Archives

978-0078025822 Bingham General Journals and Ledgers Package Part 2

978-0078025822 Bingham General Journals and Ledgers Package Part 3

978-0078025822 Bingham Solutions Package Part 1

City of Bingham Solution Page Images for Required Trial Balances, Financial Statements and Schedules, and Reports and Analyses © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any […]

978-0078025822 Bingham Solutions Package Part 2

Requirement 5-c Revenues Investment Income 37,500$ Expenditures Construction 7,530,500 Excess of Revenues Over Expenditures (7,493,000) Other Financing Sources (Uses) Proceeds of Bonds 7,500,000$ Interfund transfers out (7,000) Total Other Financing Sources/Uses 7,493,000 Increase (Decrease) in Fund Balances – Fund Balances, […]

978-0078025822 Bingham Solutions Package Part 3

Requirement 8-e Assets Cash $24,470 0.66224 Investment-bonds 414,562 Interest receivable on investments 6,159 Total Assets $445,191 Net Position Held in trust for depositors $445,191 Note: The reported values were calculated using the following formula: Asset* (CSD Total Equities After Withdrawal/Total […]

978-0078025822 Bingham Solutions Package Part 4

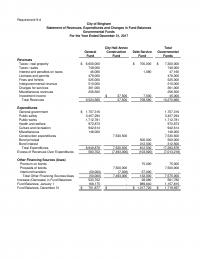

Requirement 9-d City Hall Annex Total General Construction Debt Service Governmental Fund Fund Fund Funds Revenues Taxes—real property 6,600,000$ 700,000$ 7,300,000$ Taxes—sales 748,000 748,000 Expenditures General government 1,707,316$ 1,707,316 Public safety 3,457,294 3,457,294 Public works 1,712,781 1,712,781 Health and welfare […]

978-0078025822 Chapter 1 Lecture Note

Chapter 01 – Introduction to Accounting and Financial Reporting for Governmental and Not-for-Profit Entities © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may […]

978-0078025822 Chapter 10 Lecture Note Part 1

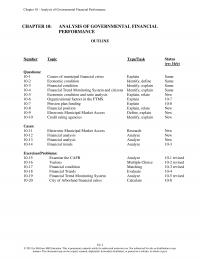

Chapter 10 – Analysis of Governmental Financial Performance 10-1 CHAPTER 10: ANALYSIS OF GOVERNMENTAL FINANCIAL PERFORMANCE OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 10-1 Causes of municipal financial crises Explain Same 10-2 Economic condition Identify, define Same 10-3 Financial […]

978-0078025822 Chapter 10 Lecture Note Part 2

Chapter 10 – Analysis of Governmental Financial Performance 10–10 Ch. 10, Solutions (Cont’d) 10-14. a. The solution to this case will depend on which year’s Financial Trends report each student obtains. In the 2013 report, the following indicators are labeled […]

978-0078025822 Chapter 11 Lecture Note Part 1

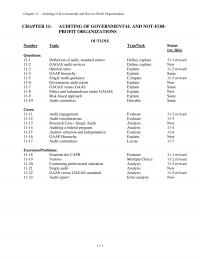

Chapter 11 – Auditing of Governmental and Not-for-Profit Organizations 11-1 CHAPTER 11: AUDITING OF GOVERNMENTAL AND NOT-FOR- PROFIT ORGANIZATIONS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 11-1 Definition of audit, standard setters Define, explain 11-1 revised 11-2 GAGAS audit […]

978-0078025822 Chapter 11 Lecture Note Part 2

Chapter 11 – Auditing of Governmental and Not-for-Profit Organizations 11–10 11-14. Although this case requires no analysis, it is a useful exercise to give students a feel for the resources auditors use to test for compliance in performing single audits. […]

