Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 2

The material in Chapter 2 is best suited for two types of problems:

1. Matching funds to fund types or fund definitions; and

2. Transaction analysis.

Since transactions are an essential part of Chapters 3 through 12 and 16 through 18, we recommend using

the transaction analysis with journal entries in those chapters. To that end, transaction analysis will be

demonstrated in those chapters.

Problem 1 – Matching funds types to fund categories.

Indicate how the following funds types would be classified as to category: (G) governmental, (P)

proprietary, or as (F) fiduciary.

1. Internal Service

2. Agency

3. General

4. Special Revenue

5. Investment Trust

6. Capital Projects

7. Debt Service

8. Pension Trust

9. Permanent

10. Enterprise

11. Private-Purpose Trust

Answers:

1

Copyright © 2013 Pearson Education, Inc.

Problem 2 – Fund and Nonfund Accounts identification

1Match the following situations with the fund or nonfund accounts best suited to account for it.

A fund or nonfund accounts may be used more than once. The funds and nonfund accounts are:

A Agency Fund G General Long-Term Liability accounts

B Capital Projects Fund H Internal Service Fund

C Debt Service Fund J Pension Trust Fund

D Enterprise Fund K Permanent Fund

E General Capital Asset accounts L Private Purpose Trust Fund

F General Fund M Special Revenue Fund

1. The operations of a city bus line receiving all its funding from user charges.

2. Receipts from a special fishing tax restricted to maintain the (no-charge) public fishing pier.

3. Collects taxes withheld from employees throughout the government and makes payments to the

appropriate government for these withholdings.

4. Donation to the city to be invested in perpetuity with the earnings from that investment to help

maintain city parks.

5. The activities of a central motor pool that provides and services vehicles for the use of municipal

employees on official business.

6. The segregation of resources accumulated to pay principal and interest on long-term debt of the

general government.

7. The levy and collection of property taxes for general operations of a city.

8. Used to account for acquisition of major capital assets.

9. Accounts for contributions by the government and employees to be invested and paid to

employees after retirement.

10. Amounts owed to general government bondholders that must be paid in the future.

11. Used to account for land, buildings, and equipment owned by the government.

12. Activities whose management requires a periodic measurement of revenues and expenses, and

whose customers are the general public.

13. Receipts from a special tax levy to retire and pay interest on general obligation bonds issued to

finance the construction of a new city hall.

14. Donation to the city where the principal is to remain intact forever and the earnings are to be used

to benefit the Boy Scout and Girl Scout organizations in the city.

2

Copyright © 2013 Pearson Education, Inc.

Answers:

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 3

Problem 1 – Matching events with types of interfund transactions

2Transactions in governmental accounting may be classified as being either:

External – transactions between the governmental unit and its citizens, employees,

suppliers, creditors, or other governments.

Internal – transactions between funds

A listing of all possible transactions would then look like this:

A. External transactions

B. Long-term loans

C. Transfers

D. Interfund Services

E. Reimbursements

F. Short-term loans

G. Other transactions between funds that do not meet the criteria B to F

Identify the type of transaction that best fits each of the following events:

1. A government-owned and operated electric utility billed its industrial and commercial

users $2,000,000 for electric usage.

2. The same government-owned and operated electric utility billed the local government

$150,000 for electric usage. The entire bill was sent to the General Fund.

3. Some General Fund money was advanced to a Capital Projects Fund to allow

construction on a project to begin before related bonds were to be issued. The amount is

to be repaid in 6 months.

3

Copyright © 2013 Pearson Education, Inc.

4. A vehicle used by the Parks and Recreation Activity, which is accounted for in the

General Fund, was transferred to the Golf course, which is accounted for in an Enterprise

Fund.

5. Property taxes were levied by the General Fund on the property owners of the City.

6. The annual payment from the General Fund to a Debt Service Fund for the annual long-

term debt principal and interest payment on some serial bonds issued five years earlier by

the General Fund.

7. An invoice that should have been paid by Special Revenue Fund #1 was erroneously paid

by Special Revenue Fund #2. Money was paid by SRF #1 to SRF #2 to correct the error.

8. Computer support for government functions is provided centrally by an Automated Data

Processing Internal Service Fund which bills each function monthly based on CPU time.

The bill for November was sent to the General Fund for payment.

9. Special Revenue Fund cash was contributed to establish an Enterprise Fund.

10. A payment from an Enterprise Fund to the General Fund for utilities paid for with

General Fund cash and recorded as expenditures in the General Fund in the current year

(See #2).

11. The remaining assets of a Debt Service Fund were transferred to the General Fund for use

in operations.

12. The General Fund provided money to an Enterprise Fund to purchase capital assets. This

payment is to be repaid in 5 years without interest.

