Chapter 17: Common and Preferred Stock Financing

17-20. Solution:

Enterprise Storage Company

b. Stock Price

Present value of common stock dividends

PV Factor Present

Amount at 14% Value

Present value of future stock price

1. Stock price = P/E × EPS

2. PV of stock price (four years in the future)

PV Factor Present

Amount at 14% Value

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

c.

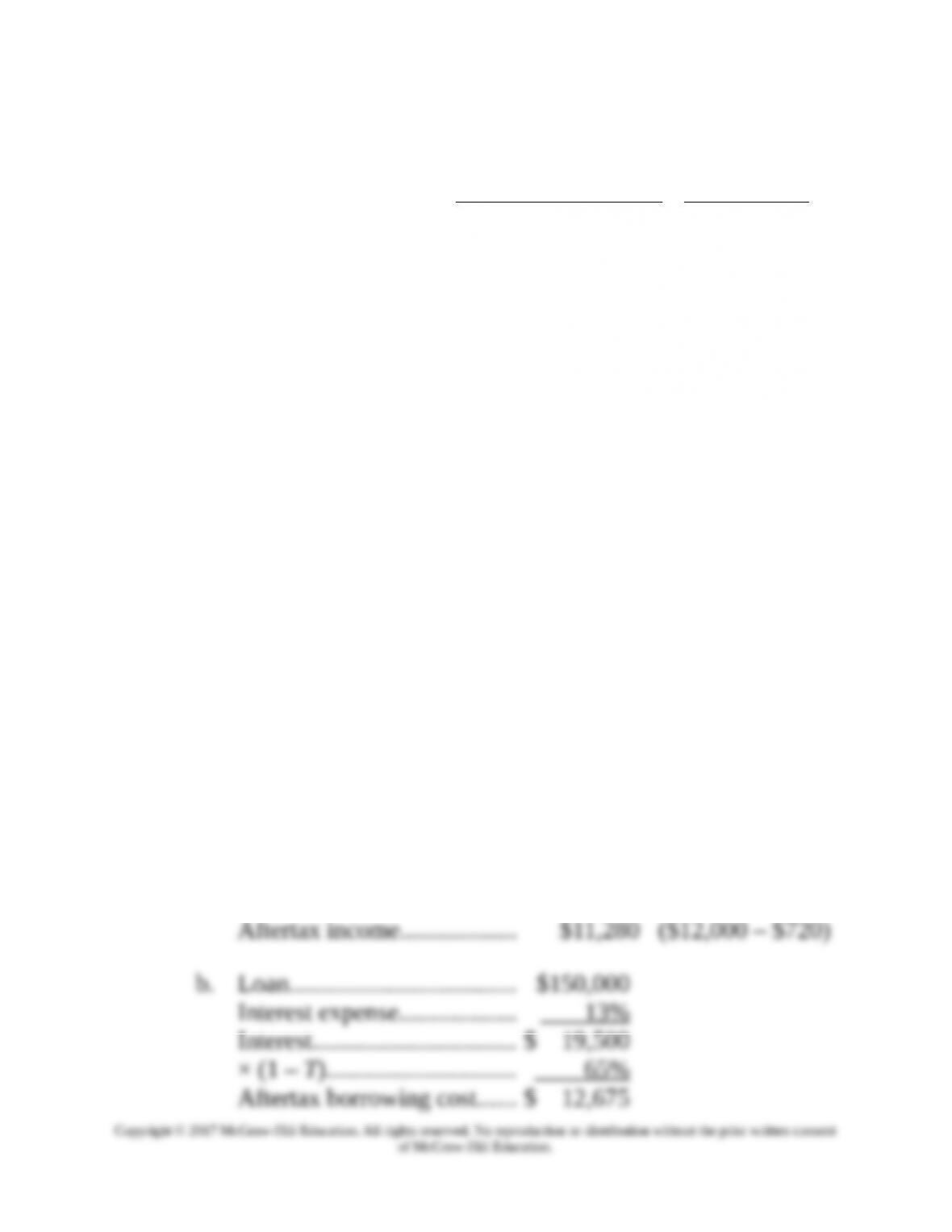

21. Borrowing funds to purchase preferred stock (LO17-5) The treasurer of Kelly Bottling

Company (a corporation) currently has $150,000 invested in preferred stock yielding 8

percent. He appreciates the tax advantages of preferred stock and is considering buying

