Chapter 21: International Financial Management

21-2. Solution:

One dollar is worth 2.929 Polish zloty ($1/0.3414) and one

British pound is worth 1.4973 dollars.

3. Purchasing power theory (LO21-2) From the base price level of 100 in 1979, Saudi

Arabian and U.S. price levels in 2008 stood at 200 and 410, respectively. If the 1979 $/riyal

exchange rate was $0.26/riyal, what should the exchange rate be in 2008? Suggestion:

Using purchasing power parity, adjust the exchange rate to compensate for inflation. That

is, determine the relative rate of inflation between the United States and Saudi Arabia and

multiply this times $/riyal of 0.26.

21-3. Solution:

$/riyal = $.26 in 1979

The value of the Saudi Arabian riyal to the dollar will rise in

4. Continuation of Purchasing power theory (LO21-2) From the base price level of 100 in

1981, Saudi Arabian and U.S. price levels in 2010 stood at 250 and 100, respectively.

Assume the 1981 $/riyal exchange rate was $.46/riyal. Suggestion: Using the purchasing

power parity, adjust the exchange rate to compensate for inflation. That is, determine the

relative rate of inflation between the United States and Saudi Arabia and multiply this times

$/riyal of .46. What should the exchange rate be in 2010?

21-4. Solution:

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

$/riyal = $.46 in 1981

United States 100

Comparative rate of inflation 0.4

Saudi Arabia 250

= = =

This is what the riyal should be if the purchasing power parity

theory holds.

5. Adjusting returns for exchange rates (LO21-2) An investor in the United States bought a

one-year Brazilian security valued at 195,000 Brazilian reals. The U.S. dollar equivalent

was 100,000. The Brazilian security earned 16 percent during the year, but the Brazilian

real depreciated 5 cents against the U.S. dollar during the time period ($0.51 to $0.46).

After transferring the funds back to the United States, what was the investor’s return on her

$100,000? Determine the total ending value of the Brazilian investment in Brazilian reals

and then translate this Brazilian value to U.S. dollars. Afterward, compute the return on the

$100,000.

21-5. Solution:

Initial value × (1 + Interest rate)

195,000 × 1.16 = 226,200 Brazilian reals

6. Adjusting returns for exchange rates (LO21-2) A Peruvian investor buys 150 shares of

a U.S. stock for $7,500 ($50 per share). Over the course of a year, the stock goes up by $4 per

share.

a. If there is a 10 percent gain in the value of the dollar versus the nuevo sol, what will be

the total percentage return to the Peruvian investor? First, determine the new dollar

value of the investment and multiply this figure by 1.10. Divide this answer by $7,500

and get a percentage value, and then subtract 100 percent to get the percentage return.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

b. Instead assume that the stock increases by $7, but that the dollar decreases by 10

percent versus the nuevo sol. What will be the total percentage return to the Peruvian

investor? Use 0.90 in place of 1.10 in this case.

21-6. Solution:

8,910 1.1880 1 18.80 %

7,500 = – =

7,695 1.0260 1

7,500

r= = +

7. Hedging exchange rate risk (LO21-3) You are the vice president of finance for Exploratory

Resources, headquartered in Houston, Texas. In January 20X1, your firm’s Canadian

subsidiary obtained a six-month loan of 150,000 Canadian dollars from a bank in Houston to

finance the acquisition of a titanium mine in the province of Quebec. The loan will also be

repaid in Canadian dollars. At the time of the loan, the spot exchange rate was U.S.

$.8995/Canadian dollar and the Canadian currency was selling at a discount in the forward

market. The June 20X1 contract (face value = C$150,000 per contract) was quoted at U.S.

$0.8930/Canadian dollar.

a. Explain how the Houston bank could lose on this transaction assuming no hedging.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

b. If the bank does hedge with the forward contract, what is the maximum amount it can

lose?

21-7. Solution:

