16-19. Solution:

The Sunbelt Corporation

First compute the discount rate

Outflows

1. Payment on call provision

2. Underwriting cost on new issue

IFA

*PV

16-19. (Continued)

Inflows

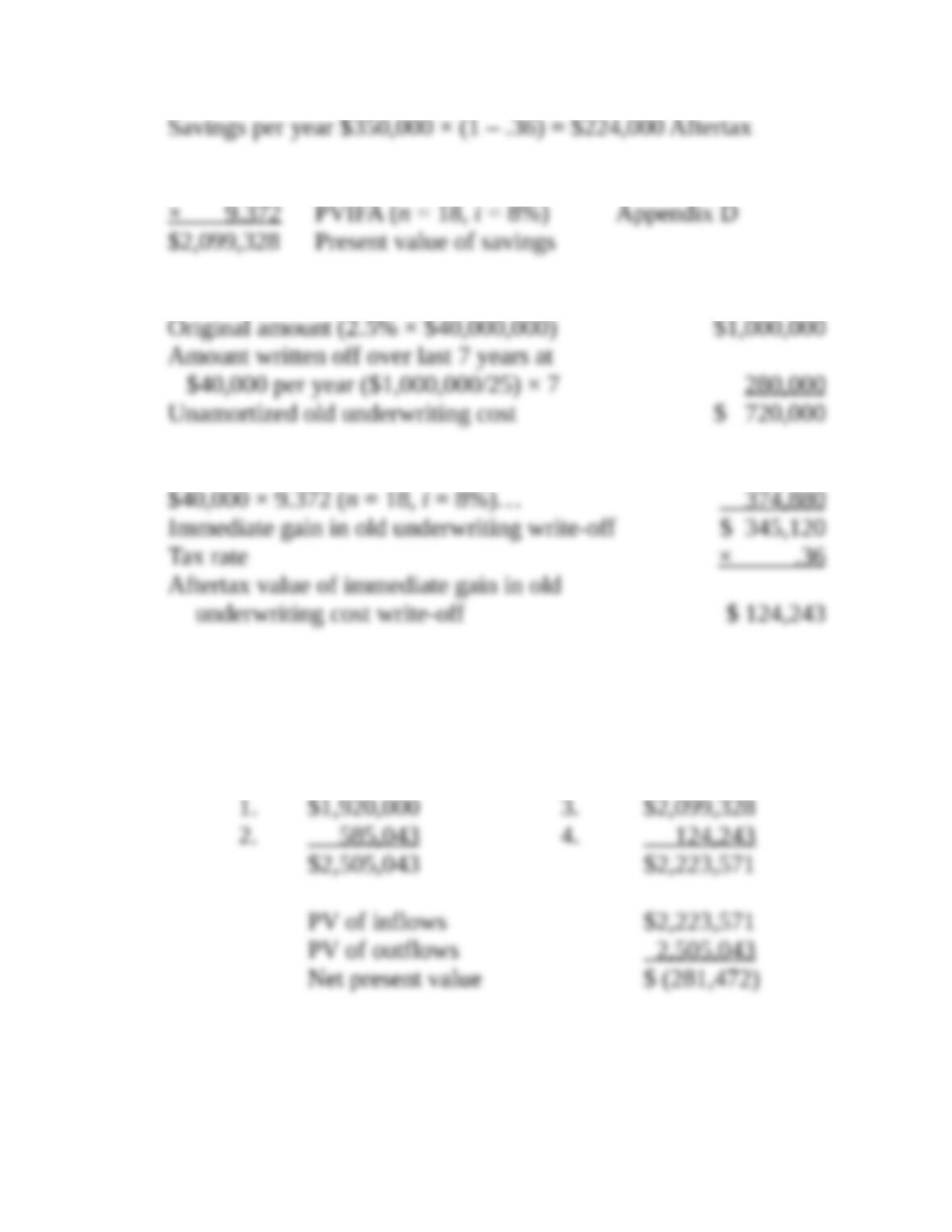

3. Cost savings in lower interest rates

$ 224,000

4. Underwriting cost on old issue

Present value of deferred future write-off:

