Problem 3 –

The following information was derived from the accounts and records of Mockingbird State

University for 20X3. All amounts are in thousands of dollars.

Tuition and fees

Total assessed…………………………………………………………………………………………. $4,000

Expected uncollectible…………………………………………………………………….…….… 80

Appropriations

State………………………………………………………………………………………………………. 800

Auxiliary enterprises

Sales………………………………………………………………………………………….…….……. 500

Salaries……………………………………………………………………………………………..…… 280

Other expenses…………………………………………………………………………………….…. 140

Endowment income

Restricted to research………………………………………………………………………..….…. 370

Private gifts and grants

Restricted to student scholarships……………………………………………………….….…. 0,200

Restricted to plant expansion……………………………………………………………….…… 2,000

Unrestricted………………………………………………………………………………………….… 180

Expenses:

Instruction………………………………………………………………………………..……….…… 3,100

Research………………………………………………………………………………………….….…. 600

Student services………………………………………………………………….…….…….……... 220

Institutional support…………………………………………………………………..…….……… 190

Operation of plant…………………………………………………………………….….…….…… 180

Mortgage payment ($10,000 interest)…………………………………………………………..…. 15

Scholarships allowances……………………………………………………………..…….…….……. 200

Net positon, January 1, 20X3…………………………………………………………………………. 3,827

Mockingbird State University reports as a special purpose government engaged only in business-

type activities.

Requirement: Prepare a statement of revenues, expenses, and changes in net position for

Mockingbird State University for 20X3.

131

Copyright © 2013 Pearson Education, Inc.

Answer:

Mockingbird State University

Statement of Revenues, Expenses, and Changes in Net Position

For the Year Ended December 31, 20X3

Revenues

Operating Revenues

132

Copyright © 2013 Pearson Education, Inc.

Problem 4 – College & University Annuity Gift Transactions

Dogwood State University is a government university that reports as a special government

engaged only in business-type activities. Listed below are selected transactions that affect its

annuity gifts. All amounts are in thousands of dollars.

Transactions:

1. At the beginning of the year, the college receives cash of $200 with a stipulation that the

donor be paid $25 a year for 10 years. The present value of the payment to the donor is

$175.

2. Investments in the amount of $195 are purchased.

3. Payments of $25 are made to the donor at year end.

4. Investment income of $13 is received during the year.

5. The present value of the annuity payable to the donor at year end was $162.

Requirement: Prepare the necessary journal entries to record these transactions.

Answers:

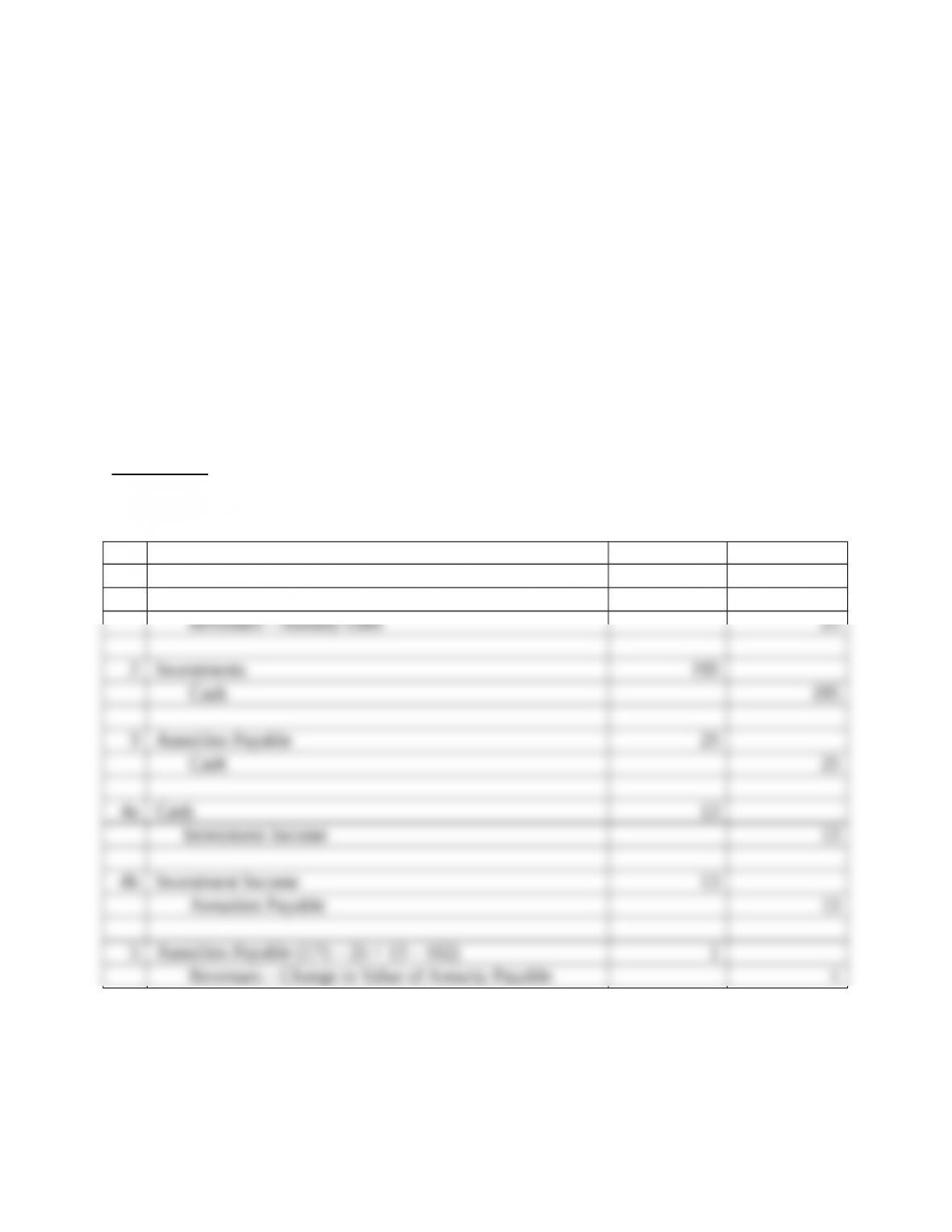

# Accounts Debit Credit

1 Cash 200

Annuities Payable 175

Governmental and Nonprofit Accounting: Theory and Practice, 10e (Freeman)

Problems – Chapter 18

133

Copyright © 2013 Pearson Education, Inc.

