15. Assume that a Debt Service Fund does not have nonspendable fund balance. Further assume

that after restricted and committed levels of fund balance have properly identified, the

remaining balance is a deficit. This deficit fund balance should

A. Be reported as negative assigned fund balance.

B. Be reported as a negative unassigned fund balance.

C. Be reported as a negative nonspendable fund balance.

D. Be netted against the positive committed fund balance.

16. A special tax has been levied by the city council in a formal vote. This new revenue source

has been set aside for debt service purposes. This revenue source would most likely impact

A. Restricted fund balance.

B. Committed fund balance.

C. Assigned fund balance.

D. Unassigned fund balance.

17. The residual fund balance classification for a Debt Service Fund is

A. Unassigned.

B. Restricted.

C. Assigned

D. Committed.

18. A Debt Service Fund retires bond principal during the year that is not related to a defeasance.

The entry necessary to reflect the principal retirement would be

A. Debit bonds payable and credit cash.

B. Debit other financing use and credit cash.

C. Debit expenditures and credit cash.

D. Debit other financing source and credit cash.

19. Which of the following would not be a likely financial resource for a Debt Service Fund?

A. Property taxes.

B. Sales tax.

C. Transfers from the General Fund.

D. Proceeds from the sale of capital assets.

20. If cash from the General Fund is transferred to a Debt Service Fund, the entry in the Debt

Service Fund would

A. Debit cash and credit revenues.

B. Debit cash and credit other financing sources.

C. Debit cash and credit accounts receivable.

D. Debit cash and credit fund balance.

71

21. If a special tax is levied to finance debt service for a particular debt issue, the entry to record

the levy in the Debt Service Fund would be

A. Debit Taxes Receivable and credit to Revenues.

B. Debit Taxes Receivable and credit to Other Financing Sources.

C. Debit Prepaid Assets and credit to Revenues.

D. Tax levies may not be reported in a Debt Service Fund.

22. In the fiscal year ended September 30, 20X9, debt service payments were made in January

and July from the Debt Service Fund in the total amount of $25,000 ($10,000 principal,

$15,000 interest). The sole financial resource for the debt service payments are the proceeds

of a special debt service tax levy. The taxes are paid in increments of about $27,000 and are

due in June of each year. For the fiscal year ended September 30, 20X9, assuming $24,000 of

taxes had been collected for this fiscal year, the expenditures reported in the Debt Service

Fund would be

A. $10,000.

B. $15,000.

C. $24,000.

D. $25,000.

24. ?

A. A balance sheet.

B. A statement of cash flows.

C. A budget-to-actual statement.

D. A statement of revenues, expenditures, and changes in fund.

25. If General Fund cash is transferred to a Debt Service Fund to provide resources to refund

outstanding debt, the Debt Service Fund statement of revenues, expenditures, and changes in

fund balance would report

A. An other financing source when the cash is received.

B. An other financing use when the cash is used to refund the outstanding debt.

C. A revenue.

D. A special item for the difference in the amount received and the amount paid.

72

26. A government has $3,000,000 of 6%, 10-year general obligation bonds outstanding. The

bonds were issued on November 1, 20X8 to finance construction of a general capital asset.

Interest is payable semiannually on October 31 and April 30. What amount of debt service

expenditures should the government report for the year ended December 31, 20X8?

A. $0.

B. $30,000.

C. $90,000.

D. $180,000.

27. A government has $3,000,000 of 6%, 10-year general obligation bonds outstanding. The

bonds were issued on July 2, 20X7 to finance construction of a general capital asset. Interest

is payable semiannually on January 1 and July 1. What is the minimum amount of interest

expenditures that the government would be permitted to report on the bonds for 20X7?

A. $0

B. $30,000

C. $90,000

D. $180,000

28. A government has $3,000,000 of 6%, 10-year general obligation bonds outstanding. The

bonds were issued on July 2, 20X7 to finance construction of a general capital asset. Interest

is payable semiannually on January 1 and July 1. What is the maximum amount of interest

expenditures that the government would be permitted to report on the bonds for 20X7?

