CHAPTER 14: BOND PRICES AND YIELDS

29. a. The floating rate note pays a coupon that adjusts to market levels. Therefore, it

b. Floating rate notes may not sell at par for any of several reasons:

(i) The yield spread between one-year Treasury bills and other money

(ii) The credit standing of the firm may have eroded (or improved) relative

(iii) The coupon increases are implemented with a lag, i.e., once every

c. The risk of call is low. Because the bond will almost surely not sell for much

d. The fixed-rate note currently sells at only 88% (93/106) of the call price, so that

e. The 6% coupon notes currently have a remaining maturity of 15 years and sell

f. Because the floating rate note pays a variable stream of interest payments to

maturity, the effective maturity for comparative purposes with other debt

30. a. The yield to maturity on the par bond equals its coupon rate, 8.75%. All else

equal, the 4% coupon bond would be more attractive because its coupon rate is far

below current market yields, and its price is far below the call price. Therefore, if

b. If an investor expects yields to fall substantially, the 4% bond offers a greater

expected return.

14-1

CHAPTER 14: BOND PRICES AND YIELDS

c. Implicit call protection is offered in the sense that any likely fall in yields

HPR

%54.191954.0

46.705$

)46.705$29.793($50$

b. Using OID tax rules, the cost basis and imputed interest under the constant

yield method are obtained by discounting bond payments at the original 8% yield

and simply reducing maturity by one year at a time:

Constant yield prices (compare these to actual prices to compute capital gains):

