Topics to Stimulate Class Discussion

1. If a firm consistently exports to a country with low interest rates and needs to consistently borrow

funds, explain how it could coordinate its invoicing and financing to reduce its financing costs.

2. What is the risk of borrowing a low interest rate currency?

3. Assume that foreign currencies X, Y, and Z are highly correlated. If a firm diversifies its financing

among these three currencies, will it substantially reduce its exchange rate exposure (as opposed to

borrowing all funds from one of these foreign currencies)? Explain.

POINT/COUNTER-POINT:

Do MNCs Increase Their Risk When Borrowing Foreign Currencies?

POINT: Yes. MNCs should borrow the currency that matches their cash inflows. If they borrow a foreign

currency to finance business in a different currency, they are essentially speculating on the future exchange

rate movements. The results of this strategy are uncertain, which represents risk to the MNC and its

shareholders.

COUNTER-POINT: No. If MNCs expect that they can reduce the effective financing rate by borrowing a

foreign currency, they should consider borrowing that currency. This enables them to achieve lower costs,

and improves their ability to compete. If they take the most conservative approach by borrowing whatever

currency matches their inflows, they may incur higher costs, and have a greater chance of failure.

WHO IS CORRECT? Use the Internet to learn more about this issue. Which argument do you support?

Offer your own opinion on this issue.

Answers to End of Chapter Questions

1. Financing From Subsidiaries. Explain why an MNC parent would consider financing from its

subsidiaries.

ANSWER: A parent may obtain funds at a lower cost from its subsidiaries than from a bank, since a

2. Foreign Financing.

a. Explain how a firm’s degree of risk aversion enters into its decision of whether to finance in a

foreign currency or a local currency.

b. Assume that interest rate parity exists. If the forward rate is an unbiased forecast of the future spot

rate, explain the implications from borrowing a foreign currency (versus local financing) over time.

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 2

ANSWER: A very risk-averse firm may prefer to borrow domestically since it knows with certainty

the cost of financing in advance. Yet, other firms may feel that the potential cost savings from foreign

financing outweighs the risk (uncertainty); this may motivate them to consider financing in a foreign

3. Probability Distribution.

a. Discuss the development of a probability distribution of effective financing rates when financing in

a foreign currency. How is this distribution developed?

b. Once the probability distribution of effective financing rates from financing in a foreign currency is

developed, how can this distribution be used in deciding whether to finance in the foreign currency

or the home currency?

ANSWER: First, a probability distribution of exchange rate changes is created. Using this along with

4. Financing and Exchange Rate Risk. How can a U.S. firm finance in euros and not necessarily be

exposed to exchange rate risk?

5. Short-term Financing Analysis. Assume that Davenport Inc. needs $3 million for a one-year period.

Within one year, it will generate enough U.S. dollars to pay off the loan. It is considering three

options: (1) borrowing U.S. dollars at an interest rate of 6%, (2) borrowing Japanese yen at an interest

rate of 3%, or (3) borrowing Canadian dollars at an interest rate of 4%. Davenport Inc. expects that

the Japanese yen will appreciate by 1% over the next year and that the Canadian dollar will appreciate

by 3%. What is the expected “effective” financing rate for each of the three options? Which option

appears to be most feasible? Why might Davenport Inc. not necessarily choose the option reflecting

the lowest effective financing rate?

ANSWER:

Expected

Interest Expected Percentage Effective

Currency Rate Change in Currency Financing Rate

Dollars 6% — 6.00%

Japanese yen 3% +1% 4.03%

Canadian dollars 4% +3% 7.12%

ANSWER: The Japanese yen option appears to be the most feasible option. Yet, the exchange rate

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 3

6. Effective Financing Rate. How is it possible for a firm to incur a negative effective financing rate?

ANSWER: If the currency borrowed substantially depreciates against the firm’s home currency (by at

7. IRP Application to Short-term Financing. Connecticut Co. plans to finance its operations in the

U.S. It can borrow euros on a short-term basis at a lower interest rate than if it borrowed

dollars. If interest rate parity does not hold, what strategy should Connecticut Co. consider when it

needs short-term financing?

a. Assume that Connecticut Co. needs dollars. It borrows euros at a lower interest rate than that for

dollars. If interest rate parity exists and if the forward rate of the euro is a reliable predictor of the

future spot rate, what does this suggest about the feasibility of such a strategy?

b. If Connecticut Co. expects the spot rate to be a more reliable predictor of the future spot rate, what

does this suggest about the feasibility of such a strategy?