978-0078025822 Chapter 12 Lecture Note Part 1

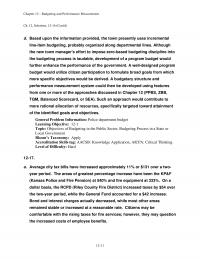

Chapter 12 – Budgeting and Performance Measurement 12-1 CHAPTER 12: BUDGETING AND PERFORMANCE MEASUREMENT OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 12-1 Budgeting reporting Explain New 12-2 Line-item budgeting approaches Compare 12-3 12-3 Performance and program budgeting Describe 12-4 […]

978-0078025822 Chapter 12 Lecture Note Part 2

Chapter 12 – Budgeting and Performance Measurement 12-11 Ch. 12, Solutions, 12–16 (Cont’d) d. Based upon the information provided, the town presently uses incremental line-item budgeting, probably organized along departmental lines. Although the new town manager’s effort to impose zero-based […]

978-0078025822 Chapter 13 Lecture Note Part 1

Chapter 13 – Accounting for Not-for-Profit Organizations © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025822 Chapter 13 Lecture Note Part 2

Chapter 13 – Accounting for Not-for-Profit Organizations 13–16 Ch. 13, Solutions, 13-18 (Cont’d) • Expenses are reported in the temporarily restricted net asset column. Expenses can only be reported in the unrestricted column. If the purpose for which net assets […]

978-0078025822 Chapter 13 Lecture Note Part 3

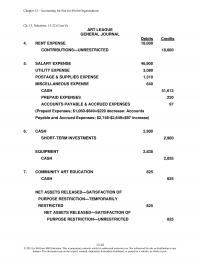

Chapter 13 – Accounting for Not-for-Profit Organizations 13–28 Ch. 13, Solutions, 13–22 (Cont’d) ART LEAGUE GENERAL JOURNAL Debits Credits 4. RENT EXPENSE 18,000 CONTRIBUTIONS—UNRESTRICTED 18,000 5. SALARY EXPENSE 46,900 UTILITY EXPENSE 3,080 POSTAGE & SUPPLIES EXPENSE 1,310 MISCELLANEOUS EXPENSE 640 […]

978-0078025822 Chapter 14 Lecture Note Part 1

Chapter 14 – Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues 14-1 CHAPTER 14: NOT-FOR-PROFIT ORGANIZATIONS— REGULATORY, TAXATION, AND PERFORMANCE ISSUES OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 14-1 Regulatory authority of states and federal government Identify New 14-2 Differences in […]

978-0078025822 Chapter 14 Lecture Note Part 2

Chapter 14 – Not-for-Profit Organizations—Regulatory, Taxation, and Performance Issues 14–11 Ch. 14, Solutions, 14-14 (Cont’d) The balance of the student’s answer to this question will vary from student to student. The authors suggest grading on the thoughtfulness and analysis in […]

978-0078025822 Chapter 15 Lecture Note Part 1

Chapter 15 – Accounting for Colleges and Universities 15-1 CHAPTER 15: ACCOUNTING FOR COLLEGES AND UNIVERSITIES OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 15-1 Financial statements Identify Same 15-2 Recording grants Compare New 15-3 Net asset categories Identify Same […]

978-0078025822 Chapter 15 Lecture Note Part 2

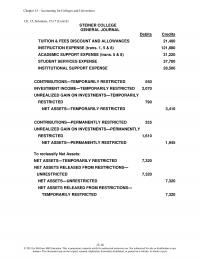

Chapter 15 – Accounting for Colleges and Universities 15–16 Ch. 15, Solutions, 15-17 (Cont’d) STEINER COLLEGE GENERAL JOURNAL Debits Credits TUITION & FEES DISCOUNT AND ALLOWANCES 21,400 INSTRUCTION EXPENSE (trans. 1, 5 & 8) 121,880 ACADEMIC SUPPORT EXPENSE (trans. 5 […]

