CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

PROBLEM SETS

1. (a) and (e). Short-term rates and labor issues are factors that are common to all

2. (a) and (c). After real estate is added to the portfolio, there are four asset classes in

the portfolio: stocks, bonds, cash, and real estate. Portfolio variance now includes a

4. The parameters of the opportunity set are:

From the standard deviations and the correlation coefficient we generate the

covariance matrix [note that

( , )

S B S B

Cov r r r s s= ´ ´

]:

Bonds Stocks

Bonds

225

45

Stocks 45 900

The minimum-variance portfolio is computed as follows:

wMin(S) =

1739.0

)452(225900

45225

)(Cov2

)(Cov

22

2

BSBS

BSB

,rr

,rr

The minimum variance portfolio mean and standard deviation are:

7-1

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

σ

Min =

2/12222

)],(Cov2[

BSBSBBSS

rrwwww

5.

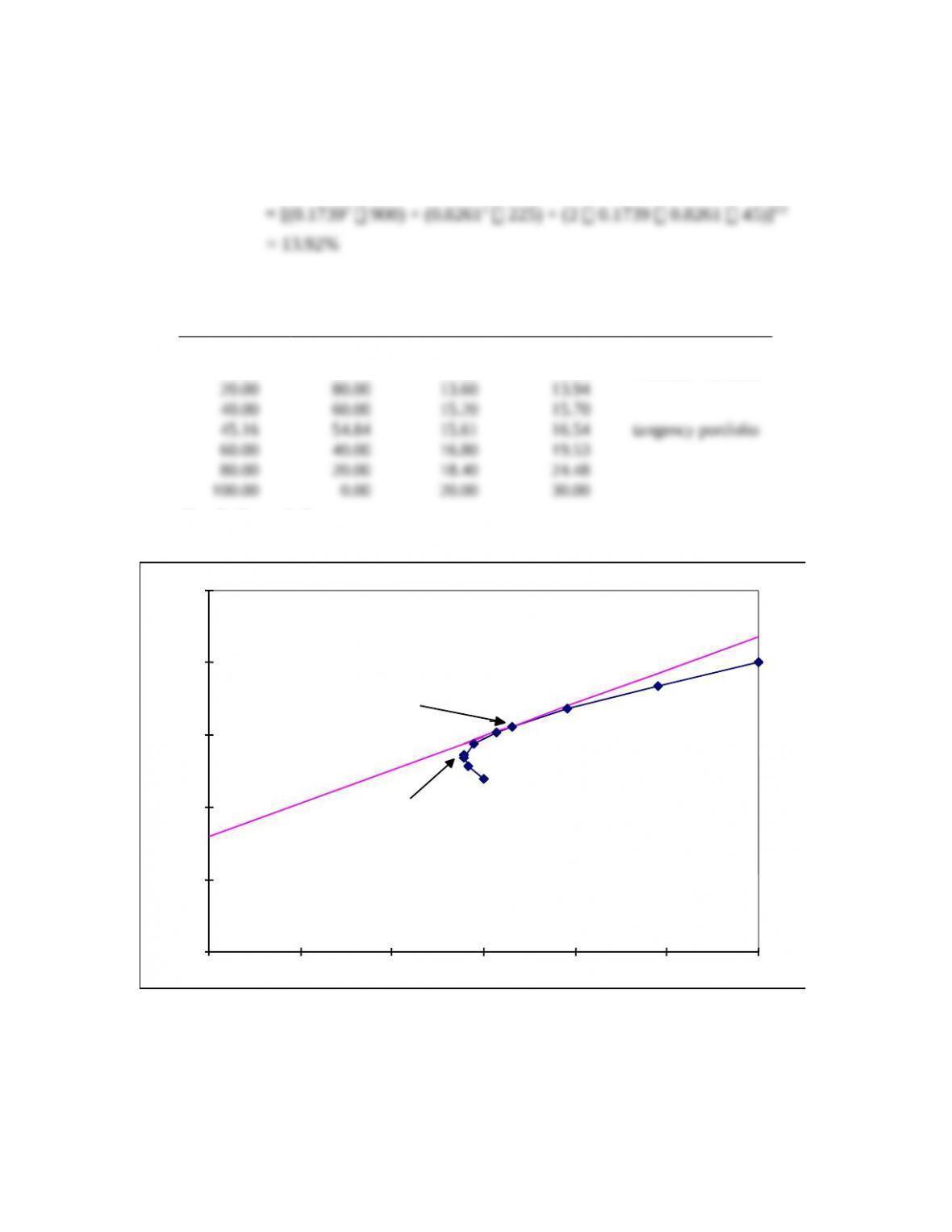

Proportion

in Stock Fund

Proportion

in Bond Fund

Expected

Return

Standard

Deviation

0.00% 100.00% 12.00% 15.00%

17.39 82.61 13.39 13.92 minimum variance

Graph shown below.

0.00

5.00

10.00

15.00

20.00

25.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Tangency

Portfolio

Minimum

Variance

Portfolio

Efficient frontier

of risky assets

CML

INVESTMENT OPPORTUNITY SET

rf = 8.00

6. The above graph indicates that the optimal portfolio is the tangency portfolio with

expected return approximately 15.6% and standard deviation approximately 16.5%.

7-2

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