Problem 1 – Government Hospital Journal Entries

Listed below are selected transactions from the City of Watertown Hospital. All amounts are in

thousands of dollars.

Transactions:

1. The hospital provided patient services during the year that had standard charges of

$12,500. Contractual adjustments awarded to patients under contracts with insurance

companies and under government programs totaled $2,000. Uncollectible accounts are

expected to be approximately $800.

2. Nursing and other professional salaries paid during the year totaled $2,300.

3. Depreciation for the year was $500 for the building and $900 for equipment.

4. Medical supplies costing $2,600 were purchased during the year. The inventory of

supplies increased from $200 at the beginning of the year to $300 at year end.

5. The hospital received a $4,000 to be used for the purchase of specialized diagnostic

equipment.

6. The hospital received a $500 gift to be used for providing specialized coronary care

services to patients.

7. The hospital purchased $2,000 of diagnostic equipment with the donation received for

that purpose.

8. The hospital incurred $400 of operating expenses for the care of coronary patients

consistent with the purposes of that donation.

9. The hospital issued $5,000 of 20-year, 8% bonds at par at mid-year to finance a new

addition for the hospital.

10. The hospital estimates that malpractice claims against the hospital of $400 ultimately will

result in liabilities of $100 that will have to be paid–but probably will not have to be paid

during the next fiscal year.

Requirement: Prepare the journal entries required of a government hospital for these

transactions.

134

Copyright © 2013 Pearson Education, Inc.

Answers:

135

Copyright © 2013 Pearson Education, Inc.

# Accounts Debit Credit

1a Accounts Receivable 12,500

# Accounts Debit Credit

136

Copyright © 2013 Pearson Education, Inc.

Problem 2 – Hospital Reporting Discussion Questions

Briefly answer the following questions on hospital reporting:

1. Identify the financial statements that must be presented for a government hospital.

2. How are the financial statements for a government hospital different from the financial

statements for a not-for-profit hospital?

Answers:

1. The required statements for a government hospital are:

Statement of Net Position

Statement of Revenues, Expenses, and Changes in Net Position

Statement of Cash Flows

2. Although there are many similarities among the financial statements for a government

hospital and a not-for-profit hospital, the key differences are:

Net assets for not-for-profit hospitals are classified as unrestricted, temporarily

restricted, and permanently restricted. Net position for government hospitals are

classified as unrestricted, restricted, and net investment in capital assets.

Not-for-profit hospitals report a statement of operations and a statement of changes in

net assets. Government hospitals report a statement of revenues, expenses, and

changes in net position.

Not-for-profit hospitals report changes in all three categories of net assets.

Government hospitals report only changes in total net position.

Not-for-profit hospitals report assets released from restrictions. Government hospitals

do not report assets released from restrictions.

Not-for-profit hospitals follow FASB cash flow statement guidance (three sections).

Not-for-profit hospitals may prepare the statement using either the indirect method or

the direct method. Government hospitals follow GASB cash flow statement guidance

(four sections). Government hospitals must prepare the statement using the direct

method.

Government hospitals defer revenue recognition on reimbursement grants until

qualifying costs are incurred. Nongovernment, not-for-profit hospitals do not.

137

Copyright © 2013 Pearson Education, Inc.

Problem 3 – Government Hospital Financial Reporting

The following selected information is taken from the accounting records of the Jackson County

Hospital for fiscal year 20X0. All accounts have a normal balance and are listed in alphabetical

order. Also, all amounts are in thousands of dollars.

Administrative expenses…………………………………………………………………….…….…… $440

Cafeteria sales…………………………………………………………………………………..…….…… 440

Charity services (at gross amounts) …………………………………………………….…….…… 500

Contractual adjustments………………………………………………………………………………… 1,100

Depreciation—Building………………………………………………………………………….….…. 1,400

Depreciation—Other…………………………………………………………………………………..… 2,740

Estimated uncollectible accounts……………………………………………………………..…….. 710

Federal grant restricted for heart research (all eligibility requirements met)............ 1,300

Fiscal service expenses………………………………………………………………….….…….……. 300

Gain on sale of capital assets………………………………………………………….….…….……. 75

General services expenses……………………………………………………………………………… 1,100

Gross patient service charges…………………………………………………………………..….…. 18,000

Income from investments of endowment—donor restricted to heart research…....... 870

Other professional services expense…………………………………………………..….…….…. 890

Net investment in capital assets, January 1………………………………………………………. 15,000

Nursing services expense………………………………………………………………………..….…. 8,000

Proceeds from bond issue for building addition………………………………..….…….……. 22,000

Restricted net position, January 1………………………………………………………..…….…… 3,200

State appropriations—capital……………………………………………………………………….… 700

State appropriations—operating…………………………………………………..…….…….……. 500

Unrestricted contributions……………………………………………………………………………... 350

Unrestricted net position, January 1………………………………………………………………… 9,000

138

Copyright © 2013 Pearson Education, Inc.