Chapter 20 – External Growth through Mergers

20-6 Solution:

Noble Corporation and Barnes Enterprises

(approach similar to Table 20–3)

New earnings per share for Barnes Enterprises

$7,440,000 $2.15

3,460,000

= =

b. Earnings per share of Barnes Enterprises increased because it

has a higher P/E ratio than Noble Corporation (20x versus

29x). Any time a firm acquires another company at a lower

P/E ratio than its own, there is an immediate increase in

postmerger earnings per share.

c. Although earnings per share for Barnes Enterprises went up,

we can not automatically assume the firm is better off. We

need to know whether Noble Corporation will increase or

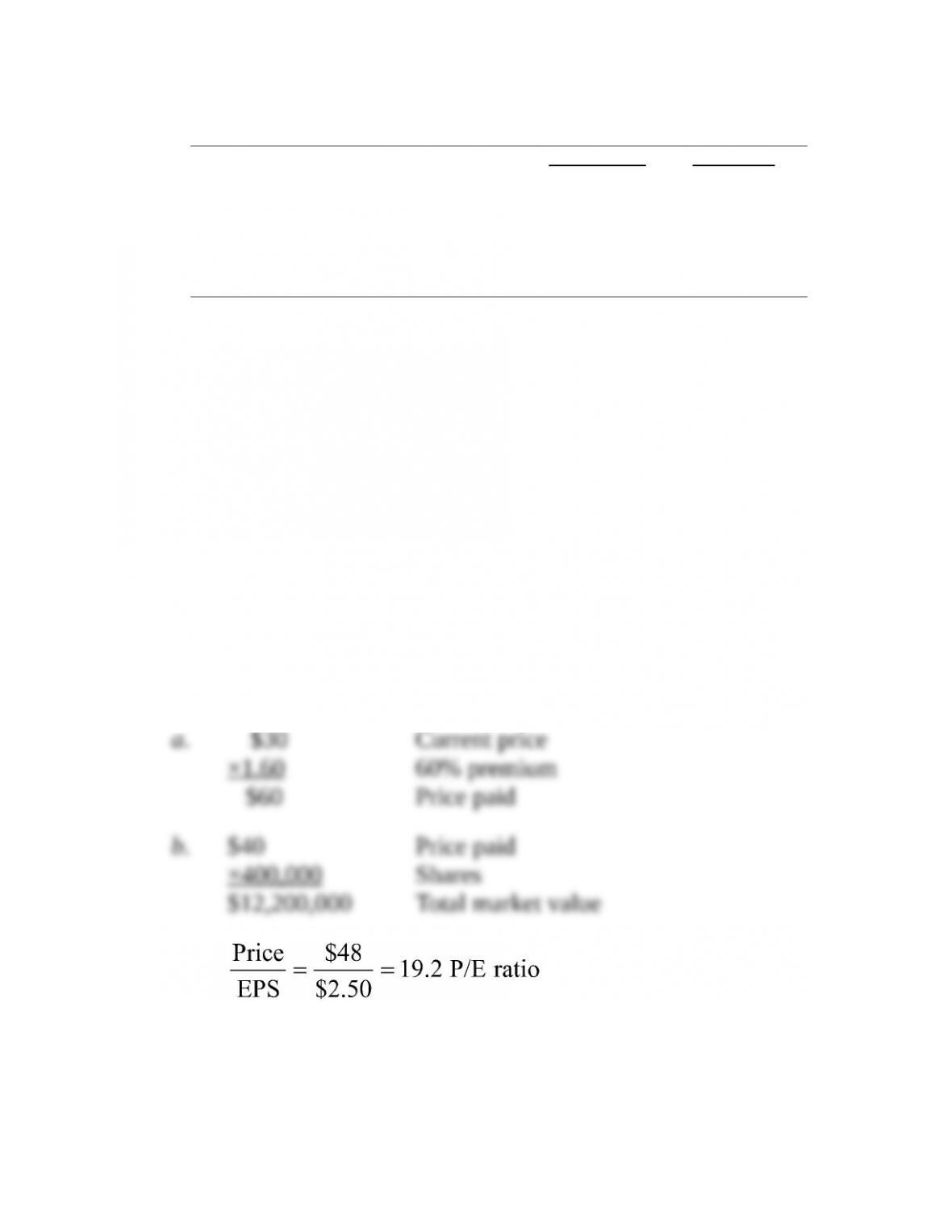

7. Mergers and dilution (LO20-3) The Jeter Corporation is considering acquiring the A-Rod

Corporation.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

The data for the two companies are as follows:

A-Rod Corp. Jeter Corp.