a. The Houston bank has extended a loan denominated in

Canadian dollars and will be repaid in Canadian dollars. If

b. If the bank hedges by buying Canadian dollars now for

Problem

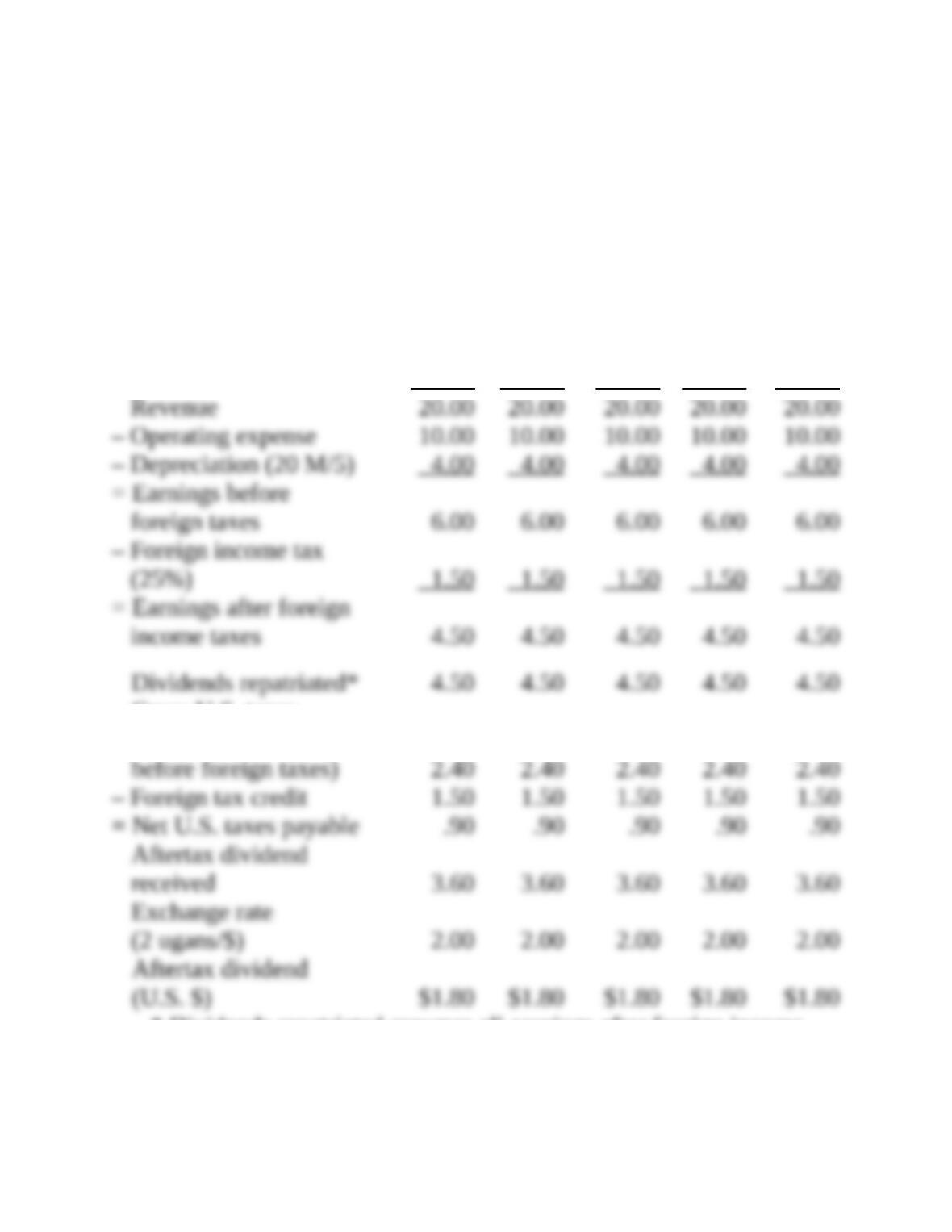

21A-1. Cash flow analysis with a foreign investment (LO21-2) The Office Automation

Corporation is considering a foreign investment. The initial cash outlay will be

$10 million. The current foreign exchange rate is 2 ugans = $1. Thus the investment in

foreign currency will be 20 million ugans. The assets have a useful life of five years

and no expected salvage value. The firm uses a straight-line method of depreciation.

Sales are expected to be 20 million ugans and operating cash expenses 10 million ugans

every year for five years. The foreign income tax rate is 25 percent. The foreign

subsidiary will repatriate all aftertax profits to Office Automation in the form of

dividends. Furthermore, the depreciation cash flows (equal to each year’s depreciation)

will be repatriated during the same year they accrue to the foreign subsidiary. The

applicable cost of capital that reflects the riskiness of the cash flows is 16 percent. The

U.S. tax rate is 40 percent of foreign earnings before taxes.

a. Should the Office Automation Corporation undertake the investment if the foreign

exchange rate is expected to remain constant during the five-year period?

b. Should Office Automation undertake the investment if the foreign exchange rate is

expected to be as follows:

Year 0……………………………. $1 = 2.0 ugans

Year 1……………………………. $1 = 2.2 ugans

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

Year 2……………………………. $1 = 2.4 ugans

Year 3……………………………. $1 = 2.7 ugans

Year 4……………………………. $1 = 2.9 ugans

Year 5……………………………. $1 = 3.2 ugans

21A-1. Solution:

The Office Automation Corporation

(Values in millions of ugans)

a.