P0 = $705.46

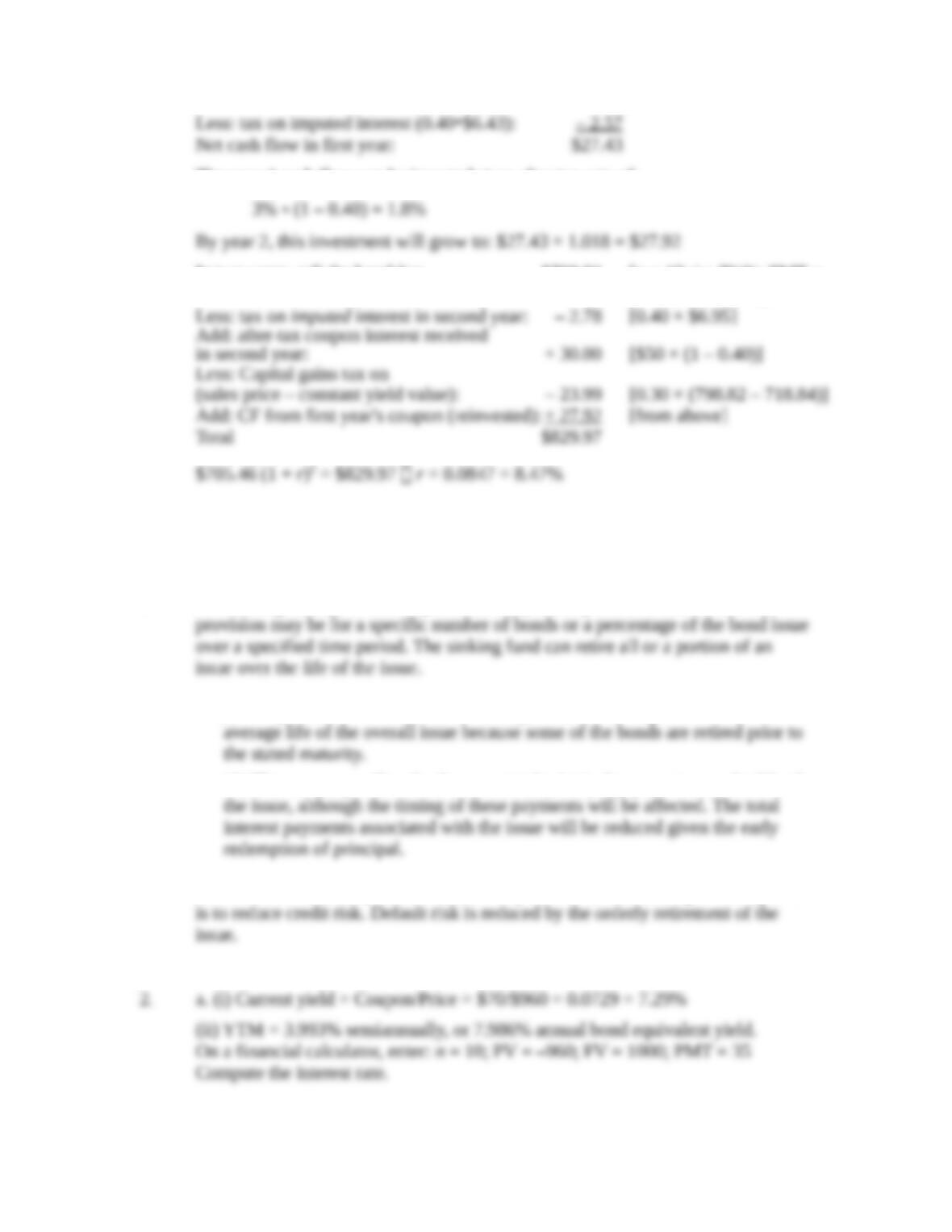

P1 = $711.89 implicit interest over first year = $6.43

P2 = $718.84 implicit interest over second year = $6.95

Tax on explicit interest plus implicit interest in first year =

Capital gain in first year = Actual price at 7% YTM—constant yield price =

c. After tax HPR =

%88.121288.0

46.705$

99.46$)46.705$29.793($50$

d. Value of bond after two years = $798.82 [using n = 18; i = 7%; PMT = $50; FV =

$1,000]

Reinvested income from the coupon interest payments = $50*1.03 + $50 = $101.50

Total funds after two years = $798.82 + $101.50 = $900.32

Therefore, the investment of $705.46 grows to $900.32 in two years:

$705.46 (1 + r)2 = $900.32 r = 0.1297 = 12.97%

e. Coupon interest received in first year: $50.00

Less: tax on coupon interest @ 40%: – 20.00

14-2

CHAPTER 14: BOND PRICES AND YIELDS

The year-1 cash flow can be invested at an after-tax rate of:

In two years, sell the bond for: $798.82 [n = 18; i = 7%%; PMT =

$50; FV = $1,000]

CFA PROBLEMS

1. a. A sinking fund provision requires the early redemption of a bond issue. The

b. (i) Compared to a bond without a sinking fund, the sinking fund reduces the

(ii) The company will make the same total principal payments over the life of

c. From the investor’s point of view, the key reason for demanding a sinking fund

14-3

CHAPTER 14: BOND PRICES AND YIELDS

(iii) Realized compound yield is 4.166% (semiannually), or 8.332% annual bond

equivalent yield. To obtain this value, first find the future value (FV) of reinvested

Three years from now, the bond will be selling at the par value of $1,000 because

Then find the rate (yrealized) that makes the FV of the purchase price equal to

b. Shortcomings of each measure:

(i) Current yield does not account for capital gains or losses on bonds bought at

(ii) Yield to maturity assumes the bond is held until maturity and that all coupon

(iii) Realized compound yield is affected by the forecast of reinvestment rates,

3.a. The maturity of each bond is 10 years, and we assume that coupons are paid

The price of the Colina bond will increase, but only to the call price of 102. The

b. If rates are expected to fall, the Sentinal bond is more attractive: since it is not

subject to call, its potential capital gains are greater.

If rates are expected to rise, Colina is a relatively better investment. Its higher

14-4

CHAPTER 14: BOND PRICES AND YIELDS

c. An increase in the volatility of rates will increase the value of the firm’s option

to call back the Colina bond. If rates go down, the firm can call the bond, which

Conversion premium = Bond price – Market conversion value

5. a. The call feature requires the firm to offer a higher coupon (or higher promised

yield to maturity) on the bond in order to compensate the investor for the firm’s

b. The call feature reduces the expected life of the bond. If interest rates fall

substantially so that the likelihood of a call increases, investors will treat the

c. The advantage of a callable bond is the higher coupon (and higher promised

yield to maturity) when the bond is issued. If the bond is never called, then an

investor earns a higher realized compound yield on a callable bond issued at par

6. a. (iii)

b. (iii) The yield to maturity on the callable bond must compensate the

investor for the risk of call.

Choice (i) is wrong because, although the owner of a callable bond

14-5

CHAPTER 14: BOND PRICES AND YIELDS

c. (iii)

d. (ii)

14-6