978-0078025822 Chapter 15 Lecture Note Part 3

Chapter 15 – Accounting for Colleges and Universities 15–27 Ch. 15, Solutions, 15-19 (Cont’d) b. SOUTH STATE UNIVERSITY STATEMENT OF NET POSITION JUNE 30, 2017 ASSETS CASH $ 134,700 ACCOUNTS RECEIVABLE (NET OF DOUBTFUL ACCOUNTS OF $17,000) 297,300 INTEREST RECEIVABLE […]

978-0078025822 Chapter 16 Lecture Note Part 1

Chapter 16 – Accounting for Health Care Organizations © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025822 Chapter 16 Lecture Note Part 2

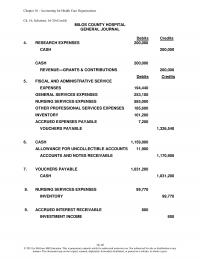

Chapter 16 – Accounting for Health Care Organizations 16–16 Ch. 16, Solutions, 16-20 (Cont’d) MILOS COUNTY HOSPITAL GENERAL JOURNAL Debits Credits 4. RESEARCH EXPENSES 200,000 CASH 200,000 CASH 200,000 REVENUE—GRANTS & CONTRIBUTIONS 200,000 Debits Credits 5. FISCAL AND ADMINISTRATIVE SERVICE […]

978-0078025822 Chapter 17 Lecture Note Part 1

Chapter 17 – Accounting and Reporting for the Federal Government 17-1 CHAPTER 17: ACCOUNTING AND REPORTING FOR THE FEDERAL GOVERNMENT OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 17-1 Roles of GOA, Treasury, and OMB in federal financial reporting Explain […]

978-0078025822 Chapter 17 Lecture Note Part 2

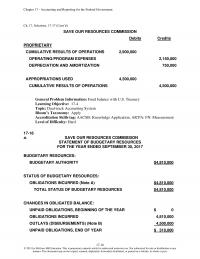

Chapter 17 – Accounting and Reporting for the Federal Government 17–16 Ch. 17, Solutions, 17-17 (Cont’d) SAVE OUR RESOURCES COMMISSION Debits Credits PROPRIETARY CUMULATIVE RESULTS OF OPERATIONS 2,900,000 OPERATING/PROGRAM EXPENSES 2,150,000 DEPRECIATION AND AMORTIZATION 750,000 APPROPRIATIONS USED 4,500,000 CUMULATIVE RESULTS […]

978-0078025822 Chapter 2 Lecture Note

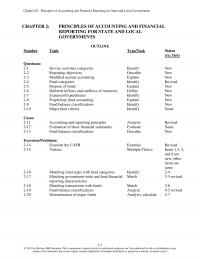

Chapter 02 – Principles of Accounting and Financial Reporting for State and Local Governments © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may […]

978-0078025822 Chapter 3 Lecture Note Part 1

CHAPTER 3: GOVERNMENTAL OPERATING STATEMENT ACCOUNTS; BUDGETARY ACCOUNTING 3-1 OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 3-1 Distinguishing characteristics of fund-based and government-wide financial statements Identify and describe Same 3-2 Distinguishing direct and indirect expenses Define and describe Same […]

978-0078025822 Chapter 3 Lecture Note Part 2

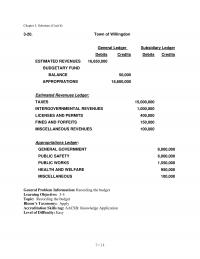

3-14 Chapter 3, Solutions (Cont’d) 3-20. Town of Willingdon General Ledger Subsidiary Ledger Debits Credits Debits Credits ESTIMATED REVENUES 16,650,000 Learning Objective: 3-4 Topic: Recording the budget Bloom’s Taxonomy: Apply Accreditation Skills tag: AACSB: Knowledge Application Level of Difficulty: Easy […]