Answers:

4

Copyright © 2013 Pearson Education, Inc.

Problem 2 – Matching: Financial Statement Preparation

3Listed below are the sections of the Balance Sheet and Statement of Revenues, Expenditures,

and Changes in Fund Balance that would be prepared for the General Fund:

Balance Sheet Statement of Revenues, Expenditures, and Changes in Fund Balance

A

B

C

Assets

Liabilities

Fund Balance

D

E

F

G

H

Revenues

Expenditures

Other Financing Sources and Uses, including transfers

Special and Extraordinary Items

Fund Balance

Certain accounts from the general ledger or other transactions of the City of Six Mile are listed

below. For each account or transaction identify the section of the appropriate financial statement

where each account would be reported. If an account is not reported on either statement, indicate

that by using a X. A section may be used more than once.

1. Payment to employees for services rendered

2. Allowance for Uncollectible Taxes

3. Advance to Enterprise Fund

4. Sale of park land (considered unusual but under the control of management)

5. Property taxes levied and collected

6. Fund Balance – Nonspendable – Inventory

7. Vouchers Payable

8. Transfer to the Special Revenue Fund

9. Correction of Prior Year Error

10. Due to Internal Service Fund

11. Purchase of a capital asset

12. Building inspection services provided to contractors

13. Receipt of materials ordered

14. Payment from Fund A to Fund B for transaction erroneously recorded in Fund B

15. Insurance recovery from a tornado (tornado was considered unusual and infrequent)

16. Investments

17. Interest earned on investments

18. Short-term borrowing from a bank

19. Interest paid on short-term loan

20. Due from Special Revenue Fund

5

Copyright © 2013 Pearson Education, Inc.

Answers:

6

Copyright © 2013 Pearson Education, Inc.

Problem 3 –Journal Entries and Transaction Analysis

4Selected transactions of the City of Miser Station General Fund for the 20X1 fiscal year are

presented on the following page. All amounts are in thousands of dollars.

General instructions:

a. Dates and formal explanations may be omitted, but number your entries appropriately.

b. All interest rates are annual percentage rates (APRs).

c. Record your entries on the lined paper provided with your answer pages. Sufficient space

has been provided to allow you to skip lines between entries.

d. When recording Revenues, classify them as Revenues–Property Taxes or Revenues–

Other. When recording expenditures, classify them as Expenditures–Operating,

Expenditures–Debt Service, or Expenditures–Capital Outlay.

e. Show all work for any amount required in an entry that is not given in the exam

(except when recording the amount necessary to balance the journal entry).

Requirements:

1. Prepare the general ledger journal entries for the transactions. If no entry is required, do

not leave it blank. State “No Entry Required” and briefly explain why.

2. Indicate the effects of the transaction on the accounting equations for the General Fund

and the General Capital Assets and General Long-Term Liabilities accounts. Do not

leave a cell blank. If a transaction has no effect on a particular element, use “NE”.

Transactions:

1. The property tax levy was recorded, $10,000, of which 3% will probably prove

uncollectible.

2. The City borrowed $500 from the Blount National Bank on a two-month, 6% note.

3. Ordered and received, on account, supplies costing $135.

4. Cash receipts were (see entry #1):

Property Taxes………………………………………………………………………… 8,500

License and Permits……………………………………………………..…………. 150

Total Receipts…………………………………………………………………………. 8,650

5. A loan of $50 was made from the General Fund to the City Gasoline Tax Fund (CGTF),

which is accounted for as a Special Revenue Fund. The loan will be repaid in five years.

6. The $10 assets (cash) from a terminated Capital Projects Fund (CPF) were received.

7. The City repaid the short-term note (Entry #2) when due.

7

Copyright © 2013 Pearson Education, Inc.

8. A pickup truck purchased seven years ago for $30 with General Fund money was sold for

$5. The City’s proprietary funds usually depreciate this type of asset over a 10-year

period using straight-line depreciation with zero (0) salvage value and disposes of assets

at the end of its useful life.

9. City employees were paid, $25.

10. Sold land for $300, which had been used many years ago as a public park. The land had

been purchased for $140.

11. General Fund resources of $250 were paid to a newly established Capital Projects Fund.

The resources will not be repaid to the General Fund.

12. The City paid $140 from its General Fund to the fund that services its long-term debt.

13. The county purchased a police vehicle for $22 and paid cash.

14. Paid $500 the Debt Service Fund to provide for upcoming principal and interest

payments.

15. Paid $5,000 to the City Airport Enterprise Fund to provide financing for a major

expansion project; $2,000 is not required to be repaid, but $3,000 is to be repaid at the

end of five years.

