Archives

978-0132751261 Problem Part 1

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman) Problems – Chapter 2 The material in Chapter 2 is best suited for two types of problems: 1. Matching funds to fund types or fund definitions; and 2. Transaction analysis. Since […]

978-0132751261 Problem Part 10

Answers: # Fund or Nonfund Accounts Accounts Debit Credit 1a SC GF Taxes Receivable – Current 12,000 91 Copyright © 2013 Pearson Education, Inc. Allowance for Uncollectible Taxes – Current 240 Revenues – Property Taxes 11,760 1b SC AF Taxes […]

978-0132751261 Problem Part 11

# Fund or Nonfund Accounts Accounts Debit Credit 1a GF Expenditures – Operating 400 # Fund or Nonfund Accounts Accounts Debit Credit 101 Copyright © 2013 Pearson Education, Inc. Due to Pension Trust Fund 400 1b GF Expenditures – Operating […]

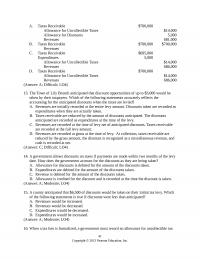

978-0132751261 Problem Part 12

Problem 3 – Statement of Net Position Reconciliation Information about the conversion of the Governmental Funds Balance Sheet to the Statement of Net Position for the City of Pleasant Hill is presented below (all amounts are in thousands of dollars): […]

978-0132751261 Problem Part 13

# Accounts Debit Credit 1 Cash 300 # Accounts Debit Credit 121 Copyright © 2013 Pearson Education, Inc. Unrestricted Support — Contributions 300 2 Cash 1,245 Temporarily Restricted Support – Contributions – Education 43 Temporarily Restricted Support – Contributions – […]

978-0132751261 Problem Part 14

Problem 3 – The following information was derived from the accounts and records of Mockingbird State University for 20X3. All amounts are in thousands of dollars. Tuition and fees Total assessed…………………………………………………………………………………………. $4,000 Expected uncollectible…………………………………………………………………….…….… 80 Appropriations State………………………………………………………………………………………………………. 800 Auxiliary enterprises […]

978-0132751261 Problem Part 15

Answer: Jackson County Hospital Statement of Revenues, Expenses, and Changes in Net Position For the Year Ended December 31, 20X0 ** Calculations: Patient service charges ($18,000) less charity service ($500) less contractual adjustments ($1,100) less uncollectible accounts ($710). ***Calculations: Net […]

978-0132751261 Problem Part 2

Trans # Assets Liabilities Fund Balance GCA GLTL Net Position 1 9,700 NE 9,700 NE NE NE There are several possible answers to this question, all of them correct at this stage of the book: The decrease of $30 indicates […]

978-0132751261 Problem Part 3

City of Walland Preclosing Trial Balance For the Year Ended June 30, 20X4 Advance to Enterprise Fund……………………………………………………………………… 1,000 Allowance for Uncollectible Taxes……………………………………………………….…… 300 Appropriations……………………………………………………………………..….…….…….… 8,850 Budgetary Fund Balance………………………………………………………………………..… 150 Cash………………………………………………………………………………………………………. $5,000 Due from Special Revenue Fund………………………………………………………….…… 100 Encumbrances Outstanding………………………………………………….…….…….……… 60 […]

978-0132751261 Problem Part 4

31 Copyright © 2013 Pearson Education, Inc. 2. F – reported as a capital outlay expenditure by the SRF 3. C 4. F – reported as a general long-term liability until paid 5. F – Balance Sheet liability 6. F […]

978-0132751261 Problem Part 5

(2) Indicate the effects of each transaction on the accounting equation of the Capital Projects Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If an element is not affected, put “NE” in the appropriate box. 41 […]

978-0132751261 Problem Part 6

Answers: Requirement #1 # Accounts Debit Credit Situation A Requirement #2 Situation A Trans # Assets Liabilities Fund Balance GCA GLTL Net Position 1 8,160 NE 8,160 NE 8,160 (8,160) 2 (8,160) NE (8,160) NE (8,160) 8,160 Situation B Trans […]

978-0132751261 Problem Part 7

# Fund or Nonfund Accounts Accounts Debit Credit 1a GF Expenditures – Capital Outlay 2,000 Fund or 61 Copyright © 2013 Pearson Education, Inc. OFS – Capital Lease 2,000 1b GCA/GLTL Equipment under Capital Lease 2,000 Leases Payable 2,000 2a […]

978-0132751261 Problem Part 8

Problem 7 – Other Interfund Transactions: Debt Refunding Transactions: The City of Armona has decided to refinance $8,000 of par value, general government, general obligation bonds outstanding. The bonds had a related unamortized bond premium of $200. The city issues […]