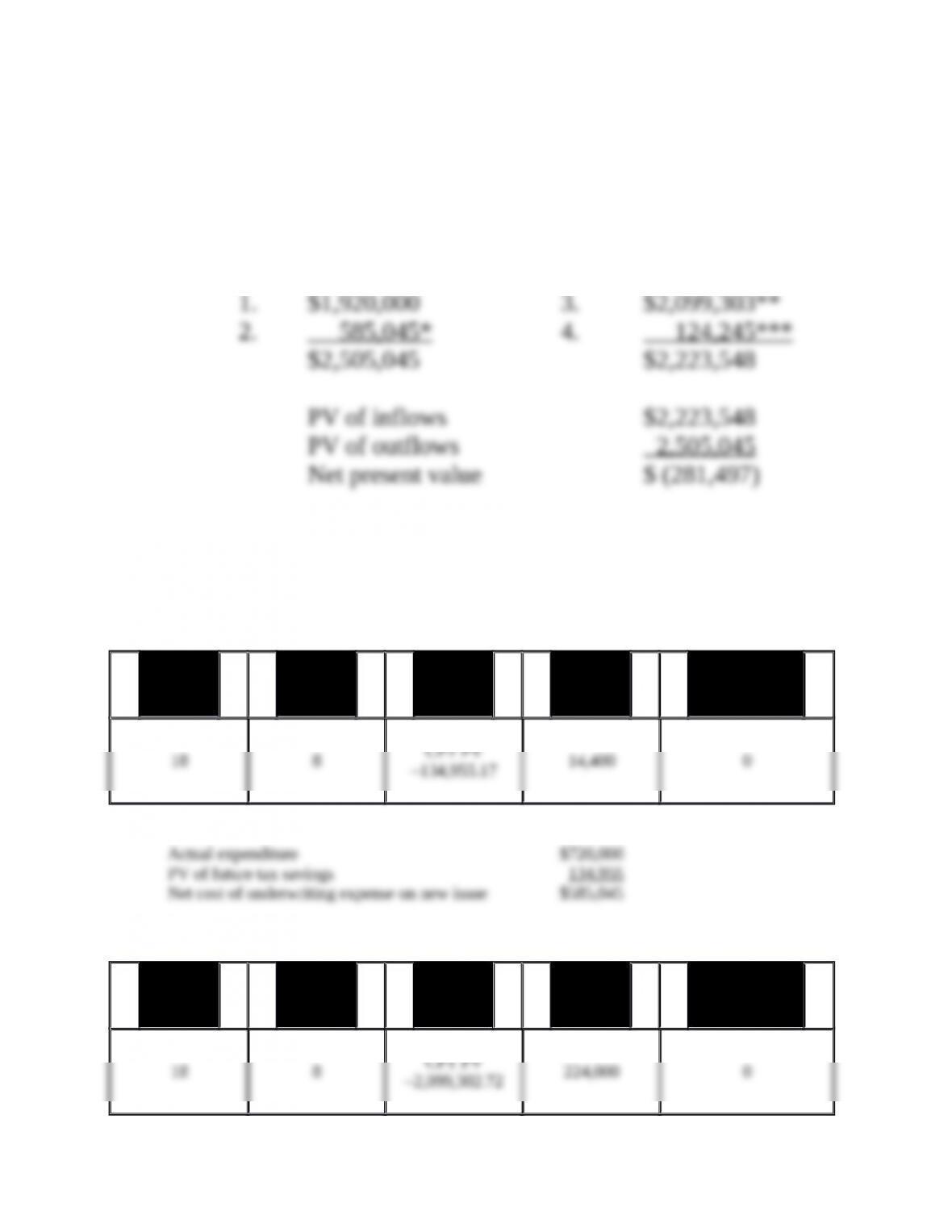

Summary

Outflows Inflows

Based on the negative net present value, the Sunbelt

Corporation should not refund the issue.

Calculator solution:

Summary

Outflows Inflows

Based on the negative net present value, the Sunbelt Corporation should

not refund the issue.

*Present value of future tax savings

N I/Y PV PMT FV

PV of future tax savings $134,955

**Present value of savings

N I/Y PV PMT FV

PV of future tax savings $2,099,303

***Present value of deferred future write-off:

N I/Y PV PMT FV

PV of deferred future write-off $374,875

20. Capital lease or operating lease (LO16-4) The Deluxe Corporation has just signed a

168-month lease on an asset with a 19-year life. The minimum lease payments are $1,300

per month ($15,600 per year) and are to be discounted back to the present at a 9 percent

annual discount rate. The estimated fair value of the property is $165,000.

a. Calculate the lease period as a percentage to the estimated life of the leased property.

b. Calculate the present value of lease payments as a percentage to the fair value of the

property.

c. Should the lease be recorded as a capital lease or an operating lease. (Use criteria 3 and

4 for a capital lease.)

16-20. Solution:

The Deluxe Corporation

The lease is less than 75 percent of the estimated life of the

leased property.