16. Loaned $320 to the Capital Projects Fund—to be repaid in 90 days.

17. Paid $12 to the Special Revenue Fund to repay it for General Fund employee salaries that

were inadvertently recorded as expenditures of that fund.

18. Received a bill from the Utility Enterprise Fund for electricity usage charged to General

Fund departments and agencies, $300.

19. Instructed the Library Special Revenue Fund to pay its portion of the utility bill (Entry

#18), $25; the cash was not immediate received.

20. The Library Special Revenue Fund paid the amount owed (Entry #19).

21. Wrote off $100 of taxes receivable as uncollectible.

8

Copyright © 2013 Pearson Education, Inc.

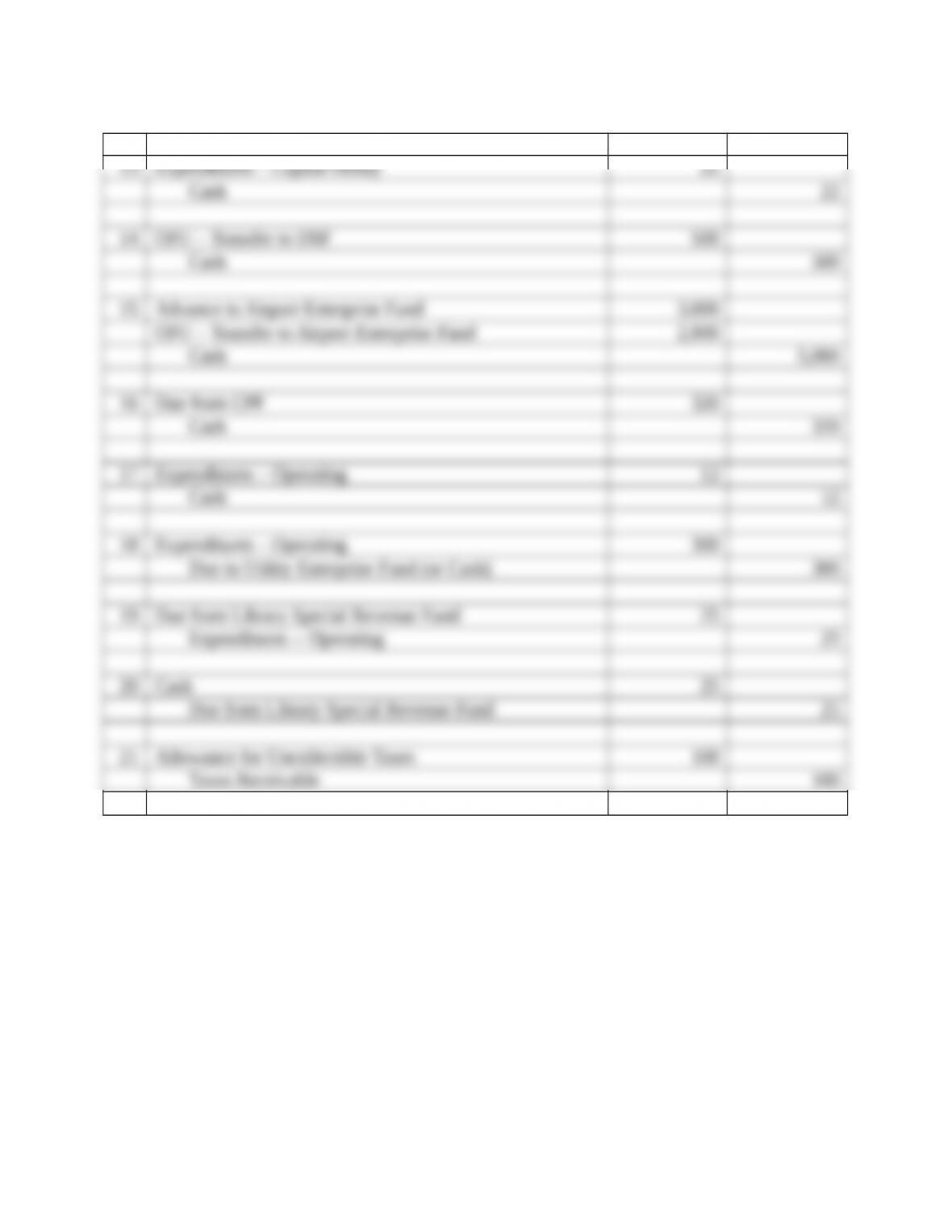

# Accounts Debit Credit

1 Taxes Receivable 10,000

Allowance for Uncollectible Taxes (3% x 10,000) 300

9

Copyright © 2013 Pearson Education, Inc.

# Accounts Debit Credit

10

Copyright © 2013 Pearson Education, Inc.