CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

PROBLEM SETS

1. Using the regression feature of Excel with the data presented in the text, the

first-pass (SCL) estimation results are:

Stock: A B C D E F G H I

2. The hypotheses for the second-pass regression for the SML are:

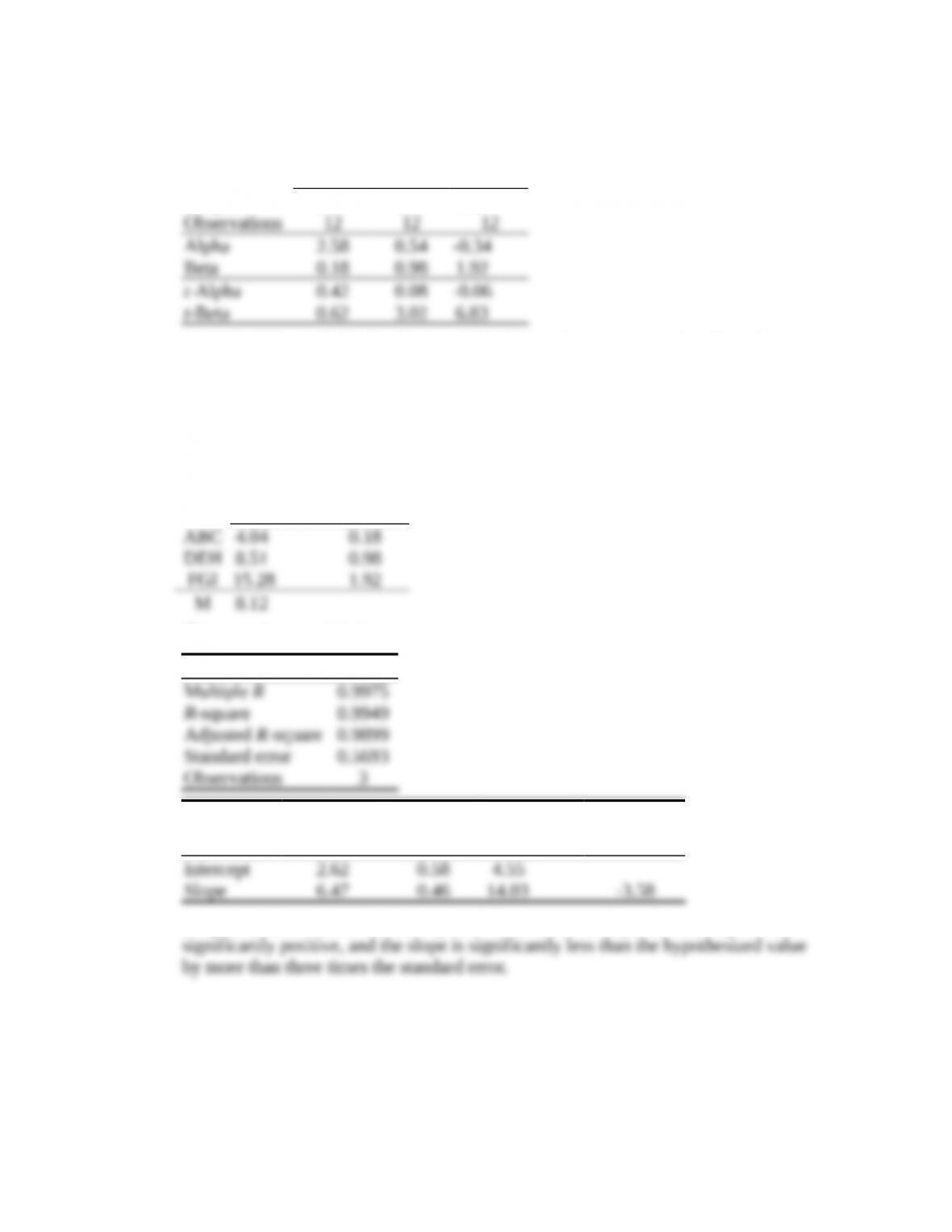

3. The second-pass data from first-pass (SCL) estimates are:

Average

Excess

Return Beta

A 5.18 -0.47

B 4.19 0.59

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

S

The second-pass regression yields:

Regression Statistics

Multiple R0.7074

Coefficients

Standard

Error

t Statistic

for β=0

t Statistic

for β=8.12

4. As we saw in the chapter, the intercept is too high (3.92% per year instead of 0) and

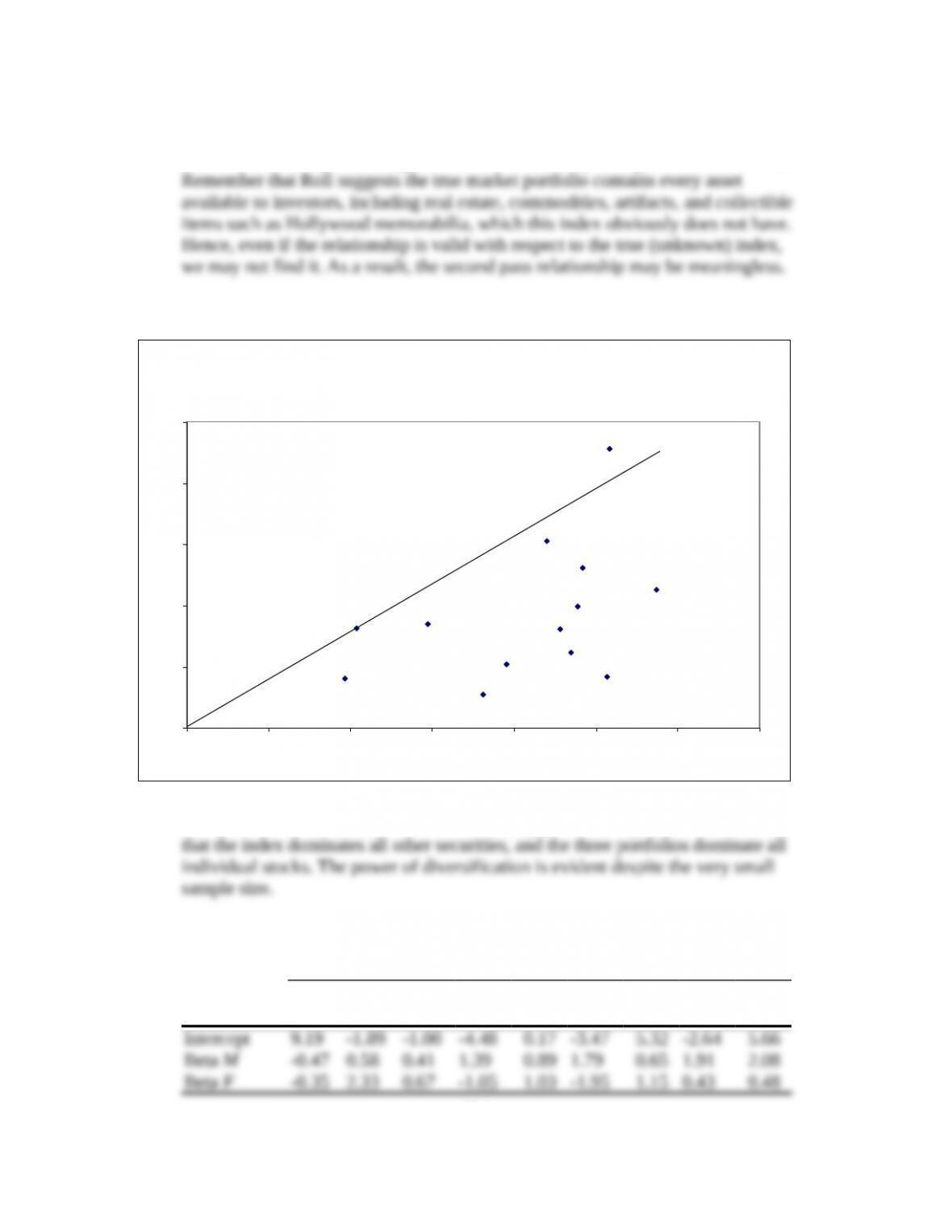

5. Arranging the securities in three portfolios based on betas from the SCL estimates,

the first pass input data are:

Year ABC DEG FHI

1 15.05 25.86 56.69

2 -16.76 -29.74 -50.85

13-2

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

The first-pass (SCL) estimates are:

ABC DEG FHI

R-square 0.04 0.48 0.82

Grouping into portfolios has improved the SCL estimates as is evident from the

higher R-square for Portfolio DEG and Portfolio FHI. This means that the beta

(slope) is measured with greater precision, reducing the error-in-measurement

problem at the expense of leaving fewer observations for the second pass.