978-0132751261 Problem Part 9

10. Cash received from a capital grant, $5,000. 11. Cash paid for construction costs that qualify under the capital grant, $1,500. 12. The City acquired land for future plant expansion, $750, by issuing a 10-year bond in the same amount. […]

978-0132751261 SM Part 1

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman) Chapter 1 Governmental and Nonprofit Accounting—Environment and Characteristics 1. Which of the following would not be considered a government or nonprofit organization? A. A software company that sells software exclusively to […]

978-0132751261 SM Part 10

17. The Public Utilities Enterprise Fund was ordered by the court to pay environmental damages of $500,000. The fund is to pay $100,000 immediately and the remaining $400,000 in equal installments for next four years. In the year of the […]

978-0132751261 SM Part 11

24. If a Self-Insurance Internal Service Fund pays claims of $5,000 during the month, the fund will report A. Expenses of $5,000. B. Transfers out of $5,000. C. Nonoperating expenses of $5,000. D. A decrease in prepaid assets of $5,000. […]

978-0132751261 SM Part 12

(Answer: C; Easy; LO2) 10. For general purpose external financial reporting, discretely presented component unit information A. Is not presented. B. Is included in the government-wide statements only. C. Is included in the fund financial statements only. D. Is included […]

978-0132751261 SM Part 13

10. A city has a long-term general government liability for compensated absences of $700,000 at the beginning of the year and $650,000 at the end of the year. What adjustment is needed to changes in fund balance to reconcile the […]

978-0132751261 SM Part 14

A. Required in the basic financial statements and in the CAFR. B. Optional in the basic financial statements but required in the CAFR. C. Optional in the basic financial statements and optional in the CAFR. D. Required in the CAFR. […]

978-0132751261 SM Part 15

20X8; $20,000 in contributions restricted for use in 20X9; and a $400,000 contribution restricted for the establishment of a permanent endowment. It is anticipated that 10% of all pledges except the endowment pledge will be uncollectible. Pledges receivable for 20X8 […]

978-0132751261 SM Part 16

33. A government college received a $2 million grant restricted to research on developing a process for synthesizing a stable triple helix. $500,000 of qualifying research costs were incurred during the year. The college should report: A. Grant revenues of […]

978-0132751261 SM Part 17

14. When agency directors make allotments, what budgetary accounts are affected? A. Unapportioned Authority and Allotments–Realized Resources. B. Allotments–Realized Resources and Undelivered Orders. C. Appropriations and Allotments–Realized Resources. D. Allotments–Realized Resources and Expended Appropriations. 15. Assume that Congress enacted an […]

978-0132751261 SM Part 2

25. Incurring construction costs on a major general government capital project would A. Decrease fund balance in a Capital Projects Fund. B. Decrease cash in the General Capital Assets accounts. C. Increase capital assets in a Capital Projects Fund. D. […]

978-0132751261 SM Part 3

B. A net decrease of $5,000. C. A decrease of $15,000. D. A net increase of $5,000. (Answer: A; Moderate; LO3) 19. The city’s central garage, which is accounted for as an Internal Service Fund, repairs and maintains all of […]

978-0132751261 SM Part 4

B. The budgetary entry to record an encumbrance would be a debit to Encumbrances and a credit to Encumbrances Outstanding. C. If the actual cost of a purchase exceeds the amount of the original encumbrance, the original encumbrance is still […]

978-0132751261 SM Part 5

A. Taxes Receivable Allowance for Uncollectible Taxes Revenues $700,000 $14,000 681,000 B. Taxes Receivable Revenues $700,000 $700,000 C. Taxes Receivable $695,000 Expenditures Allowance for Uncollectible Taxes $14,000 Revenues 5,000 686,000 D. Taxes Receivable Allowance for Uncollectible Taxes $14,000 Revenues $700,000 […]

978-0132751261 SM Part 6

14. The General Fund reported a beginning balance of inventory of materials and supplies of $122,000. The ending balance was $150,000. Supplies purchased during the year totaled $600,000. The county uses the consumption method. The General Fund should report expenditures […]

978-0132751261 SM Part 7

22. A city was awarded a $600,000 federal grant to help finance a bridge construction project 60% (nonrefundable) at the beginning of the project in Year 1, and (2) 40% when the project is completed. Capital Projects Fund revenue should […]

978-0132751261 SM Part 8

15. Assume that a Debt Service Fund does not have nonspendable fund balance. Further assume that after restricted and committed levels of fund balance have properly identified, the remaining balance is a deficit. This deficit fund balance should A. Be […]

978-0132751261 SM Part 9

14. The city’s new tax collector foreclosed on a piece of land. The fair market value of the land at the time of foreclosure was $9,000. The taxpayer had acquired the property at a cost of $11,000. The past due […]