ANSWER: The firm could consider borrowing a foreign currency and purchasing the currency

8. IRP Application to Foreign Financing. Seabreeze Co. needs to finance some dollar-denominated

expenses for one year. It can borrow euros cheaper than dollars. Interest rate partiy exists. The one–

year forward rate of the euro contains a premium of 4%. If it believes the euro will appreciate by 6%

over the next year, would its expected financing expense be lower if it borrowed dollars or euros.

ANSWER: If the euro appreciates by 4%, it will cause the financing with euros to beas costly as a

9. IRP Application to Short-term Financing. Assume that interest rate parity exists. If a firm believes

that the forward rate is an unbiased predictor of the future spot rate, will it expect to achieve lower

financing costs by consistently borrowing a foreign currency with a low interest rate?

ANSWER: No, because a foreign currency with a relatively low interest rate exhibits a forward

10. Effective Financing Rate. Greensboro, Inc., needs $4 million for one year. It currently has no

business in Japan but plans to borrow Japanese yen from a Japanese bank, because the Japanese

interest rate is three percentage points lower than the U.S. rate. Assume that interest rate parity exists;

also assume that Greensboro believes that the one-year forward rate of the Japanese yen will exceed the

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 4

future spot rate one year from now. Will the expected effective financing rate be higher, lower, or the

same as financing with dollars? Explain.

ANSWER: Since the forward rate is expected to overestimate the future spot rate, this implies that the

11. IRP Application to Short-term Financing. Assume that the U.S. interest rate is 7 percent and the

euro’s interest rate is 4 percent. Assume that the euro’s forward rate has a premium of 4 percent.

Determine whether the following statement is true: “Interest rate parity does not hold; therefore, U.S.

firms could lock in a lower financing cost by borrowing euros and purchasing euros forward for one

year.” Explain your answer.

ANSWER: No. While interest rate parity does not hold, the financing with euros would result in an

12. Implications of the Forward Rate for Foreign Financing. Mizner, Inc., is a U.S.-based MNC with a

subsidiary in Mexico. Its Mexican subsidiary needs a one-year loan of 10 million pesos for operating

expenses. It can borrow pesos at 11% and can use peso revenues to be received over the year to repay

the loan. Alternatively, it can borrow dollars at 6%. Interest rate parity exists. The forward rate of the

peso is expected to overestimate the spot rate of the peso in one year. Should the subsidiary borrow

pesos or dollars?

ANSWER: If the subsidiary borrows dollars, it will have to convert its peso revenues to repay the loan.

13. Financing During a Crisis. Bradenton, Inc., has a foreign subsidiary in Asia that commonly obtains

short-term financing from local banks. If Asian suddenly experiences a crisis, explain why Bradenton

may not be able to easily obtain funds from the local banks.

ANSWER: The foreign subsidiary may find that the local banks do not have adequate funding from

14. Impact of Credit Crisis on Risk of Financing. Homewood Co. commonly finances some of its U.S.

expansion by repeatedly borrowing on a short-term basis. Explain how a global credit crisis might limit

the firm’s ability to repeatedly borrow short-term funds and increase the cost of borrowing.

ANSWER: A credit crisis could limit the amount of short-term funds that banks are willing to lend,

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 5

15. Probability Distribution of Financing Costs. Missoula, Inc., decides to borrow Japanese yen for one

year. The interest rate on the borrowed yen is 8 percent. Missoula has developed the following

probability distribution for the yen’s degree of fluctuation against the dollar:

Possible Degree of

Fluctuation of Percentage

Yen Against the Dollar Probability

–4% 20%

–1% 30%

0% 10%

3% 40%

Given this information, what is the expected value of the effective financing rate of the Japanese yen

from the U.S. corporation’s perspective?

