Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 7 – Other Interfund Transactions: Debt Refunding

Transactions:

The City of Armona has decided to refinance $8,000 of par value, general government, general

obligation bonds outstanding. The bonds had a related unamortized bond premium of $200. The

city issues $6,000 of refunding bonds and transfers $2,700,000 from the General Fund to the

Debt Service Fund. The city paid $8,700 from the Debt Service Fund into an irrevocable trust to

cover future payments on the original bonds.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, or OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

Answers:

#

Fund or

Nonfund

Accounts Accounts Debit Credit

1a DSF Cash 6,000

Problem 8 – Other Liability Transactions

71

Copyright © 2013 Pearson Education, Inc.

Assume that the fiscal year-end for all the transactions below is June 30.

Transactions:

1. The General Fund paid $12 to a Special Revenue Fund to repay it for General Fund

employee salaries that were inadvertently recorded as expenditures in the Special

Revenue Fund.

2. The government decided to settle a lawsuit on the advice of its legal counsel. The lawsuit

came about because of damage to a citizen’s property caused by a garbage service

employee. The garbage operation is accounted for in the General Fund. The government

settled the suit for $300, paying $100 on June 1, 20X1, and $50 on August 1 for each of

the next 4 fiscal years. For these types of lawsuits, the government is self-insured for the

first $50 and 100% insured for the remaining payments. Because of a cash flow issue,

the government borrowed $200 on a 6 month, 3% note that comes due 2 months after

year-end. No money was received from the insurance company by year-end, but the total

amount due was expected by August 15. Prepare all journal entries required through the

end of the 20X1 fiscal year.

3. The government’s employees earned $25 in compensated absences during the year. Of

this amount, $10 was paid during the year and another $8 will be paid in the first 45 days

of the following fiscal year. In addition, $5 due at the end of last year was paid at the

beginning of this year.. Finally, $3 earned in earlier years was paid this year.

4. The actuarial amount owed to the government’s OPEB Plan for the year is $20,000. Of

this amount, only $5,000 – the approximate amount of retiree healthcare costs paid for

the year – was paid to the plan. The balance will be paid in later years.

Requirement: Prepare the general journal entries using standard fund-type terminology,

identifying the fund or nonfund accounts for which the entry is being prepared.

Appropriate abbreviations are acceptable (e.g., GF, SRF, CPF, DSF, GCA, GLTL,

OFS, OFU). If no entry is required, write “No Entry Required” and briefly

explain why. Do not include formal entry explanations or dates, but include any

important assumptions made and all calculations.

Answers:

72

Copyright © 2013 Pearson Education, Inc.

#

Fund or

Nonfund

Accounts Accounts Debit Credit

1a GF Expenditures – Operating 12

Cash 12

Copyright © 2013 Pearson Education, Inc.

Problem 9 – General Capital Assets Note Disclosure

The general capital assets balances for the City of Sugarland as end of the December 31, 20X1

fiscal year are:

Nondepreciable Capital Assets

Land............................................................................................................... 1,350

Construction in Progress................................................................................ 2,200

Depreciable Capital Assets

Buildings........................................................................................................ 16,500

Accumulated Depreciation....................................................................... 7,500

Infrastructure.................................................................................................. 186,000

Accumulated Depreciation....................................................................... 103,000

Vehicles.......................................................................................................... 8,500

Accumulated Depreciation....................................................................... 2,600

Equipment...................................................................................................... 3,450

Accumulated Depreciation....................................................................... 2,800

The following events related to the city’s capital assets occurred during fiscal year 20X2:

1. A pickup truck purchased for $30 was sold. It had accumulated depreciation of $21.

2. Land purchased many years ago for $140 was sold.

3. A new police car was purchased for $50 (5 year useful life) as was a new fire truck for

$250 (10 year useful life). Both were purchased at the beginning of the fiscal year.

Depreciation on all new buildings, vehicles, and equipment is for the nearest full year,

using the straight-line method with zero salvage value.

4. A new civic center was started in the previous fiscal year. Costs were $2,200 in the

previous year. It cost $2,800 to finish it in the current fiscal year. The center was ready

for use just in time for a Christmas pageant on December 20, 20X2.

5. New roads costing $550 were built during the year. Depreciation on new roads starts the

following fiscal year.

6. Depreciation expenses for FY 20X2 on capital assets on hand at the beginning of the year

are: Building, $500; Infrastructure, $2,500; Vehicles, $415; and Equipment, $200.