Total earnings…………………………………..….…. $1,000,000 $4,000,00

0

Number of shares of stock outstanding………. 400,000 2,000,000

Earnings per share………………………………..…. $2.50 $2.00

Price-earnings ratio (P/E)…………………………. 12 15

Market price per share……….….…….….…….… $30 $30

a. The Jeter Corp. is going to give A-Rod Corp. a 60 percent premium over A-Rod’s

current market value. What price will it pay?

b. At the price computed in part a, what is the total market value of A-Rod Corp.?

(Use the number of A-Rod Corp. shares times price.)

c. At the price computed in part a, what is the P/E ratio Jeter Corp. is assigning

A-Rod Corp?

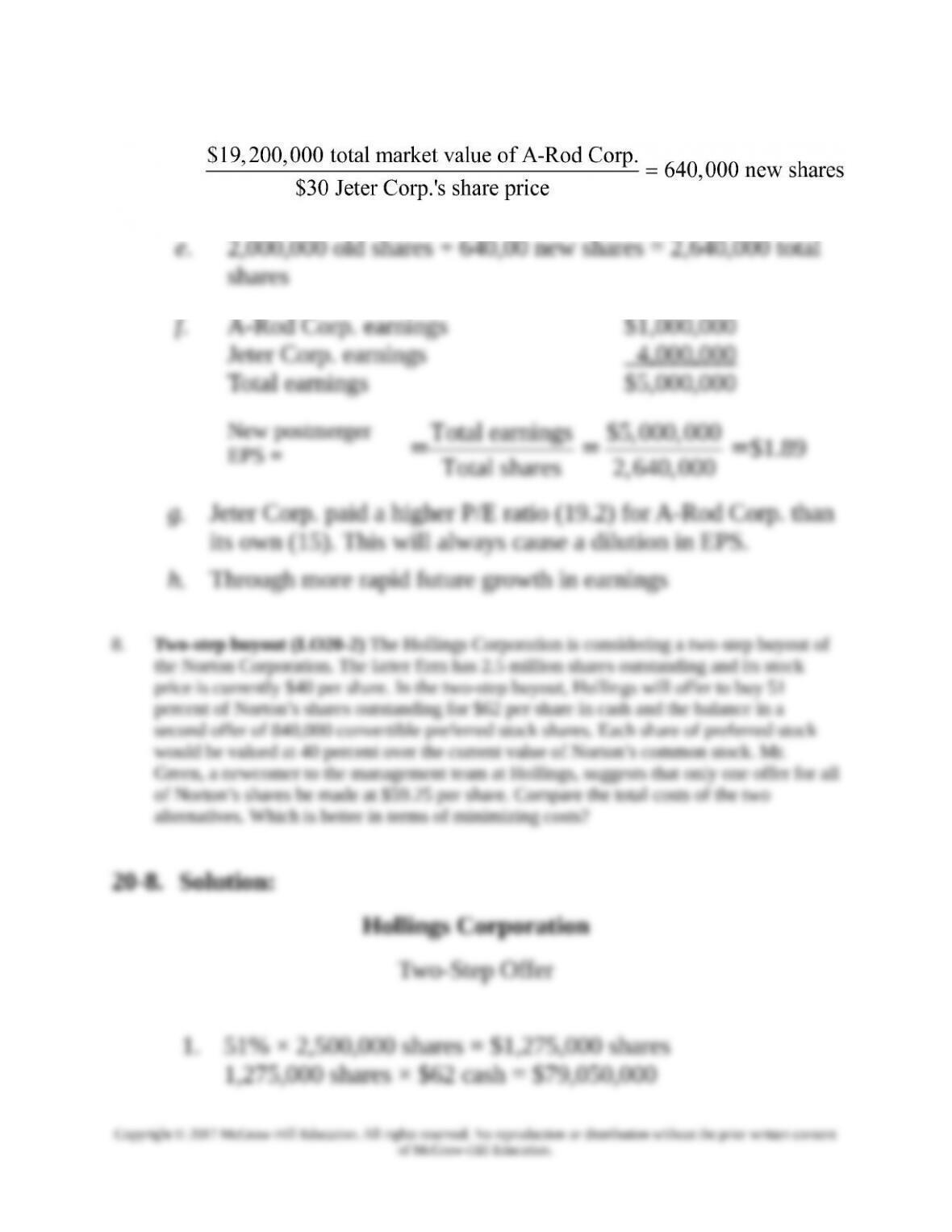

d. How many shares must Jeter Corp. issue to buy the A-Rod Corp. at the total value