16. Analysis of Short-term Financing. Jacksonville Corp. is a U.S.-based firm that needs $600,000.

It has no business in Japan but is considering one-year financing with Japanese yen, because the annual

interest rate would be 5 percent versus 9 percent in the United States. Assume that interest rate parity

exists.

a. Can Jacksonville benefit from borrowing Japanese yen and simultaneously purchasing yen one year

forward to avoid exchange rate risk? Explain.

b. Assume that Jacksonville does not cover its exposure and uses the forward rate to forecast the

future spot rate. Determine the expected effective financing rate. Should Jacksonville finance with

Japanese yen? Explain.

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 6

c. Assume that Jacksonville does not cover its exposure and expects that the Japanese yen will

appreciate by either 5 percent, 3 percent, or 2 percent, and with equal probability of each

occurrence. Use this information to determine the probability distribution of the effective financing

rate. Should Jacksonville finance with Japanese yen? Explain.

ANSWER:

17. Financing With a Portfolio. Pepperdine, Inc., considers obtaining 40 percent of its one-year financing

in Canadian dollars and 60 percent in Japanese yen. The forecasts of appreciation in the Canadian

dollar and Japanese yen for the next year are as follows:

Probability

Possible Percentage of that Percentage

Change in the Spot Change in the

Currency Rate Over the Loan Life Spot Rate Occurring

Canadian dollar 4% 70%

Canadian dollar 7 30

Japanese yen 6 50

Japanese yen 9 50

The interest rate on the Canadian dollar is 9 percent, and the interest rate on the Japanese yen is 7

percent. Develop the possible effective financing rates of the overall portfolio and the probability of

each possibility based on the use of joint probabilities.

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 7

18. Financing With a Portfolio.

a. Does borrowing a portfolio of currencies offer any possible advantages over the borrowing of a

single foreign currency?

b. If a firm borrows a portfolio of currencies, what characteristics of the currencies will affect the

potential uncertainty of the portfolio’s effective financing rate? What characteristics would be

desirable from a borrowing firm’s perspective?

ANSWER: Currencies which are volatile and highly correlated with each other could cause the

19. Financing With a Portfolio. Raleigh Corp. needs to borrow funds for one year to support its

operations in the United States. The following interest rates are available:

Country Borrowing Rate

U.S. 10%

Canada 6%

Japan 5%

The percentage change in the spot rates of the Canadian dollar and Japanese yen over the next year are

as follows:

Canadian Dollar Japanese Yen

Percentage Change Percentage Change

Probability in Spot Rate Probability in Spot Rate

10% 5% 20% 6%

90% 2% 80% 1%

If Raleigh Corporation borrows a portfolio that has 50 percent of funds from Canadian dollars and 50

percent of funds from yen, determine the probability distribution of the effective financing rate of the

portfolio. What is the probability that Raleigh will incur a higher effective financing rate from

borrowing this portfolio than from borrowing U.S. dollars?

ANSWER:

Effective

Financing

Interest Possible Rate Based on

Currency Rate % Change that Change Probability

Canadian dollar 6% 5% 11.3% 10%

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 8

Possible Joint

Effective

Financing Rate Joint Effective Financing

C$ JY Probability Rate of Portfolio

11.3% 11.3% (10%)(20%) = 2% .5(11.3%) + .5(11.3%) = 11.3%

There is a 2 percent chance that Raleigh will incur a higher effective financing rate from borrowing the

portfolio.

CRITICAL THINKING

MNC’s Use of Dollar–Denominated Short-term Debt In recent years, U.S. short-term interest rates have

been close to zero. Write a short essay to provide your opinion on whether you (as a manger of an MNC)

might be more willing to use dollar-denominated short-term debt to cover short-term funding needs for

subsidiaries in foreign countries that generate positive earnings. Explain the possible tradeoffs involved.