978-0078025822 Chapter 4 Lecture Note Part 1

Chapter 04 – Accounting for Governmental Operating Activities 4-1 CHAPTER 4: ACCOUNTING FOR GOVERNMENTAL OPERATING ACTIVITIES ⎯ ILLUSTRATIVE TRANSACTIONS AND FINANCIAL STATEMENTS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 4-1 Dual effects of transactions Explain, examples Same 4-2 Encumbrances […]

978-0078025822 Chapter 4 Lecture Note Part 2

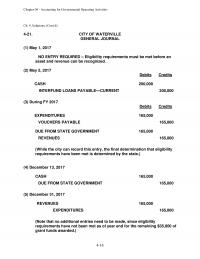

Chapter 04 – Accounting for Governmental Operating Activities 4-16 Ch. 4, Solutions, (Cont’d) 4-21. CITY OF WATERVILLE GENERAL JOURNAL (1) May 1, 2017 NO ENTRY REQUIRED – Eligibility requirements must be met before an asset and revenue can be recognized. […]

978-0078025822 Chapter 4 Lecture Note Part 3

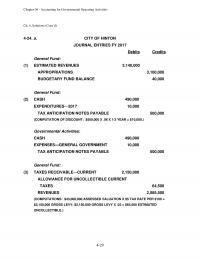

Chapter 04 – Accounting for Governmental Operating Activities 4-29 Ch. 4, Solutions (Cont’d) 4-24. a. CITY OF HINTON JOURNAL ENTRIES FY 2017 Debits Credits General Fund: (1) ESTIMATED REVENUES 3,140,000 APPROPRIATIONS 3,100,000 BUDGETARY FUND BALANCE 40,000 General Fund: (2) CASH […]

978-0078025822 Chapter 5 Lecture Note Part 1

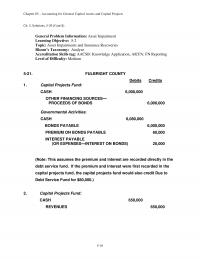

Chapter 05 – Accounting for General Capital Assets and Capital Projects 5-1 CHAPTER 5: ACCOUNTING FOR GENERAL CAPITAL ASSETS AND CAPITAL PROJECTS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 5-1 Defining and reporting general capital assets Define and explain […]

978-0078025822 Chapter 5 Lecture Note Part 2

Chapter 05 – Accounting for General Capital Assets and Capital Projects 5–16 Ch. 5, Solutions, 5-20 (Cont’d) General Problem Information: Asset Impairment Learning Objective: 5-2 Topic: Asset Impairments and Insurance Recoveries Bloom’s Taxonomy: Analyze Accreditation Skills tag: AACSB: Knowledge Application, […]

978-0078025822 Chapter 5 Lecture Note Part 3

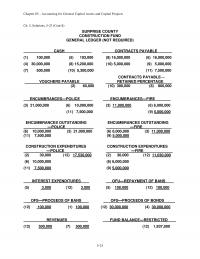

Chapter 05 – Accounting for General Capital Assets and Capital Projects 5–25 Ch. 5, Solutions, 5-23 (Cont’d) SURPRISE COUNTY CONSTRUCTION FUND GENERAL LEDGER (NOT REQUIRED) CASH CONTRACTS PAYABLE CONTRACTS PAYABLE⎯ VOUCHERS PAYABLE RETAINED PERCENTAGE (2) 60,000 (10) 300,000 (8) 800,000 […]

978-0078025822 Chapter 6 Lecture Note Part 1

Chapter 06 – Accounting for General Long–term Liabilities and Debt Service 6-1 CHAPTER 6: ACCOUNTING FOR GENERAL LONG-TERM LIABILITIES AND DEBT SERVICE OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 6-1 Defining general long-term liabilities; financial reporting Define, explain Same […]

978-0078025822 Chapter 6 Lecture Note Part 2

Chapter 06 – Accounting for General Long–term Liabilities and Debt Service 6–16 Ch. 6, Solutions, 6-18 (Cont’d) c. Calculation of Interfund Transfer to Debt Service Fund: Amount of appropriation required for the interest INTEREST EXENSE 96,000 CASH 120,000 e. The […]