A. $0.

B. $30,000.

C. $90,000.

D. $180,000.

29. A government has $1,000,000 of 6%, 10-year general obligation bonds outstanding. The

bonds were issued on August 15, 20X6 to finance construction of a general capital asset.

Interest is payable semiannually on February 15 and August 15. What is the maximum

amount of interest expenditures that the government would be permitted to report on the

bonds for 20X6?

A. $0.

B. $22,500.

C. $30,000.

D. $60,000.

73

30. A government has $1,000,000 of 6%, 10-year general obligation bonds outstanding. The

bonds were issued on November 1, 20X7 to finance construction of a general capital asset.

Interest is payable semiannually on November 1 and May 1. The bonds also require an

annual principal payment of $100,000 on May 1. What amount of debt service expenditures

should the government report for the year ended December 31, 20X8?

A. $60,000.

B. $90,000.

C. $160,000.

D. $190,000.

31. A government retired $5,000,000 of outstanding general obligation bonds when due. The

government used $3,000,000 of proceeds from new bonds issued to provide resources for

retiring the old bonds. The other $2,000,000 had been accumulated from tax and interest

revenues over the years that the old bonds were outstanding. The government should report

this transaction in its Debt Service Fund as

A. Other financing uses of $5,000,000.

B. Expenditures of $5,000,000.

C. Other financing uses of $3,000,000 and expenditures of $2,000,000.

D. Other financing uses of $2,000,000 and expenditures of $3,000,000.

32. A Debt Service Fund received an annual payment from the General Fund to finance

upcoming debt service payments. The amount received from the General Fund should be

reported in the Debt Service Fund statement of revenues, expenditures, and changes in fund

balance as

A. Other financing sources.

B. Revenues.

C. Proceeds from interfund loans.

D. Special item.

33. A Debt Service Fund received a $100,000 payment from the General Fund to finance

upcoming debt service payments. During the year, Debt Service Fund payments of $50,000

interest and $60,000 principal were made as they become due. The Debt Service Fund

statement of revenues, expenditures, and changes in fund balance should report

A. An excess of revenues over expenditures of $50,000.

B. An excess of expenditures over revenues of $10,000.

C. An excess of expenditures over revenues of $50,000.

D. An excess of expenditures over revenues of $110,000.

74

34. Debt Service Fund expenditures would include all of the following except

A. Fiscal agent fees.

B. Repayment of refunded bonds using resources transferred from the General Fund.

C. Principal retirement payments.

D. Discounts on refunding bonds.

35. Assume that a county with a June 30 fiscal year end levied $900,000 in special assessments

20X1. The levy is to be paid by the property owners over a 10 year period beginning in

January 20X2. The amount of revenue recognized by the county in the Debt Service Fund as

of June 30 20X1 would be

A. $900,000.

B. $90,000.

C. $0.

D. Tax and special assessment revenues are never recognized in a Debt Service Fund.

36. A Debt Service Fund should be used to account for debt service on special assessment

indebtedness

A. Always.

B. Unless the government is not obligated in any manner on the debt.

C. If the government is obligated in some manner for the debt.

D. Never. A Special Assessment Fund should be used.

37. Which of the following is not usually a requirement of a Debt Service Fund (DSF) for a term

bond issue?

A. The DSF should be used to accumulate the necessary funds to pay the term bonds when

they come due.

B. The DSF makes period interest payment on the debt during its life.

C. The DSF will have funded reserves as required by the debt covenant.

D. A DSF that services a term bond issue has no requirements that distinguish it from a DSF

that services serial bonds.

75

38. In the year that a governmental entity enters into a legal advance refunding, which of the

following note disclosures would not be required?

A. The present value of the net debt service savings or cost of advance refunding

transaction.

B. The amount of defeased debt that is still outstanding.

C. The difference between total of the remaining debt service requirements of the old

defeased issue and the total debt service requirements of the new issue, adjusted for any

additional cash received or paid.

