Archives

Chapter 10 1 Valuation of nonmonetary asset. Gain recognition on plant asset

CHAPTER 10 ACQUISITION AND DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENT IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Definition of plant assets. b 22. Characteristics of plant […]

Chapter 10 2 The building was completed and ready for occupancy on September

Acquisition and Disposition of Property, Plant, and Equipment 10 – 21 74. On May 1, 2017, Goodman Company began construction of a building. Expenditures of $600,000 were incurred monthly for 5 months beginning on May 1. The building was completed […]

Chapter 10 3 A major overhaul of factory machinery in 2017, which extended

Test Bank for Intermediate Accounting, Sixteenth Edition 10 – 40 DERIVATIONS — Computational (cont.) No. Answer Derivation 82. c ($600,000 × 12/12) + ($1,800,000 × 4/12) + ($1,800,000 × 0/12) = $1,200,000. 83. b $1,200,000 (from # 82) × 12% […]

Chapter 11 1 Economic factors affecting useful service life

CHAPTER 11 DEPRECIATION, IMPAIRMENTS, AND DEPLETION IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Knowledge of depreciation accounting. b 22. Conceptual rationale for depreciation accounting. c 23. […]

Chapter 11 2 what entry should it make when plant assets that originally

Depreciation, Impairments, and Depletion 11 – 21 81. Orton Corporation, which has a calendar year accounting period, purchased a new machine for $80,000 on April 1, 2013. At that time Orton expected to use the machine for nine years and […]

Chapter 11 3 An asset’s cost minus its accumulated depreciation equals

Test Bank for Intermediate Accounting, Sixteenth Edition 11 – 36 DERIVATIONS — Computational (cont.) No. Answer Derivation DERIVATIONS — CPA Adapted No. Answer Derivation 117. c $1,000,000 × 0.3 × 0.5 = $150,000. 118. b Conceptual. 119. b $450,000 × […]

Chapter 12 1 Which The Following Not Intangible Asset

CHAPTER 12 INTANGIBLE ASSETS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description F 25. Example of research and development costs. MULTIPLE CHOICE—Conceptual Answer No. Description b 26 Characteristics of intangible assets. c 27 Characteristics […]

Chapter 12 2 What amount should be reported for patent amortization

Intangible Assets 12 – 21 92. ELO Corporation purchased a patent for $135,000 on September 1, 2016. It had a useful life of 10 years. On January 1, 2018, ELO spent $33,000 to successfully defend the patent in a lawsuit. […]

Chapter 12 3 Varying approaches are used to define goodwill

Intangible Assets 12 – 39 Solution 12-140 Ex. 12-141 Listed below is a selection of accounts found in the general ledger of Marshall Corporation as of December 31, 2018: Accounts receivable Research & development costs Goodwill Internet domain name Organization […]

Chapter 13 1 None These Answers Are Correct ans Lo Bloom

CHAPTER 13 CURRENT LIABILITIES AND CONTINGENCIES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Definition of a liability. d 22. Nature of current liabilities. a 23. Recording […]

Chapter 13 2 The effective interest on a 12-month, zero-interest-bearing

Current Liabilities and Contingencies 13 – 21 85. Which of the following is not an acceptable treatment for the presentation of current liabilities? a. Listing current liabilities in order of maturity b. Listing current liabilities according to amount c. Offsetting […]

Chapter 13 3 Notes Payable described Below Are Certain Transactions Lamar

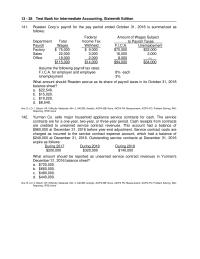

Test Bank for Intermediate Accounting, Sixteenth Edition 13 – 38 141. Roasten Corp.’s payroll for the pay period ended October 31, 2018 is summarized as follows: Federal Amount of Wages Subject Department Total Income Tax to Payroll Taxes Payroll Wages […]

Chapter 14 1 Indicate how to present and analyze long-term debt

CHAPTER 14 LONG-TERM LIABILITIES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Liability identification. a 22. Bond terms. b 23. Definition of “debenture bonds.” a P24. Definition […]