Year 1 Year 2 Year 3 Year 4 Year 5

Gross U.S. taxes

(40% of earnings

* Dividends repatriated assumes all earnings after foreign income

taxes will be repatriated.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

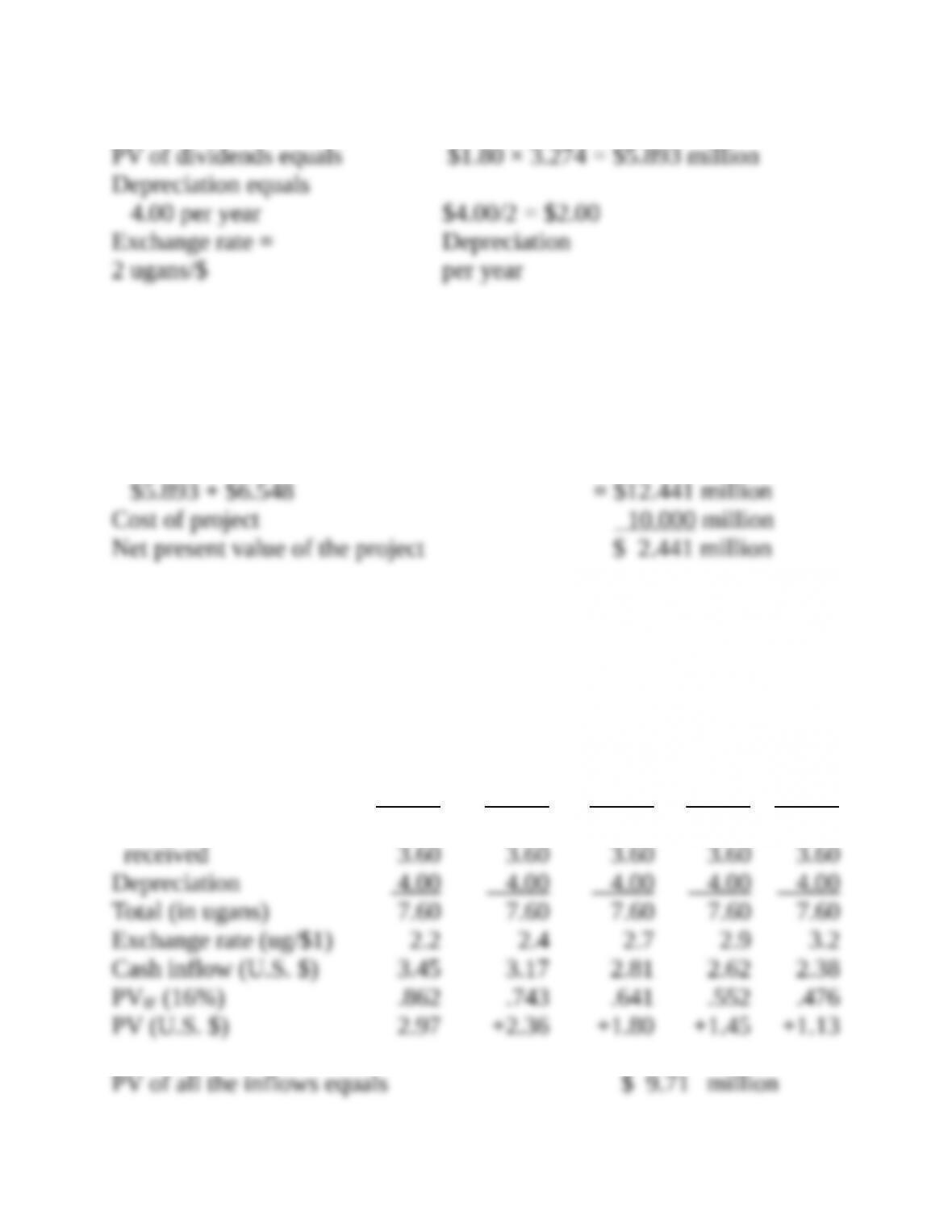

PVIFA (16% for 5 years) 3.274

PV of depreciation

equals $2.00 × 3.274 = $6.548 million

The PV of all the cash inflows equals

Since NPV is positive, accept the project!

b. The change in foreign exchange values must be applied to both

aftertax dividends received (in ugans) and depreciation (in ugans).

(in millions)

Year 1 Year 2 Year 3 Year 4 Year 5

Aftertax dividend

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 21: International Financial Management

On a purely economic basis, the investment should now be rejected.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.