978-0078025822 Chapter 6 Lecture Note Part 3

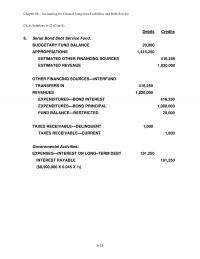

Chapter 06 – Accounting for General Long–term Liabilities and Debt Service 6–25 Ch. 6, Solutions, 6-22 (Cont’d) Debits Credits 6. Serial Bond Debt Service Fund: BUDGETARY FUND BALANCE 20,000 APPROPRIATIONS 1,416,250 ESTIMATED OTHER FINANCING SOURCES 416,250 ESTIMATED REVENUE 1,020,000 OTHER […]

978-0078025822 Chapter 7 Lecture Note Part 1

Chapter 07 – Accounting for the Business–type Activities of State and Local Governments 7-1 CHAPTER 7: ACCOUNTING FOR THE BUSINESS-TYPE ACTIVITIES OF STATE AND LOCAL GOVERNMENTS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 7-1 Proprietary funds Explain New 7-2 […]

978-0078025822 Chapter 7 Lecture Note Part 2

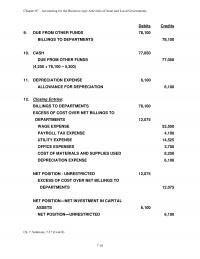

Chapter 07 – Accounting for the Business–type Activities of State and Local Governments 7–16 Debits Credits 9. DUE FROM OTHER FUNDS 78,100 BILLINGS TO DEPARTMENTS 78,100 (4,250 + 78,100 – 5,300) 11. DEPRECIATION EXPENSE 6,100 ALLOWANCE FOR DEPRECIATION 6,100 12. […]

978-0078025822 Chapter 7 Lecture Note Part 3

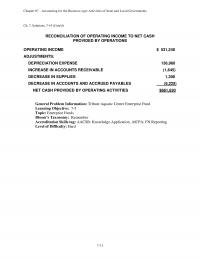

Chapter 07 – Accounting for the Business–type Activities of State and Local Governments 7–31 Ch. 7, Solutions, 7-19 (Cont’d) RECONCILIATION OF OPERATING INCOME TO NET CASH PROVIDED BY OPERATIONS OPERATING INCOME $ 531,240 ADJUSTMENTS: DEPRECIATION EXPENSE 136,960 General Problem Information: […]

978-0078025822 Chapter 8 Lecture Note Part 1

Chapter 08 – Accounting for Fiduciary Activities—Agency and Trust Funds 8-1 CHAPTER 8: ACCOUNTING FOR FIDUCIARY ACTIVITIES— AGENCY AND TRUST FUNDS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 8-1 Distinction between agency and trust funds Distinguish 8-1 revised 8-2 […]

978-0078025822 Chapter 8 Lecture Note Part 2

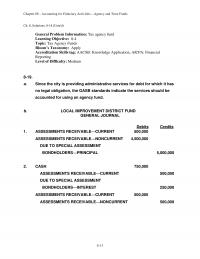

Chapter 08 – Accounting for Fiduciary Activities—Agency and Trust Funds 8–13 Ch. 8, Solutions, 8-18 (Cont’d) General Problem Information: Tax agency fund Learning Objective: 8-4 Topic: Tax Agency Funds Bloom’s Taxonomy: Apply Accreditation Skills tag: AACSB: Knowledge Application, AICPA: Financial […]

978-0078025822 Chapter 9 Lecture Note Part 1

Chapter 09 – Financial Reporting of State and Local Governments 9-1 CHAPTER 9: FINANCIAL REPORTING OF STATE AND LOCAL GOVERNMENTS OUTLINE Number Topic Type/Task Status (re: 16/e) Questions: 9-1 Communicating financial information Identify New 9-2 Primary governments Identify New 9-3 […]