The present value of the lease payments is less than 90 percent

of the fair value of the property.

$ 15,600 Annual lease payments

Since none of the four criteria for compulsory treatment as an

Calculator solution:

Present value of lease payments

N I/Y PV PMT FV

PV of lease payments $121,464

21. Balance sheet effect of leases (LO16-4) The Ellis Corporation has heavy lease

commitments. Prior to SFAS No. 13, it merely footnoted lease obligations in the balance

sheet, which appeared as follows:

In $ millions In $ millions

Current asserts……………………………...$ 70 Current liabilities……..…….….….….….$ 30

Fixed asserts……………………………..…. 70 Long-term liabilities……………………… 30

Total liabilities…………………………..$ 60

Stockholders’ equity……………………… 80

Total assets……………………….….….…..$140

Total liabilities and

stockholders’ equity……….….….…..$140

The footnotes stated that the company had $14 million in annual capital lease obligations

for the next 20 years.

a. Discount these annual lease obligations back to the present at a 10 percent discount

rate (round to the nearest million dollars).

b. Construct a revised balance sheet that includes lease obligations, as in Table 16-8.

c. Compute total debt to total assets on the original and revised balance sheets.

d. Compute total debt to equity on the original and revised balance sheets.

e. In an efficient capital market environment, should the consequences of SFAS No. 13,

as viewed in the answers to parts c and d, change stock prices and credit ratings?

f. Comment on management’s perception of market efficiency (the viewpoint of the

financial officer).

16-21. Solution:

The Ellis Corporation

16-21. (Continued)

b. Current assets $70 million Current liabilities $ 30 million

c. Original Revised

Total debt $60 million $179 million

42.9% 69.1%

Total assets $140 million $259 million

= = =

d. Original Revised

Total debt $60 million $179 million

75.0% 223.8%

Equity $80 million $80 million

= = =

e. No, the information was already known by financial

f. Management is concerned about whether the market is as

Calculator solution:

*Present value of annual lease payments

N I/Y PV PMT FV

PV of future tax savings $119.190 million rounds to $119 million

22. Determining size of lease payment (LO16-4) The Hardaway Corporation plans to lease a

$740,000 asset to the O’Neil Corporation. The lease will be for 11 years.

a. If the Hardaway Corporation desires a 13 percent return on its investment, how much

should the lease payments be?

b. If the Hardaway Corporation is able to take a 10 percent deduction from the purchase

price of $740,000 and will pass the benefits along to the O’Neil Corporation in the

form of lower lease payments (related to the Hardaway Corporation in the form of

lower initial net cost), how much should the revised lease payments be? The

Hardaway Corporation desires a 13 percent return on the 11-year lease.

16-22. Solution:

Hardaway Corporation

a. Determine 11-year annuity that will yield 13 percent.

A IFA

A = PV / PV ( = 13%, = 11) Appendix D

$740,000

= $130,121

5.687

i n

=

b. Original amount $740,000

–10% 74,000

Net cost $666,000

$666,000

A = $117,109

5.687 =

Calculator solution:

a.

N I/Y PV PMT FV

Lease payment is equal to $130,123.

b.

N I/Y PV PMT FV

Lease payment is equal to $117,110.

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Broadband Inc. Bond prices refunding (LO16-2 and 3) Barton Simpson, the chief financial

officer of Broadband Inc. could hardly believe the change in interest rates that had taken place

over the last few months. The interest rate on A2 rated bonds was now 6 percent. The $30

million, 15-year bond issue that his firm has outstanding was initially issued at 9 percent five

years ago.

Because interest rates had gone down so much, he was considering refunding the bond issue.

The old issue had a call premium of 8 percent. The underwriting cost on the old issue had been

3 percent of par and on the new issue, it would be 5 percent of par. The tax rate would be 30

percent and a 4 percent discount rate will be applied for the refunding decision. The new bond

would have a 10-year life.

Before Barton used the 8 percent call provision to reacquire the old bonds, he wanted to make

sure he could not buy them back cheaper in the open market.

a. First compute the price of the old bonds in the open market. Use the valuation procedures for

a bond that were discussed in Chapter 10 (use the annual analysis). Determine the price of a

single $1,000 par value bond.

b. Compare the price in part a to the 8 percent call premium over par value. Which appears to

be more attractive in terms of reacquiring the old bonds?

c. Now do the standard bond refunding analysis as discussed in this chapter. Is the refunding

financially feasible?

d In terms of the refunding decision, how should Barton be influenced if he thinks interest rates

might go down even more?