$150,000 more with borrowed funds. The cost of the borrowed funds is 13 percent. He

suggests this proposal to his board of directors. They are somewhat concerned by the fact

that the treasurer will be paying 5 percent more for funds than the company will be earning

on the investment. Kelly Bottling is in a 35 percent tax bracket, with dividends taxed at

20 percent.

a. Compute the amount of the aftertax income from the additional preferred stock if it is

purchased.

b. Compute the aftertax borrowing cost to purchase the additional preferred stock. That

is, multiply the interest cost times (1 – T).

c. Should the treasurer proceed with his proposal?

d. If interest rates and dividend yields in the market go up six months after a decision to

purchase is made, what impact will this have on the outcome?

17-21. Solution:

Kelly Bottling Company

a. Preferred stock……………….. $150,000

Dividend……………………….. $ 12,000

Taxable income (35%)…….. 3,600

Tax rate (20%)……………….. 720

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

Number of shares

of common stock

to eliminate the

deficit

$20,460,000

Deficit

common stock value $27.95

(732,021 shares) 732,021

==

= =

Chapter 17: Common and Preferred Stock Financing

c. No, the return does not exceed the cost.

d. The outcome could become quite unfavorable for two

Note the dangers of these problems could be overcome by

buying floating-rate preferred stock. The market value of

22. Floating-rate preferred stock (LO17-5) Barnes Air Conditioning Inc. has two classes of

preferred stock: floating rate preferred stock and straight (normal) preferred stock. Both

issues have a par value of $100. The floating-rate preferred stock pays an annual dividend

yield of 4 percent, and the straight preferred stock pays 5 percent. Since the issuance of the

two securities, interest rates have gone up by 2.50 percent for each issue. Both securities

will pay their year-end dividend today.

a. What is the price of the floating-rate preferred stock likely to be?

b. What is the price of the straight preferred stock likely to be? Refer back to Chapter 10

and use Formula 10-4 to answer this question.

17-22. Solution:

Barnes Air Conditioning Inc.

a. The floating rate preferred stock should be trading at very

b. Based on Formula 10-4, the price of straight preferred stock

will be:

$5 $66.67

.075

P

P

P

D

PK

= = =

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Crandall Corporation (rights offering and the impact on shareholders ) (LO17-3) The

Crandall Corporation currently has 100,000 shares outstanding that are selling at $50 per share. It

needs to raise $900,000. Net income after taxes is $500,000. Its vice president of finance and its

investment banker have decided on a rights offering, but are not sure how much to discount the

subscription price from the current market value. Discounts of 10 percent, 20 percent, and 40

percent have been suggested. Common stock is the sole means of financing for the Crandall

Corporation.

a. For each discount, determine the subscription price, the number of shares to be issued, and

the number of rights required to purchase one share. (Round to one place after the decimal

point where necessary.)

b. Determine the value of one right under each of the plans. (Round to two places after the

decimal point.)

c. Compute the earnings per share before and immediately after the rights offering under a

10 percent discount from the market price.

d. By what percentage has the number of shares outstanding increased?

e. Stockholder X has 100 shares before the rights offering and participated by buying 20 new

shares. Compute his total claim to earnings both before and after the rights offering (that is,

multiply shares by the earnings per share figures computed in part c).

f. Should Stockholder X be satisfied with this claim over a longer period of time?

CP 17-1. Solution:

Crandall Corp.

a. A 10 percent discount-subscription price equals $45.