Chapter 14 2 The entry to record the issuance of the bonds would include

Long-Term Liabilities 14 – 21 On October 1, 2017 Macklin Corporation issued 5%, 10-year bonds with a face value of $6,000,000 at 104. Interest is paid on October 1 and April 1, with any premiums or discounts amortized on a […]

Chapter 14 3 Requires that bond discount be reported in the balance

Long-Term Liabilities 14 – 35 DERIVATIONS — CPA Adapted (cont.) No. Answer Derivation BRIEF EXERCISES BE. 14-117—Terms related to long-term debt. Place the letter of the best matching phrase before each word. ____ 1. Indenture ___ 6. Times Interest Earned […]

Chapter 15 1 These questions also appear in the Problem-Solving Survival

CHAPTER 15 STOCKHOLDERS’ EQUITY IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Nature of stockholders’ interest. b 22. Pre-emptive right. d 23. Pre-emptive right. b S24. Definition […]

Chapter 15 2 shares of common stock with a par value of $6 per share

Stockholders’ Equity 15 – 21 79. On September 1, 2017, Valdez Company reacquired 30,000 shares of its $10 par value common stock for $15 per share. Valdez uses the cost method to account for treasury stock. The journal entry to […]

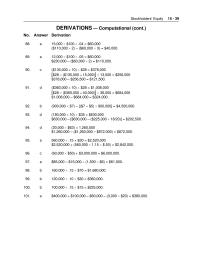

Chapter 15 3 Treasury Stock is credited for the original cost (purchase price)

Stockholders’ Equity 15 – 39 DERIVATIONS — Computational (cont.) No. Answer Derivation 88. a 15,000 $100 .04 = $60,000 ($110,000 2) – ($60,000 3) = $40,000. 89. a 12,000 $100 .05 = $60,000 $230,000 […]

Chapter 16 1 Reporting additional payment to encourage conversion

CHAPTER 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE IFRS questions are available at the end of this chapter. TRUE-FALSE—Dilutive Securities—Conceptual Answer No. Description MULTIPLE CHOICE—Dilutive Securities, Conceptual Answer No. Description d 21. Nature of convertible bonds. d 22. Recording conversion […]

Chapter 16 2 Using a fair value option pricing model, total compensation expense

Dilutive Securities and Earnings per Share 16 – 21 67. On January 1, 2018, Ritter Company granted stock options to officers and key employees for the purchase of 20,000 shares of the company’s $1 par common stock at $20 per […]

Chapter 16 3 Capital Excess Par Calculations premium Related 12 The

Dilutive Securities and Earnings per Share 16 – 41 DERIVATIONS — Dilutive Securities, Computational No. Answer Derivation 43. a $1,280,000 + ($280,000 × .32) – (12,800 × 30 × $30) = $217,600. 44. b $150,000 – (3,000 × $45) – […]

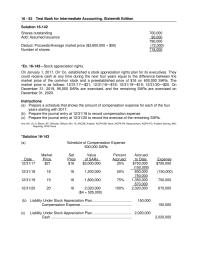

Chapter 16 4 Capital Structure Cumulative Preferred Stock 100 Par

Test Bank for Intermediate Accounting, Sixteenth Edition 16 – 52 Solution 16-142 *Ex. 16-143—Stock appreciation rights. On January 1, 2017, Orr Co. established a stock appreciation rights plan for its executives. They could receive cash at any time during the […]

Chapter 17 1 The Effective interest Method Applied Investments Debt Securities

CHAPTER 17 INVESTMENTS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Debt securities. b 22. Valuation of debt securities. c 23. Held-to-maturity securities. c 24. Unrealized gain/loss […]

Chapter 17 2 Investments Dobbs Account The End 2019 OFA

Investments 17 – 21 76. On November 1, 2018, Horton Company purchased Lopez, Inc., 10-year, 9%, bonds with a face value of $800,000, for $720,000. An additional $24,000 was paid for the accrued interest. Interest is payable semiannually on January […]

