Archives: Solution Manual

978-1259277177 Chapter 15 Solution Manual Part 2

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 17. a. We obtain forward rates from the following table: Maturit y YTM Forward Rate Price (for parts c, d) 1 year 10% $1,000/1.10 = $909.09 b., c. We obtain next year’s […]

978-1259277177 Chapter 15 Solution Manual Part 1

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS. 1. In general, the forward rate can be viewed as the sum of the market’s expectation of the future short rate plus […]

978-1259277177 Chapter 14 Solution Manual Part 2

CHAPTER 14: BOND PRICES AND YIELDS 29. a. The floating rate note pays a coupon that adjusts to market levels. Therefore, it b. Floating rate notes may not sell at par for any of several reasons: (i) The yield spread […]

978-1259277177 Chapter 14 Solution Manual Part 1

CHAPTER 14: BOND PRICES AND YIELDS CHAPTER 14: BOND PRICES AND YIELDS PROBLEM SETS 1. a. Catastrophe bond—A bond that allows the issuer to transfer “catastrophe risk” from the firm to the capital markets. Investors in these bonds receive a […]

978-1259277177 Chapter 13 Solution Manual

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS PROBLEM SETS 1. Using the regression feature of Excel with the data presented in the text, the first-pass (SCL) estimation results are: Stock: A B C […]

978-1259277177 Chapter 12 Solution Manual Part 2

24. In order to create the relative strength measure, we converted the weekly returns for the Fidelity Banking Fund and for the S&P 500 to weekly index values, using a base of 100 for a. The following graph summarizes the […]

978-1259277177 Chapter 12 Solution Manual Part 1

CHAPTER 12: BEHAVIORAL FINANCE AND TECHNICAL ANALYSIS CHAPTER 12: BEHAVIORAL FINANCE AND TECHNICAL ANALYSIS PROBLEM SETS 1. Technical analysis can generally be viewed as a search for trends or patterns in market prices. Technical analysts tend to view these trends […]

978-1259277177 Chapter 11 Solution Manual

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS PROBLEM SETS 1. The correlation coefficient between stock returns for two nonoverlapping periods 2. No. Microsoft’s continuing profitability does not imply that stock market investors who purchased Microsoft […]

978-1259277177 Chapter 10 Solution Manual

CHAPTER 10: ARBITRAGE PRICING THEORY AND MULTIFACTOR MODELS OF RISK AND RETURN CHAPTER 10: ARBITRAGE PRICING THEORY AND MULTIFACTOR MODELS OF RISK AND RETURN PROBLEM SETS 1. The revised estimate of the expected rate of return on the stock would […]

978-1259277177 Chapter 9 Solution Manual

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL CHAPTER 9: THE CAPITAL ASSET PRICING MODEL PROBLEM SETS 1. 2. If the security’s correlation coefficient with the market portfolio doubles (with all other variables such as variances unchanged), then beta, and therefore […]

978-1259277177 Chapter 8 Solution Manual Part 2

CHAPTER 8: INDEX MODELS 17. a. Alpha (α) Expected excess return αi = ri – [rf + βi × (rM – rf ) ] E(ri ) – rf αA = 20% – [8% + 1.3 × (16% – 8%)] = […]

978-1259277177 Chapter 8 Solution Manual Part 1

CHAPTER 8: INDEX MODELS CHAPTER 8: INDEX MODELS PROBLEM SETS 1. The advantage of the index model, compared to the Markowitz procedure, is the vastly reduced number of estimates required. In addition, the large number of 2. The trade-off entailed […]

978-1259277177 Chapter 7 Solution Manual Part 2

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS 17. The correct choice is (c). Intuitively, we note that since all stocks have the same expected rate of return and standard deviation, we choose the stock that will result in lowest risk. This is […]