computed in part b? (Keep in mind that Jeter Corp.’s price per share is $30.)

e. Given the answer to part d, how many shares will Jeter Corp. have after the merger?

f. Add together the total earnings of both corporations and divide by the total shares

computed in part e. What are the new postmerger earnings per share?

g. Why has Jeter Corp.’s earnings per share gone down?

h. How can Jeter Corp. hope to overcome this dilution?

20-7 Solution:

Jeter Corp. A-Rod Corp.

c.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

d.

Chapter 20 – External Growth through Mergers

2. 840,000 shares of convertible preferred stock ×

Single Offer

9. Future tax obligation to selling stockholder (LO20-1) Al Simpson helped start Excel

Systems several years ago. At the time, he purchased 116,000 shares of stock at $1 per

share. Now he has the opportunity to sell his interest in the company to Folsom Corp. for

$50 a share in cash. His capital gains tax rate would be 15 percent.

a. If he sells his interest, what will be the value for before-tax profit, taxes, and aftertax

profit?

b. Assume, instead of cash, he accepts Folsom Corp. stock valued at $50 per share. He

pays no tax at that time. He holds the stock for five years and then sells it for $82.50

(the stock pays no cash dividends). What will be the value for before-tax profit, taxes,

and aftertax profit in 2020? His capital gains tax is once again 15 percent.

c. Using a 9 percent discount rate, calculate the aftertax profit. That is, discount back the

answer in part b for five years and compare it to the answer in part a.

20-9 Solution:

Excel Systems

b. Sales amount 116,000 shares × $82.50 $9,570,000

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

c. Discount back $8,035,900 for five years at 9 percent.

This value of $5,223,335 clearly exceeds the value in part (a)