978-0078025822 Chapter 9 Lecture Note Part 2

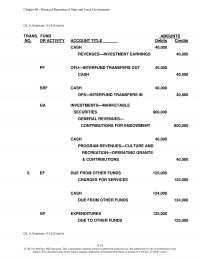

Chapter 09 – Financial Reporting of State and Local Governments 9-14 Ch. 9, Solutions, 9-18 (Cont’d) TRANS. FUND AMOUNTS NO. OR ACTIVITY ACCOUNT TITLE Debits Credits CASH 40,000 REVENUES—INVESTMENT EARNINGS 40,000 PF OFU—INTERFUND TRANSFERS OUT 40,000 CASH 40,000 SRF CASH […]

978-0078025822 Full Solutions Package Smithville Full Part 1

This page and the next two pages report data from chapter 3 Chapter 4 data starts with this page 4b. Cash 553,615$ Taxes receivable—delinquent 209,071$ Less: Allowance for uncollectible delinquent taxes 105,430 103,641 City of Smithville General Fund Balance Sheet […]

978-0078025822 Full Solutions Package Smithville Full Part 2

6b. As of December 31, 2017 Assets City of Smithville Street Improvement Bond Debt Service Fund Balance Sheet Cash 40,000$ Total Assets 40,000$ Fund Balances: Restricted—debt service 40,000$ Total Liabilities and Fund Balances 40,000$ Liabilities and Fund Balances Revenues: Accrued […]

978-0078025822 Full Solutions Package Smithville Full Part 3

City of Smithville Solid Waste Disposal Fund Statement of Revenue, Expenses and Changes in Fund Net Position for the year ended December 31, 2017 Charges for services (net of $960 provision 2,246,572$ for doubtful accounts) Operating Expenses: Payroll and fringe […]

978-0078025822 Full Solutions Package Smithville Full Part 4

9-c Total fund balances 801,091$ Capital assets used in governmental activities are not 19,299,826 financial resources and therefore are not reported in in the funds City of Smithville Reconciliation of the Governmental Funds Balance Sheet to the Government-Wide Statement of […]

978-0078025822 Instructions Bingham Part 1

For use with McGraw-Hill/Irwin Accounting for Governmental & Nonprofit Entities 17th Edition By Jacqueline L. Reck and Suzanne L. Lowensohn Instructions City of Bingham Computerized Cumulative Problem 1 2 Table of Contents Chapter 1 Introducing City of Bingham Welcome………………………………………………………. 4 […]

978-0078025822 Instructions Bingham Part 2

16 e. Select [Reports, Trial Balances, Post-Closing Trial Balance] and print the trial balance for 2016 or save the report as a PDF. If printed, retain the printed trial balance in your personal cumulative folder until the due date assigned […]

978-0078025822 Instructions Bingham Part 3

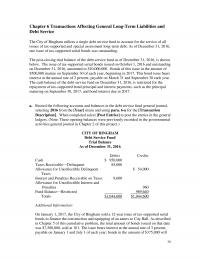

30 Chapter 6 Transactions Affecting General Long-Term Liabilities and Debt Service The City of Bingham utilizes a single debt service fund to account for the service of all issues of tax-supported and special assessment long-term debt. As of December 31, […]

978-0078025822 Instructions Smithville Full Part 1

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

978-0078025822 Instructions Smithville Full Part 2

whole or part. 16 Vouchers Payable 272,187 Due to Federal Government 135,720 Due to State Government 32,600 Internal Payables to Business-type Activities 6,400 Net Position—Net Investment in Capital Assets 17,684,376 Net Position—Restricted for Public Safety 15,000 Net Position—Unrestricted 505,425 Totals […]