ANSWER

The use of short-term dollar denominated debt results in a lower interest expense. However, the MNC

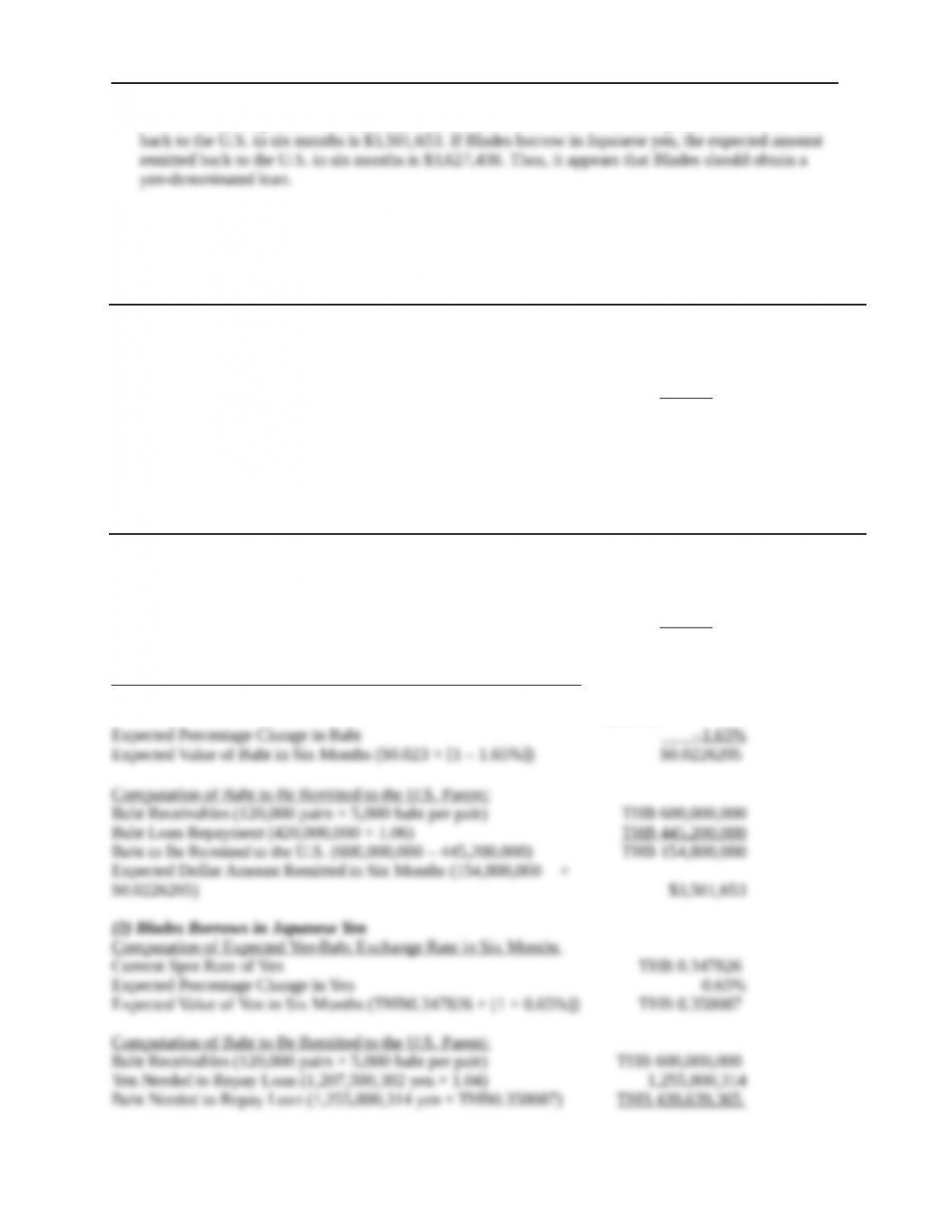

Solution to Continuing Case Problem: Blades, Inc.

1. What is the amount, in baht, that Blades needs to borrow to cover the payments due to the Thai

suppliers? What is the amount, in yen, that Blades needs to borrow to cover the payments due to the

Thai suppliers?

ANSWER: Since Blades will purchase materials necessary to manufacture 120,000 pairs of

If Blades borrows in yen, the yen would be converted to Thai baht in order to pay the Thai supplier.

Thus, Blades will have to obtain a loan for THB420,000,000/THB0.347826 = ¥1,207,500,302.

2. Given that Blades will use the receipts from the receivables in Thailand to repay the loan and that the

subsidiary plans to remit all baht-denominated cash flows back to the U.S. parent whether it borrows in

baht or yen, does the future value of the yen with respect to the baht affect the cost of the loan if Blades

borrows in yen?