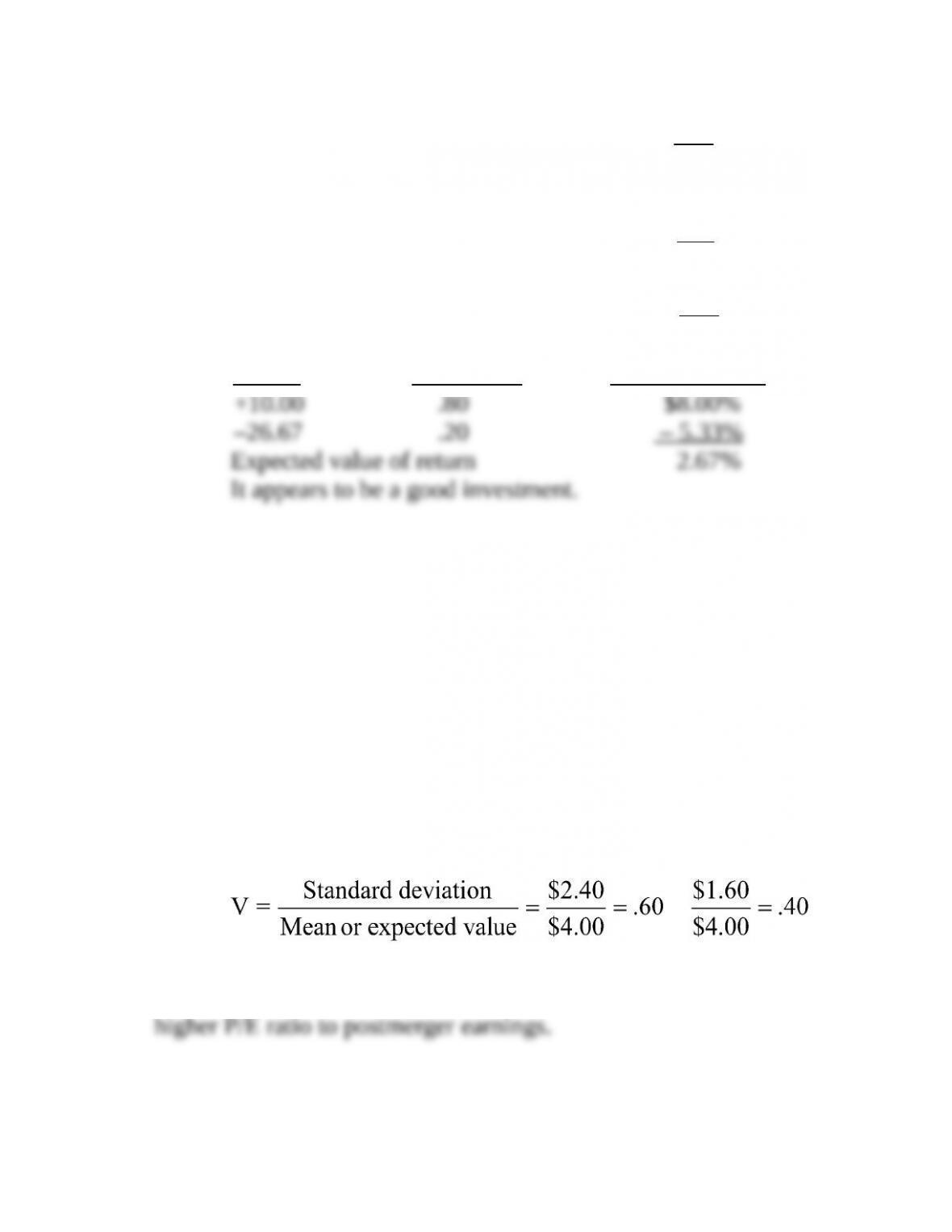

10. Premium offers and stock price movement (LO20-1) Chicago Savings Corp. is planning

to make an offer for Ernie’s Bank & Trust. The stock of Ernie’s Bank & Trust is currently

selling for $44 a share.

a. If the tender offer is planned at a premium of 50 percent over market price, what will be

the value offered per share for Ernie’s Bank & Trust?

b. Suppose before the offer is actually announced, the stock price of Ernie’s Bank & Trust

goes to $60 because of strong merger rumors. If you buy the stock at that price and the

merger goes through (at the price computed in part a), what will be your percentage gain?

c. Because there is always the possibility that the merger could be called off after it is

announced, you also want to consider your percentage loss if that happens. Assume you

buy the stock at $60 and it falls back to its original value after the merger cancellation.

What will be your percentage loss?

d. If there is an 80 percent probability that the merger will go through when you buy the

stock at $60 and only a 20 percent chance that it will be called off, does this appear to

be a good investment? Compute the expected value of the return on the investment.

20-10.Solution:

Chicago Savings Corp.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

Percentage gain

$ 6 10.00%

$60 =

c. Value after cancellation (original value) $44

Purchase price 60

Loss $16

Percentage loss

$16 26.67%

$60 =

d. Return Probability Expected Value

11. Portfolio effect of a merger (LO20-4) Assume the Knight Corporation is considering the

acquisition of Day Inc. The expected earnings per share for the Knight Corporation will be

$4.00 with or without the merger. However, the standard deviation of the earnings will go

from $2.40 to $1.60 with the merger because the two firms are negatively correlated.

a. Compute the coefficient of variation for the Knight Corporation before and after the

merger (consult Chapter 13 to review statistical concepts if necessary).

b. Discuss the possible impact on Knight’s postmerger P/E ratio, assuming investors are

risk-averse.

20-11. Solution:

Knight Corporation

a. Premerger Postmerger

b. Risk-averse investors are being offered less risk and may assign a

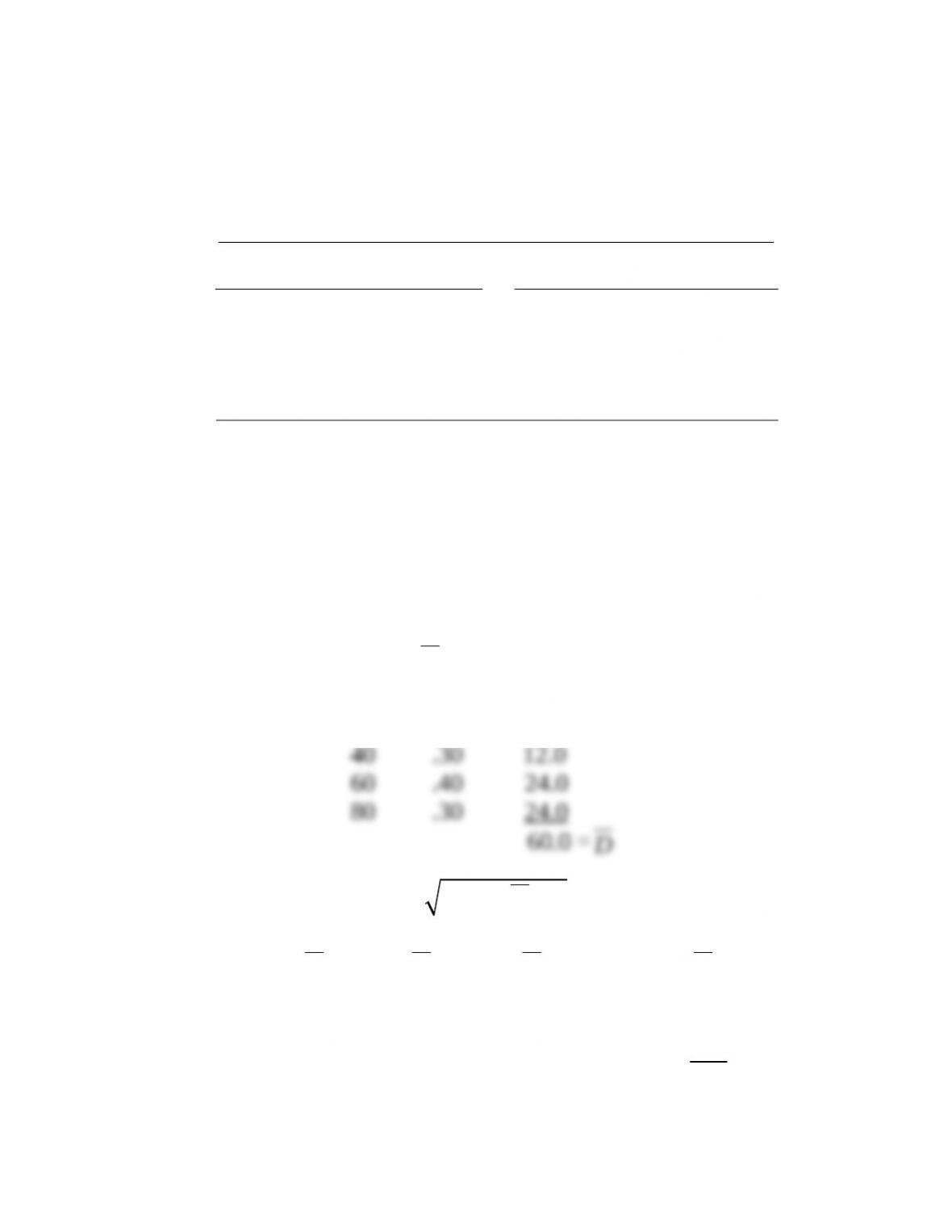

12. Portfolio consideration and risk aversion (LO20-4) General Meters is considering two

mergers. The first is with Firm A in its own volatile industry, the auto speedometer industry,

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

while the second is a merger with Firm B in an industry that moves in the opposite

direction (and will tend to level out performance due to negative correlation).

a Compute the mean, standard deviation, and coefficient of variation for both investments

(refer to Chapter 13 if necessary).

General Meters Merger General Meters Merger

with Firm A with Firm B

Possible Possible

Earnings Earnings

($ in millions) Probability ($ millions) Probability

$40…………………… .30 $40…………...... .25

60………….…….…. .40 60…............... .50

80…………..…….…. .30 80…............... .25

b. Assuming investors are risk-averse, which alternative can be expected to bring the

higher valuation?

