24. For y to be less than 1.0 (that the investor is a lender), risk aversion (A) must be large

enough such that:

1

σ

2

M

fM

A

r)E(r

y

1.28

0.25

0.050.13

2

A

For y to be greater than 1 (the investor is a borrower), A must be small enough:

1

σ

)(

2

M

fM

A

rrE

y

0.64

0.25

0.090.13

2

A

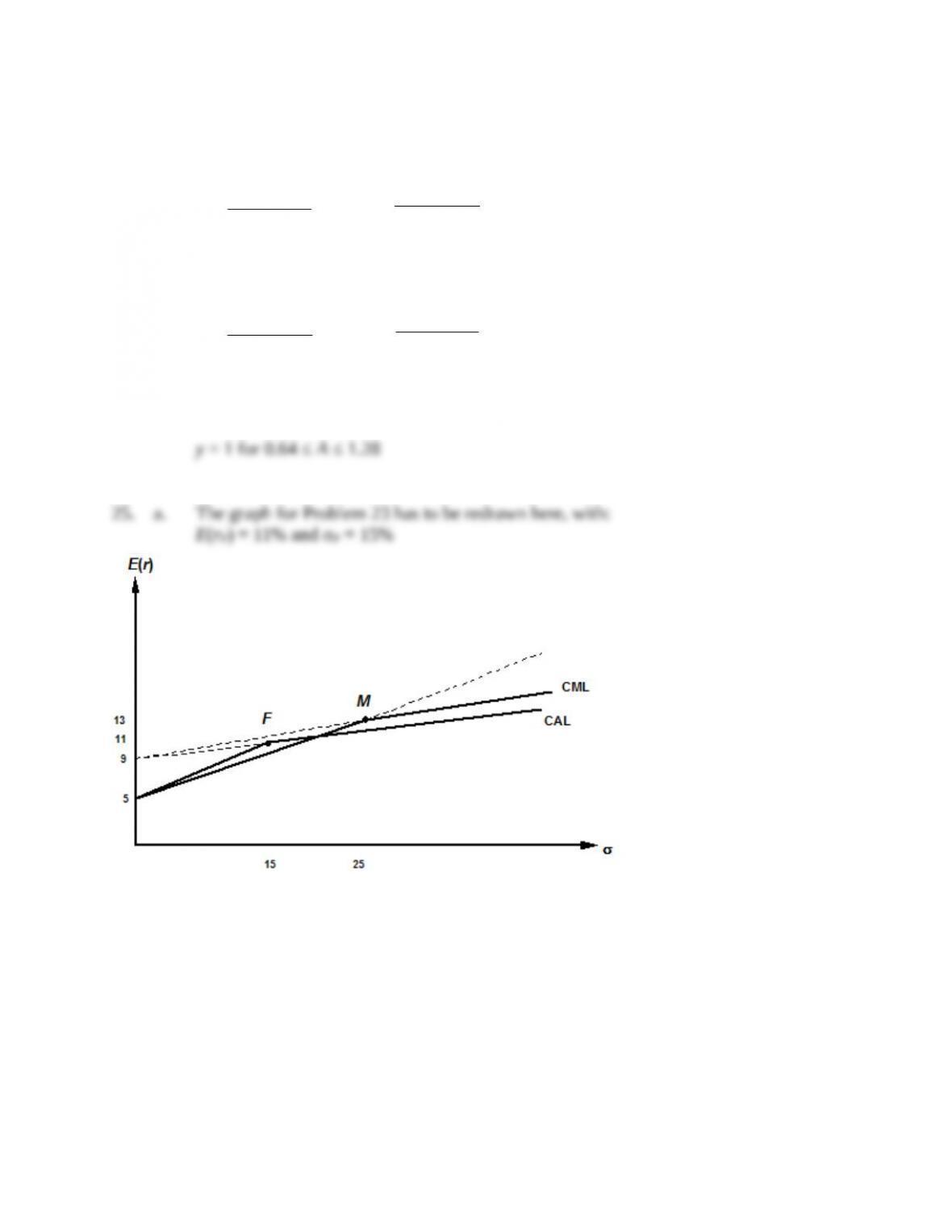

For values of risk aversion within this range, the client will neither borrow nor lend but

will hold a portfolio composed only of the optimal risky portfolio:

CML and CAL

0

2

4

6

8

10

12

14

16

18

0

10

20

30

Standard Deviation

Expected Retrun

CAL: Slope = 0.3571

CML: Slope = 0.20

b. My fund allows an investor to achieve a higher mean for any given standard deviation than would a

passive strategy, i.e., a higher expected return for any given level of risk.