The inputs for the second pass regression are:

Average

Excess

Return Beta

The second-pass estimates are:

Regression Statistics

Coefficients

Standard

Error

t Statistic

for β =0

t Statistic

for β =8.12

Despite the decrease in the intercept and the increase in slope, the intercept is now

13-3

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

6. Roll’s critique suggests that the problem begins with the market index, which is

not the theoretical portfolio against which the second pass regression should hold.

7.

Except for Stock I, which realized an extremely positive surprise, the CML shows

8. The first-pass (SCL) regression results are summarized below:

A B C D E F G H I

R-square 0.07 0.36 0.11 0.44 0.24 0.84 0.12 0.68 0.71

Observations 12 12 12 12 12 12 12 12 12

13-4

CAPITAL MARKET LINE FROM SAMPLE DATA

ABC

Market

DEG

C

B

A

D

E

F

G

H

FHI

I

0

5

10

15

20

25

0 10 20 30 40 50 60 70

Standard Deviation

Average Return

CML

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

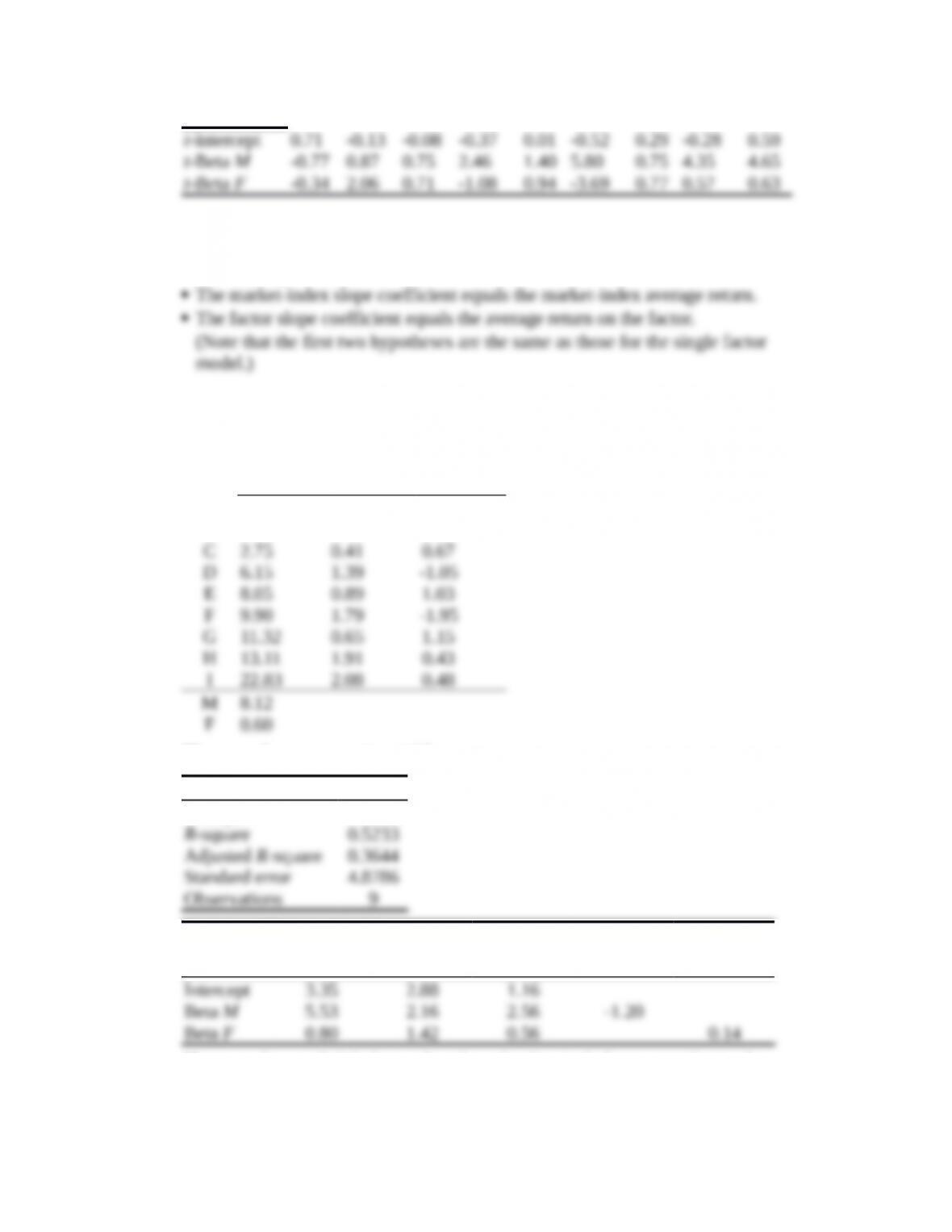

9. The hypotheses for the second-pass regression for the two-factor SML are:

The intercept is zero.