Chapter 17 3 Ramirez Company Has Held for collection Investment The

Test Bank for Intermediate Accounting, Sixteenth Edition 17 – 36 BRIEF EXERCISES BE. 17-116—Investment in debt securities at premium. On April 1, 2018, West Company purchased $600,000 of 6% bonds for $623,625 plus accrued interest as an available-for-sale security. Interest […]

Chapter 18 1 Gross profit to be recognized using percentage-of-completion

CHAPTER 18 REVENUE RECOGNITION TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 26. Comprehensive revenue recognition model. c 27. Revenue recognition standard. b 28. First step in revenue recognition process. d 29. Revenue recognition process steps. a 30. […]

Chapter 18 2 Kiner Uses The Completed contract Method The Gross

Revenue Recognition 18 – 21 96. On August 5, 2018, Famous Furniture shipped 40 dining sets on consignment to Furniture Outlet, Inc. The cost of each dining set was $350 each. The cost of shipping the dining sets amounted to […]

Chapter 18 3 The Appliance Store is an experienced home appliance dealer

Revenue Recognition 18 – 37 Solution 18-127 (cont.) Ex. 18-128—Sales with returns and discounts. On July 2, 2018, Lake Company sold to Sue Black merchandise having a sales price of $9,000 (cost $5,400) with terms of 2/10. n/30. f.o.b. shipping […]

Chapter 19 1 Classification of deferred income tax on the balance sheet

CHAPTER 19 ACCOUNTING FOR INCOME TAXES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 21. Differences between taxable and accounting income. c 22. Differences between taxable and accounting […]

Chapter 19 2 Customers who purchase furniture on thein stallment basis

68. Ewing Company sells household furniture. Customers who purchase furniture on the installment basis make payments in equal monthly installments over a two-year period, with no down payment required. Ewing’s gross profit on installment sales equals 40% of the selling […]

Chapter 19 3 The estimated litigation expenses of $890,000 will be deductible

Test Bank for Intermediate Accounting, Sixteenth Edition 19 – 38 BRIEF EXERCISES BE. 19-105—Computation of taxable income. The records for Bosch Co. show this data for 2018: • Gross profit on installment sales recorded on the books was $480,000. Gross […]

Chapter 2 1 The first level of the conceptual framework identifies

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. GAAP defined. d 22. Purpose of conceptual framework. c 23. Conceptual framework. […]

Chapter 2 2 The accounting principle of expense recognition is best

Test Bank for Intermediate Accounting, Sixteenth Edition 2 – 20 89. The measurement principle includes the a. fair value principle only. b. historical cost principle only. c. revenue recognition principle and expense recognition principle. d. historical cost principle and the […]

Chapter 20 1 This topic is dealt with in an Appendix to the chapter

CHAPTER 20 ACCOUNTING FOR PENSIONS AND POSTRETIREMENT BENEFITS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Factors considered by actuaries. c 22. Process of funding a pension […]

Chapter 20 2 The settlement rate is 10%. Other data related to the pension plan

Accounting for Pensions and Postretirement Benefits 20–21 74. The actual return on plan assets in 2018 was a. $600,000. b. $510,000. c. $400,000. d. $310,000. Ans: B, LO: 1, Bloom: AP, Difficulty: Moderate, Min: 4, AACSB: Analytic, AICPA BB: None, […]

Chapter 20 3 The Expected Return Plan Assets And the Settlement

Accounting for Pensions and Postretirement Benefits 20–41 Solution 20-115 Ex. 20-116—Pension plan calculations and journal entry. On January 1, 2018, McGee Co. had the following balances: Projected benefit obligation $7,800,000 Fair value of plan assets 7,800,000 Other data related to […]

Chapter 20 4 Company follows GAAP for its external financial reporting whereas

Test Bank for Intermediate Accounting, Sixteenth Edition 20–48 Pr. 20-123 (cont.) Instructions (a) Determine the missing amounts in the 2018 pension worksheet, indicating whether the amounts are debits or credits. (b) Prepare the journal entry to record 2018 pension expense […]

Chapter 21 1 The Present Value The Minimum Lease Payment SC

CHAPTER 21 ACCOUNTING FOR LEASES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Advantages of leasing. d 22. Captive leasing companies. b 23. Basic principle of lease […]