D. General description of the transaction.

39. The City of Newport issued $1,500,000 of general obligation refunding bonds at a 2%

premium. Bond issuance costs of $15,000 were incurred. The proceeds, net of the premium

and bond issue costs, are being used to refund the outstanding bonds. Debt Service Fund

Expenditures will be debited for

A. $15,000.

B. $30,000.

C. $1,455,000.

D. $1,470,000.

40. The Village of Bakersville issued $700,000 of refunding bonds at a 1% premium. Bond

issuance costs were $10,000; $695,000 is to be used to retire the existing bonds. Other

financing uses will be debited for

A. $7,000.

B. $10,000.

C. $683,000.

D. $695,000.

41. Apex County advance refunded $3,000,000 of outstanding bonds. $2,500,000 was financed

with net refunding bond proceeds and the remaining $500,000 was transferred from the

General Fund. The county incurred $35,000 of bond issuance costs when issuing the

refunding bonds. Which of the following statements about the reporting of these transactions

in the Debt Service Fund is not true? The Debt Service Fund financial statements would

report

A. $2,500,000 of other financing uses.

B. Expenditures of $535,000.

C. Transfers in of $500,000.

D. Net other financing sources of $500,000.

76

42. A government defeased in substance $5,000,000 of outstanding general obligation bonds

several years prior to their maturity. The government paid $6,000,000 into an irrevocable

trust to accomplish the defeasance in substance. The payment included $3,000,000 of

proceeds from new bonds issued that were to provide resources for the bond defeasance. The

other $3,000,000 had been accumulated over previous years from taxes and interest earnings

in the Debt Service Fund. The government should report the payment into the irrevocable

trust from its Debt Service Fund as

A. Other financing uses of $6,000,000.

B. Expenditures of $6,000,000.

C. Other financing uses of $3,000,000 and expenditures of $3,000,000.

D. Other financing uses of $5,000,000 and expenditures of $1,000,000.

43. A government paid $6,000,000 into an irrevocable trust to be used to service $5,000,000 of

outstanding general obligation bonds, but the transaction does not meet the defeasance in

substance criteria. The payment included $3,000,000 of proceeds from a new bond issue that

was issued to provide resources for the old bond. The other $3,000,000 had been

accumulated over previous years from taxes and interest earnings in the Debt Service Fund.

The government should report this transaction in its Debt Service Fund as

A. Other financing uses of $6,000,000.

B. Expenditures of $6,000,000.

C. Other financing uses of $3,000,000 and expenditures of $3,000,000.

D. No expenditures or other financing uses should be reported.

1. Which of the following methods of capital asset valuation is not considered an acceptable

alternative under generally accepted accounting principles for a donated capital asset?

A. Original cost

B. Estimate cost

C. Fair market value

D. Book value to donor.

2. Assume that the city foreclosed on a piece of property with a fair market value of $5,000. It

has an assessed value for taxes of $4,000. The outstanding amount of taxes and penalties due

on the property totals $3,500. Normally, the city would value the foreclosed property at

A. $0.

B. $3,500.

C. $4,000.

D. $5,000.

77

Copyright © 2013 Pearson Education, Inc.

3. Which of the following comments best describes the accounting and financial reporting

guidelines for works of art and historical treasures?

A. Governments should capitalize works of art and historical treasures but should not

depreciate them unless they are considered exhaustible.

B. Works of art and historical treasures may be capitalized, but they should never be

depreciated under any circumstances.

C. Works of art and historical treasures that must be held for public exhibition, must be

protected, and the proceeds of any sales must be used to acquire more collections are

always capitalized and depreciated.

D. Works of art should only be valued historical cost at the time of receipt.

4. Which of the following capital assets would not be considered a general capital asset?

A. Land at the local municipal park

B. A highway bridge maintained by a city government

C. Infrastructure associated with the local water system

D. Public safety vehicles

5. The parks and recreation department, which is accounted for within the General Fund,

purchased a new athletic field mower at a cost of $25,000. The mower has an estimated

2 in the amount of

A. $0.

B. $5,000.

C. $10,000.

D. $25,000.

6. A government entered into a general government capital lease in the prior year. During the

current year, a lease payment of $50,000, which includes implicit interest of $12,000, was

made from the General Fund. What effect does the $50,000 payment have on the General

Capital Assets and General Long-Term Liabilities accounts?