7. Depreciation on all capital assets except infrastructure is allocated to government

functions as follows: general government, 30%; public safety, 50%; streets and roads,

20%. Infrastructure depreciation is charged to the function responsible for maintaining it.

Requirement: Using the information presented above, complete the general capital asset note

disclosure for FY 20X2. Note, the incomplete note is in this Excel file:

Ch09P-9.xlsx

Answers: The solution is in this Excel File: Ch09P-9S.xlsx

74

Copyright © 2013 Pearson Education, Inc.

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 10

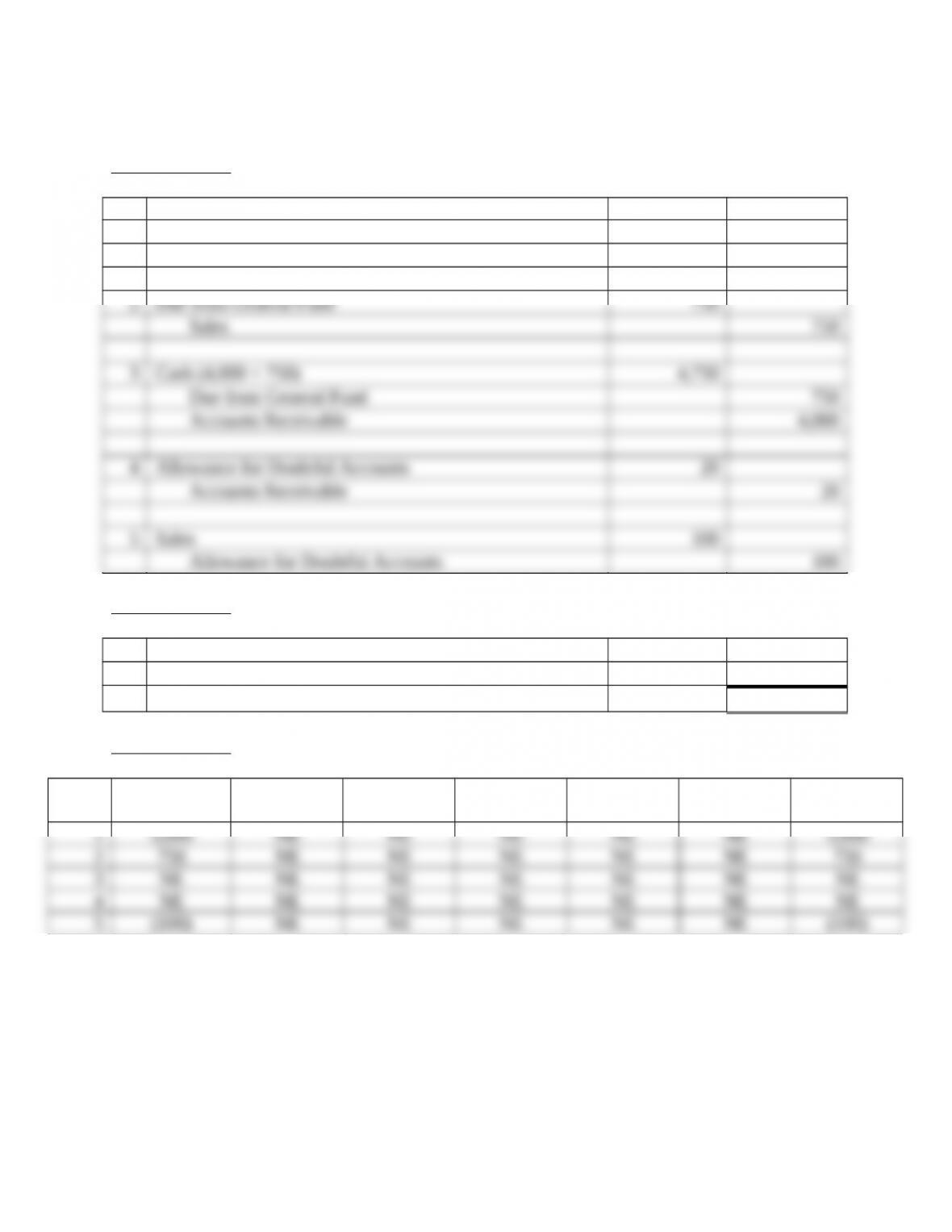

Problem 1 – Enterprise Fund Transactions

Listed below are selected transactions for the Rhea County Garbage Service, which is accounted

for in an Enterprise Fund. All amounts are in thousands of dollars.

Transactions:

1. Services of $5,000 were provided and billed to outside customers.

2. Services of $750 were provided and billed to the General Fund.

3. $750 was collected from other funds, and $4,000 was collected on account.