Chapter 21 2 lt does not have knowledge of the 8% implicit

Accounting for Leases 21 – 21 75. What type of lease is this from Alt Corporation’s viewpoint? a. Operating lease b. Capital lease c. Sales-type lease d. Direct-financing lease 76. If Alt accounts for the lease as an operating lease, […]

Chapter 21 3 Eubanks Incremental Borrowing Rate 10 Per Year

Accounting for Leases 21 – 37 DERIVATIONS — Computational (cont.) No. Answer Derivation 79. c Fair value = $1,600,000. 80. d Conceptual. 81. a Hook: ($80,000 × 6) + ($100,000 6) – ($6,400,000 ÷ 8) = $280,000 Emley: ($80,000) […]

Chapter 22 1 accumulated depreciation after a change in estimate

CHAPTER 22 ACCOUNTING CHANGES AND ERROR ANALYSIS TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 21. Accounting changes and consistency concept. b 22. Identify changes in accounting principle. c 23. Identify a non-retrospective change. d 24. Identify a […]

Chapter 22 2 Corrections Errors Are Recorded The

Test Bank for Intermediate Accounting, Sixteenth Edition 22 – 20 MULTIPLE CHOICE—CPA Adapted 68. Which of the following should be reported as a prior period adjustment? Change in Change from Estimated Lives Unaccepted Principle of Depreciable Assets to Accepted Principle […]

Chapter 23 1 The tax rate is 30%.103.On the statement of cash flows

CHAPTER 23 STATEMENT OF CASH FLOWS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Objective of the statement of cash flows. c 22. Primary purpose of the […]

Chapter 23 2 Linda Inc Accounted For Under The Equity Method

Statement of Cash Flows 23 – 21 Equipment that cost $875,000 and had a book value of $390,000 was sold for $450,000. Data from the comparative balance sheets are: 12/31/18 12/31/17 Equipment $5,400,000 $4,875,000 Accumulated Depreciation 1,650,000 1,425,000 62. Equipment […]

Chapter 23 3 financial statements of Harlan mining co. for 2019 and 2018

Statement of Cash Flows 23 – 41 99.The net cash provided (used) by financing activities during 2018 is a. $(3,300,000). b. $1,110,000. c. $2,600,000. d. $2,000,000. Ans: D, LO: 4, Bloom: AP, Difficulty: Moderate, Min: 3, AACSB: Analytic, AICPA BB: […]

Chapter 23 4 which appear in the major sections of the statement

Test Bank for Intermediate Accounting, Sixteenth Edition 23 – 60 Ex. 23-124—Preparation of statement of cash flows (format provided). The balance sheets for Kinder Company showed the following information. Additional information concerning transactions and events during 2018 are presented below. […]

Chapter 24 1 The Absolute Amount Its Profit Loss

CHAPTER 24 FULL DISCLOSURE IN FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Disclosure of significant accounting policies. c 22. Disclosure of inventory accounting policy. […]

Chapter 24 2 Final Income Statement For The Quarter Ended march

Full Disclosure in Financial Reporting 24 – 21 The following data are provided: December 31 2018 2017 Cash $ 1,500,000 $ 1,000,000 Accounts receivable (net) 1,600,000 1,200,000 Inventories 2,600,000 2,200,000 Plant assets (net) 7,000,000 6,500,000 Accounts payable 1,100,000 800,000 Income […]

Chapter 24 3 Test Bank For Intermediate Accounting Sixteenth Edition solution

Test Bank for Intermediate Accounting, Sixteenth Edition 24 – 34 Solution 24-87 (cont.) Ex. 24-88—Inventory and cost of goods sold at interim dates. Discuss how inventory and cost of goods sold may be afforded special accounting treatment at interim dates. […]

Chapter 3 1 Bank For Intermediate Accounting Sixteenth Edition which The

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM IFRS questions are available at the end of this chapter. TRUE/FALSE Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Purpose of an accounting system. d 22. Definition of posting. d 23. Purpose […]