A. Increases net investment in capital assets by $38,000.

B. Increases capital assets $50,000.

C. Increases capital assets by $38,000.

D. Decrease capital lease liability by $50,000.

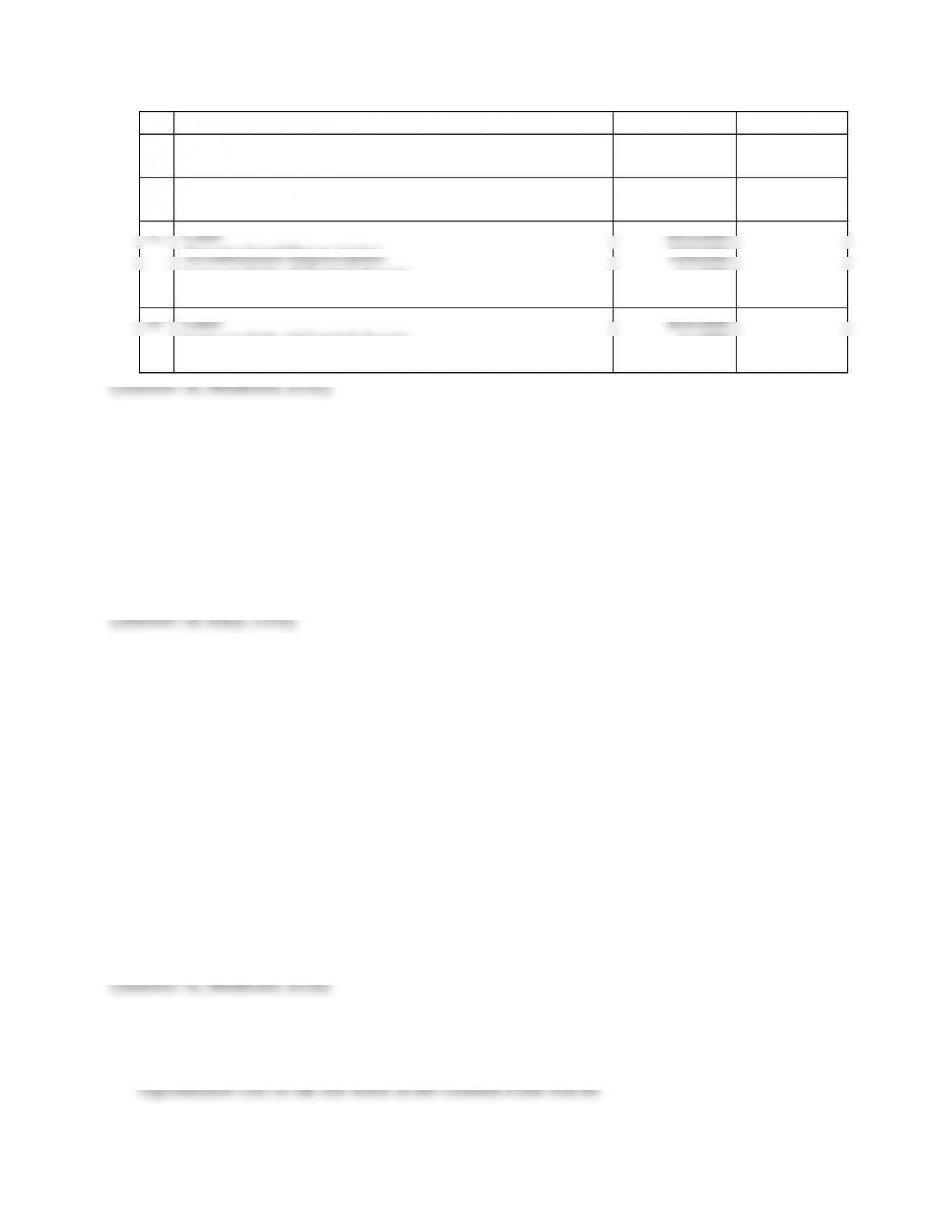

7. A county government sold two of its emergency vehicles for a total of $35,000. The vehicles

had a collective net book value of $46,000 (total original cost = $150,000; accumulated

depreciation = $104,000). The entry that would be made in the General Fund at the time of

78

Copyright © 2013 Pearson Education, Inc.