978-1259277177 Chapter 7 Solution Manual Part 1

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS CHAPTER 7: OPTIMAL RISKY PORTFOLIOS PROBLEM SETS 1. (a) and (e). Short-term rates and labor issues are factors that are common to all 2. (a) and (c). After real estate is added to the portfolio, […]

978-1259277177 Chapter 6 Solution Manual Part 2

24. For y to be less than 1.0 (that the investor is a lender), risk aversion (A) must be large enough such that: 1 σ 2 M fM A r)E(r y 1.28 0.25 0.050.13 2 A […]

978-1259277177 Chapter 6 Solution Manual Part 1

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS PROBLEM SETS 1. (d) While a higher or lower Sharpe ratios are not an indication of an investor’s 2. (b) […]

978-1259277177 Chapter 5 Solution Manual

CHAPTER 5: INTRODUCTION TO RISK, RETURN, AND THE HISTORICAL RECORD CHAPTER 5: INTRODUCTION TO RISK, RETURN, AND THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected […]

978-1259277177 Chapter 3 Solution Manual

CHAPTER 3: HOW SECURITIES ARE TRADED CHAPTER 3: HOW SECURITIES ARE TRADED PROBLEM SETS 1. Stop-loss order: allows a stock to be sold if the price falls below a predetermined 2. In response to the potential negative reaction to large […]

978-1259277177 Chapter 1 Solution Manual

CHAPTER 1: THE INVESTMENT ENVIRONMENT CHAPTER 1: THE INVESTMENT ENVIRONMENT PROBLEM SETS 1. While it is ultimately true that real assets determine the material well-being of an economy, financial innovation in the form of bundling and unbundling securities 2. Securitization […]

978-1259277160 Chapter 21 Solution Manual Part 2

Chapter 21: International Financial Management 21-2. Solution: One dollar is worth 2.929 Polish zloty ($1/0.3414) and one British pound is worth 1.4973 dollars. 3. Purchasing power theory (LO21-2) From the base price level of 100 in 1979, Saudi Arabian and […]

978-1259277160 Chapter 21 Solution Manual Part 1

Chapter 21 International Financial Management Discussion Questions 21-1. What risks does a foreign affiliate of a multinational firm face in today’s business world? In addition to the normal risks that a domestic firm faces (such as the risk 21-2. What […]

978-1259277160 Chapter 21 Lecture Note

International Financial Management Author’s Overview The instructor should stress the importance of international financial management (and international trade) to the class. The students can easily appreciate the everyday events that bring the world closer together. An important point is that […]

978-1259277160 Chapter 20 Solution Manual Part 2

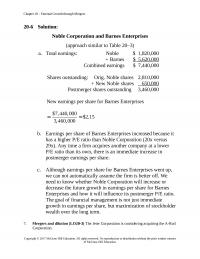

Chapter 20 – External Growth through Mergers 20-6 Solution: Noble Corporation and Barnes Enterprises (approach similar to Table 20–3) New earnings per share for Barnes Enterprises $7,440,000 $2.15 3,460,000 = = b. Earnings per share of Barnes Enterprises increased because […]

978-1259277160 Chapter 20 Solution Manual Part 1

Chapter 20 External Growth through Mergers Discussion Questions 20-1. Name three industries in which mergers have been prominent. 20-2. What is the difference between a merger and a consolidation? In a merger, two or more companies are combined, but only […]

978-1259277160 Chapter 20 Lecture Note

External Growth through Mergers Author’s Overview The discussion of mergers and acquisitions brings together a number of topics discussed earlier in the text. The instructor is able to take a second look at earnings per share growth, price-earnings ratios, stockholder […]

978-1259277160 Chapter 19 Solution Manual Part 3

Chapter 19: Convertibles, Warrants, and Derivatives 19-20. Solution: Online Network Inc. a. Basic earnings per share Earnings $650,000 $6.50 Shares 100,000 = = = b. Diluted earnings per share Adjusted earnings after taxes Shares outstanding + All convertible securities = […]