7-3

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

7. The proportion of the optimal risky portfolio invested in the stock fund is given by:

2

2 2

[ ( ) ] [ ( ) ] ( , )

[ ( ) ] [ ( ) ] [ ( ) ( ) ] ( , )

S f B B f S B

S

S f B B f S S f B f S B

E r r E r r Cov r r

wE r r E r r E r r E r r Cov r r

s

s s

– ´ – – ´

=– ´ + – ´ – – + – ´

[(.20 .08) 225] [(.12 .08) 45] 0.4516

[(.20 .08) 225] [(.12 .08) 900] [(.20 .08 .12 .08) 45]

– ´ – – ´

= =

– ´ + – ´ – – + – ´

1 0.4516 0.5484

B

w= – =

The mean and standard deviation of the optimal risky portfolio are:

8. The reward-to-volatility ratio of the optimal CAL is:

( ) .1561 .08 0.4601

.1654

p f

p

E r r

s

––

= =

9. a. If you require that your portfolio yield an expected return of 14%, then you

can find the corresponding standard deviation from the optimal CAL. The

equation for this CAL is:

( )

( ) .08 0.4601

p f

C f C C

P

E r r

E r r s s

s

–

= + = +

If E(rC) is equal to 14%, then the standard deviation of the portfolio is

13.04%.

b. To find the proportion invested in the T-bill fund, remember that the mean of

the complete portfolio (i.e., 14%) is an average of the T-bill rate and the

optimal combination of stocks and bonds (P). Let y be the proportion invested

in the portfolio P. The mean of any portfolio along the optimal CAL is:

( ) (1 ) ( ) [ ( ) ] .08 (.1561 .08)

C f P f P f

E r y r y E r r y E r r y= – ´ + ´ = + ´ – = + ´ –

Setting E(rC) = 14% we find: y = 0.7884 and (1 − y) = 0.2119 (the proportion

invested in the T-bill fund).