978-0078025822 Instructions Smithville Full Part 3

31 Chapter 6 Transactions Affecting General Long-term Liabilities and Debt Service The City of Smithville created a Street Improvement Bond Debt Service Fund to be used to retire the bonds issued for the purposes described in Chapter 5 of this […]

978-0078025822 Instructions Smithville Full Part 4

whole or part. 39 the year). Apply these rates to the original cost of buildings and equipment as of December 31, 2016, assuming no residual or salvage value. 9. [Para. 7-b-9] Interest of $4,000 had accrued on the notes payable […]

978-0078025822 Smithville Full General Journals and Ledgers Package Part 1

Accounting for Governmental & Nonprofit Entities 17th Edition By Jacqueline L. Reck and Suzanne L. Lowensohn City of Smithville Full Version Solution Page Images for Fund and Government-wide General Journals and General Ledgers © 2016 by McGraw-Hill Education. This is […]

978-0078025822 Smithville Full General Journals and Ledgers Package Part 2

978-0078025822 Smithville Full General Journals and Ledgers Package Part 3

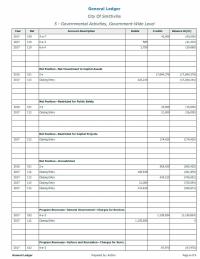

978-0078025822 Bingham General Journals and Ledgers Package Part 1

City of Bingham Solution Page Images for Fund and Government-wide General Journals and General Ledgers © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document […]

AC 29104

State educational appropriations received by a public university are classified as which of the following on the statement of revenues, expenses, and changes in net position? A. Nonoperating revenue. B. Operating revenue. C. Other financing source. D. Increase in unrestricted […]

Accounting 41957

Generally accepted government auditing standards (GAGAS) apply to financial audits of state and local governments only if they expend $750,000 or more in federal financial assistance. The Governmental Accounting Standards Board (GASB) is the body authorized to establish accounting principles […]

Accounting 49718

The following cash transactions were among those reported by Genesee County’s Wastewater Enterprise Fund for the year: Proceeds from sale of revenue bonds for construction $5,000,000 Interest income 300,000 Capital contributed by developers 1,000,000 A. $5,000,000. B. $5,300,000. C. $5,300,000. […]

ACCT 24398

The recorded premium on tax-supported bonds issued by a capital projects fund should be amortized at both the government-wide and fund levels. Under the FASB Codification a $5 million endowment that cannot be spent for 50 years should be classified […]

Acct 43083

Capital projects funds differ from the General Fund and special revenue funds in that the latter categories have a year-to-year life, whereas capital projects funds have a project-life focus. A contractual adjustment is recorded as a contra-revenue account. Answer: TRUE […]

ACCT 94305

The FASB requires that a statement of functional expenses be prepared by which of the following entities? A. Colleges and universities. B. Health care entities. C. Voluntary health and welfare entities. D. Religious entities. Which of the following volunteer services […]

Acct 94383

A not-for-profit typically has gross receipts of $4,500 or less each year. According to the IRS it would not have to file with the IRS to be considered tax-exempt under Sec. 501(c)(3). Service-level solvency is the government’s ability to meet […]

ACT 16087

Governmental activities are to be classified as governmental or business-type. The types of funds that may be used in governmental accounting are classified into the three categories of governmental, proprietary, and fiduciary. Answer: TRUE Governments can, in part, demonstrate operational […]

MET MG 26535

The FASB Codification requires the following financial statements for all not-for-profit organizations: A. Statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses. B. Statement of financial position, statement of operations, statement of cash […]

MET MG 79809

An effective system of monitoring financial condition may permit management to identify unfavorable financial trends in sufficient time to take preventive action to avoid financial distress. The FASB requires that long-term unconditional pledges (those that will not be collected within […]

SMG AC 67598

Under GASB standards, only proprietary funds prepare a statement of cash flows. A large intergovernmental revenues ratio can be viewed as a positive sign concerning a government’s financial condition. Answer: FALSE The General Fund data for a blended component unit […]