Required funds $900,000

Number of new shares = 20,000

Subscription price $45

= =

Old shares 100,000

Number of rights to purchase one share = 5

New shares 20,000

= =

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

EPS after rights offering = Net income/(Old + New shares)

f. No, he would expect greater earnings. He and others have put

additional capital into the corporation so total claims to earnings

COMPREHENSIVE PROBLEM

Comprehensive Problem 2.

Electro Cardio Systems Inc. (poison pill strategy) (LO17-4) Dr. Robert Grossman founded

Electro Cardio Systems Inc. (ECS) in 2001. The principal purpose of the firm was to engage in

the research and development of heart pump devices. Although the firm did not show a profit

until 2006, by 2010 it reported aftertax earnings of $1,200,000. The company had gone public in

2004 at $10 a share. Investors were initially interested in buying the stock because of its future

prospects. By year-end 2010, the stock was trading at $42 per share because the firm had made

good on its promise to produce lifesaving heart pumps and, in the process, was now making

reasonable earnings. With 850,000 shares outstanding, earnings per share were $1.41.

Dr. Grossman and the members of the board of directors were initially pleased when another

firm, Parker Medical Products, began buying their stock. John Parker, the chairman and CEO of

Parker Medical Products, was thought to be a shrewd investor and his company’s purchase of

50,000 shares of ECS was taken as an affirmation of the success of the firm.

However, when Parker bought another 50,000 shares, Dr. Grossman and members of the

board of directors of ECS became concerned that John Parker and his firm might be trying to take

over ECS.

Upon talking to her attorney, Dr. Grossman was reminded that ECS had a poison pill

provision that took effect when any outside investor accumulated 25 percent or more of the shares

outstanding. Current stockholders, excluding the potential takeover company, were given the

privilege of buying up to 500,000 shares of ECS at 80 percent of current market value. Thus new

shares would be restricted to friendly interests.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

The attorney also found that Dr. Grossman and “friendly” members of the board of directors

currently owned 175,000 shares of ECS.

a. How many more shares would Parker Medical Products need to purchase before the poison

pill provision would go into effect? Given the current price of ECS stock of $42, what would

be the cost to Parker to get up to that level?

b. ECS’s ultimate fear was that Parker Medical Products would gain over a 50 percent interest

in ECS’s outstanding shares. What would be the additional cost to Parker to get 50 percent

(plus 1 share) of the stock outstanding of ECS at the current market price of ECS stock? In

answering this question, assume Parker had previously accumulated the 25 percent position

discussed in a.

c. Now assume that Parker exceeds the number of shares you computed in part b and gets all the

way up to accumulating 625,000 shares of ECS. Under the poison pill provision, how many

shares must “friendly” shareholders purchase to thwart a takeover attempt by Parker? What

will be the total cost? Keep in mind that friendly interests already own 175,000 shares of ECS

and to maintain control, they must own one more share than Parker.

d. Would you say the poison pill is an effective deterrent in this case? Is the poison pill in the best

interest of the general stockholders (those not associated with the company)?

CP 17-2. Solution:

Electro Cardio Systems Inc.

a. If Parker owns 25 percent of the shares outstanding of ECS, the

poison pill will go into effect.

b. To get a 50 percent + 1 share interest in ECS, Parker would need to

own 425,000 (one-half of 850,000) + 1 share. This number is

425,001.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

c. One more share than Parker would necessitate an ownership of

625,001 shares.

CP17-2. (Continued)

Because under the poison pill provision, they can buy at 80 percent

of current market value, the total cost of the 450,001 shares would

be $15,120,033.

d. Yes, the poison pill is an effective deterrent in this case. Since the

poison pill provision allows up to 500,000 additional shares to be

purchased by “friendly” interests, the “friendly” interests are assured

of always owning more than 625,000 shares. Their total potential is

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 17: Common and Preferred Stock Financing

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.