Debit Credit

A

.

Cash

Capital Contribution

$35,000

$35,000

B. Cash

Other Financing Sources – Sale of Capital Assets

$35,000

$35,000

Loss on Sale of Capital Assets

Capital Assets — Vehicles

11,000

$150,000

.

Loss on Sale of Capital Assets

Other Financing Sources – Sale of Capital Assets

11,000

$46,000

8. Assume that a governmental entity acquires a new garbage truck. The garbage truck costs

$189,000. The vendor allowed a $30,000 allowance with the trade-in of the entity’s old

garbage truck, which had a net book value of $42,000. The government financed the balance

with a short-term bank note. The new garbage truck would be recorded in the General Capital

Assets account at

A. $147,000.

B. $159,000.

C. $189,000.

D. $201,000.

9. New municipal building office equipment costs $400,000 and is being financed with a capital

lease. If the government makes a $40,000 down payment, which of the following best

describes the external financial reporting effects?

A. The General Fund statements will report expenditures of $400,000 and other financing

sources of $360,000. The General Long-Term Liabilities accounts will report a liability of

$360,000 and the General Capital Assets accounts will report an asset of $400,000.

B. The General Fund statements will report expenditures of $40,000 and other financing

sources of $360,000. The General Long-Term Liabilities accounts will report a liability of

$400,000 and the General Capital Assets accounts will report an asset of $360,000.

C. The General Fund statements will report expenditures of $360,000 and other financing

sources of $400,000. The General Long-Term Liabilities accounts will report a liability of

$360,000 and the General Capital Assets accounts will report an asset of $360,000.

D. The General Fund statements will report expenditures and other financing sources of

$40,000. The General Long-Term Liabilities accounts will report a liability of $360,000

and the General Capital Assets accounts will report an asset of $360,000.

10. A city recently ordered a new fire truck. The base cost of the truck is $250,000. In addition,

the city will be paying $1,000 in delivery charges and $5,000 for necessary calibrations once

it is delivered; and the city will also have the necessary logos added at a cost $2,500. The

79

Copyright © 2013 Pearson Education, Inc.

A. $0.

B. $251,000.

C. $256,000.

D. $258,500.

11. A local citizen donated land with a fair market value of $500,000 to the county government.

The donor had paid $550,000 for the land five years ago. The county incurred $150,000 in

development costs to convert the land into a public park. The county should capitalize the

new public park in the General Capital Assets accounts in the amount of

A. $500,000.

B. $550,000.

C. $650,000.

D. $700,000.

12. A local government purchased land to be used for a new city hall to be built within the next

five years. The purchase price was for the land’s fair value, $1,500,000. The government

financed the required $150,000 down payment by securing a short-term note with a local

lending institution. The remaining $1,350,000 was financed by issuing certificates of

participation. Costs incurred in issuing the certificates of participation totaled $60,000. The

land should be capitalized in the General Capital Assets account in the amount of

A. $1,350,000.

B. $1,410,000.

C. $1,500,000.

D. $1,560,000.

13. A bridge construction project, accounted for in a Capital Projects Fund, is in Year 2 of an

2, $1,530,000 of costs were incurred. What entry would be necessary in the General Capital

Assets accounts for Year 2?

Debit Credit

A

.

Capital Outlay

Cash

$1,530,000

$1,530,000

B. Construction in progress

Cash

$1,530,000

$1,530,000

C. Construction in progress

Net investment in capital assets

$1,530,000

$1,530,000

D

.

Construction in progress

Net investment in capital assets

$1,830,000

$1,830,000

80