3. Using a spreadsheet, compute the expected amount (in U.S. dollars) that will be remitted back to the

U.S. in six months if Blades finances its working capital requirements by borrowing baht versus

borrowing yen. Based on your analysis, should Blades obtain a yen– or baht-denominated loan?

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 9

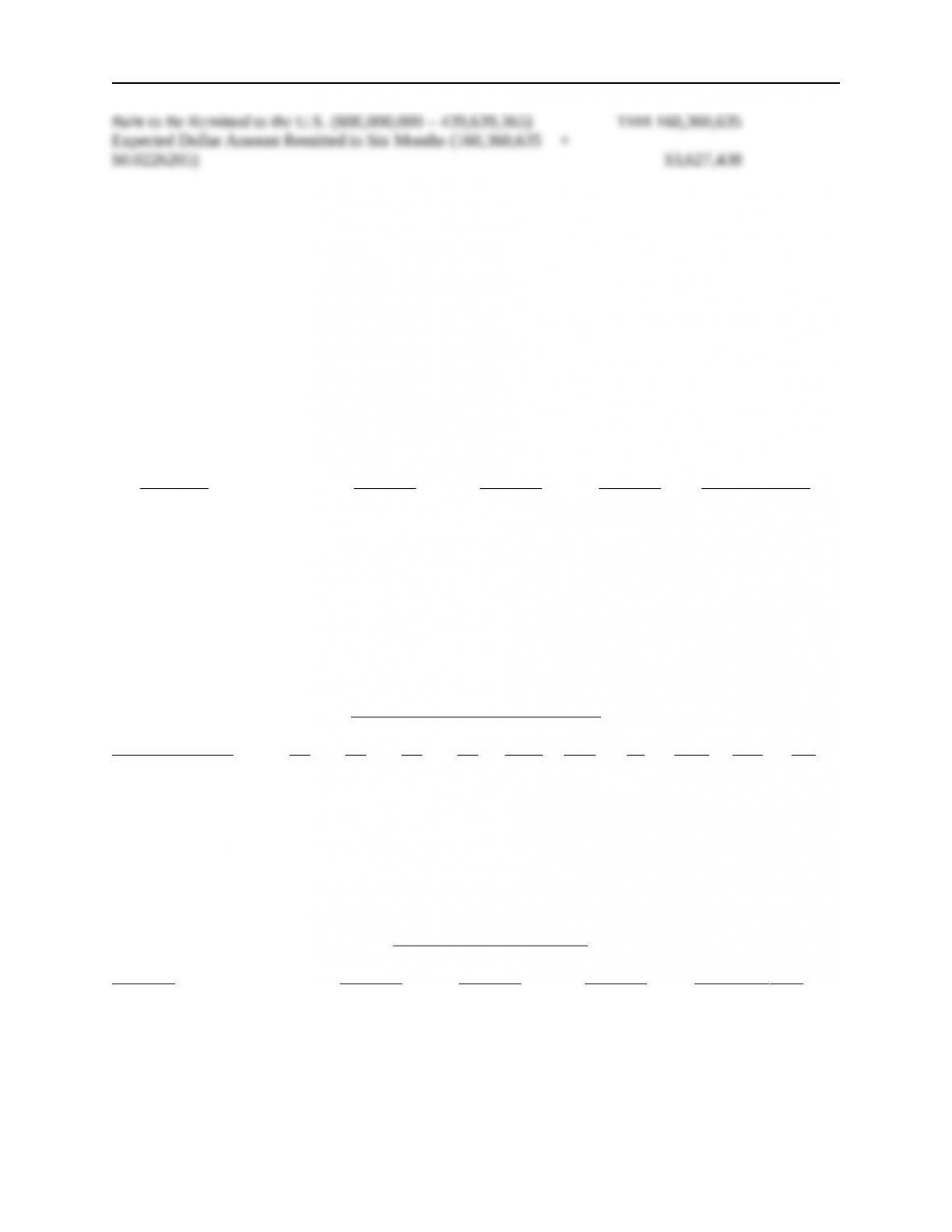

ANSWER: (See spreadsheet attached.) If Blades borrows in Thai baht, the expected amount remitted

