. Barry believes that the

Japanese yen will fluctuate widely against the U.S. dollar in the coming month. Currently, one-month

call options on Japanese yen (¥) are available with a strike price of $.0085 and a premium of $.0007

per unit. One-month put options on Japanese yen are available with a strike price of $.0084 and a

premium of $.0005 per unit. One option contract on Japanese yen contains 6.25 million yen. (See

Appendix B in this chapter.)

a. Describe how Barry Egan could utilize these options to speculate on the movement of the

Japanese yen.

b. Assume Barry decides to construct a long strangle in yen. What are the break-even points of this

strangle?

c. What is Barry’s total profit or loss if the value of the yen in one month is $.0070?

d. What is Barry’s total profit or loss if the value of the yen in one month is $.0090?

ANSWER:

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

36. Currency Bullspreads and Bearspreads. A call option on British pounds (₤) exists with a strike

price of $1.56 and a premium of $.08 per unit. Another call option on British pounds has a strike price

of $1.59 and a premium of $.06 per unit. (See Appendix B in this chapter.)

a. Complete the worksheet for a bullspread below.

Value of British Pound at Option Expiration

$1.50 $1.56 $1.59 $1.65

Call @ $1.56

Call @ $1.59

Net

b. What is the breakeven point for this bullspread?

c. What is the maximum profit of this bullspread? What is the maximum loss?

d. If the British pound spot rate is $1.58 at option expiration, what is the total profit or loss for the

bullspread?

e. If the British pound spot rate is $1.55 at option expiration, what is the total profit or loss for a

bearspread?

ANSWER:

a.

Value of British Pound at Option Expiration

$1.50 $1.56 $1.59 $1.65

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Currency Derivatives 10

c. The maximum gain for the bullspread is limited to the difference between the strike prices less

d.

Per Unit Per Contract

Selling Price of ₤ $1.58 $49,375 ($1.58 × 31,250 units)

e. A bearspread using these options involves writing the call option with the $1.56 exercise price

and buying the call option with the $1.59 exercise price. At a spot price of $1.55, neither call

option will be exercised, so the bearspreader nets the difference in options premiums.

Per Unit Per Contract

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.