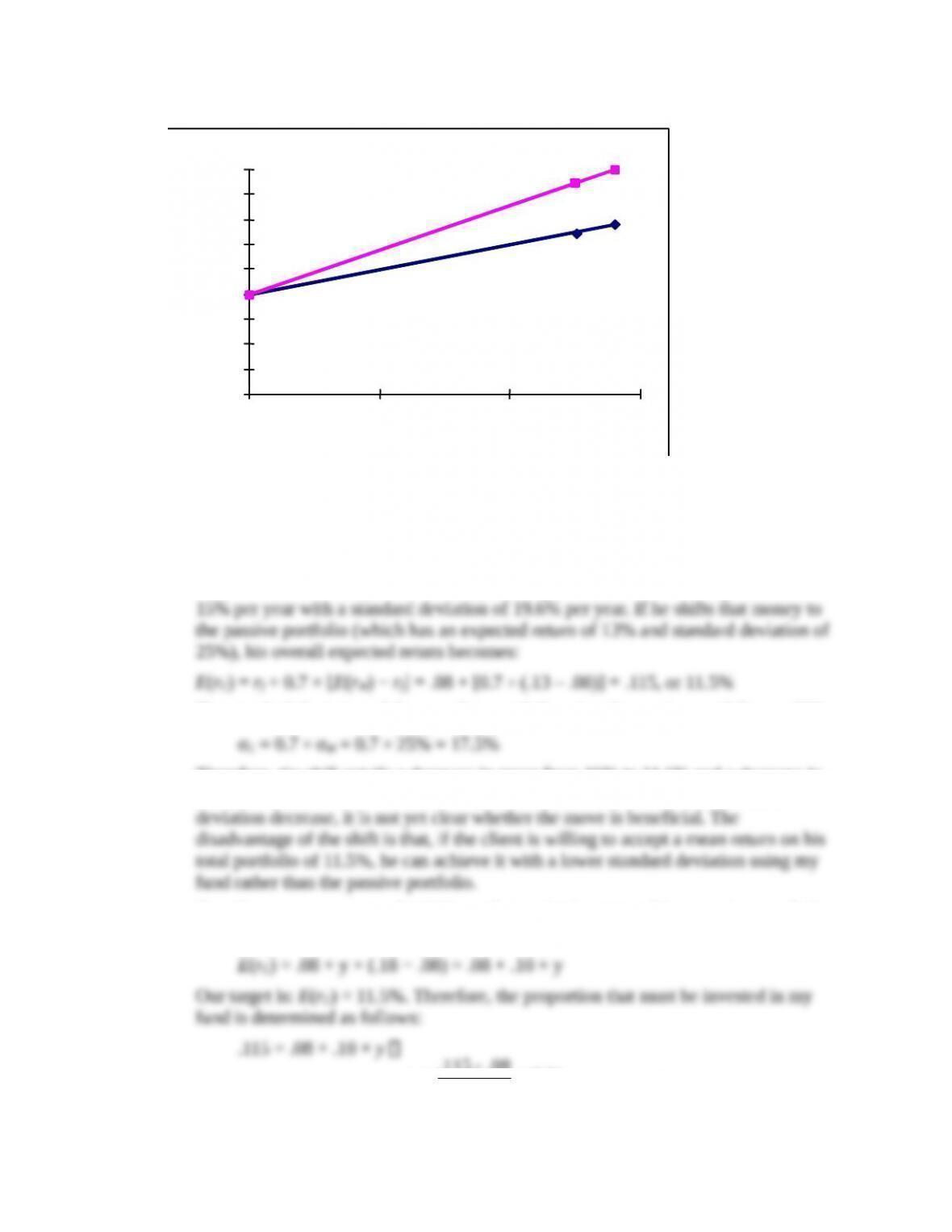

28. a. With 70% of his money invested in my fund’s portfolio, the client’s expected return is

The standard deviation of the complete portfolio using the passive portfolio would be:

Therefore, the shift entails a decrease in mean from 15% to 11.5% and a decrease in

standard deviation from 19.6% to 17.5%. Since both mean return and standard

To achieve a target mean of 11.5%, we first write the mean of the complete portfolio

as a function of the proportion invested in my fund (y):

Our target is: E(rC) = 11.5%. Therefore, the proportion that must be invested in my

fund is determined as follows:

Thus, by using my portfolio, the same 11.5% expected return can be achieved with a

the passive portfolio.

b. The fee would reduce the reward-to-volatility ratio, i.e., the slope of the CAL. The

client will be indifferent between my fund and the passive portfolio if the slope of the

b. The answer here is the same as the answer to Problem 28(b). The fee that you can

CFA PROBLEMS

1. Utility for each investment = E(r) – 0.5 × 4 × σ2

We choose the investment with the highest utility value, Investment 3.

Investment

Expected

return

E(r)

Standard

deviation

Utility

U

1

0.12

0.30

-0.0600

20.15 0.50 -0.3500

30.21 0.16 0.1588

40.24 0.21 0.1518

2. When investors are risk neutral, then A = 0; the investment with the highest utility is

Investment 4 because it has the highest expected return.

8. Expected return for equity fund = T-bill rate + Risk premium = 6% + 10% = 16%

b. With insurance coverage for the full value of the house, costing $200, end-of-year

wealth is certain, and equal to:

c. With insurance coverage for 1½ times the value of the house, the premium is $300,

Probability Wealth

No fire

0.999

$252,682

Fire

0.001

352,682

For this distribution, expected utility is computed as follows:

The certainty equivalent is:

Therefore, full insurance dominates both over- and underinsurance. Overinsuring