CP 16-1. Solution:

a.

Broadband Inc.

Price of Old Bond

Total present value

CP16-1. (Continued)

b. The price of $1,220.40 is more than 20 percent over par. The

c. Refunding Decision

Outflows

1. Payment of call premium

2. Underwriting cost on new issue

CP16-1. (Continued)

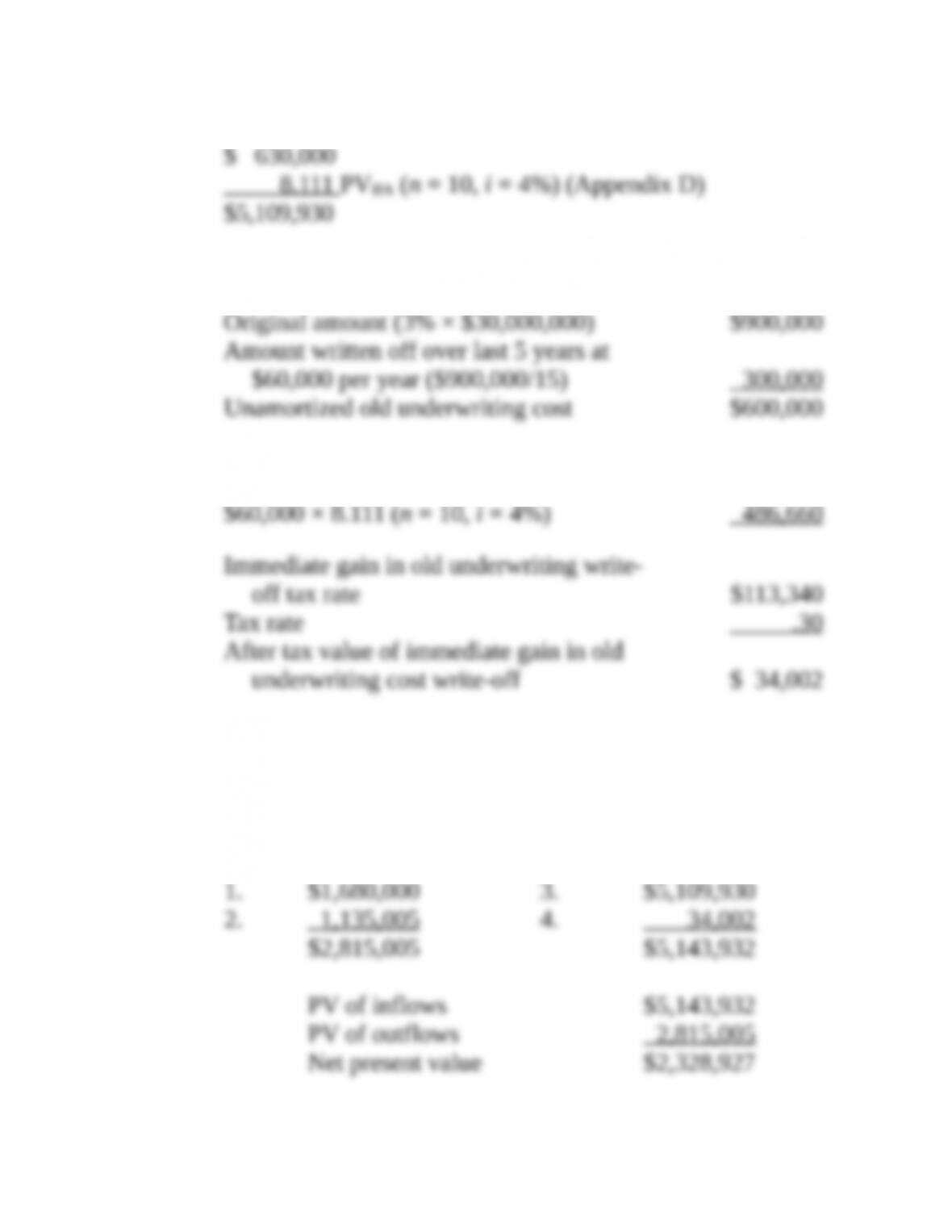

3. Cost savings in lower interest rates

Savings per year $900,000 × (1 – 30) = $630,000 after tax

4. Underwriting cost on old issue

Present value of deferred future write-off

After tax value of immediate gain in old

CP16-1. (Continued)

Summary

Outflows Inflows

The refunding is financially feasible.

d. If Barton thinks interest rates are going down even more, he

might want to wait on the refunding because the net present