4. $20 of accounts receivable were written off as uncollectible.

5. Estimated bad debts for the year were $100.

Requirements:

4. Prepare the journal entries required in the Enterprise Fund. If no entry is required, state

“No entry required” and explain why.

5. Compute the amount of sales revenues that should be reported for the Enterprise Fund.

6. Indicate the effects of each transaction on the accounting equation of the Enterprise Fund

accounts. If an element of the equation is not affected or if the net effect is zero, put

“NE” in the appropriate box.

75

Copyright © 2013 Pearson Education, Inc.

Answers:

Requirement #1

# Accounts Debit Credit

1 Accounts Receivable 5,000

Sales 5,000

Requirement #2

Gross Sales (5,000 + 750) 5,750

Less Increase in Allowance for Doubtful Accounts 100

Net Sales 5,650

Requirement #3

Trans

#

Current

Assets

Noncurrent

Assets

Deferred

Outflows

Current

Liabilities

Noncurrent

Liabilities

Deferred

Inflows

Net

Position

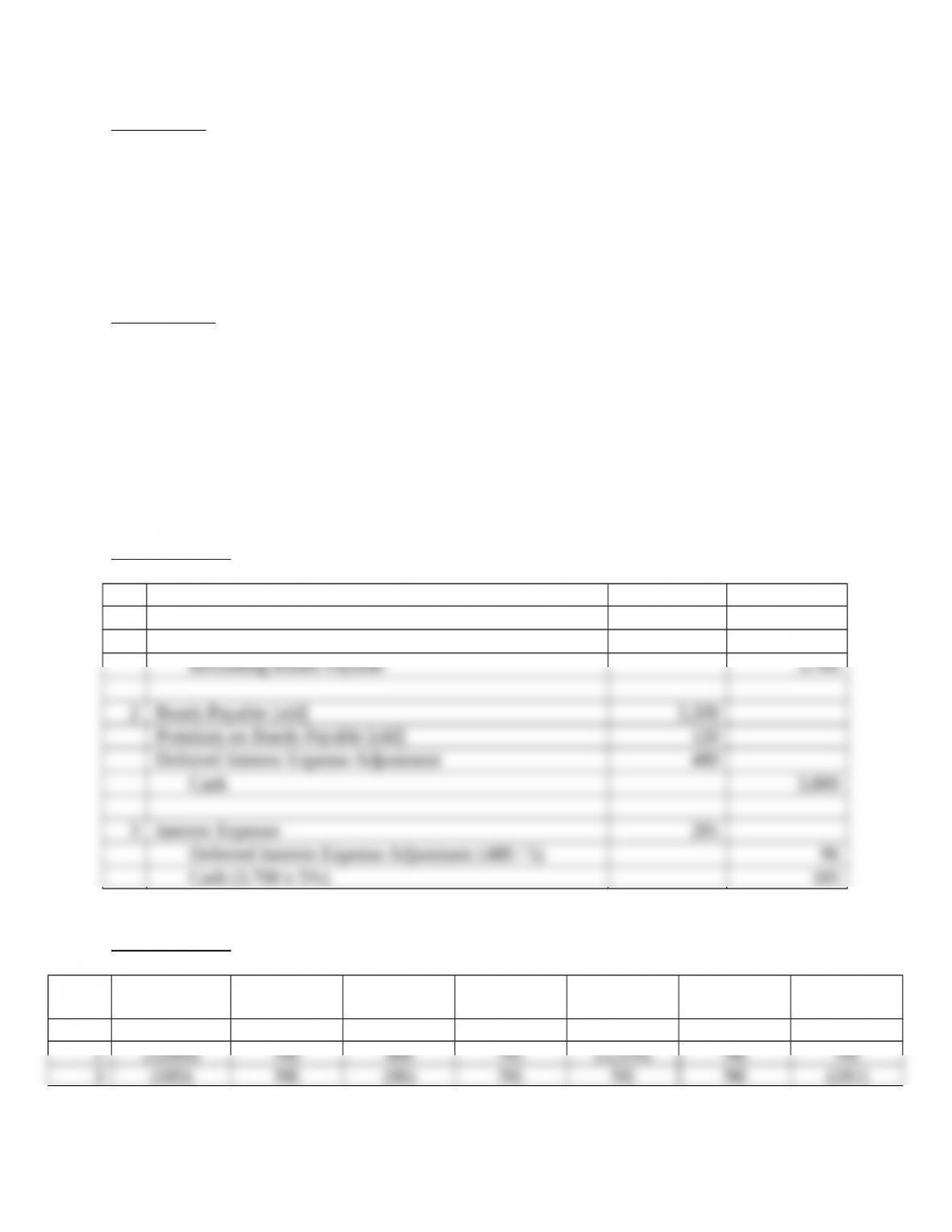

Problem 2 – Advance Refunding of Debt

Dayton County decided to refund an outstanding term bond issue in its Enterprise Fund. The old

bonds have a par value of $3,200 and an unamortized premium of $120. These bonds are

scheduled to mature in 6 more years.