978-1259277160 Chapter 19 Solution Manual Part 2

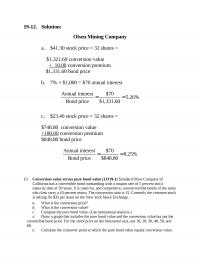

19-12. Solution: Olsen Mining Company b. 7% × $1,000 = $70 annual interest Annual interest $70 5.26% Bond price $1,331.60 = = c. $23.40 stock price × 32 shares = $748.80 conversion value +100.00 conversion premium $848.80 bond price Annual […]

978-1259277160 Chapter 19 Solution Manual Part 1

Chapter 19 Convertibles, Warrants, and Derivatives Discussion Questions 19-1. What are the basic advantages to the corporation of issuing convertible securities? The advantages to the corporation of a convertible security are: 19-2. Why are investors willing to pay a premium […]

978-1259277160 Chapter 19 Lecture Note

Convertibles, Warrants, and Derivatives Author’s Overview Because the material in the chapter can be viewed from both a corporate finance and investments perspective, the student’s interest in the chapter is usually quite high. The student is given an in depth […]

978-1259277160 Chapter 18 Solution Manual Part 3

Chapter 18: Dividend Policy and Retained Earnings 18-18. Solution: Ace Products *240,000 shares × ($20 market price – $5 par value) = 240,000 × $15 = $3,600,000 $ 5,000,000 Beginning capital in excess of par account + $ 3,600,000 Additional […]

978-1259277160 Chapter 18 Solution Manual Part 2

18-10. Solution: Pills Berry Company a. Annual dividend yield = Cash dividends/Price b. Earnings per share = Cash dividends/.5 = $1.80/.5 = $3.60 P/E ratio = Price/Earnings per share = $60/$3.60 = 16.67x 11. Dividend yield (LO18-1) The shares of […]

978-1259277160 Chapter 18 Solution Manual Part 1

Chapter 18 Dividend Policy and Retained Earnings Discussion Questions 18-1. How does the marginal principle of retained earnings relate to the returns that a stockholder may make in other investments? The marginal principle of retained earnings suggests that the corporation […]

978-1259277160 Chapter 18 Lecture Note

Dividend Policy and Retained Earnings Author’s Overview The key initial question to be asked is: How does a corporation determine the amount of dividends to be paid? The discussion should move to the marginal principle of retained earnings with the […]

978-1259277160 Chapter 17 Solution Manual Part 3

Chapter 17: Common and Preferred Stock Financing 17-20. Solution: Enterprise Storage Company b. Stock Price Present value of common stock dividends PV Factor Present Amount at 14% Value D1$1.15 .877 $1.01 D21.25 .769 .96 D31.35 .675 .91 D4 1.45 .592 […]

978-1259277160 Chapter 17 Solution Manual Part 2

17-10. Solution: Northern Airlines Mr. Michaels controls 280,000 votes (40,000 shares × 7 directors). 11. Different classes of voting stock (LO17-1) Rust Pipe Co. was established in 1994. Four years later, the company went public. At that time, Robert Rust, […]

978-1259277160 Chapter 17 Solution Manual Part 1

Chapter 17 Common and Preferred Stock Financing Discussion Questions 17-1. Why has corporate management become increasingly sensitive to the desires of large institutional investors? Corporate management has become increasingly sensitive to the desires of 17-2. Why might a corporation use […]

978-1259277160 Chapter 17 Lecture Note

Common and Preferred Stock Financing Author’s Overview The first part of the chapter gives the student a clear view of the changing nature of stock ownership through increasing institutional participation and the declining importance of individual stock ownership. The residual […]

978-1259277160 Chapter 16 Solution Manual Part 5

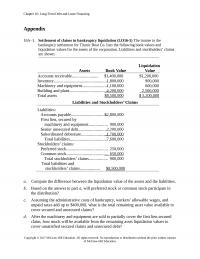

Chapter 16: Long-Term Debt and Lease Financing Appendix 16A–1. Settlement of claims in bankruptcy liquidation (LO16-5) The trustee in the bankruptcy settlement for Titanic Boat Co. lists the following book values and liquidation values for the assets of the corporation. […]