10. The inputs for the second pass regression are:

Average

Excess

Return Beta MBeta F

A 5.18 -0.47 -0.35

B 4.19 0.58 2.33

The second-pass regression yields:

Regression Statistics

Multiple R0.7234

Coefficients

Standard

Error

t Statistic

for β =0

t Statistic

for β =8.12

t Statistic

for β =0.6

These results are slightly better than those for the single factor test; that is, the

intercept is smaller and the slope of M is slightly greater. We cannot expect a great

13-5

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

improvement since the factor we added does not appear to carry a large risk

11. When we use the actual factor, we implicitly assume that investors can perfectly

replicate it, that is, they can invest in a portfolio that is perfectly correlated with the

factor. When this is not possible, one cannot expect the CAPM equation (the second

pass regression) to hold. Investors can use a replicating portfolio (a proxy for the

Proxy Portfolio for Factor F (PF)

Weights on

Universe

Stocks Year

PF Holding

Period

Returns

A -0.14 1 -33.51

B 1.00 2 62.78

This proxy (PF) has an R-square with the actual factor of 0.80.

We next perform the first pass regressions for the two factor model using PF

instead of P:

A B C D E F G H I

R-square

0.08

0.55

0.20

0.43

0.33

0.88

0.16

0.71

0.72

Intercept

9.28

-2.53

-1.35

-4.45

-0.23

-3.20

4.99

-2.92

5.54

13-6

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

Beta PF -0.06 0.42 0.16 -0.13 0.21 -0.29 0.21 0.11 0.08

t-intercept

0.72

-0.21

-0.12

-0.36

-0.02

-0.55

0.27

-0.33

0.58

Note that the betas of the nine stocks on M and the proxy (PF) are different from

those in the first pass when we use the actual proxy.

The first-pass regression for the two-factor model with the proxy yields:

Average

Excess

Return

Beta M Beta PF

A 5.18 -0.50 -0.06

B 4.19 0.80 0.42

The second-pass regression yields:

Regression Statistics

Multiple R0.71

Coefficients Standard

Error

t Statistic

for β =0

t Statistic

for β =8.12

t Statistic

for β =0.6

Intercept 3.50 2.99 1.17

We can see that the results are similar to, but slightly inferior to, those with the

actual factor, since the intercept is larger and the slope coefficient smaller. Note

13-7

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

12. We assume that the value of your labor is incorporated in the calculation of the rate

of return for your business. It would likely make sense to commission a valuation of

your business at least once each year. The resultant sequence of figures for

percentage change in the value of the business (including net cash withdrawals from

CFA PROBLEMS

1. (i) Betas are estimated with respect to market indexes that are proxies for the true

market portfolio, which is inherently unobservable.

(ii) Empirical tests of the CAPM show that average returns are not related to beta

2. a. The basic procedure in portfolio evaluation is to compare the returns on a

where rf is the risk-free rate, E(rM ) is the expected return for the unmanaged

b. The benchmark error might occur when the unmanaged portfolio used in the

13-8

CHAPTER 13: EMPIRICAL EVIDENCE ON SECURITY RETURNS

c. Your graph should show an efficient frontier obtained from actual returns, and

d. The answer to this question depends on one’s prior beliefs. Given a consistent

track record, an agnostic observer might conclude that the data support the

e. The question is really whether the CAPM is at all testable. The problem is that

even a slight inefficiency in the benchmark portfolio may completely

3. The effect of an incorrectly specified market proxy is that the beta of Black’s

portfolio is likely to be underestimated (i.e., too low) relative to the beta calculated

Proxy

2

Proxy

Cov( , )

βσ

Portfolio Market

Portfolio

Market

r r

=

An incorrectly specified market proxy is likely to produce a slope for the security

market line (i.e., the market risk premium) that is underestimated relative to the true

13-9