Computation of Expected Change in Value of Thai Baht (Relative to the Dollar)

(1) (2) (3) = (1) × (2)

Possible Rate of Change in the Probability of

Thai Baht Over the Life of the Loan Occurrence Product

–3% 30% –0.90%

–2% 30% –0.60%

–1% 20% –0.20%

0% 15% 0.00%

1% 5% 0.05%

–1.65% = Expected Change

Computation of Expected Change in Value of Japanese Yen (Relative to the Baht)

(1) (2) (3) = (1) × (2)

Possible Rate of Change in the Probability of

Japanese Yen Over the Life of the Loan Occurrence Product

2% 30% 0.60%

1% 30% 0.30%

0% 20% 0.00%

–1% 15% –0.15%

–2% 5% –0.10%

0.65% = Expected Change

(1) Blades Borrows in Thai Baht

Computation of Expected Baht-Dollar Exchange Rate in Six Months

Current Spot Rate of Baht

$0.0230

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 10

Solution to Supplemental Case: Flyer Company

a. The optimal portfolio is dependent on your degree of risk aversion. By converting the information in

the table above into 4 bar charts (showing the probability distribution), one above another, you can

review the risk-return tradeoff.

By using a spreadsheet format, the percentage changes in exchange rates can be easily computed.

Using these percentage changes along with the interest rates, the effective financing rate can be

computed for each currency under each scenario. The effective financing rates are provided below for

each scenario, along with the expected value of the effective financing rate (using the probabilities

assigned to each scenario):

Somewhat Expected Value

Strong $ Stable $ Weak $ of Effective

Currency Scenario Scenario Scenario Financ ing Rate

Australian dollar –0.56% 14.51% 28.07% 14.05%

British pound 4.56 14.48 21.10 13.49

Canadian dollar 9.71 9.71 17.45 12.03

Japanese yen –1.00 11.60 29.60 13.22

Mexican peso –8.18 13.47 18.06 8.35

New Zealand dollar –5.48 5.22 12.35 4.14

Singapore dollar –4.60 1.76 10.24 2.40

South African rand 2.19 5.59 15.81 7.64

U.S. dollar 9.00 9.00 9.00 9.00

Venezuelan bolivar 2.20 10.60 20.40 11.02

Percentage of Funds Borrowed from:

Type of Portfolio A$ BP C$ JY MXP NZ$ S$ SAR US$ VB

Risk neutral 0 0 0 0 0 0 100 0 0 0

Balanced 0 0 0 0 25 25 25 25 0 0

Conservative 0 0 0 0 10 10 10 10 60 0

Ultra-conservative 0 0 0 0 0 0 0 0 100 0

Each portfolio’s effective financing rates are determined as a sum of weighted effective financing rates

under each scenario.

Portfolio’s Effective

Financing Rate Based on a Expected Value

Strong $ Stable $ Weak $ of Effective

Portfolio Scenario Scenario Scenario Financing Rate

Risk neutral –4.60% 1.76% 10.24% 2.40%

Balanced –4.02 6.51 14.11 5.63

Conservative 3.79 8.00 11.04 7.65

Ultra-conservative 9.00 9.00 9.00 9.00

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Short-Term Financing 11

The decision of which portfolio to use would be based on your degree of risk aversion. By converting the

table above into 4 bar charts, (showing the profitability distribution), one above another, you can review

the tradeoff between lower financing costs and risk.

Small Business Dilemma

Short-Term Financing by the Sports Exports Company

1. Should Logan borrow dollars or pounds to finance his joint venture business? Why?

ANSWER: Jim should borrow pounds. Although the British interest rate is slightly higher, Jim could

2. Logan could also borrow euros at an interest rate that is lower than the U.S. or British rate. The values

of the euro and pound tend to move in the same direction against the dollar but not always by the same

degree. Would borrowing euros to support the British joint venture result in more exposure to

exchange rate risk than borrowing pounds? Would it result in more exposure to exchange rate risk than

borrowing dollars?

ANSWER: Borrowing euros would result in more exchange rate risk than borrowing pounds, because

© 2018 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.