978-1259277160 Chapter 16 Solution Manual Part 4

16-19. Solution: The Sunbelt Corporation First compute the discount rate Outflows 1. Payment on call provision $40,000,000 × 7.5% = $3,000,000 $3,000,000 (1 – .36) = $1,920,000 2. Underwriting cost on new issue Actual expenditure 1.8% × $40,000,000 = $720,000 […]

978-1259277160 Chapter 16 Solution Manual Part 3

16-16. Solution: Mr. Robinson – Mrs. Pinson a. Present value of interest payments Present value of principal payment at maturity PV = FV × PVIF (n = 10*, i = 5.00%) PV = $1,000 × .614 = $614.00 Appendix B […]

978-1259277160 Chapter 16 Solution Manual Part 2

16-6. Solution: Florida Investment Company a. Present value of interest payments Present value of principal payment at maturity PV = FV × PVIF (n = 20, i = 6%) Appendix B PV = $1,000 × .312 = $312.00 Total present […]

978-1259277160 Chapter 16 Solution Manual Part 1

Chapter 16 Long-Term Debt and Lease Financing Discussion Questions 16-1. Corporate debt has been expanding very dramatically in the last three decades. What has been the impact on interest coverage, particularly since 1977? 16-2. What are some specific features of […]

978-1259277160 Chapter 16 Lecture Note

Long-Term Debt and Lease Financing Author’s Overview This chapter covers a broad range of debt topics including secured versus unsecured debt, sinking fund provisions, bond prices, yields, ratings, and conversion and call features. The student gets a good indoctrination into […]

978-1259277160 Chapter 15 Solution Manual Part 3

Chapter 15: Investment Banking: Public and Private Placement 15-19. Solution: Presley Corporation a. $25 Price 95% = $23.75 Net Price b. Earnings per Share before Stock Issue = $7,200,000/2,100,000 = $3.43 c. Earnings per Share after Stock Issue = […]

978-1259277160 Chapter 15 Solution Manual Part 2

15-10. Solution: Wrigley Corporation c. The stock alternative has the larger percentage spread. This is normal because there is more uncertainty in the market associated with a stock offering and investment bankers want to be appropriately compensated. 11. Secondary offering […]

978-1259277160 Chapter 15 Solution Manual Part 1

Chapter 15 Investment Banking: Public and Private Placement Discussion Questions 15-1. In what way is an investment banker a risk taker? The investment banker is a risk taker (underwriter) in that the investment banking 15-2. What is the purpose of […]

978-1259277160 Chapter 15 Lecture Note

Investment Banking: Public and Private Placement Author’s Overview This chapter presents a detailed account of the functions of the investment banker. By making maximum use of material covered under the “distribution process,” the instructor can present a good picture of […]

978-1259277160 Chapter 14 Lecture Note

Capital Markets Author’s Overview This chapter on capital markets is basic to the understanding of the flow of funds through the economy and the relationship of capital markets to corporate bonds, stocks, and preferred stock. Students often view bonds as […]

978-1259277160 Chapter 13 Solution Manual Part 5

COMPREHENSIVE PROBLEMS Comprehensive Problem 1. Gibson Appliance Co. (portfolio effect of a merger) (LO13-5) Gibson Appliance Co. is a very stable billion-dollar company with a sales growth of about 7 percent per year in good or bad economic conditions. Because […]

978-1259277160 Chapter 13 Solution Manual Part 4

13-21. Solution: Oklahoma Pipeline Company a. Standard deviation—year 1 D D ( )D D– 2 ( )D D– P 2 ( )D D– P $55 70 –15 225 .40 90 70 70 0 0 .20 0 85 70 +15 225 […]