76

Copyright © 2013 Pearson Education, Inc.

Transactions:

1. On January 2, 20x2, the County issued refunding bonds at par, $3,700. The bonds bear

interest at 5% payable annually and mature in five years. The bond issuance costs were

$250.

2. On January 2, The County paid $3,800 into an irrevocable trust in order to defease in

substance the previously outstanding bonds payable of the Enterprise Fund.

3. The annual interest payment on the new bonds was made on December 31 when due.

Requirements:

1. Prepare the journal entries required in an Enterprise. If no entry is required, state “No

entry required” and explain why.

2. Indicate the effects of each transaction on the accounting equation of the Enterprise Fund

accounts. If an element of the equation is not affected or if the net effect is zero, put

“NE” in the appropriate box.

Answers:

Requirement #1

# Accounts Debit Credit

1 Cash 3,450

Expenses – Bond Issue Costs 250

Requirement #2

Trans

#

Current

Assets

Noncurrent

Assets

Deferred

Outflows

Current

Liabilities

Noncurrent

Liabilities

Deferred

Inflows

Net

Position

1 3,450 NE NE NE 3,700 NE (250)

77

Copyright © 2013 Pearson Education, Inc.

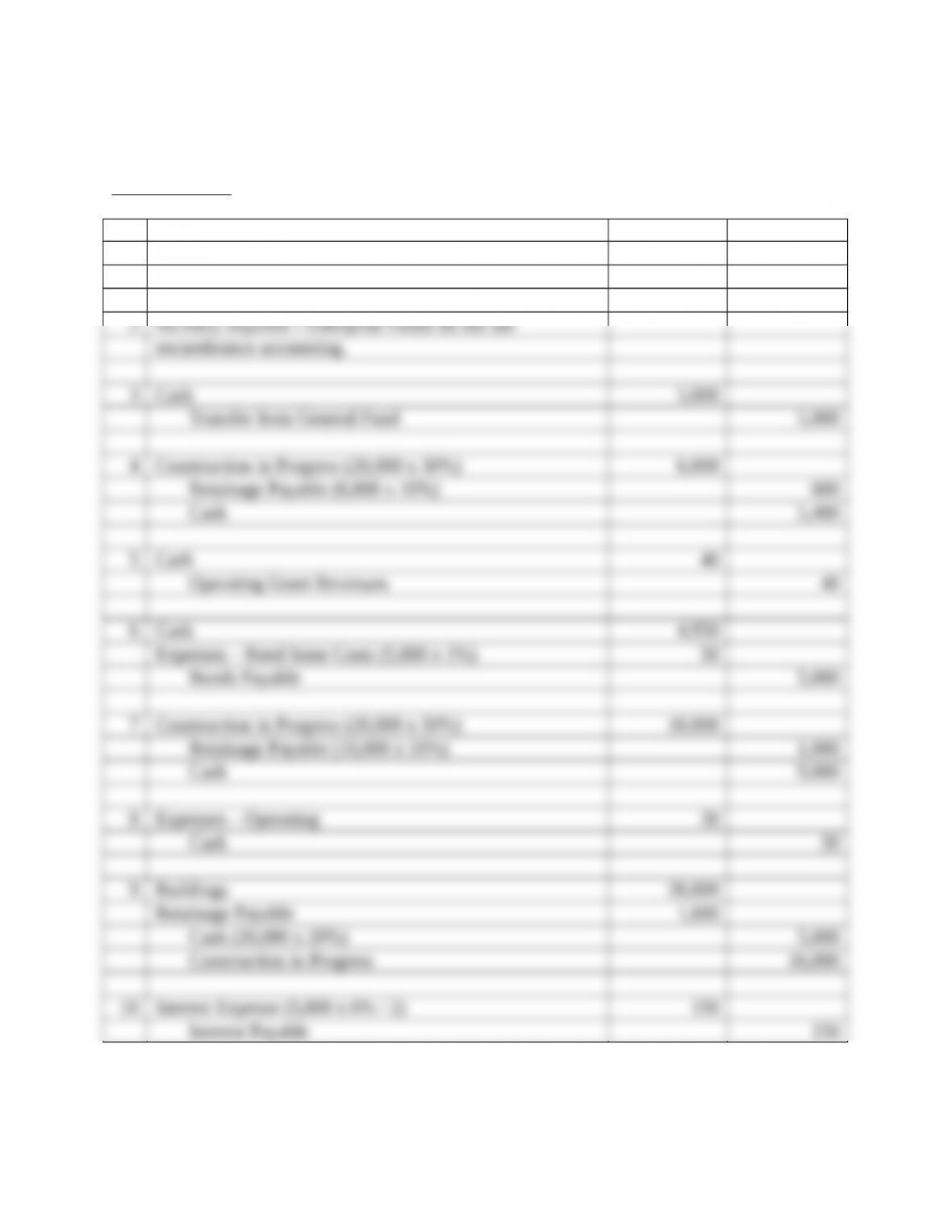

Problem 3 – Grant Accounting and Reporting

Over the course of one year, Obed County received two grants:

$10,000 grant (in cash) to be used to finance half the cost of expanding the town’s water

treatment plant. All eligibility requirements have been met.

$40 grant to educate users on water conservation measures and to monitor water usage by

a study group.

Transactions:

1. Received the grant to assist in expanding the water treatment plant.

2. Signed a contract with Swann & Hall Construction to build the water treatment plant

expansion, $20,000. The construction project is expected to take less than one year.

3. Received a $5,000 transfer from the General Fund to cover part of the cost of expanding

the treatment plant.

4. Received an invoice from S&H Construction for 30% of the project. Paid the contractor

the invoiced amount less a 10% retainage.

5. Received the grant to do the water study.

6. Issued $5,000 in bonds at mid-year at par to provide part of the financing for the

treatment plant expansion. The bond issue costs were 1% of the face value. The bonds

bear interest at 6%, payable semiannually.

7. Received a second invoice for 50% of the project. Paid the contractor the invoiced

amount less a 10% retainage.

8. Expenses incurred and paid during the year under this second grant total $30.