7-4

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

7-5

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

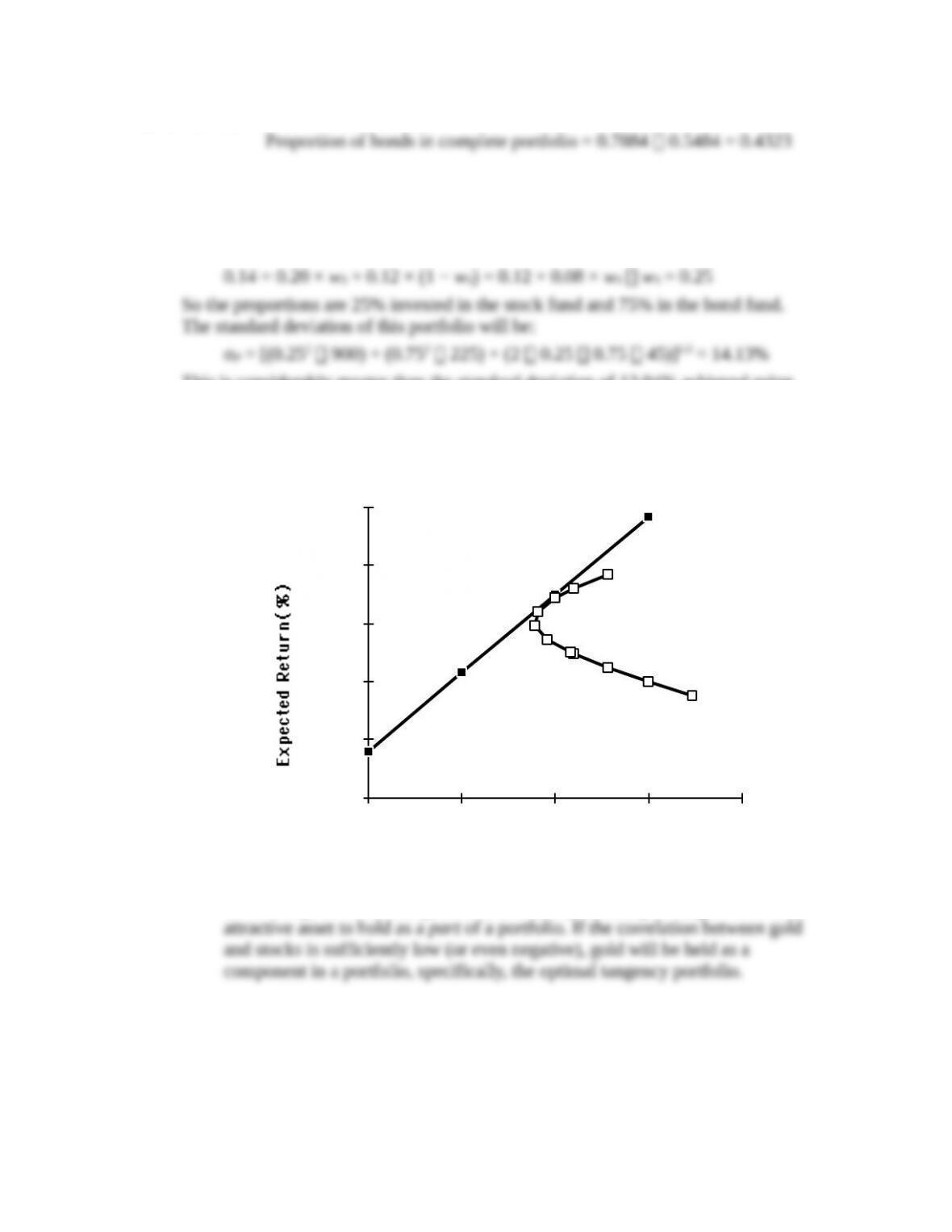

10. Using only the stock and bond funds to achieve a portfolio expected return of 14%,

we must find the appropriate proportion in the stock fund (wS) and the appropriate

proportion in the bond fund (wB = 1 − wS) as follows:

This is considerably greater than the standard deviation of 13.04% achieved using

T-bills and the optimal portfolio.

11. a.

Standar d Deviat ion(% )

0.00

5.00

10.00

15.00

20.00

25.00

0 10 20 30 40

Gold

Stocks

Optim al CAL

P

Even though it seems that gold is dominated by stocks, gold might still be an

7-6

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

b. If the correlation between gold and stocks equals +1, then no one would be

willing to hold gold: its return is lower than stocks, its standard deviation is

Standard Deviation(%)

0

5

10

15

20

25

0.00

10.00

20.00

30.00

40.00

Gold

Stocks

r

f

18

c. Of course, this situation could not be an equilibrium. As long as no one is

12. Since Stock A and Stock B are perfectly negatively correlated, a risk-free portfolio

can be created and the rate of return for this portfolio, in equilibrium, will be the

risk-free rate. To find the proportions of this portfolio [with the proportion wA

invested in Stock A and wB = (1 – wA ) invested in Stock B], set the standard

deviation equal to zero. With perfect negative correlation, the portfolio standard

deviation is:

σP = Absolute value [wAσA wBσB]

The expected rate of return for this risk-free portfolio is:

7-7

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

Therefore, the risk-free rate is: 11.667%

7-8

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

of the component-asset standard deviations. The portfolio variance is a weighted

sum of the elements in the covariance matrix, with the products of the portfolio

proportions as weights.

15. The probability distribution is:

Probability Rate of Return

7-9