20-12.Solution:

General Meters

a. Merger with A (answer in millions of dollars)

D DP=å

D P DP

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 20 – External Growth through Mergers

240 15.49 s= =

Coefficient of Variation =

15.49 .258

60

D

s= =

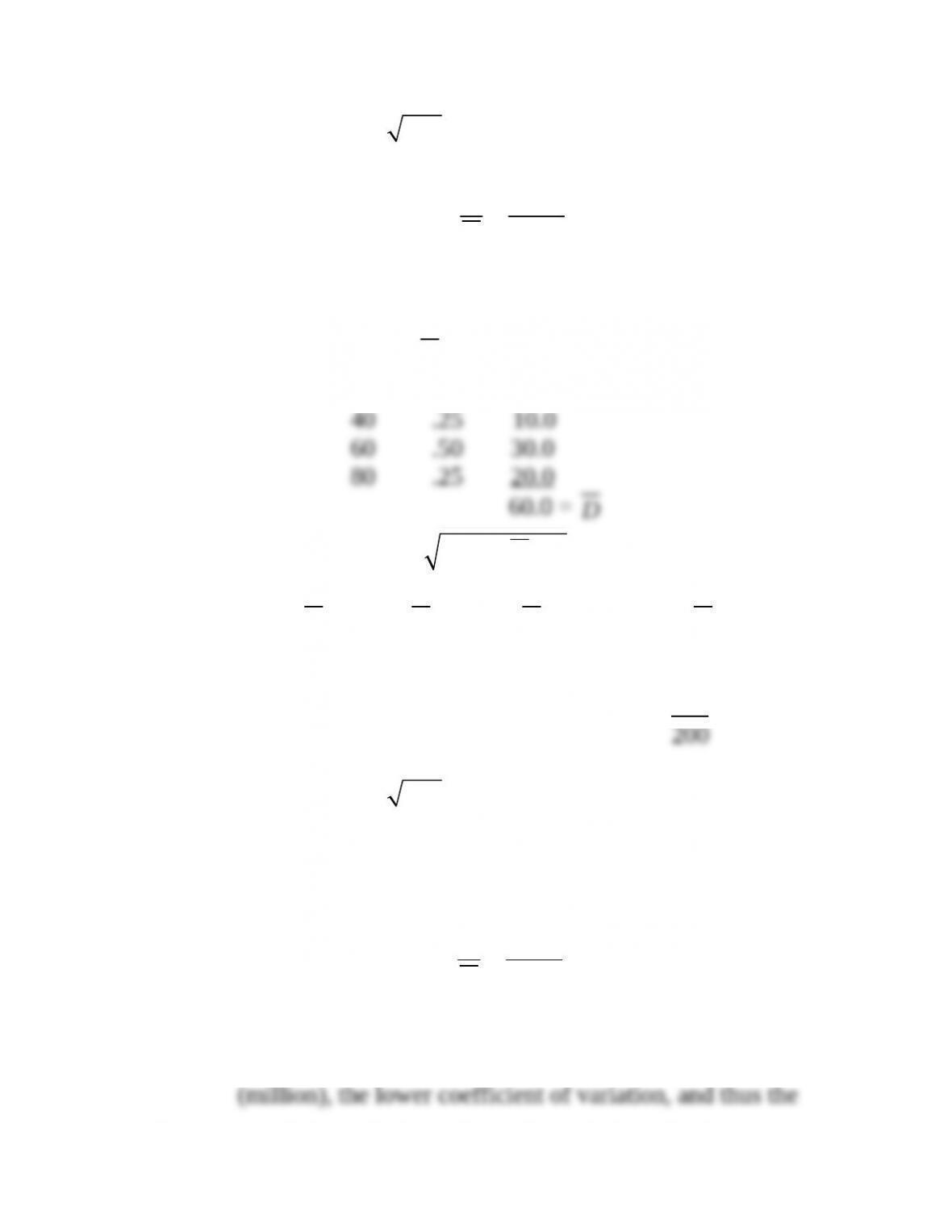

Merger with B (answer in millions of dollars)

D DP=å

D P DP

2

( )D D Ps= å –

D

D

(D –

D

) (D –

D

)2P(D –

D

)2P

40 60 –20 400 .25 100

60 60 0 0 .50 0

80 60 +20 400 .25 100

200

200 14.14 s= =

20-12. (Continued)

Coefficient of variation =

14.14 .236

60

D

s= =

b. Though both alternatives have an expected value of $50

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

D

Chapter 20 – External Growth through Mergers

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.