Chapter 3 2 Interest The Note Payable The First Day

The Accounting Information System 3 – 21 Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. 21. d 32. a 43. c 54. a 65. c 76. c 22. d 33. a 44. d […]

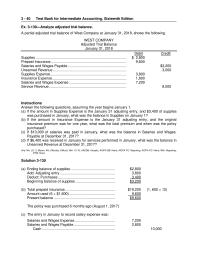

Chapter 3 3 Bad Debt Expense Allowance For Doubtful Accounts

Test Bank for Intermediate Accounting, Sixteenth Edition 3 – 40 Ex. 3-130—Analyze adjusted trial balance. A partial adjusted trial balance of West Company at January 31, 2018, shows the following. WEST COMPANY Adjusted Trial Balance January 31, 2018 Debit Credit […]

Chapter 4 3 Company income Statement for The Year Ended December 31

Income Statement and Related Information 4 – 41 Solution 105 (cont.) Net income …………………………………………………………. $330,000 Dividends ……………………………………………………………. (12,000) 12/31/17 Retained earnings …………………………………… $ 318,000(e) Ex. 4-106—Income statement classifications. Indicate the major section or subsection of a multiple-step income statement in […]

Chapter 5 2 Stine Corp.’s trial balance reflected the following account balances

Balance Sheet and Statement of Cash Flows 5 – 21 83. For Randolph Company, the following information is available: Capitalized leases $560,000 Copyrights 240,000 Long-term receivables 210,000 In Randolph’s balance sheet, intangible assets should be reported at a. $240,000. b. […]

Chapter 5 3 The Net Accounts Receivable Balance Includes A

Balance Sheet and Statement of Cash Flows 5 – 39 Solution 5-116 Ex. 5-117—Statement of cash flows. For each event listed below, select the appropriate category which describes the effect of the event on a statement of cash flows: a. […]

Chapter 6 1 What Time Value Money Concept Appropriate for This

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Appropriate use of an annuity due table. d 22. Time […]

Chapter 6 3 Lease Covers Office Equipment Which Could Purchased

Accounting and the Time Value of Money 6 – 39 BRIEF EXERCISES BE. 6–133—Present and future value concepts. On the right are six diagrams representing six different present and future value concepts stated on the left. Identify the diagrams with […]

Chapter 8 1 Sales with high rates of return inventories are included in net income

CHAPTER 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Identify manufacturer inventory similar to merchandise inventory. d 22. Sales with […]

Chapter 8 2 then it must also be used for external financial

Valuation of Inventories: A Cost-Basis Approach 8 – 21 Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. 21. C 30. c 39. b 48. d 57. c 66. b 75. a […]

Chapter 8 3 The effect of the errors in ending inventories reverse themselves

Valuation of Inventories: A Cost-Basis Approach 8 – 39 145. Keck Co. had 300 units of product A on hand at January 1, 2017, costing $21 each. Purchases of product A during January were as follows: Date Units Unit Cost […]

Chapter 9 1 Gross profit percentage .Disadvantage of gross profit method

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Recording inventory loss under the loss method. d 22. Recording inventory loss under […]

Chapter 9 2 The total selling price is $840,000, and estimated costs

Inventories: Additional Valuation Issues 9 – 21 77. Given the historical cost of product Dominoe is $12, the selling price of product Dominoe is $15, costs to sell product Dominoe are $2, the replacement cost for product Dominoe is $11, […]

Chapter 9 3 Keen’s gross profit on sales has remained constant at 25%

Inventories: Additional Valuation Issues 9 – 41 135. Keen Company‘s accounting records indicated the following information: Inventory, 1/1/17 $ 1,800,000 Purchases during 2017 9,000,000 Sales during 2017 11,400,000 A physical inventory taken on December 31, 2017, resulted in an ending […]

Chapter 9 4 GAAP Certain Agricultural Products And Mineral Products

Inventories: Additional Valuation Issues 9 – 53 Solution 9-147 PROBLEMS Pr. 9-148—Gross profit method. On December 31, 2018 Felt Company’s inventory burned. Sales and purchases for the year had been $1,500,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2018) […]