9. Received the final invoice from the contractor. The expansion project was finished on-

time and in accordance with the contract. Paid the contractor all amounts owed.

10. Make any necessary year-end adjusting entries.

Requirements:

1. Prepare the journal entries required in an Enterprise. If no entry is required, state “No

entry required” and explain why.

2. Indicate the effects of each transaction on the accounting equation of the Enterprise Fund

accounts. If an element of the equation is not affected or if the net effect is zero, put

“NE” in the appropriate box.

3. How would these grants be reported in the statement of revenues, expenses, and changes

in net position of the Enterprise Fund?

4. Assuming year-end had occurred after transaction #4, how would the grant and transfer

affect the Statement of Net Position for the Enterprise Fund.

78

Copyright © 2013 Pearson Education, Inc.

Answers:

Requirement #1

# Accounts Debit Credit

1 Cash 10,000

Capital Contributions 10,000

79

Copyright © 2013 Pearson Education, Inc.

Requirement #2

Trans

#

Current

Assets

Noncurrent

Assets

Deferred

Outflows

Current

Liabilities

Noncurrent

Liabilities

Deferred

Inflows

Net

Position

1 10,000 NE NE NE NE NE 10,000

Requirement #3

Requirement #4

Problem 4 – Preparation of the Statement of Cash Flows

The following transactions occurred in the City of Jimtown Enterprise Fund:

1. Equipment belonging to the Enterprise Fund was sold for $300.

2. The proceeds from the sale of the asset were transferred to the General Fund.

3. Cash, $2,800, was paid for construction costs. The cash was paid out of unrestricted cash

available for any Enterprise Fund purpose—i.e., was not set aside strictly for capital asset

construction or acquisition.

4. Paid principal, $18, and interest, $59, on a mortgage note.

5. The Enterprise Fund collected $12,500 from external customers and $2,500 from the

General Fund for services.

6. The City signed a lease for equipment. The present value of the future payments and fair

value of the equipment is $5,000, and the City made a down payment of $500

7. Proceeds of bonds issued to refund previously outstanding bonds which had been issued

to finance plant expansion several years earlier, $18,000.

8. Interest paid on the refunding bonds, $1,080.

9. Cash proceeds from sale of investments, $900. Investments were purchased with the

proceeds of debt issued to finance construction of specialized equipment that is almost

completed.

80

Copyright © 2013 Pearson Education, Inc.